Authors: Milena Barg, Anna-Maria Hausner, Berit Pippert, Christian von Hollen, Gero Vorwerck

Edited by: –

Last updated: October 8, 2025

Executive summary

Sustainability controlling extends traditional controlling by integrating social and ecological dimensions alongside economic goals. It supports management in planning, monitoring, and implementing sustainability strategies across all organizational levels.

The concept builds on classic controlling principles but adapts them to address climate change, resource scarcity, and societal expectations. It involves strategic and operational instruments, such as SWOT and materiality analyses, Sustainability Balanced Scorecards, and KPIs for ecological, social, and long-term economic performance.

Practical implementation requires embedding sustainability into corporate strategy, aligning processes, and leveraging IT systems for data transparency. Reporting and communication play a vital role in demonstrating progress and meeting stakeholder expectations.

Drivers include societal pressure, regulatory frameworks, and internal employee engagement, while barriers often stem from financial focus, lack of quantifiable metrics, and resistance to change. Overcoming these challenges ensures resilience and long-term success.

1 Definition and relevance

The definition of sustainability controlling does not differ essentially from the definition of classic controlling1Colsman, B. Nachhaltigkeitscontrolling: Strategien, Ziele, Umsetzung (Springer Gabler, 2016). which is to manage, plan and control all units of a business by processing and providing data and information.2Weber, J. Controlling. Gabler Wirtschaftslexikon. https://wirtschaftslexikon.gabler.de/definition/controlling-30235/version-370809 (2019). However, the function of controlling has expanded over the past years, according to Horváth, a renowned controlling expert:

“The controller […] is both a financial specialist and an internal consultant, [who] looks at the past as well as the future and characterizes proactive action and holistic communication. It is precisely this understanding of the role that is also required when implementing sustainability and the associated sustainability controlling. The topic of sustainability basically reinforces the development into a business partner of management”.3Horváth, P. & Berlin, S. Green-Controlling-Roadmap: Ansätze in der Unternehmenspraxis. in CSR und Controlling: Unternehmerische Verantwortung als Gestaltungsaufgabe des Controlling (eds. Günther, E. & Steinke, K.H.) 23-40 (Springer-Verlag Berlin Heidelberg, 2016).

As a result, a sustainability controller is the consistent development of the classic controller whose core area of responsibility is not changed by the topic of sustainability, but rather develops further. In view of the increasing danger of the climate crisis and with that decreased predictability and increased volatility, the implementation of sustainability in the core of controlling unit and thus in the controlling of an entire company is essential.1Colsman, B. Nachhaltigkeitscontrolling: Strategien, Ziele, Umsetzung (Springer Gabler, 2016).

Therefore, management tools that only focus on financial aspects become less useful and those that measure sustainability related social, ecological, and economic aspects gain relevance.4Initiative Neue Qualität der Arbeit. Führungskultur im Wandel (2014).

2 Background

Current trends but also factors that cannot be ignored, such as the climate crisis and societal problems, increasingly find their way into controlling activities. The core of current tasks r mains the same: support the corporate management in achieving the goals and take on the tasks of planning, management, and control.5Becker, W. & Ulrich, P. Handbuch Controlling. (Springer Gabler, 2022). This thematic introduction will briefly deal with the development of controlling and afterwards elaborate on the development towards sustainability controlling.

2.1 Controlling

Controlling activities were institutionalized in the USA in the 19th century as a consequence of the industrialization. At that time, controlling was responsible for internal accounting as well as internal control and ensured the cooperation with external accounting. In sum, controlling was seen as a collector of fiscal and financial variables. But over the course of time, controlling developed more and more into a business partner that supports and coordinates corporate management.6Horváth, P. Controlling (Vahlen, 2012).

There is no uniform definition of controlling but there are partly overlapping ones. Reichmann for example, sees controlling as a unit that provides targeted support to corporate management and uses various systems and instruments to obtain information, processes it and uses it for planning, coordination, and control. This should improve the quality of decision-making at all management levels.7Reichmann, T. Controlling mit Kennzahlen und Management-Tools: Die systemgestützten Controlling-Konzeption (Vahlen, 2011). Horváth, on the other hand, attributes a goal-oriented coordination function, which the practice accords. In his opinion, controlling has no authority to issue directives due to the organizational assignment, but it has primarily goal-oriented, information-supplying tasks. This information supply is increasingly extended by interpretation tasks that allow controlling to point out decision-making options.6Horváth, P. Controlling (Vahlen, 2012). The main tasks of this concept are considered to be useful and proven in practice.8Hubert, B. Controlling-Konzeptionen: Ein schneller Einstieg in Theorie und Praxis (Springer Gabler, 2018).

This means that the controller gives advice and is able to identify weaknesses and strengths. Sometimes the controller is described as a person who advises the captain of a ship how to steer in certain situations. For this reason, controlling should have a forward-looking view of alternative courses of action and weigh up their opportunities and risks before providing management with advice on how to achieve the company’s goals. This also implies that as a first step, it is necessary to set targets and then secondly the course to reach it becomes relevant.1Colsman, B. Nachhaltigkeitscontrolling: Strategien, Ziele, Umsetzung (Springer Gabler, 2016).

Classically, the main goal of a company should be the long-lasting existence by profit generation. For this purpose, a company should meet the needs of the target group, in the best case better than its competitors. Derived from this, the individual business units are often given different time-based targets, which are divided into short-, medium- or long-term targets.1Colsman, B. Nachhaltigkeitscontrolling: Strategien, Ziele, Umsetzung (Springer Gabler, 2016).

The classic division in controlling consists of a strategic unit with a long-term planning horizon and an operational unit with a short to medium-term planning horizon. Strategic controlling supports strategic management and deals with the further development and safeguarding of success potentials and points out the way towards new ones. It also focuses on potential opportunities and risks. The tasks relate to long-term planning and control, coupled with a strategic supply of information that provides strategic management with advice and direction. Operational controlling, on the other hand, is concerned with assessing suitability of certain procedures for achieving the overriding goals. It acts as a link between profitability and planning and takes countermeasures in the event of deviations from the planning.9Wellbrock, W. Nachhaltigkeitscontrolling: Instrumente und Kennzahlen für die strategische und operative Unternehmensführung (Springer, 2020).

2.2 Sustainability management

In the broader sustainability debate, the purely economic focus of corporate objectives is being increasingly criticized. As a result, there is growing pressure on companies to address besides economic factors also social and ecological issues and to integrate them into their business activities. Companies are an integral part to contribute to the transformation towards a sustainable society. According to this, it is important that the company creates an individual understanding and interpretation of sustainability as basis for their Sustainability Management. At first, the company should be aware about the meaning of ‘sustainability’. The most common definition of sustainability, the Brundtlandt-Definiton states that „sustainable development is a development that meets the needs of present generations without compromising the ability of future generations to meet their own needs”.10World Commission on Environment and Development. Our Common Future. (1987). This definition gives a clear understanding of the term, but it is hard to derive any guiding principle for a company from that. Additionally, the company should set up an idea how to implement sustainability into the management sphere. To facilitate the implementation in companies, there are existing guidelines. Individual characteristics of sustainability management implementation according to the company’s situation can be derived from that. Establishing a concept of sustainability management can be seen as the first component of a Sustainability Controlling.1Colsman, B. Nachhaltigkeitscontrolling: Strategien, Ziele, Umsetzung (Springer Gabler, 2016).

To be dedicated to sustainability, a company should implement in its management activities all three dimensions of sustainability – the social, environmental, and economic. Therefore, we can define Sustainability Management as all activities of a company to develop, design and control sustainable economic development in harmony with the ecological and social spheres and emphasize that the needs of the present generation do not deprive the desires and needs of future generations.11Wördenweber, M. Nachhaltigkeitsmanagement: Grundlagen und Praxis unternehmerischen Handelns (Schäffer-Poeschel Verlag, 2017).

According to the economic dimension of sustainability, a long-term increase in value is desirable which does not bring disadvantages for future generations. To this end, the generation and thus also the company should not live beyond its means. According to the ecological view of sustainability, the basic assumptions are to preserve nature, ergo the basis of life. Consequently, business activities should not contribute to the destruction of natural ecosystem services, preserve habitats, and be considerate of resources. The social dimension of sustainability includes for example social justice, the organization of communities, the safeguarding of basic needs and equal opportunities in general.9Wellbrock, W. Nachhaltigkeitscontrolling: Instrumente und Kennzahlen für die strategische und operative Unternehmensführung (Springer, 2020).

In this way, the awareness of assuming corporate social responsibility can be strengthened and pursued within the company. This requires clear objectives of a desirable condition which should be developed, communicated, and pursued within the framework of sustainability management. For this purpose, instruments and concepts should be integrated into the organization that promote an improvement in all three sustainability dimensions. However, implementation alone is not enough to do justice to corporate social responsibility. Rather continuous efforts are required to anchor sustainable action in the firm structures and processes of the company.12Weissenberger-Eibl, M. A.& Braun, A. Nachhaltige Unternehmensentwicklung. In Nachhaltiges Management (eds. Englert, M. & Ternés, A) 249-270 (Springer Gabler, 2019).

