Authors: Lina Helen Kleine Klausing

Edited by: –

Last updated: October 5, 2025

Executive summary

Green bonds are financial instruments designed to fund projects that deliver environmental benefits and support climate change mitigation. They have grown rapidly since their introduction in 2007, driven by global climate agreements and investor demand for sustainable finance.

The green bond market includes various types of bonds, such as Use of Proceeds Bonds and Project Bonds, and is supported by standards like the Green Bond Principles (GBP), Climate Bond Standard (CBS), and the European Green Bond Standard (EuGBS). These standards aim to ensure transparency, proper use of proceeds, and environmental integrity.

Issuers and investors are motivated by financial and non-financial incentives, including reputation, signaling commitment to sustainability, and portfolio diversification. However, challenges remain, such as the risk of greenwashing, lack of uniform standards, and higher issuance costs.

Research shows mixed evidence on the financial benefits of green bonds, such as the existence of a greenium (lower yields compared to conventional bonds). Ecological impacts are generally positive, with reductions in CO₂ emissions observed over time and improvements in environmental ratings.

Best practices for issuers include creating a Green Bond Framework, obtaining external reviews, and publishing impact reports. These measures enhance transparency and credibility. As the market evolves, harmonization of standards and continued monitoring of environmental outcomes will be critical for scaling green finance globally.

1 Relevance

The issue of combating climate change is currently a highly salient topic in the academic and public discourse. Global warming confronts us with a series of challenges that require the development of solution strategies to overcome. As reported by the EU climate change service Copernicus (2024)1Copernicus Climate Change Service. Surface air temperature for June 2024. Copernicus <https://climate.copernicus.eu/surface-air-temperature-june-2024> (2024) [accessed 14.08.2024]., June 2024 was the hottest June since global temperature records began. In June 2024, a temperature increase of 1.5°C was recorded in comparison to the average temperatures recorded in pre-industrial times from 1850 to 1900. In 2015, 196 countries adopted on a global climate protection agreement at the UN Climate Change Conference in Paris with the aim of limiting global warming to below 2°C compared to the pre-industrial levels and to finance the reduction of greenhouse gas emissions and the development of climate resilience.2United Nations Framework Convention on Climate Change (UNFCCC). The Paris Agreement. UNFCCC <https://unfccc.int/process-and-meetings/the-paris-agreement> (n.d.) [accessed 14.08.2024].,3United Nations Framework Convention on Climate Change (UNFCCC). The Paris Agreement. UNFCCC <https://unfccc.int/sites/default/files/resource/parisagreement_publication.pdf> (2015) [accessed 14.08.2024]. In particular, the objective of the Paris Agreement is to avoid exceeding a global average temperature rise of 1.5°C, as exceeding this value would pose a global risk with far-reaching consequences.3United Nations Framework Convention on Climate Change (UNFCCC). The Paris Agreement. UNFCCC <https://unfccc.int/sites/default/files/resource/parisagreement_publication.pdf> (2015) [accessed 14.08.2024]. As indicated by data from Copernicus (2024)1Copernicus Climate Change Service. Surface air temperature for June 2024. Copernicus <https://climate.copernicus.eu/surface-air-temperature-june-2024> (2024) [accessed 14.08.2024]., the 1.5°C threshold was exceeded for the twelfth time in succession in June 2024. This underlines the requirement for additional measures to be implemented in order to achieve the temperature objective of 2°C set out in the Paris Agreement. A reduction in greenhouse gases and the achievement of climate neutrality are required for this. The implementation of the measures also requires that companies rethink and adapt their business practices in order to achieve a more climate-friendly approach.4Bhutta, U. S., Tariq, A., Farrukh, M., Raza, A. & Iqbal, M. K. Green bonds for sustainable development: Review of literature on development and impact of green bonds. Technological Forecasting and Social Change 175, 121378 (2022). https://doi.org/10.1016/j.techfore.2021.121378 As part of the Paris Agreement, companies are advised to integrate environmental, social and governance (ESG) strategies into their business plans.4Bhutta, U. S., Tariq, A., Farrukh, M., Raza, A. & Iqbal, M. K. Green bonds for sustainable development: Review of literature on development and impact of green bonds. Technological Forecasting and Social Change 175, 121378 (2022). https://doi.org/10.1016/j.techfore.2021.121378 However, the realisation of the measures and projects is associated with considerable capital requirements, which must be covered by both public and private investment.5Jäger, L., Ringel, M. & Schiereck, D. Green Bonds als Instrumente der Klimaschutzfinanzierung: Eine Literaturübersicht. Zeitschrift für Bankrecht und Bankwirtschaft 33, 209-225 (2021). https://doi.org/10.15375/zbb-2021-0307 In this context, it is necessary to determine which financial instruments are best suited to climate financing. In recent years, green bonds have emerged as one of the most prominent instruments for climate financing.

The objective of this bachelor’s thesis is to provide an explanation of the nature and functions of green bonds as a climate-friendly financial instrument, as well as to present a set of practical applications pertinent to the context of green bond issuance. The bachelor thesis is structured as follows. Firstly, the methodology section outlines the procedure for the selection and analysis of the scientific literature. The thesis is then subdivided into two main sections: the literature review and the practical implementation. The literature section begins with the fundamentals and background of green bonds, including a definition of green bonds and an overview of the development of the global market for green bonds. Subsequently, the two most important actors in the green bond market, namely issuers and investors, and the rationale behind their issuance of green bonds are presented. The final part of the literature review considers the impact of green bonds, examining both the financial and ecological dimensions. As part of the practical implementation, globally recognised standards are initially presented, which serve as a voluntary framework for the issuance of green bonds. A particular focus is placed on the Green Bond Principles, which form the basis for a large numbers of green bond issues and further on for other standards. Building on this, two company examples are presented that have created a green bond framework and had it verified by an external review. Three guidelines are then presented and compared, which were made available to issuers to support the issuance of green bonds and provide best practices based on international experience. Finally, the drivers and barriers for implementing green bonds in companies and organizations are presented.

2 Literature review

2.1 Fundamentals and background

This section offers an initial overview of the fundamental characteristics of green bonds and the development and actors in the green bond market.

2.1.1 Definition of green bonds

Green bonds are fixed-income securities that allow both issuers and investors to support projects that promote environmental sustainability and counteract climate change.4Bhutta, U. S., Tariq, A., Farrukh, M., Raza, A. & Iqbal, M. K. Green bonds for sustainable development: Review of literature on development and impact of green bonds. Technological Forecasting and Social Change 175, 121378 (2022). https://doi.org/10.1016/j.techfore.2021.121378,5Jäger, L., Ringel, M. & Schiereck, D. Green Bonds als Instrumente der Klimaschutzfinanzierung: Eine Literaturübersicht. Zeitschrift für Bankrecht und Bankwirtschaft 33, 209-225 (2021). https://doi.org/10.15375/zbb-2021-0307 Green bonds are generally structured like conventional bonds.6Caramichael, J. & Rapp, A. C. The green corporate bond issuance premium. Journal of Banking & Finance 162, 107126 (2024). https://doi.org/10.1016/j.jbankfin.2024.107126,7Maltais, A. & Nykvist, B. Understanding the role of green bonds in advancing sustainability. Journal of Sustainable Finance & Investment, 1-20 (2020). https://doi.org/10.1080/20430795.2020.1724864 Schuster & Uskova (2015)8Schuster, T. & Uskova, M. Finanzierung: Anleihen, Aktien, Optionen. (Springer Gabler Berlin, 2015). https://doi.org/10.1007/978-3-662-46239-3 describe a bond in the following way. The issuer of a bond borrows from many different investors. The issue volume is divided into many shares. At the end of the term, called the maturity of the bond, the issuer is obliged to repay these shares. In return for providing the money, the investor receives a fee in the form of interest. The interest rate is called the coupon and is paid periodically, usually annually, over the life of the bond.8Schuster, T. & Uskova, M. Finanzierung: Anleihen, Aktien, Optionen. (Springer Gabler Berlin, 2015). https://doi.org/10.1007/978-3-662-46239-3 The main difference is that a use of proceeds for green bonds is specified, indicating that the proceeds will be used for financing or refinancing green projects.9Kedia, N. & Joshipura, M. Green bonds for sustainability: current pathways and new avenues. Managerial Finance 49, 948-974 (2023). https://doi.org/10.1108/MF-08-2022-0367,7Maltais, A. & Nykvist, B. Understanding the role of green bonds in advancing sustainability. Journal of Sustainable Finance & Investment, 1-20 (2020). https://doi.org/10.1080/20430795.2020.1724864 These green projects are characterised by the fact that they make an environmental contribution to mitigating or preventing climate change.10Schöning, S., Michael, E. T. & Nolte, B. Corporate Green Bonds als innovative Finanzanlage – eine kritische Betrachtung. in Bank- und Finanzwirtschaft im Stress: Aktuelle Herausforderungen und Lösungsansätze (eds Stephan Schöning, Nils Moch, & Sonja Schütte-Biastoch) 125-159 (Springer Fachmedien Wiesbaden, 2023). https://doi.org/10.1007/978-3-658-41884-7_6

The problem is that people struggle with the definition of green bonds.4Bhutta, U. S., Tariq, A., Farrukh, M., Raza, A. & Iqbal, M. K. Green bonds for sustainable development: Review of literature on development and impact of green bonds. Technological Forecasting and Social Change 175, 121378 (2022). https://doi.org/10.1016/j.techfore.2021.121378 There is no single, universally recognised definition of green bonds.5Jäger, L., Ringel, M. & Schiereck, D. Green Bonds als Instrumente der Klimaschutzfinanzierung: Eine Literaturübersicht. Zeitschrift für Bankrecht und Bankwirtschaft 33, 209-225 (2021). https://doi.org/10.15375/zbb-2021-0307,11Tang, D. Y. & Zhang, Y. Do shareholders benefit from green bonds? Journal of Corporate Finance 61, 101427 (2020). https://doi.org/10.1016/j.jcorpfin.2018.12.001 A commonly used definition is that of the International Capital Market Association (ICMA), which defines green bonds as “any type of bond instrument where the proceeds or an equivalent amount will be exclusively applied to finance or re-finance, in part or in full, new and/or existing eligible Green Projects” (ICMA , 2022a, p. 3).12International Capital Market Association (ICMA). Green Bond Principles: Voluntary Process Guidelines for Issuing Green Bonds. ICMA <https://www.icmagroup.org/assets/documents/Sustainable-finance/2022-updates/Green-Bond-Principles-June-2022-060623.pdf> (2022a) [accessed 03.04.2024].