Sustainability management can be understood in two ways, namely functionally and institutionally. The functional understanding is that sustainability management should shape the company in such a way that sustainable corporate development results from the pursuit of social, ecological, and economic goals which contribute to a sustainable society. Sustainability management understood institutionally, means that diverse corporate actors come together and add social and ecological action to the existing economic dimension in the company’s strategy.13Sailer, U. Nachhaltigkeitscontrolling: Was Controller und Manager über die Steuerung der Nachhaltigkeit wissen sollten (UTB, 2020). A key event is therefore the embedding of sustainability in the normative corporate level. The vision and mission of the company should also provide for sustainable development for the holistic course. Only appropriate guidelines of the enterprise bring the necessary identification for all stakeholders as well as the determination of the company’s action and an exact goal guidance.9Wellbrock, W. Nachhaltigkeitscontrolling: Instrumente und Kennzahlen für die strategische und operative Unternehmensführung (Springer, 2020).

If a company is willing to incorporate all sustainability dimensions into its actions, it can begin to specify its sustainability management. Then, existing concepts can be used in addition to the company’s own definitions about sustainability and the management of it. These general templates can be individually adapted to the corporate’s requirements. The publishers of these templates differ, as do their approaches. For example, there are concepts from foundations, associations of states, organizations and certification agencies that facilitate the implementation of sustainability management.13Sailer, U. Nachhaltigkeitscontrolling: Was Controller und Manager über die Steuerung der Nachhaltigkeit wissen sollten (UTB, 2020). These conceptual frameworks and instruments (chapter 3.3) make it easier to link global ecological and social requirements and the actions of an individual company. In conclusion, a sustainability management concept should break the exclusively financially focused management control of organizations and provide goals as well as approaches to achieve this desired sustainability targets.13Sailer, U. Nachhaltigkeitscontrolling: Was Controller und Manager über die Steuerung der Nachhaltigkeit wissen sollten (UTB, 2020).

2.3 Objectives of sustainability controlling

Based on the understanding of controlling (chapter 2.1) and sustainability management in chapter 2.2, its objectives need to be specified. Whereas controlling in its conventional mode of operation has mainly focused fiscal and financial figures, sustainability controlling addresses the issues of the social and ecological dimension which arise from the derived goals of sustainability management. The actual task of controlling has therefore not changed but has been adapted in its depth and breadth. Sustainability controlling supports and advises corporate management in the integration of sustainability goals as defined at the various levels of sustainability management. In addition, controlling considers strategic and operational time horizons in planning and control. Based on the defined normative level of sustainability, controlling supports the company in its strategic positioning and derives a roadmap for the operational level.9Wellbrock, W. Nachhaltigkeitscontrolling: Instrumente und Kennzahlen für die strategische und operative Unternehmensführung (Springer, 2020). The expansion of the tasks is accompanied by increased complexity, since the three dimensions expand the working environment, and additionally there may result conflicts of the objectives of different dimensions. In a company that is committed to social and environmental goals and emphasizes long-term economic goals in addition to the classic economic indicators, controlling provides information on these goals and develop a roadmap on how to achieve them13Sailer, U. Nachhaltigkeitscontrolling: Was Controller und Manager über die Steuerung der Nachhaltigkeit wissen sollten (UTB, 2020). which then can be addressed by the term sustainability controlling.

This approach requires additional sources, categories, and measurements of data and information. Whereas previously solely financial and quantifiable parameters could be taken into account, this measurement is only possible to a limited extent for the data on social and ecological parameters. Often, there are various scales that cannot be offset against each other. For this reason, sustainability controlling must develop instruments and perspectives that allow new forms of assessment. Traditional instruments of controlling do not lose their relevance, but reporting, key figures, evaluations, forecasts, and various other instruments can be expanded to include social and ecological aspects.9Wellbrock, W. Nachhaltigkeitscontrolling: Instrumente und Kennzahlen für die strategische und operative Unternehmensführung (Springer, 2020).

In addition, companies face further challenges like globalization, digitalization, individualization, and social changes through social media. Hence the traditional controlling approach of goal setting, planning, and reviewing became significantly more complicated and is under scrutiny.13Sailer, U. Nachhaltigkeitscontrolling: Was Controller und Manager über die Steuerung der Nachhaltigkeit wissen sollten (UTB, 2020). With the increasing complexity of the business environment, the demands on management, leadership styles and controlling are under constant change. The study “Führungskultur im Wandel” (leadership culture under change) conducted by Kruse and Greve in 2014, surveyed 400 managers on future leadership skills.4Initiative Neue Qualität der Arbeit. Führungskultur im Wandel (2014). It shows that, as circumstances become increasingly complex, the skills and tools needed by leaders change. With decreased predictability and increased volatility, the usefulness of management tools that only ensure financial results is reduced.4Initiative Neue Qualität der Arbeit. Führungskultur im Wandel (2014). In contrast the importance of competencies like collaboration skills, personal coaching, motivation, and networking abilities are increasing. Moreover, 100 per cent of the managers consider open-ended process design to be a key competence and prefer self-organizing networks in a dynamic environment to remain flexible and innovative.4Initiative Neue Qualität der Arbeit. Führungskultur im Wandel (2014). Under those circumstances, sustainability controlling should enable the company to react flexibly, keep processes adaptable and increase resilience. This also involves a change in the own self-image of controlling because the formulation of instructions via figures and data loses significance in such a corporate culture.

In summary, sustainability controlling is the natural or socially necessary development of traditional controlling. It does not lose its central task of preparing relevant information for controlling the company, also regarding sustainability, but develops into an internal consultant responsible for the successful implementation and control of the sustainability strategy in the three dimensions of sustainability. There is an increasing demand for qualitative evaluation methods in sustainability controlling, “which have the goal of anchoring sustainability in the sense of initiating permanent and self-evident organizational learning processes”.14Olbert-Bock, S. & Lux, W. Strategisches Controlling als Teil des Sustainability Performance Managements – auch für KMU. CONTROLLER Magazin (5), 4-12 (2016).

3 Practical implementation of sustainability controlling

The first step to implement an integrated sustainability controlling is to develop a sustainability strategy and set targets accordingly for all three dimensions (see chapter 2.2 and 3.3.1).15Michel, U., Isensee, J. & Stehle, A. Sustainability Controlling: Planung, Steuerung und Kontrolle der Realisierung der Nachhaltigkeitsstrategie. in CSR und Finance: Beitrag und Rolle des CFO für eine Nachhaltige Unternehmensführung (eds. Schulz, T. & Bergius, S.) 97-111 (Springer Gabler, 2014). Based on the developed strategy, processes and instruments for sustainability controlling can

be identified. If for example the focus lies on CO2 emissions, then the targets lowering emissions should be prioritized. The general understanding of sustainability controlling in this case is the coordination of economic, ecologic, and social factors and integrating those into the decision-making processes of management control.15Michel, U., Isensee, J. & Stehle, A. Sustainability Controlling: Planung, Steuerung und Kontrolle der Realisierung der Nachhaltigkeitsstrategie. in CSR und Finance: Beitrag und Rolle des CFO für eine Nachhaltige Unternehmensführung (eds. Schulz, T. & Bergius, S.) 97-111 (Springer Gabler, 2014).

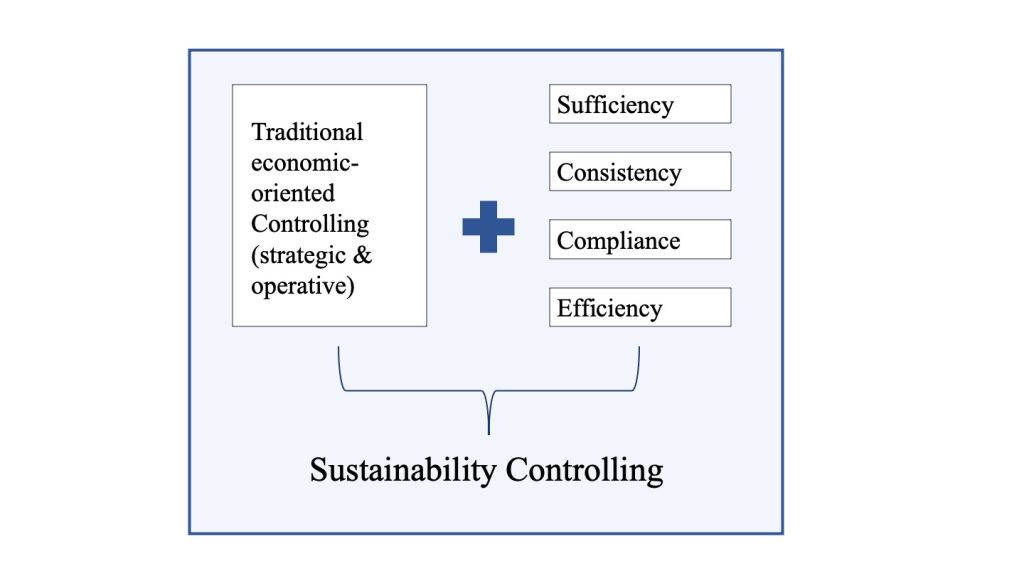

Sailer13Sailer, U. Nachhaltigkeitscontrolling: Was Controller und Manager über die Steuerung der Nachhaltigkeit wissen sollten (UTB, 2020). identifies four approaches that may underlie a sustainability strategy:

- Compliance strategy: following laws and internal guidelines to ensure the legality and legitimacy of the corporation’s actions.13Sailer, U. Nachhaltigkeitscontrolling: Was Controller und Manager über die Steuerung der Nachhaltigkeit wissen sollten (UTB, 2020).