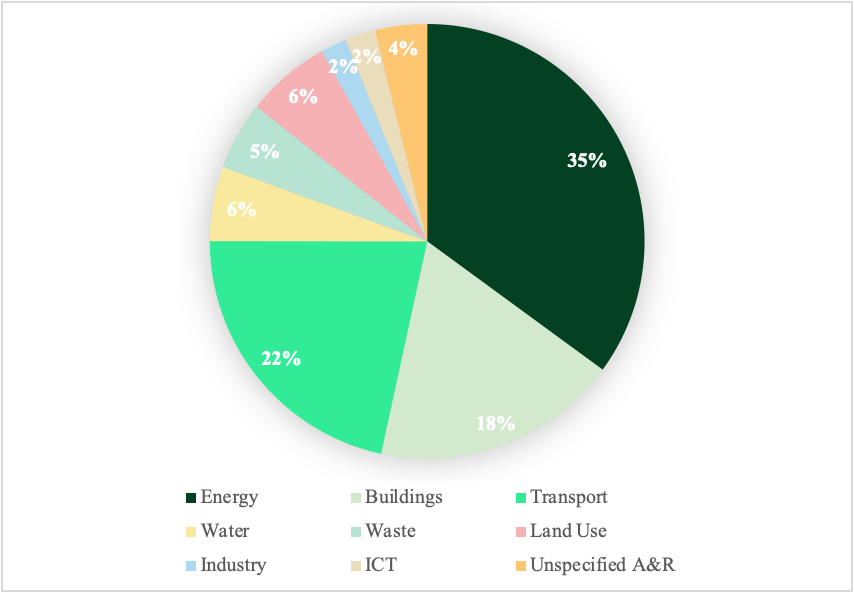

Other disagreements relate to the definition of green projects. There are different views on which projects qualify as green and which do not.13Gilchrist, D., Yu, J. & Zhong, R. The limits of green finance: A survey of literature in the context of green bonds and green loans. Sustainability 13, 478 (2021). https://doi.org/10.3390/su13020478 There are already voluntary standards trying to define green and sustainable projects. Among the most prominent are the ICMA’s Green Bond Principles (GBP) and the Climate Bond Standard (CBS) developed by the Climate Bond Initiative (CBI).11Tang, D. Y. & Zhang, Y. Do shareholders benefit from green bonds? Journal of Corporate Finance 61, 101427 (2020). https://doi.org/10.1016/j.jcorpfin.2018.12.001 Chapter 4.1 describes these two standards and the recently published EU Green Bond Standard. Eligible projects according to the GBP are for example renewable energy, energy efficiency, pollution prevention and control, clean transportation, sustainable water and wastewater management and green buildings.12International Capital Market Association (ICMA). Green Bond Principles: Voluntary Process Guidelines for Issuing Green Bonds. ICMA <https://www.icmagroup.org/assets/documents/Sustainable-finance/2022-updates/Green-Bond-Principles-June-2022-060623.pdf> (2022a) [accessed 03.04.2024]. In 2023, the proceeds of green bonds were used as shown in Figure 1. Energy (35%), buildings (18%) and transport (22%) are the three largest Use of Proceeds sectors in 2023. These are followed by water (6%), waste (5%) and land use (6%). Smaller categories are industry with 2%, information and communication technologies (ICT) with 2% and unspecified A&R with 4%.

Green Bonds are a type of labelled bonds, as the name already implies what they aim to finance.5Jäger, L., Ringel, M. & Schiereck, D. Green Bonds als Instrumente der Klimaschutzfinanzierung: Eine Literaturübersicht. Zeitschrift für Bankrecht und Bankwirtschaft 33, 209-225 (2021). https://doi.org/10.15375/zbb-2021-0307,7Maltais, A. & Nykvist, B. Understanding the role of green bonds in advancing sustainability. Journal of Sustainable Finance & Investment, 1-20 (2020). https://doi.org/10.1080/20430795.2020.1724864 Other examples of labelled bonds are war bonds, which were used to finance military expenditure in times of war, or railroad bonds, which were used to finance transport projects.5Jäger, L., Ringel, M. & Schiereck, D. Green Bonds als Instrumente der Klimaschutzfinanzierung: Eine Literaturübersicht. Zeitschrift für Bankrecht und Bankwirtschaft 33, 209-225 (2021). https://doi.org/10.15375/zbb-2021-0307 Moreover, green bonds may be regarded as a form of impact investing.15Monk, A. & Perkins, R. What explains the emergence and diffusion of green bonds? Energy Policy 145, 111641 (2020). https://doi.org/10.1016/j.enpol.2020.111641 Impact investing is the practice of investing in companies, projects and funds with the specific intention of achieving a measurable positive impact on the environment or society, in addition to a positive financial return.16Bernard-Rau, B. & Schnerring, G. Gabler Kompakt-Lexikon Corporate Social Responsibility. (Springer Fachmedien Wiesbaden, 2022). https://doi.org/10.1007/978-3-658-34940-0

As outlined by ICMA (2022a)12International Capital Market Association (ICMA). Green Bond Principles: Voluntary Process Guidelines for Issuing Green Bonds. ICMA <https://www.icmagroup.org/assets/documents/Sustainable-finance/2022-updates/Green-Bond-Principles-June-2022-060623.pdf> (2022a) [accessed 03.04.2024]., the current classification of green bonds encompasses four distinct types: Standard Green Use of Proceeds Bond, Green Revenue Bond, Green Project Bond, and Secured Green Bond. These four types and their characteristics are listed in Table 1.

Table 1: Types of green bonds, ICMA (2022a, p.8)12International Capital Market Association (ICMA). Green Bond Principles: Voluntary Process Guidelines for Issuing Green Bonds. ICMA

| Standard Green Use of Proceeds Bond | “an unsecured debt obligation with full recourse-to-the-issuer only and aligned with the GBP” (ICMA, 2022a, p.8)12International Capital Market Association (ICMA). Green Bond Principles: Voluntary Process Guidelines for Issuing Green Bonds. ICMA |

| Green Revenue Bond | “a non-recourse-to-the-issuer debt obligation aligned with the GBP in which the credit exposure in the bond is to the pledged cash flows of the revenue streams, fees, taxes etc., and whose use of proceeds go to related or unrelated Green Project(s)” (ICMA, 2022a, p.8)12International Capital Market Association (ICMA). Green Bond Principles: Voluntary Process Guidelines for Issuing Green Bonds. ICMA |

| Green Project Bond | “a project bond for a single or multiple Green Project(s) for which the investor has direct exposure to the risk of the project(s) with or without potential recourse to the issuer, and that is aligned with the GBP” (ICMA, 2022a, p.8)12International Capital Market Association (ICMA). Green Bond Principles: Voluntary Process Guidelines for Issuing Green Bonds. ICMA |

| Secured Green Bond | “a secured bond where the net proceeds will be exclusively applied to finance or refinance either: The Green Project(s) securing the specific bond only (a ‘Secured Green Collateral Bond’); or The Green Project(s) of the issuer, originator or sponsor, where such Green Projects may or may not be securing the specific bond in whole or in part (a ‘Secured Green Standard Bond’). A Secured Green Standard Bond may be a specific class or tranche of a larger transaction.” (ICMA, 2022a, p.8)12International Capital Market Association (ICMA). Green Bond Principles: Voluntary Process Guidelines for Issuing Green Bonds. ICMA |

2.1.2 Development of the green bond market

The green bond market is a relatively young market and has grown rapidly in the recent years.17Ehlers, T. & Packer, F. Green bond finance and certification. BIS Quarterly Review September (2017). The first green bond was issued by European Investment Bank (EIB) in 2007, called climate awareness bond.5Jäger, L., Ringel, M. & Schiereck, D. Green Bonds als Instrumente der Klimaschutzfinanzierung: Eine Literaturübersicht. Zeitschrift für Bankrecht und Bankwirtschaft 33, 209-225 (2021). https://doi.org/10.15375/zbb-2021-0307,18Hachenberg, B. & Schiereck, D. Are green bonds priced differently from conventional bonds? Journal of Asset Management 19, 371-383 (2018). https://doi.org/10.1057/s41260-018-0088-5 The World Bank issued its first green bond just one year later in 2008, which was marketed to a wider range of investors.5Jäger, L., Ringel, M. & Schiereck, D. Green Bonds als Instrumente der Klimaschutzfinanzierung: Eine Literaturübersicht. Zeitschrift für Bankrecht und Bankwirtschaft 33, 209-225 (2021). https://doi.org/10.15375/zbb-2021-0307,18Hachenberg, B. & Schiereck, D. Are green bonds priced differently from conventional bonds? Journal of Asset Management 19, 371-383 (2018). https://doi.org/10.1057/s41260-018-0088-5 In the years that followed, green bonds were issued mainly by supranational agencies and sovereigns, and private participation remained low due to information asymmetries and a lack of green definitions and standards.9Kedia, N. & Joshipura, M. Green bonds for sustainability: current pathways and new avenues. Managerial Finance 49, 948-974 (2023). https://doi.org/10.1108/MF-08-2022-0367

According to the CBI (n.d.)19Climate Bonds Initiative (CBI). Explaining Green Bonds. CBI <https://www.climatebonds.net/market/explaining-green-bonds> (n.d.) [accessed 17.06.2024]., the issuance of the first green corporate bond by Swedish property company Vasokronan in November 2013 marked a turning point in the green bond market. The market started to boom in 2014. Since then, a new record has been set every year. Milestones are 2015, when cumulative green bond issuance reaches USD 100 billion; 2017, when cumulative issuance reaches USD 250 billion; and 2020, when cumulative issuance reaches USD 1 trillion.19Climate Bonds Initiative (CBI). Explaining Green Bonds. CBI <https://www.climatebonds.net/market/explaining-green-bonds> (n.d.) [accessed 17.06.2024]. Ehlers & Packer (2017)17Ehlers, T. & Packer, F. Green bond finance and certification. BIS Quarterly Review September (2017). describe the introduction of the GBPs in January 2014, the foundation of many existing green labels, as the driver for the growth of the green bond market.

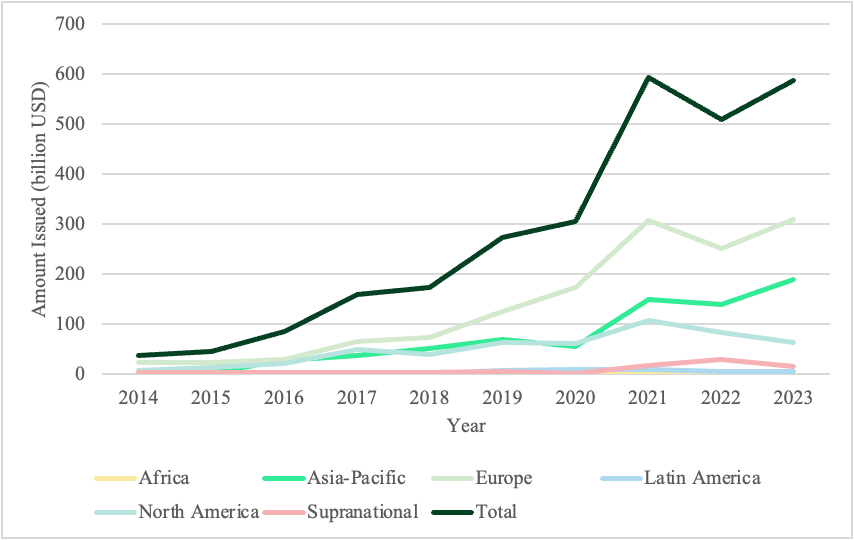

Figure 2 shows the amount of green bonds issued between 2014 and 2023, classified by regions. There is a steady increase in the total volume of green bonds issued until 2021. In 2022, the growth rate decreases slightly compared to 2021. USD 593.9 billion is issued in 2021 and USD 509.6 billion in 2022. This drop in volume is mainly due to “post-COVID-19 inflation concerns and broader market volatility following the Russian invasion of Ukraine” (CBI, 2022, p. 3)20Climate Bonds Initiative (CBI). Sustainable Debt Market Summary H1 2022. CBI <https://www.climatebonds.net/files/reports/cbi_susdebtsum_h1_2022_02c.pdf> (2022) [accessed 19.06.2024].. In 2023, the total volume increases again to USD 587.7 billion. In 2023, over half of the total volume of green bonds (close to 53%) originated from Europe.21Climate Bonds Initiative (CBI). Global State of the Market Report 2023. CBI <https://www.climatebonds.net/files/reports/cbi_sotm23_02h.pdf> (2024b) [accessed 12.05.2024]. Asia-Pacific was the second most important region for green bond issuance, representing approximately one-third of the global total issuance (USD 190.2 billion).21Climate Bonds Initiative (CBI). Global State of the Market Report 2023. CBI <https://www.climatebonds.net/files/reports/cbi_sotm23_02h.pdf> (2024b) [accessed 12.05.2024].,14Climate Bonds Initiative (CBI). Interactive Data Platform. CBI <https://www.climatebonds.net/market/data/> (2024a) [accessed 08.05.2024].

Africa is a region particularly vulnerable to the risks of climate change.21Climate Bonds Initiative (CBI). Global State of the Market Report 2023. CBI <https://www.climatebonds.net/files/reports/cbi_sotm23_02h.pdf> (2024b) [accessed 12.05.2024]. The CBI (2024b)21Climate Bonds Initiative (CBI). Global State of the Market Report 2023. CBI <https://www.climatebonds.net/files/reports/cbi_sotm23_02h.pdf> (2024b) [accessed 12.05.2024]. documents that the green issuance from Africa has increased significantly, with a 326% year-on-year increase compared to 2022. In the year 2023, an aligned volume of USD 2 billion was documented. In comparison to the previous year, the number of issuers increased from four to eleven in 2023.21Climate Bonds Initiative (CBI). Global State of the Market Report 2023. CBI <https://www.climatebonds.net/files/reports/cbi_sotm23_02h.pdf> (2024b) [accessed 12.05.2024].

In 2023, the total cumulative size of the green bond market was USD 2.8 trillion across 96 countries and 53 currencies.21Climate Bonds Initiative (CBI). Global State of the Market Report 2023. CBI <https://www.climatebonds.net/files/reports/cbi_sotm23_02h.pdf> (2024b) [accessed 12.05.2024]. China is the leading country source in the green bond market in 2023 with USD 83.5 billion, followed by Germany (USD 67.5 billion) and the USA (USD 59.9 billion).21Climate Bonds Initiative (CBI). Global State of the Market Report 2023. CBI <https://www.climatebonds.net/files/reports/cbi_sotm23_02h.pdf> (2024b) [accessed 12.05.2024]. The top 3 currencies in the market in 2023 were led by EUR with USD 260 billion, followed by USD (USD 126.7 billion) and CNY (USD 79.2 billion).21Climate Bonds Initiative (CBI). Global State of the Market Report 2023. CBI <https://www.climatebonds.net/files/reports/cbi_sotm23_02h.pdf> (2024b) [accessed 12.05.2024]. A total of 2,746 green bonds were issued in 2023, which represents a decrease of around 29% compared to the 3,848 green bonds issued in 2022.14Climate Bonds Initiative (CBI). Interactive Data Platform. CBI <https://www.climatebonds.net/market/data/> (2024a) [accessed 08.05.2024].

However, the share of green bonds is still a very small part of total global bond issuance. Table 2 shows the share of green bond issuance in global long-term fixed income issuance. The percentage share has increased more than elevenfold from 0.204% in 2014 to 2.262% in 2022.

Table 2: Share of green bond issuance (%), own illustration using data from SIFMA Research (2023)22SIFMA Research. 2023 Capital Markets Fact Book. SIFMA

| Year | Global Long-Term Fixed Income Issuance24 (billion USD) | Green Bond Issuance16 (billion USD) | Share of green bond issuance (%) |

| 2014 | 18,132.5 | 37 | 0.204% |

| 2015 | 20,181.3 | 46.4 | 0.230% |

| 2016 | 20,630.6 | 85.3 | 0.413% |

| 2017 | 18,919.1 | 160 | 0.846% |

| 2018 | 18,364.8 | 172.9 | 0.941% |

| 2019 | 23,031.8 | 274.4 | 1.191% |

| 2020 | 28,009.7 | 305.4 | 1.090% |

| 2021 | 27,318.8 | 593.9 | 2.174% |

| 2022 | 22,527.8 | 509.6 | 2.262% |

2.1.3 Actors in the green bond market

The green bond market has the same players as the general bond market. Park (2018)23Park, S. K. Investors as Regulators: Green Bonds and the Governance Challenges of the Sustainable Finance Revolution. Stanford Journal of International Law 54, 1-48 (2018). lists a number of actors and stakeholders that regulate the green bond market. These include “issuers, underwriters, investors, credit rating agencies and research organizations, advocacy groups, multilateral institutions, stock exchanges, and government agencies” (Park, 2018, p. 6).23Park, S. K. Investors as Regulators: Green Bonds and the Governance Challenges of the Sustainable Finance Revolution. Stanford Journal of International Law 54, 1-48 (2018). The two most important stakeholders are issuers and investors, which are explained in more detail below.

In their study, Maltais & Nykvist (2020)7Maltais, A. & Nykvist, B. Understanding the role of green bonds in advancing sustainability. Journal of Sustainable Finance & Investment, 1-20 (2020). https://doi.org/10.1080/20430795.2020.1724864 discern three categories of motivations and drivers for investment in the green bond market. These are the financial case, the business case and the legitimacy and institutionally oriented drivers. The financial case is driven by motivations, including enhanced financial returns, lower financial risk and cost of capital, as well as universal investor incentives. The business case also encompasses aspects such as brand development, market expansion and risk reduction. Legitimacy and institutionally oriented drivers can include the pursuit of legitimacy and the attainment of institutional recognition, as well as the influence of institutional pressures.7Maltais, A. & Nykvist, B. Understanding the role of green bonds in advancing sustainability. Journal of Sustainable Finance & Investment, 1-20 (2020). https://doi.org/10.1080/20430795.2020.1724864