- Strategy of consistency: existing needs should be met with fewer, regenerative or without a loss of resources.13Sailer, U. Nachhaltigkeitscontrolling: Was Controller und Manager über die Steuerung der Nachhaltigkeit wissen sollten (UTB, 2020).

- Strategy of sufficiency: economy, products, culture etc. should consist of less consumption, fewer resources, and less negative effects on the social and ecological environment.13Sailer, U. Nachhaltigkeitscontrolling: Was Controller und Manager über die Steuerung der Nachhaltigkeit wissen sollten (UTB, 2020).

- Strategy of efficiency: economy and products should be improved to work more efficient so that less resources are needed.13Sailer, U. Nachhaltigkeitscontrolling: Was Controller und Manager über die Steuerung der Nachhaltigkeit wissen sollten (UTB, 2020).

Following this logic, an integrated sustainability strategy is a combination of sufficiency, consistency, and efficiency (see figure 1).13Sailer, U. Nachhaltigkeitscontrolling: Was Controller und Manager über die Steuerung der Nachhaltigkeit wissen sollten (UTB, 2020).

3.1 Organization and processes

In general, controlling is a top-level task and therefore it is an ongoing, but important question where the classical financial controlling is located within the organization. Same question has to be posed for Sustainability Controlling. It can either be implemented as an extra unit, for example the environmental department, or might be integrated into the financial controlling.

Integration into financial controlling implies that responsibility for coordinating and measuring targets and integrating them into overall corporate management is in the hands of the controlling department, while operational tasks continue to be managed by the corresponding unit.13Sailer, U. Nachhaltigkeitscontrolling: Was Controller und Manager über die Steuerung der Nachhaltigkeit wissen sollten (UTB, 2020).

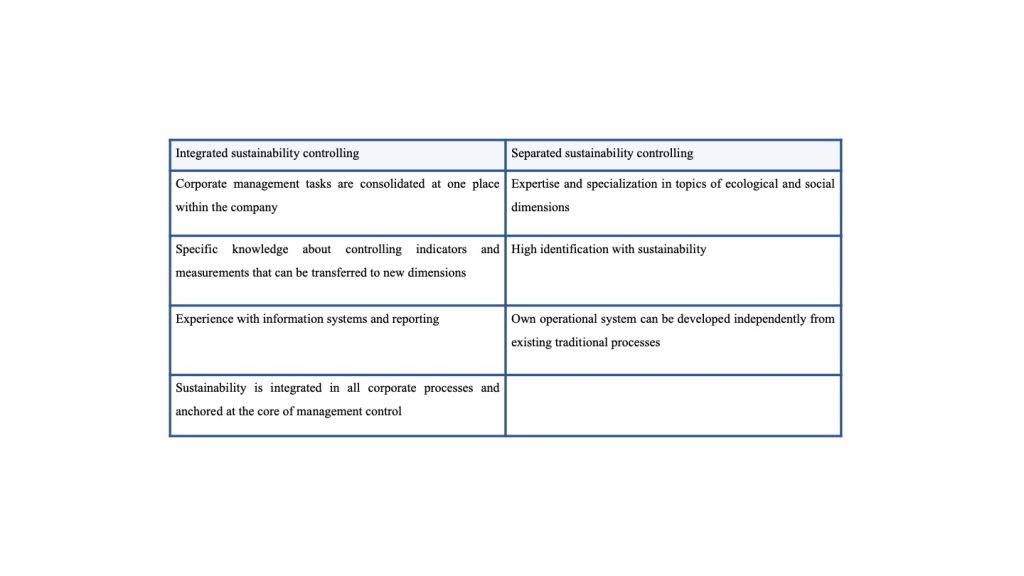

In literature, the consensus can be found that an integrated approach to sustainability controlling leads to better results than sustainability controlling as an extra department.15Michel, U., Isensee, J. & Stehle, A. Sustainability Controlling: Planung, Steuerung und Kontrolle der Realisierung der Nachhaltigkeitsstrategie. in CSR und Finance: Beitrag und Rolle des CFO für eine Nachhaltige Unternehmensführung (eds. Schulz, T. & Bergius, S.) 97-111 (Springer Gabler, 2014).,13Sailer, U. Nachhaltigkeitscontrolling: Was Controller und Manager über die Steuerung der Nachhaltigkeit wissen sollten (UTB, 2020).,1Colsman, B. Nachhaltigkeitscontrolling: Strategien, Ziele, Umsetzung (Springer Gabler, 2016). Advantages of integrating sustainability controlling into the financial controlling become clear when bearing in mind that sustainability is a relevant topic across all departures, as is classical controlling (see figure 2).13Sailer, U. Nachhaltigkeitscontrolling: Was Controller und Manager über die Steuerung der Nachhaltigkeit wissen sollten (UTB, 2020). The relationship of controlling and the existing units like environmental and compliance is similar to the one between controlling and classical units like sales.13Sailer, U. Nachhaltigkeitscontrolling: Was Controller und Manager über die Steuerung der Nachhaltigkeit wissen sollten (UTB, 2020). Close interdepartmental cooperation (especially with the environmental department) is important in order to obtain specific technical know-how from other departments for sustainability topics.15Michel, U., Isensee, J. & Stehle, A. Sustainability Controlling: Planung, Steuerung und Kontrolle der Realisierung der Nachhaltigkeitsstrategie. in CSR und Finance: Beitrag und Rolle des CFO für eine Nachhaltige Unternehmensführung (eds. Schulz, T. & Bergius, S.) 97-111 (Springer Gabler, 2014). In addition to the organizational structure, processes of controlling must be adapted and supplemented by social and ecological aspects so that all three dimensions are taken into account in decision-making processes and the control function for processes in cooperation with other departments.15Michel, U., Isensee, J. & Stehle, A. Sustainability Controlling: Planung, Steuerung und Kontrolle der Realisierung der Nachhaltigkeitsstrategie. in CSR und Finance: Beitrag und Rolle des CFO für eine Nachhaltige Unternehmensführung (eds. Schulz, T. & Bergius, S.) 97-111 (Springer Gabler, 2014).

Practice shows that an integration or extension of controlling usually does not take place in a single moment, but in a process of various steps. Horváth and Berlin3Horváth, P. & Berlin, S. Green-Controlling-Roadmap: Ansätze in der Unternehmenspraxis. in CSR und Controlling: Unternehmerische Verantwortung als Gestaltungsaufgabe des Controlling (eds. Günther, E. & Steinke, K.H.) 23-40 (Springer-Verlag Berlin Heidelberg, 2016). identify three different implementation goals, using the example of green controlling in corporate practice:

Implementation of environmental (individual) measures

Here corporations choose individual measures to improve its ecological and social performance. Often those measures are initiated by employees and not by the management (bottom- up instead of top-down). Additionally, the measures are not included in an environmental strategy, but each measure is determined individually.3Horváth, P. & Berlin, S. Green-Controlling-Roadmap: Ansätze in der Unternehmenspraxis. in CSR und Controlling: Unternehmerische Verantwortung als Gestaltungsaufgabe des Controlling (eds. Günther, E. & Steinke, K.H.) 23-40 (Springer-Verlag Berlin Heidelberg, 2016).

Examples for this strategy are e.g., the acquisition of production machines that are more energy-efficient and save the company money; or the introduction of occupational health management system that measures the health of employees and saves expenses in long-term perspective.16Endenich, C. & Trapp, R. Nachhaltigkeitscontrolling in Klein- und Mittelunternehmen. in Controlling: Aktuelle Entwicklungen und Herausforderungen: Digitalisierung, Nachhaltigkeit und Spezialaspekte (eds. Feldbauer-Durstmüller, B. & Mayr, S.) 229-246 (Springer Fachmedien Wiesbaden, 2019).

Provision of internal and external environmental reports

This goal focuses on creating transparency of ecological and social dimensions of the corporation by recording relevant information and reporting its engagement. Therefore, the focus is not on assessing individual measures but rather on the improvement of the environmental and social performance of the company and its communication to stakeholders. Thus, key performance indicators are developed, recorded and ideally, a regularly (internal or external) reports can be published with the improvements.3Horváth, P. & Berlin, S. Green-Controlling-Roadmap: Ansätze in der Unternehmenspraxis. in CSR und Controlling: Unternehmerische Verantwortung als Gestaltungsaufgabe des Controlling (eds. Günther, E. & Steinke, K.H.) 23-40 (Springer-Verlag Berlin Heidelberg, 2016).

The CargoLine GmbH & Co.KG is a practice example for this type as they can be predominantly assigned to this implementation type. The cooperation agreed to act socially, ecologically, and economically sustainable. One main goal was the recording of the cooperation’s CO2 emissions. Between 2011 and 2012 all the CO2 emissions were recorded for the first time. The long-term goal was to continue measuring the emissions, optimize it over the years and report it in the sustainability report.3Horváth, P. & Berlin, S. Green-Controlling-Roadmap: Ansätze in der Unternehmenspraxis. in CSR und Controlling: Unternehmerische Verantwortung als Gestaltungsaufgabe des Controlling (eds. Günther, E. & Steinke, K.H.) 23-40 (Springer-Verlag Berlin Heidelberg, 2016).

Development and implementation of the environmental strategy

This goal is driven by a systematic sustainability strategy that is usually top-down and implemented by the managers. Based on environmental and social impacts of the company and its products the management develops a systemic environmental strategy. First, a materiality analysis is used to identify strategic environmental issues. Then the sustainability strategy is derived and implemented via instruments, measurements, and responsibilities. Then the environmental and social goals are strategically integrated in the planning and decision-making phase e.g., sales and production planning. The focus is on the planning, measuring, and reporting of the target achievement.3Horváth, P. & Berlin, S. Green-Controlling-Roadmap: Ansätze in der Unternehmenspraxis. in CSR und Controlling: Unternehmerische Verantwortung als Gestaltungsaufgabe des Controlling (eds. Günther, E. & Steinke, K.H.) 23-40 (Springer-Verlag Berlin Heidelberg, 2016).

The Hansgrohe SE is a best practice example for this type. All activities in regard of sustainability-oriented corporate management are combined at its “Green Company” approach. Thus, the company’s sustainability vision and strategy are operationalized through guidelines, budgets, innovations, and projects. Every level of the strategy development and implementation is supported with its own controlling contributions and sustainability controlling is closely interlinked with all corporation levels.3Horváth, P. & Berlin, S. Green-Controlling-Roadmap: Ansätze in der Unternehmenspraxis. in CSR und Controlling: Unternehmerische Verantwortung als Gestaltungsaufgabe des Controlling (eds. Günther, E. & Steinke, K.H.) 23-40 (Springer-Verlag Berlin Heidelberg, 2016).

Depending on the goal and the support by the management, the implementation processes and controlling instruments used differ. While the first two implementation goals primarily require an expansion of operational controlling, the third implementation goal also requires an integrated strategic sustainability controlling. Additionally, it is important to mention that there is not always a clear separation between the different types possible as they are closely interlinked, and companies might combine the approaches.16Endenich, C. & Trapp, R. Nachhaltigkeitscontrolling in Klein- und Mittelunternehmen. in Controlling: Aktuelle Entwicklungen und Herausforderungen: Digitalisierung, Nachhaltigkeit und Spezialaspekte (eds. Feldbauer-Durstmüller, B. & Mayr, S.) 229-246 (Springer Fachmedien Wiesbaden, 2019).

3.2 IT systems

The availability of data and transparency regarding the impact of the company’s activities on the environment and stakeholders is an essential basis for managing sustainability. The information obtained in (sustainability) accounting must be stored in structured form and made available for further processing. For this purpose, an environmental or social information system must be set up. In practice, in particular environmental information systems have been developed.13Sailer, U. Nachhaltigkeitscontrolling: Was Controller und Manager über die Steuerung der Nachhaltigkeit wissen sollten (UTB, 2020). Although several software solutions have emerged during the last years, there is no standardized software so far like for Enterprise-Resource-Planning (ERP) systems. This is due to high specificity of sustainability behavior and impacts of companies and their products. The data recorded, structured, and processed by help of an information system is not restricted to be monetary data but may be also measured in physical units (chapter 3.3).15Michel, U., Isensee, J. & Stehle, A. Sustainability Controlling: Planung, Steuerung und Kontrolle der Realisierung der Nachhaltigkeitsstrategie. in CSR und Finance: Beitrag und Rolle des CFO für eine Nachhaltige Unternehmensführung (eds. Schulz, T. & Bergius, S.) 97-111 (Springer Gabler, 2014).

In small businesses the practical implementation may be done with a spreadsheet program (e.g., Excel) as well as with special software solutions. In larger, manufacturing companies, suitable software support is necessary, since the production processes with their diverse energy and material flows can be mapped or modeled. Specific information requirements of individual decision-makers can also be considered. Reliable and timely information increases acceptance and the willingness to incorporate this information into decisions. For example, statements can be made, as to whether the costs of an ecological measure are economically justifiable or whether the elimination of harmful substances has a positive effect on the health of the employees. The data is therefore not only important for documentation purposes, but also for planning and assessing various scenarios.17Schaltegger, S, Herzig, C, Kleiber, O, Klinke, T & Müller, J. Nachhaltigkeitsmanagement in Unternehmen: Von der Idee zur Praxis: Managementansätze zur Umsetzung von Corporate Social Responsibility und Corporate Sustainability (Centre for Sutainability Management, 2007).

The interdependence of ecological, economic, and social factors makes it necessary not to run the environmental and social information system as an isolated solution, but to link it with existing ERP systems, i.e., the data from existing quantity and value flows. This results in an integrated information system which is also strategically important (chapter 3.1)15Michel, U., Isensee, J. & Stehle, A. Sustainability Controlling: Planung, Steuerung und Kontrolle der Realisierung der Nachhaltigkeitsstrategie. in CSR und Finance: Beitrag und Rolle des CFO für eine Nachhaltige Unternehmensführung (eds. Schulz, T. & Bergius, S.) 97-111 (Springer Gabler, 2014). Furthermore, consistency of economic, ecologic, and social information is given, by using mainly existing IT systems, efforts for implementing sustainability controlling can be kept low. In addition to this, the automatization by information systems of retrieving the data on the social and ecological perspective, is important to reduce manual efforts for collecting the information and feeding it into the reporting systems.15Michel, U., Isensee, J. & Stehle, A. Sustainability Controlling: Planung, Steuerung und Kontrolle der Realisierung der Nachhaltigkeitsstrategie. in CSR und Finance: Beitrag und Rolle des CFO für eine Nachhaltige Unternehmensführung (eds. Schulz, T. & Bergius, S.) 97-111 (Springer Gabler, 2014).

3.3 Instruments

To fulfill their task, controllers work with various tools to collect and organize all the information and thereby find the spots where the company can optimize its performance. The aim of the instruments is to create transparency and to improve the three-dimensional performance of the firm.13Sailer, U. Nachhaltigkeitscontrolling: Was Controller und Manager über die Steuerung der Nachhaltigkeit wissen sollten (UTB, 2020). The choice of relevant instruments used in the controlling depends on the sustainability strategy and the thereby set targets. Strategic instruments are used to examine what the sustainability strategy should look like whereas the operational instruments are the ones measuring whether the sustainability strategy is resulting in positive outcomes.15Michel, U., Isensee, J. & Stehle, A. Sustainability Controlling: Planung, Steuerung und Kontrolle der Realisierung der Nachhaltigkeitsstrategie. in CSR und Finance: Beitrag und Rolle des CFO für eine Nachhaltige Unternehmensführung (eds. Schulz, T. & Bergius, S.) 97-111 (Springer Gabler, 2014).

3.3.1 Strategic instruments

Companies can use several different instruments to identify their sustainability strategy.

SWOT analysis

The SWOT analysis is a typical instrument used in the strategic controlling and it is formed of two parts: the strength and weaknesses analysis and the opportunities and threats analysis. The strength and weaknesses analysis focuses on the assessment of the company’s environment whereas the opportunities and threats analysis more on the competitive situation from the company focuses. The SWOT analysis is only counted sustainable, if analyzed on all three dimensions – the economic, ecological, and social. The analysis can be used to develop a sustainable strategy and to define critical success factors.9Wellbrock, W. Nachhaltigkeitscontrolling: Instrumente und Kennzahlen für die strategische und operative Unternehmensführung (Springer, 2020).

Materiality analysis

Another tool to develop a sustainability strategy is a materiality analysis. It provides an overview of which ecological and social goals shall be pursued and to what extent. The analysis is for each company unique and cannot be adopted. It helps companies to focus on their most relevant sustainability topics. Most often it is combined with a stakeholder dialogue to include the opinion of the company’s stakeholders. The information is collected in a matrix and the topics in the upper right corner are the sustainability goals with the highest priority for the company and its stakeholders.9Wellbrock, W. Nachhaltigkeitscontrolling: Instrumente und Kennzahlen für die strategische und operative Unternehmensführung (Springer, 2020).

Sustainability Balanced Scorecard

The Sustainability Balanced Scorecard is an extended form of the Balanced scorecard that is used to translate the company’s strategy into quantified key figures, indicators, and measurements. The sustainability balanced scorecard further includes the ecological and social perspective and is supposed to meet the requirements of sustainable corporate management. There are two versions commonly used: 1) the social and ecological factors are added as an additional perspective or 2) the social and ecological factors are directly integrated in each perspective. Both versions have several advantages and disadvantages, but each company must decide what version to choose as the strategy derived is company specific.9Wellbrock, W. Nachhaltigkeitscontrolling: Instrumente und Kennzahlen für die strategische und operative Unternehmensführung (Springer, 2020).

Iooi matrix

The input – output – outcome – impact is an instrument of the impact tracking that can be implemented on corporate activities. It is suitable for revealing the degree to which objectives have been achieved in regard of the expensed put into and it gives insight into the quality of the achievements. The conception and planning of the engagement is usually displayed in a matrix. There, indicators and measurements are defined that will be used to evaluate the impact and compare the actual with the calculated goals.1Colsman, B. Nachhaltigkeitscontrolling: Strategien, Ziele, Umsetzung (Springer Gabler, 2016).