2.1.3.1 Issuers

With the steady growth of the green bond market, there has also been an increase in the number of issuers. To provide an overview of the different types of issuers, they have been divided into sub-groups. According to Jäger et. al (2021)5Jäger, L., Ringel, M. & Schiereck, D. Green Bonds als Instrumente der Klimaschutzfinanzierung: Eine Literaturübersicht. Zeitschrift für Bankrecht und Bankwirtschaft 33, 209-225 (2021). https://doi.org/10.15375/zbb-2021-0307, on the one hand there are the governmental players, which are further subdivided into regional, national, international, sub-sovereign, sovereign and supranational issuers. On the other hand, there are private sector companies that issue corporate green bonds. In the early years, green bonds were almost exclusively issued by supranational institutions and organizations.5Jäger, L., Ringel, M. & Schiereck, D. Green Bonds als Instrumente der Klimaschutzfinanzierung: Eine Literaturübersicht. Zeitschrift für Bankrecht und Bankwirtschaft 33, 209-225 (2021). https://doi.org/10.15375/zbb-2021-0307 In particular, multilateral development banks, such as the EIB, were responsible for green bond issuance from 2007 to 2012.5Jäger, L., Ringel, M. & Schiereck, D. Green Bonds als Instrumente der Klimaschutzfinanzierung: Eine Literaturübersicht. Zeitschrift für Bankrecht und Bankwirtschaft 33, 209-225 (2021). https://doi.org/10.15375/zbb-2021-0307 Until 2013, there were practically no corporate green bonds on the market.24Flammer, C. Corporate green bonds. Journal of Financial Economics 142, 499-516 (2021). https://doi.org/10.1016/j.jfineco.2021.01.010 In 2023, around USD 335 billion of corporate green bonds were issued.14Climate Bonds Initiative (CBI). Interactive Data Platform. CBI <https://www.climatebonds.net/market/data/> (2024a) [accessed 08.05.2024]. This represents around 57 % of the total green bond market. As a result, corporate green bonds have seen strong growth and are playing an increasingly important role in practice.24Flammer, C. Corporate green bonds. Journal of Financial Economics 142, 499-516 (2021). https://doi.org/10.1016/j.jfineco.2021.01.010

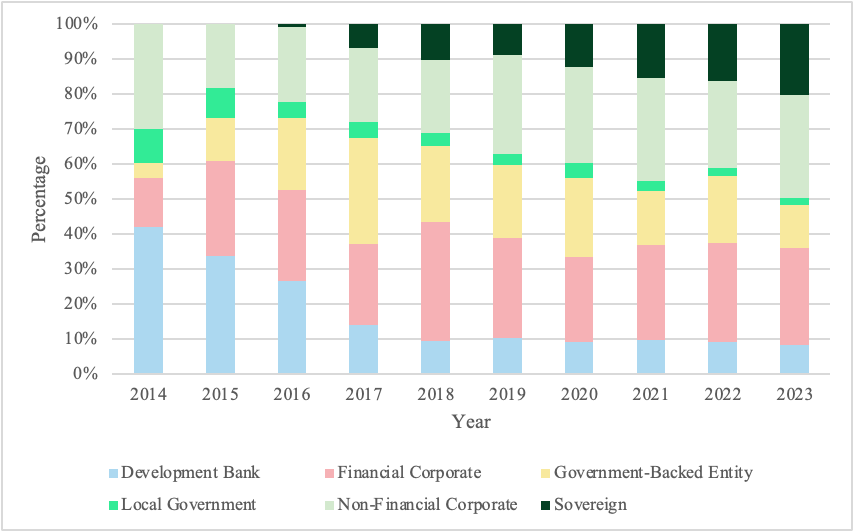

Figure 3 shows the percentage development of each type of issuer from 2014 to 2023. The CBI distinguishes between sovereigns, development banks, local governments, government-backed entities, financial corporates and non-financial corporates.14Climate Bonds Initiative (CBI). Interactive Data Platform. CBI <https://www.climatebonds.net/market/data/> (2024a) [accessed 08.05.2024]. As described above, a large share of green bond issuance (57% in 2023) is accounted for corporate entities, including financial and non-financial corporations. The development of financial corporations has risen from 14% in 2014 to almost the double a year later (27% in 2015). Since 2015, the share has remained relatively constant at a level between 23% and 29%. Only in 2018 did the share increase to 34%. In 2023, the share of financial corporates was 28%. Since 2019, the share of non-financial corporates has remained at a level between 25% and 29%. Since 2016, the share of the amount of green bonds issued by sovereigns has steadily increased from 1% (2016) to 20% (2023). The share of local government green bond issuance is rather low and was around 2% in 2023. The share of green bonds issued by government-backed entities rose significantly between 2014 and 2017, from 4% to 30%. However, the share has been decreasing since 2017 and was only 12% in 2023. In 2014, the share of green bonds issued by development banks was 42%, which decreased four years later to 9% in 2018. Since then, the share has remained constant between 8% and 10%.

An important question is why do issuers choose to issue green bonds rather than conventional bonds?

In their survey, Maltais & Nykvist (2020)7Maltais, A. & Nykvist, B. Understanding the role of green bonds in advancing sustainability. Journal of Sustainable Finance & Investment, 1-20 (2020). https://doi.org/10.1080/20430795.2020.1724864 identify “broadening the investor base, lower capital costs, and meeting investor demand for sustainable investment products” (p. 10) as the three key incentives for issuing green bonds. The incentives most frequently referenced are primarily financial in nature, such as the provision of a discount for issuers of green bonds relative to conventional bonds or enhanced access to capital through the issuance of green bonds. However, Maltais & Nykvist (2020)7Maltais, A. & Nykvist, B. Understanding the role of green bonds in advancing sustainability. Journal of Sustainable Finance & Investment, 1-20 (2020). https://doi.org/10.1080/20430795.2020.1724864 posit that these incentives are not the primary drivers for issuers’ decisions to issue green bonds. Instead, non-financial incentives are of greater significance for the surveyed issuers. For instance, issuing a green bond enables issuers to communicate externally that they have already made strides in sustainability and that the green bond issuance builds upon this foundation. In addition, the authors identify a further motivation for issuing green bonds, namely a branding incentive.7Maltais, A. & Nykvist, B. Understanding the role of green bonds in advancing sustainability. Journal of Sustainable Finance & Investment, 1-20 (2020). https://doi.org/10.1080/20430795.2020.1724864

According to Flammer (2021)24Flammer, C. Corporate green bonds. Journal of Financial Economics 142, 499-516 (2021). https://doi.org/10.1016/j.jfineco.2021.01.010, there are three potential reasons why companies choose to issue green bonds, namely (1) signalling, (2) greenwashing and (3) the cost of capital. According to (1) the signalling argument, a key objective is to reduce information asymmetry between issuers and investors in order to reduce transaction costs. Flammer (2021)24Flammer, C. Corporate green bonds. Journal of Financial Economics 142, 499-516 (2021). https://doi.org/10.1016/j.jfineco.2021.01.010 writes, that investors often do not have enough information to assess a company’s level of commitment to the environment and climate protection. The issuance of green bonds, therefore, serves to signal such a commitment to prospective investors. The company invests money directly in green projects that are effective for the environment and are transparent to investors through the company’s reporting and additional external and independent certification.24Flammer, C. Corporate green bonds. Journal of Financial Economics 142, 499-516 (2021). https://doi.org/10.1016/j.jfineco.2021.01.010 This certification is initially cost-intensive for the companies, but it can bring some advantages in the long term.5Jäger, L., Ringel, M. & Schiereck, D. Green Bonds als Instrumente der Klimaschutzfinanzierung: Eine Literaturübersicht. Zeitschrift für Bankrecht und Bankwirtschaft 33, 209-225 (2021). https://doi.org/10.15375/zbb-2021-0307 It enhances the issuer’s reputation on the market, information asymmetries can be reduced and the investor base can be broadened.25Hyun, S., Park, D. & Tian, S. The price of going green: the role of greenness in green bond markets. Accounting & Finance 60, 73-95 (2020). https://doi.org/10.1111/acfi.12515,26Hyun, S., Park, D. & Tian, S. Pricing of Green Labeling: A Comparison of Labeled and Unlabeled Green Bonds. Finance Research Letters 41, 101816 (2021). https://doi.org/10.1016/j.frl.2020.101816 Another potential rationale for issuing green bonds is (2) the greenwashing argument. Greenwashing is defined as “[…] a strategy or a practice – through marketing actions and communication – used by a company to position itself in the public eye as environmentally friendly, while its activities are harmful to the environment.” (Bernard-Rau & Schnerring, 2022, p. 46)16Bernard-Rau, B. & Schnerring, G. Gabler Kompakt-Lexikon Corporate Social Responsibility. (Springer Fachmedien Wiesbaden, 2022). https://doi.org/10.1007/978-3-658-34940-0. In the context of issuing green bonds, greenwashing refers to the risk that the proceeds generated by the bonds are not actually result into green, eligible projects.27Berensmann, K. Ausweitung des Marktes für grüne Anleihen: die Notwendigkeit für harmonisierte Standards bei grünen Anleihen. (Analysen und Stellungnahmen, No. 13/2017, Deutsches Institut für Entwicklungspolitik (DIE), Bonn, 2017). <https://hdl.handle.net/10419/200034> According to Flammer (2021)24Flammer, C. Corporate green bonds. Journal of Financial Economics 142, 499-516 (2021). https://doi.org/10.1016/j.jfineco.2021.01.010, some practitioners have concerns about whether green bonds really make a difference, or whether companies are issuing green bonds for greenwashing motivations to improve their image. She posits that these reservations are founded upon the absence of public governance in relation to green bonds.24Flammer, C. Corporate green bonds. Journal of Financial Economics 142, 499-516 (2021). https://doi.org/10.1016/j.jfineco.2021.01.010 Another reason, according to Jäger et. al (2021)5Jäger, L., Ringel, M. & Schiereck, D. Green Bonds als Instrumente der Klimaschutzfinanzierung: Eine Literaturübersicht. Zeitschrift für Bankrecht und Bankwirtschaft 33, 209-225 (2021). https://doi.org/10.15375/zbb-2021-0307, is the non-binding rules for green bond standardisation. The existing standards, such as the ICMA’s GBP, are only voluntary guidelines with some room for manoeuvre.5Jäger, L., Ringel, M. & Schiereck, D. Green Bonds als Instrumente der Klimaschutzfinanzierung: Eine Literaturübersicht. Zeitschrift für Bankrecht und Bankwirtschaft 33, 209-225 (2021). https://doi.org/10.15375/zbb-2021-0307 However, Flammer (2021)24Flammer, C. Corporate green bonds. Journal of Financial Economics 142, 499-516 (2021). https://doi.org/10.1016/j.jfineco.2021.01.010 argues that there are alternative, less costly techniques for greenwashing. These include, for example, the use of questionable eco-labels and misleading visual representations.24Flammer, C. Corporate green bonds. Journal of Financial Economics 142, 499-516 (2021). https://doi.org/10.1016/j.jfineco.2021.01.010 Jäger et. al (2021)5Jäger, L., Ringel, M. & Schiereck, D. Green Bonds als Instrumente der Klimaschutzfinanzierung: Eine Literaturübersicht. Zeitschrift für Bankrecht und Bankwirtschaft 33, 209-225 (2021). https://doi.org/10.15375/zbb-2021-0307 thinks that there are clear obstacles for issuers that make abuse more difficult. If a bond goes through the entire process of a green bond framework, including full certification by a second party, greenwashing appears to be largely ruled out.5Jäger, L., Ringel, M. & Schiereck, D. Green Bonds als Instrumente der Klimaschutzfinanzierung: Eine Literaturübersicht. Zeitschrift für Bankrecht und Bankwirtschaft 33, 209-225 (2021). https://doi.org/10.15375/zbb-2021-0307 The third reason for issuing a green bond could be the cost of capital argument. According to Flammer (2021)24Flammer, C. Corporate green bonds. Journal of Financial Economics 142, 499-516 (2021). https://doi.org/10.1016/j.jfineco.2021.01.010, green bonds could be a more favourable source of financing compared to conventional bonds. The reason for this could be that investors in green bonds accept lower yields in return to making a contribution to mitigate the effects of climate change.24Flammer, C. Corporate green bonds. Journal of Financial Economics 142, 499-516 (2021). https://doi.org/10.1016/j.jfineco.2021.01.010 Whether the issuance of green bonds offers their issuers advantages in terms of financing costs is a question that is the subject of debate in the literature. In section 3.2.1, the debate will be examined in more detail and the results of previous research will be presented.