3.3.2 Operational instruments

To measure the sustainability controlling a well-known instrument from classical controlling that is highly relied on in management control are financial key performance indicators (KPIs).15Michel, U., Isensee, J. & Stehle, A. Sustainability Controlling: Planung, Steuerung und Kontrolle der Realisierung der Nachhaltigkeitsstrategie. in CSR und Finance: Beitrag und Rolle des CFO für eine Nachhaltige Unternehmensführung (eds. Schulz, T. & Bergius, S.) 97-111 (Springer Gabler, 2014). The success of a company is usually determined by the help of financial indicators. The data required for this is provided by the company’s accounting system. To measure and integrate the environmental and social sustainability performance in the controlling a sustainability-oriented accounting system must be implemented.13Sailer, U. Nachhaltigkeitscontrolling: Was Controller und Manager über die Steuerung der Nachhaltigkeit wissen sollten (UTB, 2020).

Thus, new KPIs need to be implemented in all three dimensions. A key challenge in the conceptual design of sustainability-oriented performance measurement systems is the selection of suitable indicators. In the financial accounting there is a universally recognized standard that all companies can use, but for social and environmental accounting no generally applicable standard has yet been formulated.13Sailer, U. Nachhaltigkeitscontrolling: Was Controller und Manager über die Steuerung der Nachhaltigkeit wissen sollten (UTB, 2020). Nonetheless, the Global Reporting Initiative (GRI) can help to find feasible key indicators16Endenich, C. & Trapp, R. Nachhaltigkeitscontrolling in Klein- und Mittelunternehmen. in Controlling: Aktuelle Entwicklungen und Herausforderungen: Digitalisierung, Nachhaltigkeit und Spezialaspekte (eds. Feldbauer-Durstmüller, B. & Mayr, S.) 229-246 (Springer Fachmedien Wiesbaden, 2019). (Sustainability Accounting & Reporting). In general, indicators are suitable if they reliably show a change in the actual target value. Finding meaningful measurement of these key indicators is an ongoing challenge.

Environmental, social, and long-term economic impacts cannot always be expressed in monetary units. Alternatively to a quantification in monetary terms (e.g. costs for training measures), indicators must either be quantified in physical units such as liters or micrograms (e.g., of toxic waste, CO2 emissions, sick days) or be expressed in qualitative terms (e.g. technical status of environmental protection measures, fair treatment of suppliers).15Michel, U., Isensee, J. & Stehle, A. Sustainability Controlling: Planung, Steuerung und Kontrolle der Realisierung der Nachhaltigkeitsstrategie. in CSR und Finance: Beitrag und Rolle des CFO für eine Nachhaltige Unternehmensführung (eds. Schulz, T. & Bergius, S.) 97-111 (Springer Gabler, 2014). The use of different units to specify them has several advantages: e.g., indicators with a temporal advantage can be selected, which can indicate a change before it becomes apparent in the target figure. To give an example, incoming orders are used as a leading indicator for sales development, and the development of repurchases is a readily measurable indicator of customer satisfaction. The selection of these key figures thus has an “influence” on the actual sustainability performance of the company.13Sailer, U. Nachhaltigkeitscontrolling: Was Controller und Manager über die Steuerung der Nachhaltigkeit wissen sollten (UTB, 2020).

The new KPIs that represent a large part of the sustainability controlling are:

Ecological

Everything related to the environment e.g., materials, energy, water, biodiversity, emissions etc. can be expressed as an ecological indicator16Endenich, C. & Trapp, R. Nachhaltigkeitscontrolling in Klein- und Mittelunternehmen. in Controlling: Aktuelle Entwicklungen und Herausforderungen: Digitalisierung, Nachhaltigkeit und Spezialaspekte (eds. Feldbauer-Durstmüller, B. & Mayr, S.) 229-246 (Springer Fachmedien Wiesbaden, 2019). and they are usually the indicators considered first when implementing sustainability in corporations. Some of the indicators can be expressed in monetary terms, e.g., CO2 certificates set a price on the CO2 or compensation payments can be determined. Others may be expressed in physical units (see above).15Michel, U., Isensee, J. & Stehle, A. Sustainability Controlling: Planung, Steuerung und Kontrolle der Realisierung der Nachhaltigkeitsstrategie. in CSR und Finance: Beitrag und Rolle des CFO für eine Nachhaltige Unternehmensführung (eds. Schulz, T. & Bergius, S.) 97-111 (Springer Gabler, 2014). Examples from the Deutsche Telekom for ecological indicators are the energy usage or the CO2-emissions. For the energy usage they put the usage of energy in relation to the turnover and compare them over the years. For the CO2-emissions the change in CO2 is calculated in comparison with the base year 2008.13Sailer, U. Nachhaltigkeitscontrolling: Was Controller und Manager über die Steuerung der Nachhaltigkeit wissen sollten (UTB, 2020).

Social

Social indicators shall reflect measurements that ensure fundamental social goals such as diversity, equal opportunities, and anti-discrimination but can also be implemented in the working context, e.g., improving the working conditions.16Endenich, C. & Trapp, R. Nachhaltigkeitscontrolling in Klein- und Mittelunternehmen. in Controlling: Aktuelle Entwicklungen und Herausforderungen: Digitalisierung, Nachhaltigkeit und Spezialaspekte (eds. Feldbauer-Durstmüller, B. & Mayr, S.) 229-246 (Springer Fachmedien Wiesbaden, 2019).,13Sailer, U. Nachhaltigkeitscontrolling: Was Controller und Manager über die Steuerung der Nachhaltigkeit wissen sollten (UTB, 2020). The evaluation of a negative or positive social impact is often normative and therefore requires a dialog with stakeholders. Social accounting creates the necessary transparency for target setting, facilitates the selection of suitable measures and enables success to be monitored. The well-known “Plan-Do-Check-Act cycle” thus receives its necessary data basis: Measures to improve social performance are planned, implemented, checked, and subsequently adjusted if necessary.13Sailer, U. Nachhaltigkeitscontrolling: Was Controller und Manager über die Steuerung der Nachhaltigkeit wissen sollten (UTB, 2020).

Economic (long term)

Within the economic dimension, sustainability means above all an orientation towards long-term economic success. A decisive factor for the suitability for long-term corporate management is therefore the top key figure.13Sailer, U. Nachhaltigkeitscontrolling: Was Controller und Manager über die Steuerung der Nachhaltigkeit wissen sollten (UTB, 2020). Thus, the long-term economic success of a firm must include future success and success potentials guided by central key figures.13Sailer, U. Nachhaltigkeitscontrolling: Was Controller und Manager über die Steuerung der Nachhaltigkeit wissen sollten (UTB, 2020).

The difficulty of long-term controlling is that on one hand short-term goals need to be achieved. On the other hand, it has to ensure that short-term goals do not outweigh long-term goals.13Sailer, U. Nachhaltigkeitscontrolling: Was Controller und Manager über die Steuerung der Nachhaltigkeit wissen sollten (UTB, 2020). Criticism of unsuitable performance measurement led to the development of performance measurement, which uses financial and non-financial indicators in addition to short-term ones to ensure long-term success. Indicators that could be used as long-term and non-financial are for example customer satisfaction, innovative strength, or adaptability.18Prammer, H. K. Wie lässt sich die operative Umweltleistung von Unternehmen messen? Streiflichter auf ausgewählte Konzepte und Normen. in Corporate Sustainability: Der Beitrag von Unternehmen zu einer nachhaltigen Entwicklung in Wirtschaft und Gesellschaft, (eds. Prammer, H. K.) 8–36 (Springer Link, 2010). In a sustainably oriented controlling system, such longer-term indicators should be integrated into the planning and reporting system and be communicated comprehensively towards stakeholders. In addition, incentives that lead to short-term action should be identified and adequately modified. For example, management profit-sharing could be based on the achievement of long-term targets and not be based primarily on net income.13Sailer, U. Nachhaltigkeitscontrolling: Was Controller und Manager über die Steuerung der Nachhaltigkeit wissen sollten (UTB, 2020).

Two dimensional numbers

For an integrated sustainability controlling not only new indicators have to be introduced but also two-dimensional measures should be defined to relate KPIs to one another and put them into context. For example, a new key figure for the CO2 emissions of a plant makes it possible

to evaluate the ecological impact in addition to the purely economic consideration, e.g., based on the net present value. However, only a key figure such as CO2 cost-effectiveness (CO2 emissions in relation to the net present value) makes it possible to identify the plant that has the lowest environmental impact per euro invested.15Michel, U., Isensee, J. & Stehle, A. Sustainability Controlling: Planung, Steuerung und Kontrolle der Realisierung der Nachhaltigkeitsstrategie. in CSR und Finance: Beitrag und Rolle des CFO für eine Nachhaltige Unternehmensführung (eds. Schulz, T. & Bergius, S.) 97-111 (Springer Gabler, 2014).

3.4 Sustainability controlling as a basis for sustainability reporting and sustainability communication

The data collected and KPIs calculated all throughout the Sustainability Controlling processes can be a good basis for the creation of a sustainability report or for the support of broader sustainability communication.