2.1.3.2 Investors

Investors are another key stakeholder group in the market. In order to make an investment decision regarding green bonds, investors need information that allows them to assess whether the bond actually fulfils environmental and green criteria and to what extent the proceeds contribute to a positive environmental impact.28OECD. Mobilising Bond Markets for a Low-Carbon Transition. Green Finance and Investment, (OECD Publishing, 2017). https://doi.org/10.1787/9789264272323-en

In the study conducted by Maltais & Nykvist (2020)7Maltais, A. & Nykvist, B. Understanding the role of green bonds in advancing sustainability. Journal of Sustainable Finance & Investment, 1-20 (2020). https://doi.org/10.1080/20430795.2020.1724864, the investors surveyed indicate that the majority of the incentives are non-financial in nature, as opposed to financial. The respondents indicate that their investment in green bonds is driven by a desire to enhance their appeal to customers. This is due to the fact that a considerable number of clients require companies to provide evidence of their contribution to sustainability. Financial incentives do not play a significant role in the majority of respondents’ investment decisions. However, green bonds are perceived as a potential means of mitigating risk in comparison to investing in conventional bonds. Furthermore, the responses indicate that the motivation for investing in green bonds was not driven by a desire for legitimacy or the influence of institutional pressure.7Maltais, A. & Nykvist, B. Understanding the role of green bonds in advancing sustainability. Journal of Sustainable Finance & Investment, 1-20 (2020). https://doi.org/10.1080/20430795.2020.1724864

In the study conducted by Sangiorgi & Schopohl (2021)29Sangiorgi, I. & Schopohl, L. Why do institutional investors buy green bonds: Evidence from a survey of European asset managers. International Review of Financial Analysis 75, 101738 (2021). https://doi.org/10.1016/j.irfa.2021.101738, three key decision criteria for investing in green bonds are identified. For investors, (1) the green credentials of the bond at the time of issuance, (2) the pricing of the bond and (3) the green credentials of the bond after issuance are of significant relevance.29Sangiorgi, I. & Schopohl, L. Why do institutional investors buy green bonds: Evidence from a survey of European asset managers. International Review of Financial Analysis 75, 101738 (2021). https://doi.org/10.1016/j.irfa.2021.101738 References that take into account the aspect of sustainability are of great importance for investors. The lack of such consideration means that investors are not interested in investing in corresponding bonds.29Sangiorgi, I. & Schopohl, L. Why do institutional investors buy green bonds: Evidence from a survey of European asset managers. International Review of Financial Analysis 75, 101738 (2021). https://doi.org/10.1016/j.irfa.2021.101738 These findings corroborate the signalling argument put forth by Flammer (2021)24Flammer, C. Corporate green bonds. Journal of Financial Economics 142, 499-516 (2021). https://doi.org/10.1016/j.jfineco.2021.01.010, which posit that green bond issuances serve as a signal for issuers’ green credentials and commitment in regard to environmental issues. Furthermore, adequate pricing of the green bond compared to a conventional bond is a key factor in investors’ decision-making.29Sangiorgi, I. & Schopohl, L. Why do institutional investors buy green bonds: Evidence from a survey of European asset managers. International Review of Financial Analysis 75, 101738 (2021). https://doi.org/10.1016/j.irfa.2021.101738 The green bond must therefore be competitive.29Sangiorgi, I. & Schopohl, L. Why do institutional investors buy green bonds: Evidence from a survey of European asset managers. International Review of Financial Analysis 75, 101738 (2021). https://doi.org/10.1016/j.irfa.2021.101738 However, this is in contrast to Flammer’s (2021)24Flammer, C. Corporate green bonds. Journal of Financial Economics 142, 499-516 (2021). https://doi.org/10.1016/j.jfineco.2021.01.010 cost of capital argument, as investors are unlikely to accept significantly higher prices for green bonds.

In 2019, the CBI (2019)30Climate Bonds Initiative (CBI). Green Bond European Investor Survey. CBI <https://www.climatebonds.net/files/files/GB_Investor_Survey-final.pdf> (2019) [accessed 29/05/2024]. conducted a survey of European green bond investors to ascertain their perceptions of the green bond market. This entails an analysis of the factors that could motivate investors to make green bond investments and thus promoting market growth. Investments are primarily aimed at making a high contribution to climate protection, with capital being channelled into those sectors where the greatest reductions in greenhouse gas emissions are required. The respondents indicate that there is a greater demand for issuance in the following sectors: industrials, energy and utilities, consumer cyclicals, and materials. Among the types of investment, investors prefer green bonds issued by non-financial corporates, followed financial corporate and sovereign issuers. In this survey, 93% of respondents state that they favour corporate issuance as an investment channel. The decision to invest in a green bond is significantly influenced by three criteria: green credentials at issuance, pricing and green credentials post-issuance.30Climate Bonds Initiative (CBI). Green Bond European Investor Survey. CBI <https://www.climatebonds.net/files/files/GB_Investor_Survey-final.pdf> (2019) [accessed 29/05/2024]. These criteria correspond to the previously presented results by Sangiorgi & Schopohl (2021)29Sangiorgi, I. & Schopohl, L. Why do institutional investors buy green bonds: Evidence from a survey of European asset managers. International Review of Financial Analysis 75, 101738 (2021). https://doi.org/10.1016/j.irfa.2021.101738. Moreover, respondents indicate that positive fundamentals of the issuer and transparency of the issuer, followed by transparency of the use of proceeds, are factors that make an investment in green bonds more interesting.30Climate Bonds Initiative (CBI). Green Bond European Investor Survey. CBI <https://www.climatebonds.net/files/files/GB_Investor_Survey-final.pdf> (2019) [accessed 29/05/2024].

2.2 Impacts of green bonds

This section presents an overview of the financial and environmental impacts of green bonds, as documented in the academic literature.

2.2.1 Financial impacts

The financial impact studies can be divided into three categories: Firstly, the impact on risk; secondly, the existence of a green bond premium, in particular whether green bonds have lower yields than conventional bonds; and thirdly, the reaction of the stock market to the announcement of a green bond. Furthermore, the impact of issuing a green bond on the issuer’s ownership structure has been analysed.

The question of whether green bonds are less risky than conventional bonds is one topic of interest. There are only a small number of studies in the academic literature that deal with the risk of the green bonds compared to conventional bonds.31Liu, M. The driving forces of green bond market volatility and the response of the market to the COVID-19 pandemic. Economic Analysis and Policy 75, 288-309 (2022). https://doi.org/10.1016/j.eap.2022.05.012 Most of the studies deal with the connectedness of the green bond market with other markets. Dong et al. (2023)32Dong, X., Xiong, Y., Nie, S. & Yoon, S.-M. Can bonds hedge stock market risks? Green bonds vs conventional bonds. Finance Research Letters 52, 103367 (2023). https://doi.org/10.1016/j.frl.2022.103367 analyse the effects of geopolitical, economic and climate policy risks on green bonds. Their findings indicate that green bonds, like conventional bonds, offer “a safe-haven function” (Dong et al., 2023, p.1)32Dong, X., Xiong, Y., Nie, S. & Yoon, S.-M. Can bonds hedge stock market risks? Green bonds vs conventional bonds. Finance Research Letters 52, 103367 (2023). https://doi.org/10.1016/j.frl.2022.103367 against high geopolitical risks. However, in the case of high economic and climate policy risks, green bonds perform better as a safe haven than conventional bonds. The authors also point out that integrating green bonds into an investment portfolio enables better hedging of risks as it leads to portfolio diversification.32Dong, X., Xiong, Y., Nie, S. & Yoon, S.-M. Can bonds hedge stock market risks? Green bonds vs conventional bonds. Finance Research Letters 52, 103367 (2023). https://doi.org/10.1016/j.frl.2022.103367 Reboredo (2018)33Reboredo, J. C. Green bond and financial markets: Co-movement, diversification and price spillover effects. Energy Economics 74, 38-50 (2018). https://doi.org/10.1016/j.eneco.2018.05.030 analyse the correlation between the green bond market and other financial markets. For investors, the diversification of their investment portfolio is of significant importance in order to minimise risk. As part of the analysis, the co-movements of the green bond market with the corporate and treasury bond markets, the equity markets and the energy markets were examined. The analysis demonstrates that the green bond market is symmetrically dependent on the corporate and treasury bond markets. He states that an investment in the green bond market does not provide any significant diversification advantages for investors who already invest in the corporate and treasury bond markets. However, there is a relatively weak symmetrical dependence of the green bond market on the equity markets and independence from the energy markets. Reboredo (2018)33Reboredo, J. C. Green bond and financial markets: Co-movement, diversification and price spillover effects. Energy Economics 74, 38-50 (2018). https://doi.org/10.1016/j.eneco.2018.05.030 concludes that there are diversification advantages for investors who already invest in stocks and energy markets. Liu (2022)31Liu, M. The driving forces of green bond market volatility and the response of the market to the COVID-19 pandemic. Economic Analysis and Policy 75, 288-309 (2022). https://doi.org/10.1016/j.eap.2022.05.012 demonstrate that the market for green bonds responded to the COVID-19 pandemic in a manner analogous to that observed in the conventional bond market. In extreme conditions, such as those caused by the pandemic, the green bond market exhibits high negative yields, as does the conventional bond market. Liu (2022)31Liu, M. The driving forces of green bond market volatility and the response of the market to the COVID-19 pandemic. Economic Analysis and Policy 75, 288-309 (2022). https://doi.org/10.1016/j.eap.2022.05.012 observed that there is a co-movement between the green bond market and the corporate and treasury bond market with regard to volatility, which is consistent with the findings of Reboredo (2018)33Reboredo, J. C. Green bond and financial markets: Co-movement, diversification and price spillover effects. Energy Economics 74, 38-50 (2018). https://doi.org/10.1016/j.eneco.2018.05.030. Furthermore, Liu (2022)31Liu, M. The driving forces of green bond market volatility and the response of the market to the COVID-19 pandemic. Economic Analysis and Policy 75, 288-309 (2022). https://doi.org/10.1016/j.eap.2022.05.012 document that fluctuations in the energy market have no discernible effect on the green bond market.