3.4.1 Sustainability reporting

A sustainability report can be defined as “a public report about an organization’s social, environmental, economic, and social impacts of its day-to-day activities, and hence its positive and negative contributions towards the goal of a sustainable global economy. A sustainability report is the result of a sustainability reporting process”19Gbangbola, K. & Lawler, N. Gold Standard Sustainability Reporting: A Step by Step Guide to Producing a Sustainability Report (Routledge, 2020). Throughout the early 1990s there was an emphasis on environmental reporting to be noticed, which was followed by an increase in interest in social reporting around the mid-1990s. More recently, however, triple bottom line reporting, sustainability reporting, and integrated reporting have received most of the attention in corporate organizations20Gray, R. & Milne, M. Sustainability reporting : who’s kidding whom?. Journal of New Zealand 81(6), 66-70 (2002). even though it is important to mention that these terms cannot be used synonymously.

Reasons for implementing sustainability reporting may vary. The ones most commonly found throughout the literature are the aim to differentiate, pressure from direct competitors, investors, or regulatory pressure through reporting obligations, critical stakeholders (e. g. NGOs) or customers demanding information about sustainability, the wish to increase the company’s performance or aim to make use of reliable KPIs for management decision-making.21Frese, M. & Colsman, B. Nachhaltigkeitsreporting für Finanzdienstleister (Springer Fachmedien Wiesbaden GmbH, 2018). Only in recent years, yearly CSR-reports have become compulsory for companies of public interest and of a certain size in the EU. This compulsion is based on a guideline developed by the European Union called “guideline 2014/95/EU” and a failure to comply will result in a fine of up to ten million euros. However, there are only few requirements regarding the specific content. The minimum content requested asks for risks, strategies, and their results as well as for due-diligence-processes regarding environmental, social, and human resources concerns, the caretaking of human rights and combating corruption and bribery.21Frese, M. & Colsman, B. Nachhaltigkeitsreporting für Finanzdienstleister (Springer Fachmedien Wiesbaden GmbH, 2018).

Sustainability Reporting, if done well, can be an asset to the company’s reputation and credibility. In addition, it can be beneficial to the internal management and its decision-making, e. g., through internally promoting an understanding for sustainability, enabling efficient data collection processes, and forming a basis for contemporary corporate management and decisions to be made in the future.21Frese, M. & Colsman, B. Nachhaltigkeitsreporting für Finanzdienstleister (Springer Fachmedien Wiesbaden GmbH, 2018). In comparison to CSR reports that tend to portray the previous twelve months, sustainability reports address “the reduction of negative social, economic, and environmental effects while doing business”.22Bini, L. & Bellucci, M. Integrated Sustainability Reporting (Springer Nature Switzerland, 2020).

Regarding the content of the report, one of two main approaches is usually adopted: the inside- out perspective or the outside-in perspective.21Frese, M. & Colsman, B. Nachhaltigkeitsreporting für Finanzdienstleister (Springer Fachmedien Wiesbaden GmbH, 2018). The inside-out perspective translates sustainability from an internal point of view for external stakeholders. The company’s goal in this setting is usually to generate data and KPIs for the corporate management. Since the report is then targeted at the company’s stakeholders, the content mainly informs about the company’s priorities, measures, and goals. With the outside-in perspective the company aims to conform to external expectations on what sustainability is. Those expectations may range from aspects like branding development to more measurable aspects like ratings, rankings, or the adoption of and compliance to global sustainable development goals or the Paris agreement.21Frese, M. & Colsman, B. Nachhaltigkeitsreporting für Finanzdienstleister (Springer Fachmedien Wiesbaden GmbH, 2018). Ideally, a company’s sustainability report features both perspectives. If the focus lies too strongly on the inside-out perspective, chances are the company might miss out on current sustainability trends and developments within the context of sustainability management. When focusing predominantly on the outside-in perspective, however, the content of the report might easily be perceived as arbitrary. Solely trying to comment on environmentally important topics within society without having implemented and communicated strategies or processes might lead to reports that are mostly filled with phrases and implausible statements.21Frese, M. & Colsman, B. Nachhaltigkeitsreporting für Finanzdienstleister (Springer Fachmedien Wiesbaden GmbH, 2018).

With an increasing number of sustainability reports published by companies all over the world22Bini, L. & Bellucci, M. Integrated Sustainability Reporting (Springer Nature Switzerland, 2020). many seek consultancies’ advice on sustainability issues.23Domingues, A., Lozano, R., Ceulemans, K. & Ramos, T. Sustainability reporting in public sector organizations: Exploring the relation between the reporting process and organizational change management for sustainability. Journal of Environmental Management 192, 292-301 (2017)., mfn referencenumber=24]Barth, R. & Wolff, F. Corporate social responsibility in Europe: rhetoric and realities (Edward Elgar, 2009).[/mfn],24Deegan, C., Rankin, M. & Tobin, J. An examination of the corporate social and environmental disclosures of BHP from 1983‐1997. Accountability Journal 15(3), 312-343 (2002).,25KPMG. The KPMG survey of corporate responsibility reporting 2017. https://ass(ets.kpmg/content/dam/kpmg/xx/pdf/2017/10/kpmg-survey-of-corporateresponsibility-reporting-2017.pdf. (2017).,26Laine, M. Towards Sustaining the Status Quo: Business Talk of Sustainability in Finnish Corporate Disclosures 1987–2005. European Accounting Review 19(2), 247-274 (2010). Therefore, business actors share their opinions on social and environmental challenges as well as on sustainable growth in general. Critics argue, that since these organization are “very powerful social actors”22Bini, L. & Bellucci, M. Integrated Sustainability Reporting (Springer Nature Switzerland, 2020)., these disclosures also shape reality and have an impact on how society as a whole views sustainability.27Hines, R. Financial accounting. in Communicating reality, we construct reality. Accounting, Organizations and Society 13(3), 251-261 (1988).,28Phillips, N., & Hardy, C. Discourse analysis: Investigating processes of social construction Sage Publications, 50, (2002). As a consequence, a definite need to comprehend both the corporate drivers behind such reporting as well as the rhetoric used by corporations to further pursue their goals arises. To thoroughly be able to assess, “whether a narrative on sustainability is genuine or rhetoric requires a close, case-by-case approach”22Bini, L. & Bellucci, M. Integrated Sustainability Reporting (Springer Nature Switzerland, 2020).

The challenge in sustainability reporting lies in the difficulty to put the very complex and abstract principle of sustainability into words.21Frese, M. & Colsman, B. Nachhaltigkeitsreporting für Finanzdienstleister (Springer Fachmedien Wiesbaden GmbH, 2018). Hence, the art of communication and the translation from numbers and data gathered into tangible text is of vital importance to the success of a company’s sustainability reporting in terms of its external representation.21Frese, M. & Colsman, B. Nachhaltigkeitsreporting für Finanzdienstleister (Springer Fachmedien Wiesbaden GmbH, 2018).

The translation necessary for sustainability reporting can roughly be divided into four steps: Firstly, the company needs to thoroughly understand the term of sustainability in the context of its own market segment and branch. Secondly, the firm must be able to differentiate between sustainability within the market sector it operates in and sustainability measures applying to the specific company. This enables the company’s management to prioritize among different aspects of the sustainability context and identify the most relevant focal points. Thirdly, in order for the outward communication to be effective, the company should be using creativity to tell the story of their sustainability measures and controlling, rather than just filling the blanks in reporting standards. Lastly, the effect of sustainability shall not only be recognizable within environment and society, but among companies as well. In the best case, sustainability communication done right increases the profitability of the company at hand. The base line for any company in terms of their sustainability reporting, however, is to at least maintain, if not to increase, the social legitimacy.21Frese, M. & Colsman, B. Nachhaltigkeitsreporting für Finanzdienstleister (Springer Fachmedien Wiesbaden GmbH, 2018).

3.4.2 Sustainability communication

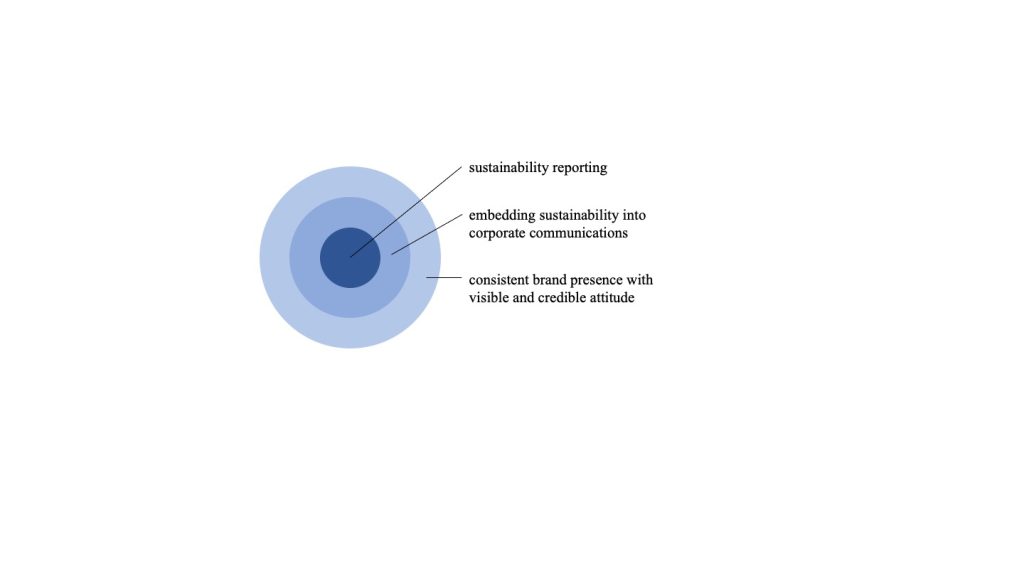

Even though it can often be witnessed, the terms sustainability reporting and sustainability communication cannot be used synonymously. Rather, sustainability reporting is ought to be the very core of sustainability communications – which, in turn, is often being viewed as the tool to make the sustainability reporting working successfully for the company in the first place. Similarly, one could say: Sustainability communication is to sustainability reporting, what marketing is to sales (Figure 3).21Frese, M. & Colsman, B. Nachhaltigkeitsreporting für Finanzdienstleister (Springer Fachmedien Wiesbaden GmbH, 2018).

The fact that sustainability reporting can be viewed as the core activity of overall brand presence and corporate communications suggests applying strategies that successfully link information throughout different sources. The aim is to not solely rely on the sustainability report to share results of sustainability controlling, while not to duplicate information on various platforms either.

Put to practice, this implies the differentiation of information into three main categories:

- Information on sustainability that can be placed outside of the sustainability report, e. g., on the company’s website.

- Placements used to teaser the full sustainability report, e. g. text referencing to the report or print documents presenting sustainability at the firm in a short way, thereby increasing the reader’s motivation to read the sustainability report.

- The actual sustainability report, which also enables links to other relevant topics (policies, strategies, etc.) in the digital format.21Frese, M. & Colsman, B. Nachhaltigkeitsreporting für Finanzdienstleister (Springer Fachmedien Wiesbaden GmbH, 2018).

Even with a sustainability communication strategy in place, the task of bringing environmental awareness to the public seems to be a difficult one. Transforming scientific information into language that the general public can understand is simply not enough to effectively communicate sustainability. For example, 29 % of Europeans, according to a recent Eurobarometer survey conducted, were aware of the SDGs but did not fully understand what they were. Only 12% of respondents claimed to be aware of the objectives and to know what they were. Due to people’s differing levels of awareness “for fully understanding the complex set of ethical, technological, legal, and societal considerations which surround solutions for sustainability related problems a one-fits-it-all approach is not suitable”.29Weder, F., Krainer, L. & Karmasin, M. The Sustainability Communication Reader (Springer Fachmedien Wiesbaden, 2021).

3.4.3 Best practice example: Commerzbank AG

The Commerzbank AG is one of the leading banks in Germany, partner for around 28,000 corporate customer associations and approx. 11 million private and corporate customers within the German market.30Commerzbank. Commerzbank AG – Über uns. https://commerzbank.com/de/hauptnavigation/konzern/konzern.html (2022). Until the year of 2014, the Commerzbank AG has annually published a sustainability report. Ever since the business year of 2015, the company established a new approach, which is better tailored to their target group – using a 40-page magazine they comprehensively present their focal topics with regard to sustainability management and sustainability controlling. The magazine is available online and in print format and on the last page they link to their online report according to GRI standards. Thereby they successfully created two different channels: one to comprehensively and lightly engaging with their stakeholders and emphasizing their own measures and strategies regarding sustainability31Commerzbank. Wie nachhaltig kann eine Bank sein?. https://www.commerzbank.de/media/nachhaltigkeit/viii__daten___fakten/berichte/2015_CR-Magazin_DE.pdf (2015)., and one for a much smaller target group, functioning as a proof for the content of the magazine, supporting all claims with more detailed numbers and statistics.21Frese, M. & Colsman, B. Nachhaltigkeitsreporting für Finanzdienstleister (Springer Fachmedien Wiesbaden GmbH, 2018).

4 Drivers and barriers of sustainability controlling

In order to create a better understanding of what constitutes a successful implementation of sustainability controlling in the future, both internal as well as external drivers and barriers are presented below. Before taking a closer look, it is important to note that there is some overlap between sustainability controlling and corporate sustainability, and that the areas cannot always be clearly separated.

4.1 Drivers

4.1.1 External

Society and customers can be seen as one key driver for the introduction of sustainability controlling due to their expectations of companies. Topics such as climate change, exploitation, scarcity of resources and loss of ecosystems and its services are among the most pressing social issues at this point in time.9Wellbrock, W. Nachhaltigkeitscontrolling: Instrumente und Kennzahlen für die strategische und operative Unternehmensführung (Springer, 2020). Because of this societal impact, a rethinking is also taking place among the companies. It is now generally accepted that only sustainable companies can be successful in the long term.32Günther, E., Endrikat, J. & Günther, T.CSR im Controlling. in CSR und Controlling (eds. Günther, E. & Steinke, K.-H.) 3-22 (Springer Gabler, 2016). This change puts companies under pressure to address this issue. All stakeholders like customers, creditors, or banks, want to see a transformation. For this purpose, as stated in this Wiki entry, the expansion of controlling to include social and ecological dimensions and the integration of these in corporate management is necessary.9Wellbrock, W. Nachhaltigkeitscontrolling: Instrumente und Kennzahlen für die strategische und operative Unternehmensführung (Springer, 2020).

In addition to the societal level, the political level plays an important role in the question of how companies interpret their actions as politics provide the legal framework. The German government, for example, established the German Council for Sustainable Development back in 2001. This interdisciplinary council is to formulate strategies and goals on how sustainable development can be achieved. Not only in a political frame, but also in society and the whole economy. In addition to that, it is to determine the social dialog and discourse and provide solution approaches for companies and society.33Ternés. A. Nachhaltigkeit und Digitalisierung als Chance für Unternehmen. In Nachhaltiges Management (eds. Englert, M. & Ternés, A.) 79-104 (Springer Gabler, 2019). In chapter 2.2, the Brundtland definition of sustainability was already displayed. This definition was formulated within the framework of the UN Commission on Environment and Development. Today, the United Nations still plays a formative role in the field of sustainability. With their Agenda 2030 and the SDGs, they provide the framework for a sustainable transformation for society, politics, and companies. Political decisions therefore affect the way corporate practice are to be carried out.34Brüssel, C. Kernkompetenz Nachhaltigkeit und Corporate Social Responsibility. In Nachhaltigkeit in der Unternehmenspraxis (eds. Brüggemann, S., Brüssel, C. & Härthe, D.) 11-24 (Springer Gabler, 2018).

Due to increased social and political expectations, a company needs a corporate unit that supports the company in its realignment, accompanies strategies and plans, and assumes management and control for them. Traditionally, these tasks are located in controlling and can expand to different instruments, (see chapter 3.3). In addition, there are benefits such as better implementation of environmental strategies, greater awareness of ecological issues, improved sustainability communication internally and externally, the general creation of transparency in sustainability issues, and also the pursuit of an image gain.22Bini, L. & Bellucci, M. Integrated Sustainability Reporting (Springer Nature Switzerland, 2020). Following the assumption that only companies that have a sustainable orientation are successful in the long term, it is a self-preservation purpose that drives companies to implement sustainability controlling.9Wellbrock, W. Nachhaltigkeitscontrolling: Instrumente und Kennzahlen für die strategische und operative Unternehmensführung (Springer, 2020).

4.1.2 Internal drivers

An internal driver of sustainability controlling may be the fact that awareness for sustainability is increasing in many parts of our society and therefore in a companies’ workforce, too. If the employees demand sustainable measures from their employer, this may also imply the controlling of the company. This could then lead to an intrinsic motivation of the company towards more sustainability, i.e., more sustainability controlling.

Furthermore, the location of sustainability controlling within an organization can be seen as a driver – as it has been described in chapter 3.1. This section has shown that integrated sustainability controlling has advantages over separate controlling in successfully implementing sustainability. Since sustainability, just like classical controlling, is a holistic topic that is relevant for all departments, the choice of location for the sustainability unit is of great importance for the success of the sustainability strategy.15Michel, U., Isensee, J. & Stehle, A. Sustainability Controlling: Planung, Steuerung und Kontrolle der Realisierung der Nachhaltigkeitsstrategie. in CSR und Finance: Beitrag und Rolle des CFO für eine Nachhaltige Unternehmensführung (eds. Schulz, T. & Bergius, S.) 97-111 (Springer Gabler, 2014).,13Sailer, U. Nachhaltigkeitscontrolling: Was Controller und Manager über die Steuerung der Nachhaltigkeit wissen sollten (UTB, 2020).,1Colsman, B. Nachhaltigkeitscontrolling: Strategien, Ziele, Umsetzung (Springer Gabler, 2016). If a company is willing to drive sustainability, it should integrate and implement its sustainability controlling within the financial controlling. Thus, the overall awareness will increase, and employees can actively be integrated in the process.

4.2 Barriers

4.2.1 External barriers

External stakeholders such as customers or non-governmental organizations can be an external barrier that could pose a threat to a company’s sustainable orientation and thus to the pursuit of sustainable goals with the support of sustainable controlling. Many practical examples show that stakeholders take a close look at how a company is positioned and how it behaves in certain situations. The promise of sustainable corporate management and sustainability goals might have a backfire effect. Once a company has decided on an approach to sustainability, it must be maintained. If, for example, negative reports come to light that contrast with the conditions and goals desired by the company, stakeholders can be angered and thus put pressure on the company. This is particularly the case if sustainability communication (Chapter 3.4.2) has previously sold this as a success or advertised it in a different light. In this case, the former image gain of being considered a sustainable company and making a positive contribution to society would quickly evaporate.35Knaut, A. Warum Kunden Unternehmen nicht verstehen. In Wirtschafts Woche https://www.wiwo.de/technologie/green/nachhaltigkeit-warum-kunden-unternehmen-nicht-verstehen/13544764.html (2012).