A key topic of the academic debate is the existence of a green bond premium. The term ‘green bond premium’ is used to describe the difference in yield between a green bond and a conventional bond with comparable characteristics.34MacAskill, S., Roca, E., Liu, B., Stewart, R. A. & Sahin, O. Is there a green premium in the green bond market? Systematic literature review revealing premium determinants. Journal of Cleaner Production 280, 124491 (2021). https://doi.org/10.1016/j.jclepro.2020.124491 A negative premium describes that green bonds are issued or traded at lower yields than comparable conventional bonds, also known as a greenium. “A ‘greenium’ implies that the yield an investor is willing to accept for a ‘green’ asset is lower than that of conventional counterparts.” (MacAskill et al., 2021, p.1)34MacAskill, S., Roca, E., Liu, B., Stewart, R. A. & Sahin, O. Is there a green premium in the green bond market? Systematic literature review revealing premium determinants. Journal of Cleaner Production 280, 124491 (2021). https://doi.org/10.1016/j.jclepro.2020.124491. A negative premium can offset the additional costs for the process of issuing a green bond, such as the monitoring and reporting of the use of proceeds or the certification process.35Fatica, S., Panzica, R. & Rancan, M. The pricing of green bonds: Are financial institutions special? Journal of Financial Stability 54, 100873 (2021). https://doi.org/10.1016/j.jfs.2021.100873 In terms of additional costs, the CBI’s certification process is estimated to cost around.1Copernicus Climate Change Service. Surface air temperature for June 2024. Copernicus <https://climate.copernicus.eu/surface-air-temperature-june-2024> (2024) [accessed 14.08.2024]. basis points (bps) and reporting costs are estimated to be between.5Jäger, L., Ringel, M. & Schiereck, D. Green Bonds als Instrumente der Klimaschutzfinanzierung: Eine Literaturübersicht. Zeitschrift für Bankrecht und Bankwirtschaft 33, 209-225 (2021). https://doi.org/10.15375/zbb-2021-0307 and 3 bps.34MacAskill, S., Roca, E., Liu, B., Stewart, R. A. & Sahin, O. Is there a green premium in the green bond market? Systematic literature review revealing premium determinants. Journal of Cleaner Production 280, 124491 (2021). https://doi.org/10.1016/j.jclepro.2020.124491 A positive green bond premium describes that green bonds are issued or traded at higher yields in comparison to comparable conventional bonds. The field of green bond premium research has grown considerably in recent years.36Cortellini, G. & Panetta, I. C. Green Bond: A Systematic Literature Review for Future Research Agendas. Journal of Risk and Financial Management 14, 589 (2021). https://doi.org/10.3390/jrfm14120589 The results of the studies on the existence of a green bond premium vary widely. Some studies document the existence of a negative premium. These include, for example, the studies by Karpf & Mandel (2018)37Karpf, A. & Mandel, A. The changing value of the ‘green’ label on the US municipal bond market. Nature Climate Change 8, 161-165 (2018). https://doi.org/10.1038/s41558-017-0062-0, Zerbib (2019)38Zerbib, O. D. The effect of pro-environmental preferences on bond prices: Evidence from green bonds. Journal of Banking and Finance 98, 39-60 (2019). https://doi.org/10.1016/j.jbankfin.2018.10.012, Gianfrate & Peri (2019)39Gianfrate, G. & Peri, M. The green advantage: Exploring the convenience of issuing green bonds. Journal of Cleaner Production 219, 127-135 (2019). https://doi.org/10.1016/j.jclepro.2019.02.022 and Fatica et al. (2021)35Fatica, S., Panzica, R. & Rancan, M. The pricing of green bonds: Are financial institutions special? Journal of Financial Stability 54, 100873 (2021). https://doi.org/10.1016/j.jfs.2021.100873. Other studies find controversial evidence of the existence of a green bond premium, like Hachenberg & Schiereck (2018)18Hachenberg, B. & Schiereck, D. Are green bonds priced differently from conventional bonds? Journal of Asset Management 19, 371-383 (2018). https://doi.org/10.1057/s41260-018-0088-5, Tang & Zhang (2020)11Tang, D. Y. & Zhang, Y. Do shareholders benefit from green bonds? Journal of Corporate Finance 61, 101427 (2020). https://doi.org/10.1016/j.jcorpfin.2018.12.001 and Hyun et al. (2020)25Hyun, S., Park, D. & Tian, S. The price of going green: the role of greenness in green bond markets. Accounting & Finance 60, 73-95 (2020). https://doi.org/10.1111/acfi.12515. However, other studies show that there are no statistically significant differences between green bonds and comparable conventional bonds. These include, for example, the studies by Larcker & Watts (2020)40Larcker, D. F. & Watts, E. M. Where’s the greenium? Journal of Accounting and Economics 69, 101312 (2020). https://doi.org/10.1016/j.jacceco.2020.101312 and Flammer (2021)24Flammer, C. Corporate green bonds. Journal of Financial Economics 142, 499-516 (2021). https://doi.org/10.1016/j.jfineco.2021.01.010. Table 3 below presents the results of eight studies investigating the existence of a green bond premium.

The study by Hachenberg & Schiereck (2018)18Hachenberg, B. & Schiereck, D. Are green bonds priced differently from conventional bonds? Journal of Asset Management 19, 371-383 (2018). https://doi.org/10.1057/s41260-018-0088-5 is centred on green bonds, with a particular focus on the ratings assigned to them. The results demonstrate that AA-, A- and BBB-rated green bonds traded tighter than their comparable conventional green bonds. Conversely, only AAA-rated green bonds traded.41Wang, J., Chen, X., Li, X., Yu, J. & Zhong, R. The market reaction to green bond issuance: Evidence from China. Pacific-Basin Finance Journal 60, 101294 (2020). https://doi.org/10.1016/j.pacfin.2020.101294 bps wider. Overall, they find a small negative green bond premium of -1,18 bps on average.18Hachenberg, B. & Schiereck, D. Are green bonds priced differently from conventional bonds? Journal of Asset Management 19, 371-383 (2018). https://doi.org/10.1057/s41260-018-0088-5 In contrast, Zerbib (2019)38Zerbib, O. D. The effect of pro-environmental preferences on bond prices: Evidence from green bonds. Journal of Banking and Finance 98, 39-60 (2019). https://doi.org/10.1016/j.jbankfin.2018.10.012 observes that green bonds with lower ratings have a more negative premium. Karpf & Mandel (2018)37Karpf, A. & Mandel, A. The changing value of the ‘green’ label on the US municipal bond market. Nature Climate Change 8, 161-165 (2018). https://doi.org/10.1038/s41558-017-0062-0 identify a negative premium of -7.34MacAskill, S., Roca, E., Liu, B., Stewart, R. A. & Sahin, O. Is there a green premium in the green bond market? Systematic literature review revealing premium determinants. Journal of Cleaner Production 280, 124491 (2021). https://doi.org/10.1016/j.jclepro.2020.124491 bps on the secondary market of the US municipal bond market. Similarly to Karpf & Mandel (2018)37Karpf, A. & Mandel, A. The changing value of the ‘green’ label on the US municipal bond market. Nature Climate Change 8, 161-165 (2018). https://doi.org/10.1038/s41558-017-0062-0, Larcker & Watts (2020)40Larcker, D. F. & Watts, E. M. Where’s the greenium? Journal of Accounting and Economics 69, 101312 (2020). https://doi.org/10.1016/j.jacceco.2020.101312 conduct an analysis of green bonds from US municipal issuers, but in this case, they focus on the primary market. In order to identify comparable bonds, precise specifications were defined for the matching method. They specify that a pair of green and non-green bonds must be issued by the same municipality on the same day, have the same maturity and rating. A positive difference of 0.45 bps was observed between the yields of green and comparable non-green bonds. However, in 85% of the matched cases, the difference in yield is exactly zero. As a result, they conclude that the premium is exactly zero.40Larcker, D. F. & Watts, E. M. Where’s the greenium? Journal of Accounting and Economics 69, 101312 (2020). https://doi.org/10.1016/j.jacceco.2020.101312 These findings differ from those previously reported by Karpf & Mandel (2018)37Karpf, A. & Mandel, A. The changing value of the ‘green’ label on the US municipal bond market. Nature Climate Change 8, 161-165 (2018). https://doi.org/10.1038/s41558-017-0062-0. Zerbib (2019)38Zerbib, O. D. The effect of pro-environmental preferences on bond prices: Evidence from green bonds. Journal of Banking and Finance 98, 39-60 (2019). https://doi.org/10.1016/j.jbankfin.2018.10.012 investigates the potential influence of environmental preferences on the pricing of green bonds. His findings indicate a negative green bond premium of -2 bps, thereby demonstrating that the influence of investors’ pro-environmental preferences is relatively limited with respect to bond prices. He posits that the lower cost of debt for companies with good environmental performance is primarily a result of lower financial risk rather than investors’ non-financial preferences.38Zerbib, O. D. The effect of pro-environmental preferences on bond prices: Evidence from green bonds. Journal of Banking and Finance 98, 39-60 (2019). https://doi.org/10.1016/j.jbankfin.2018.10.012 Gianfrate & Peri (2019)39Gianfrate, G. & Peri, M. The green advantage: Exploring the convenience of issuing green bonds. Journal of Cleaner Production 219, 127-135 (2019). https://doi.org/10.1016/j.jclepro.2019.02.022 distinguish between corporate and non-corporate green bonds in their study. They find a negative green bond premium in the primary market of -21 bps on average for corporate green bonds and -15 bps on average for non-corporate green bonds. On the secondary market they also find a negative, but the evidence is stronger in the primary market.39Gianfrate, G. & Peri, M. The green advantage: Exploring the convenience of issuing green bonds. Journal of Cleaner Production 219, 127-135 (2019). https://doi.org/10.1016/j.jclepro.2019.02.022 Tang & Zhang (2020)11Tang, D. Y. & Zhang, Y. Do shareholders benefit from green bonds? Journal of Corporate Finance 61, 101427 (2020). https://doi.org/10.1016/j.jcorpfin.2018.12.001 find on average a negative green bond premium of -6.94 bps. Nevertheless, when the comparison is restricted to green bonds from the same issuing firm and issue year, no notable price discrepancy was discerned.11Tang, D. Y. & Zhang, Y. Do shareholders benefit from green bonds? Journal of Corporate Finance 61, 101427 (2020). https://doi.org/10.1016/j.jcorpfin.2018.12.001 Flammer (2021)24Flammer, C. Corporate green bonds. Journal of Financial Economics 142, 499-516 (2021). https://doi.org/10.1016/j.jfineco.2021.01.010 analyses corporate green bonds and compares the yields of these green bonds with the most comparable conventional bonds of the same issuer, using the matching method as in Larcker & Watts (2020)40Larcker, D. F. & Watts, E. M. Where’s the greenium? Journal of Accounting and Economics 69, 101312 (2020). https://doi.org/10.1016/j.jacceco.2020.101312. She concludes that there is no green bond premium, as she could not find any statistically relevant differences between the yields of green and conventional bonds.24Flammer, C. Corporate green bonds. Journal of Financial Economics 142, 499-516 (2021). https://doi.org/10.1016/j.jfineco.2021.01.010 These results are consistent with those of Larcker & Watts (2020)40Larcker, D. F. & Watts, E. M. Where’s the greenium? Journal of Accounting and Economics 69, 101312 (2020). https://doi.org/10.1016/j.jacceco.2020.101312, and contradict the findings of Gianfrate & Peri (2019)39Gianfrate, G. & Peri, M. The green advantage: Exploring the convenience of issuing green bonds. Journal of Cleaner Production 219, 127-135 (2019). https://doi.org/10.1016/j.jclepro.2019.02.022 on corporate green bonds. Caramichael & Rapp (2024)6Caramichael, J. & Rapp, A. C. The green corporate bond issuance premium. Journal of Banking & Finance 162, 107126 (2024). https://doi.org/10.1016/j.jbankfin.2024.107126 study also the corporate green bond market and find a negative premium between -3 bps and -8 bps on the primary market.

Table 3: Overview of studies on the existence of a green bond premium, own illustration

| Author(s) and Year | Time Period | Geographical Area – Market | Sample Size | Existence of a Greenium? | Premium Dimension |

| Hachenberg & Schiereck (2018)18Hachenberg, B. & Schiereck, D. Are green bonds priced differently from conventional bonds? Journal of Asset Management 19, 371-383 (2018). https://doi.org/10.1057/s41260-018-0088-5 | 10/2015 – 03/2016 | worldwide – secondary market | 63 | Controversial | -1.18 bps on average |

| Karpf & Mandel (2018)37Karpf, A. & Mandel, A. The changing value of the ‘green’ label on the US municipal bond market. Nature Climate Change 8, 161-165 (2018). https://doi.org/10.1038/s41558-017-0062-0 | 2010 – 2016 | US municipal – secondary market | 1,880 | Yes | -7.8 bps |

| Zerbib (2019)38Zerbib, O. D. The effect of pro-environmental preferences on bond prices: Evidence from green bonds. Journal of Banking and Finance 98, 39-60 (2019). https://doi.org/10.1016/j.jbankfin.2018.10.012 | 07/2013 – 12/2017 | worldwide – secondary market | 110 | Yes | -2 bps |

| Gianfrate & Peri (2019)39Gianfrate, G. & Peri, M. The green advantage: Exploring the convenience of issuing green bonds. Journal of Cleaner Production 219, 127-135 (2019). https://doi.org/10.1016/j.jclepro.2019.02.022 | 2013 – 2017 | EU – primary and secondary market | 121 | Yes | -17 bps on average in primary market between -5 bps and -13.9 bps in secondary market |

| Larcker & Watts (2020)40Larcker, D. F. & Watts, E. M. Where’s the greenium? Journal of Accounting and Economics 69, 101312 (2020). https://doi.org/10.1016/j.jacceco.2020.101312 | 06/2013 – 07/2018 | US municipal – primary market | 640 | No | +0.45 bps, but not significant |

| Tang & Zhang (2020)11Tang, D. Y. & Zhang, Y. Do shareholders benefit from green bonds? Journal of Corporate Finance 61, 101427 (2020). https://doi.org/10.1016/j.jcorpfin.2018.12.001 | 2007 – 2017 | worldwide – primary market | 1,510 | Controversial | -6.94 bps, but no premium when the comparison is restricted to the same issuer and same issue year |

| Flammer (2021)24Flammer, C. Corporate green bonds. Journal of Financial Economics 142, 499-516 (2021). https://doi.org/10.1016/j.jfineco.2021.01.010 | 2013 – 2018 | worldwide – secondary market | 152 | No | |

| Caramichael & Rapp (2024)6Caramichael, J. & Rapp, A. C. The green corporate bond issuance premium. Journal of Banking & Finance 162, 107126 (2024). https://doi.org/10.1016/j.jbankfin.2024.107126 | 2014 – 2021 | worldwide – primary market | 1,169 | Yes | between -3 bps and -8 bps |