4.2.2 Internal barriers

The first barrier to mention here is that controlling often still attributes a financial focus. The sustainability dimensions currently still seem to have a shadowy existence in the understanding of controlling. Accordingly, controlling is mostly not seen as a significant driving force of sustainability within an organization. In order to achieve this, a controlling department must specifically focus on sustainability topics and expand the former financial focus to include the sustainability dimensions.36Hilbert. S. Nachhaltigkeitscontrolling. In Nachhaltiges Management (eds. Englert, M. & Ternés, A.) 521-549 (Springer Gabler, 2019). Like mentioned before (chapter 2.2), the topic of sustainability (in companies) is often addressed via the triple bottom line where the economic success is a requirement to finance the ecologic and social dimension and vice versa that economic success is only possible in a stable social environment. Conceptually, the triple bottom line assumes a balanced consideration of economic, social, and environmental dimensions; however, in practice, more attention is often paid to the economic dimension. Thus, measures for planet and people are traditionally taken when benefitting profit. This approach of the triple bottom line is known as the economic triple bottom line.13Sailer, U. Nachhaltigkeitscontrolling: Was Controller und Manager über die Steuerung der Nachhaltigkeit wissen sollten (UTB, 2020). Especially in bigger, management-controlled corporates this approach still prevails. The sustainability approach has changed over the years from being mainly a restrictive and costly cause to saving costs, by reducing the use of resources or new products. While this approach still only considers the profit perspective an integrated sustainability controlling is led by the idea of preserving the world for future generations taking more factors into account that are important from a social or ecological point of view.13Sailer, U. Nachhaltigkeitscontrolling: Was Controller und Manager über die Steuerung der Nachhaltigkeit wissen sollten (UTB, 2020). In that perspective, sustainability controlling still needs to be better implemented in most companies and management control systems.

Furthermore, a weakness of key figures, one of the main instruments of controlling, is that interdependencies are usually only considered selectively and provide very simplified information with sometimes limited significance.13Sailer, U. Nachhaltigkeitscontrolling: Was Controller und Manager über die Steuerung der Nachhaltigkeit wissen sollten (UTB, 2020).,1Colsman, B. Nachhaltigkeitscontrolling: Strategien, Ziele, Umsetzung (Springer Gabler, 2016). This is determined by the quality of the underlying key figure or information systems, i.e. the systematic condensation of information and the correctness of the initial data are of central importance. In this context, a sensible and valid selection and formation of key figures, can reduce the emergence of indicators that allow misinterpretations and lead to false correlations, as interdependencies of the individual variables are clarified. This requires an intensive examination of one’s own key figure system and the interpretation of the KPIs.1Colsman, B. Nachhaltigkeitscontrolling: Strategien, Ziele, Umsetzung (Springer Gabler, 2016).

Another difficulty why sustainability controlling is often not implemented is the fear of a lack of quantifiability of targets. Whereas financial and easily measurable numerical values were used and processed in classic controlling, qualified values in other scales are now often added, e.g., prevented deforestation, overfishing, social costs, social standards or stakeholder satisfaction. This hurdle still makes many companies averse to adding a sustainability level to their controlling. Therefore, companies should move away from the view that only what can be measured counts and from the premise that values that cannot be easily measured or quantified cannot be controlled or changed. But especially in capital market-oriented companies, this argument continues to prevail.13Sailer, U. Nachhaltigkeitscontrolling: Was Controller und Manager über die Steuerung der Nachhaltigkeit wissen sollten (UTB, 2020). Particularly, when competitors do not refer to sustainable goals, there is often a lack of pressure and missing focus to recognize the need to implement a sustainability strategy within the own company. Furthermore, doubts may arise within the organization as to whether it would actually bring added value or whether an expansion of activities would not only cause further costs.22Bini, L. & Bellucci, M. Integrated Sustainability Reporting (Springer Nature Switzerland, 2020).

References

- 1Colsman, B. Nachhaltigkeitscontrolling: Strategien, Ziele, Umsetzung (Springer Gabler, 2016).

- 2Weber, J. Controlling. Gabler Wirtschaftslexikon. https://wirtschaftslexikon.gabler.de/definition/controlling-30235/version-370809 (2019).

- 3Horváth, P. & Berlin, S. Green-Controlling-Roadmap: Ansätze in der Unternehmenspraxis. in CSR und Controlling: Unternehmerische Verantwortung als Gestaltungsaufgabe des Controlling (eds. Günther, E. & Steinke, K.H.) 23-40 (Springer-Verlag Berlin Heidelberg, 2016).

- 4Initiative Neue Qualität der Arbeit. Führungskultur im Wandel (2014).

- 5Becker, W. & Ulrich, P. Handbuch Controlling. (Springer Gabler, 2022).

- 6Horváth, P. Controlling (Vahlen, 2012).

- 7Reichmann, T. Controlling mit Kennzahlen und Management-Tools: Die systemgestützten Controlling-Konzeption (Vahlen, 2011).

- 8Hubert, B. Controlling-Konzeptionen: Ein schneller Einstieg in Theorie und Praxis (Springer Gabler, 2018).

- 9Wellbrock, W. Nachhaltigkeitscontrolling: Instrumente und Kennzahlen für die strategische und operative Unternehmensführung (Springer, 2020).

- 10World Commission on Environment and Development. Our Common Future. (1987).

- 11Wördenweber, M. Nachhaltigkeitsmanagement: Grundlagen und Praxis unternehmerischen Handelns (Schäffer-Poeschel Verlag, 2017).

- 12Weissenberger-Eibl, M. A.& Braun, A. Nachhaltige Unternehmensentwicklung. In Nachhaltiges Management (eds. Englert, M. & Ternés, A) 249-270 (Springer Gabler, 2019).

- 13Sailer, U. Nachhaltigkeitscontrolling: Was Controller und Manager über die Steuerung der Nachhaltigkeit wissen sollten (UTB, 2020).

- 14Olbert-Bock, S. & Lux, W. Strategisches Controlling als Teil des Sustainability Performance Managements – auch für KMU. CONTROLLER Magazin (5), 4-12 (2016).

- 15Michel, U., Isensee, J. & Stehle, A. Sustainability Controlling: Planung, Steuerung und Kontrolle der Realisierung der Nachhaltigkeitsstrategie. in CSR und Finance: Beitrag und Rolle des CFO für eine Nachhaltige Unternehmensführung (eds. Schulz, T. & Bergius, S.) 97-111 (Springer Gabler, 2014).

- 16Endenich, C. & Trapp, R. Nachhaltigkeitscontrolling in Klein- und Mittelunternehmen. in Controlling: Aktuelle Entwicklungen und Herausforderungen: Digitalisierung, Nachhaltigkeit und Spezialaspekte (eds. Feldbauer-Durstmüller, B. & Mayr, S.) 229-246 (Springer Fachmedien Wiesbaden, 2019).

- 17Schaltegger, S, Herzig, C, Kleiber, O, Klinke, T & Müller, J. Nachhaltigkeitsmanagement in Unternehmen: Von der Idee zur Praxis: Managementansätze zur Umsetzung von Corporate Social Responsibility und Corporate Sustainability (Centre for Sutainability Management, 2007).

- 18Prammer, H. K. Wie lässt sich die operative Umweltleistung von Unternehmen messen? Streiflichter auf ausgewählte Konzepte und Normen. in Corporate Sustainability: Der Beitrag von Unternehmen zu einer nachhaltigen Entwicklung in Wirtschaft und Gesellschaft, (eds. Prammer, H. K.) 8–36 (Springer Link, 2010).

- 19Gbangbola, K. & Lawler, N. Gold Standard Sustainability Reporting: A Step by Step Guide to Producing a Sustainability Report (Routledge, 2020).

- 20Gray, R. & Milne, M. Sustainability reporting : who’s kidding whom?. Journal of New Zealand 81(6), 66-70 (2002).

- 21Frese, M. & Colsman, B. Nachhaltigkeitsreporting für Finanzdienstleister (Springer Fachmedien Wiesbaden GmbH, 2018).

- 22Bini, L. & Bellucci, M. Integrated Sustainability Reporting (Springer Nature Switzerland, 2020).

- 23Domingues, A., Lozano, R., Ceulemans, K. & Ramos, T. Sustainability reporting in public sector organizations: Exploring the relation between the reporting process and organizational change management for sustainability. Journal of Environmental Management 192, 292-301 (2017).

- 24Deegan, C., Rankin, M. & Tobin, J. An examination of the corporate social and environmental disclosures of BHP from 1983‐1997. Accountability Journal 15(3), 312-343 (2002).

- 25KPMG. The KPMG survey of corporate responsibility reporting 2017. https://ass(ets.kpmg/content/dam/kpmg/xx/pdf/2017/10/kpmg-survey-of-corporateresponsibility-reporting-2017.pdf. (2017).

- 26Laine, M. Towards Sustaining the Status Quo: Business Talk of Sustainability in Finnish Corporate Disclosures 1987–2005. European Accounting Review 19(2), 247-274 (2010).