Furthermore, other studies are analysing the factors and drivers that influence the green bond premium alongside the existence of the premium. In a study conducted by Agliardi & Agliardi (2019)42Agliardi, E. & Agliardi, R. Financing environmentally-sustainable projects with green bonds. Environment and Development Economics 24, 608-623 (2019). https://doi.org/10.1017/S1355770X19000020, the impact of green bond volatility, parameters for green technologies and sustainability, and tax rates on the greenium is examined. The results show “that the greenium is increased if asset volatility increases, the parameters governing the green technology and the sustainability advantage increase, and corporate tax rates are decreased” (Agliardi & Agliardi, 2019, p. 622)42Agliardi, E. & Agliardi, R. Financing environmentally-sustainable projects with green bonds. Environment and Development Economics 24, 608-623 (2019). https://doi.org/10.1017/S1355770X19000020. Fatica et al. (2021)35Fatica, S., Panzica, R. & Rancan, M. The pricing of green bonds: Are financial institutions special? Journal of Financial Stability 54, 100873 (2021). https://doi.org/10.1016/j.jfs.2021.100873 analyse the different types of issuers and find that both supranational institutions and non-financial corporates show a yield difference when issuing green bonds. The difference is -80 bps for green bonds issued by supranational institutions and -22 bps for green bonds issued by non-financial corporates. They consider that the high yield difference on green bonds issued by supranational institutions is due to their high reputation. However, they identify no statistically significant yield differences for green bonds issued by financial companies. They assume that this has to do with the fact that it is difficult for financial corporates to link green bonds directly to specific projects.35Fatica, S., Panzica, R. & Rancan, M. The pricing of green bonds: Are financial institutions special? Journal of Financial Stability 54, 100873 (2021). https://doi.org/10.1016/j.jfs.2021.100873 Kapraun et al. (2021)43Kapraun, J., Latino, C., Scheins, C. & Schlag, C. (In)-credibly green: Which bonds trade at a green bond premium? in Proceedings of Paris December 2019 Finance Meeting EUROFIDAI-ESSEC (2021). https://doi.org/10.2139/ssrn.3347337 also document that the green bond premium shows a high variance across the types of issuers and currencies. The negative premium is particularly higher for green bonds issued by public institutions and for green bonds issued in EUR.43Kapraun, J., Latino, C., Scheins, C. & Schlag, C. (In)-credibly green: Which bonds trade at a green bond premium? in Proceedings of Paris December 2019 Finance Meeting EUROFIDAI-ESSEC (2021). https://doi.org/10.2139/ssrn.3347337 Hyun et al. (2020)25Hyun, S., Park, D. & Tian, S. The price of going green: the role of greenness in green bond markets. Accounting & Finance 60, 73-95 (2020). https://doi.org/10.1111/acfi.12515 initially find no evidence of a positive or negative green bond premium in their study. However, after filtering the green bonds with an independent reviewer or CBI certification, they observe a reduction in the green bond premium of 6 to 15 bps.25Hyun, S., Park, D. & Tian, S. The price of going green: the role of greenness in green bond markets. Accounting & Finance 60, 73-95 (2020). https://doi.org/10.1111/acfi.12515 The following study by Hyun et al. (2021)26Hyun, S., Park, D. & Tian, S. Pricing of Green Labeling: A Comparison of Labeled and Unlabeled Green Bonds. Finance Research Letters 41, 101816 (2021). https://doi.org/10.1016/j.frl.2020.101816 investigates the impact of green labels on the price relative to comparable green bonds without a green label. The results show that the yield of green bonds with labels is 24 to 36 bps lower than the yield of green bonds without labels.26Hyun, S., Park, D. & Tian, S. Pricing of Green Labeling: A Comparison of Labeled and Unlabeled Green Bonds. Finance Research Letters 41, 101816 (2021). https://doi.org/10.1016/j.frl.2020.101816 In addition, the findings of Kapraun et al. (2021)43Kapraun, J., Latino, C., Scheins, C. & Schlag, C. (In)-credibly green: Which bonds trade at a green bond premium? in Proceedings of Paris December 2019 Finance Meeting EUROFIDAI-ESSEC (2021). https://doi.org/10.2139/ssrn.3347337 indicates that certified green bonds of corporates offer a considerably lower yield, approximately 24 bps below that of comparable conventional bonds.43Kapraun, J., Latino, C., Scheins, C. & Schlag, C. (In)-credibly green: Which bonds trade at a green bond premium? in Proceedings of Paris December 2019 Finance Meeting EUROFIDAI-ESSEC (2021). https://doi.org/10.2139/ssrn.3347337 Allman & Lock (2024)44Allman, E. & Lock, B. External reviews and green bond credibility. Journal of Climate Finance 7, 100036 (2024). https://doi.org/10.1016/j.jclimf.2024.100036 also analyse the impact of an external review on the green bond premium. Their results show that the external review does not have a significant impact on the green bond premium. They conclude, that externally reviewed green bonds are not issued with lower yields compared to comparable conventional bonds.44Allman, E. & Lock, B. External reviews and green bond credibility. Journal of Climate Finance 7, 100036 (2024). https://doi.org/10.1016/j.jclimf.2024.100036 These results are in contrast to the results reported by Kapraun et al. (2021)43Kapraun, J., Latino, C., Scheins, C. & Schlag, C. (In)-credibly green: Which bonds trade at a green bond premium? in Proceedings of Paris December 2019 Finance Meeting EUROFIDAI-ESSEC (2021). https://doi.org/10.2139/ssrn.3347337 and Hyun et al. (2020)25Hyun, S., Park, D. & Tian, S. The price of going green: the role of greenness in green bond markets. Accounting & Finance 60, 73-95 (2020). https://doi.org/10.1111/acfi.12515. Li et al. (2020)45Li, Z., Tang, Y., Wu, J., Zhang, J. & Lv, Q. The Interest Costs of Green Bonds: Credit Ratings, Corporate Social Responsibility, and Certification. Emerging Markets Finance & Trade 56, 2679-2692 (2020). https://doi.org/10.1080/1540496X.2018.1548350 study the factors that influence the pricing of a green bond, in particular the interest cost. In their study, the researchers focus on the Chinese market for green bonds. In conclusion, their findings indicate “that certified green bonds with higher credit ratings or higher CSR scores have lower yield spreads and interest costs” (Li et al., 2020, p. 2687)45Li, Z., Tang, Y., Wu, J., Zhang, J. & Lv, Q. The Interest Costs of Green Bonds: Credit Ratings, Corporate Social Responsibility, and Certification. Emerging Markets Finance & Trade 56, 2679-2692 (2020). https://doi.org/10.1080/1540496X.2018.1548350. Furthermore, they argue that the advantages of certification outweigh the expenses associated with the certification process.45Li, Z., Tang, Y., Wu, J., Zhang, J. & Lv, Q. The Interest Costs of Green Bonds: Credit Ratings, Corporate Social Responsibility, and Certification. Emerging Markets Finance & Trade 56, 2679-2692 (2020). https://doi.org/10.1080/1540496X.2018.1548350

Overall, it is not possible to draw a universally valid conclusion regarding the existence of a green premium. A variety of factors influence the existence and amount of a negative green bond premium, including the timing of the issue, the type of issuer and the choice of an external review. Larcker & Watts (2020)40Larcker, D. F. & Watts, E. M. Where’s the greenium? Journal of Accounting and Economics 69, 101312 (2020). https://doi.org/10.1016/j.jacceco.2020.101312 argue that the significant discrepancies in the findings of prior studies regarding the existence and amount of a green bond premium are “the result of methodological design misspecifications that produce biased estimates” (Larcker & Watts, 2020, p. 4)40Larcker, D. F. & Watts, E. M. Where’s the greenium? Journal of Accounting and Economics 69, 101312 (2020). https://doi.org/10.1016/j.jacceco.2020.101312.

Other studies analyse the impact of the issue or announcement of a green bond on the stock market. Tang and Zhang (2020)11Tang, D. Y. & Zhang, Y. Do shareholders benefit from green bonds? Journal of Corporate Finance 61, 101427 (2020). https://doi.org/10.1016/j.jcorpfin.2018.12.001 study the reaction of the stock market to the announcement of a green bond in their study. They define the announcement day as day 0. The results of the event windows of [-10,10] days show a positive stock market reaction with a cumulative abnormal return (CAR) of 1.39 %, while a CAR of 1.39 % is observed for the event windows of [-5,10] days. Subsequently, they analyse which types of issuers are most likely to experience a stock market reaction to the issuance of a green bond. They differentiate between corporates and financial institutions. The results of the study show that the reaction of the stock market to the issue of green bonds by corporates is statistically significant, while the reaction in relation to financial institutions is not significant.11Tang, D. Y. & Zhang, Y. Do shareholders benefit from green bonds? Journal of Corporate Finance 61, 101427 (2020). https://doi.org/10.1016/j.jcorpfin.2018.12.001 In addition, Flammer (2021)24Flammer, C. Corporate green bonds. Journal of Financial Economics 142, 499-516 (2021). https://doi.org/10.1016/j.jfineco.2021.01.010 was able to prove that the stock market reacts statistically significant and positively to the announcement and issue of a green bond. Day 0 is defined as the announcement day, whereby a positive reaction of the stock market is observed in the event window of [-5,10] days with an average CAR of 0,49%. Her findings demonstrate that the stock market reaction is more pronounced for certified green bonds and first-time issuers, which corroborates her signalling argument.24Flammer, C. Corporate green bonds. Journal of Financial Economics 142, 499-516 (2021). https://doi.org/10.1016/j.jfineco.2021.01.010 Wang et al. (2020)41Wang, J., Chen, X., Li, X., Yu, J. & Zhong, R. The market reaction to green bond issuance: Evidence from China. Pacific-Basin Finance Journal 60, 101294 (2020). https://doi.org/10.1016/j.pacfin.2020.101294 also observe an abnormal and statistically significant increase in stock returns during a two-day period following the announcement of a green bond issue, as evidenced by their analysis of the green bond market in China. The authors posit that the stock market responds more favourably to the announcement of a green bond issue than to the announcement of a conventional bond issue.41Wang, J., Chen, X., Li, X., Yu, J. & Zhong, R. The market reaction to green bond issuance: Evidence from China. Pacific-Basin Finance Journal 60, 101294 (2020). https://doi.org/10.1016/j.pacfin.2020.101294

Furthermore, the impact of issuing green bonds on the ownership structure of the green bond issuer is analysed in the studies of Tang & Zhang (2020)11Tang, D. Y. & Zhang, Y. Do shareholders benefit from green bonds? Journal of Corporate Finance 61, 101427 (2020). https://doi.org/10.1016/j.jcorpfin.2018.12.001 and Flammer (2021)24Flammer, C. Corporate green bonds. Journal of Financial Economics 142, 499-516 (2021). https://doi.org/10.1016/j.jfineco.2021.01.010. The study conducted by Tang and Zhang (2020)11Tang, D. Y. & Zhang, Y. Do shareholders benefit from green bonds? Journal of Corporate Finance 61, 101427 (2020). https://doi.org/10.1016/j.jcorpfin.2018.12.001 finds that institutional ownership raises by 7.9% after a green bond issue compared to a conventional bond. They also analysed whether there are differences between domestic and foreign institutional investors. The findings demonstrate that only domestic investors exhibit a notable increase in their holdings in companies when green bonds are issued with an observed rise of 7.6% and 8.5 %, respectively. Conversely, no significant change in holdings was observed among foreign investors.11Tang, D. Y. & Zhang, Y. Do shareholders benefit from green bonds? Journal of Corporate Finance 61, 101427 (2020). https://doi.org/10.1016/j.jcorpfin.2018.12.001 In her study, Flammer (2021)24Flammer, C. Corporate green bonds. Journal of Financial Economics 142, 499-516 (2021). https://doi.org/10.1016/j.jfineco.2021.01.010 analysed the ownership structure of US companies and concluded that the increase in institutional ownership is statistically insignificant. However, the study shows that the share of both long-term and green investors increased significantly when a green bond was issued. The share of long-term investors increased by 1.8% – 2.2%, while the share of green investors increased by 2.9%.24Flammer, C. Corporate green bonds. Journal of Financial Economics 142, 499-516 (2021). https://doi.org/10.1016/j.jfineco.2021.01.010 To summarise, the findings on the ownership structure indicate that the introduction of a green bond leads to increased investor interest and the development of a more diverse investor base.11Tang, D. Y. & Zhang, Y. Do shareholders benefit from green bonds? Journal of Corporate Finance 61, 101427 (2020). https://doi.org/10.1016/j.jcorpfin.2018.12.001,24Flammer, C. Corporate green bonds. Journal of Financial Economics 142, 499-516 (2021). https://doi.org/10.1016/j.jfineco.2021.01.010

2.2.2 Ecological impacts

Another academic debate exists about the impact of green bonds on environmental performance of the issuing companies.