Authors: Melanie Bootsmann

Edited by: Fynn Ermen, Eric Keller, Jonas Strauch, Ole Sütering, Laura Köhler, Jasna Ruge, Larissa Gerold, Philine Jörgensen, Lisann Kühling, Katharina Ros

Last updated: April 8, 2026

Executive summary

The European Sustainability Reporting Standards (ESRS) establish a mandatory framework for sustainability reporting under the Corporate Sustainability Reporting Directive (CSRD). They aim to harmonize ESG disclosures across the EU, improving comparability, reliability, and transparency.

Key elements include two cross-cutting standards and ten topical standards covering environmental, social, and governance aspects. ESRS introduces double materiality, requiring companies to report both on their impacts on sustainability and on how sustainability issues affect financial performance.

The first set of ESRS, effective from 2024, includes 82 disclosure requirements categorized into policies, actions, targets, and metrics. It emphasizes materiality assessment, value chain inclusion, and connectivity between sustainability and financial reporting.

Future developments will add sector-specific standards and guidance for SMEs. ESRS also integrates with other EU regulations such as the Taxonomy Regulation and the Corporate Sustainability Due Diligence Directive. External audits ensure compliance and reliability.

Overall, ESRS represents a significant step toward standardized sustainability reporting, supporting informed decision-making and advancing the EU’s sustainability agenda.

1 Introduction

In 2014, the European Parliament Directive 2014/95/EU has adopted, which leads to an obligation of public interest entities to provide information.1Kamenšek, D. & Gornjak, M. Organisational Reporting in the EU on Sustainability. Journal of Accounting and Management 13, 77-90 (2023).,2Korca, B. & Costa, E. Directive 2014/95/EU: building a research agenda. Journal of Applied Accounting Research 22, 401-422 (2021).. However, said directive did not further specify a certain reporting form.1Kamenšek, D. & Gornjak, M. Organisational Reporting in the EU on Sustainability. Journal of Accounting and Management 13, 77-90 (2023). As conclusion, large organizations decided to create non-binding reporting rules as solution for the missing definition.1Kamenšek, D. & Gornjak, M. Organisational Reporting in the EU on Sustainability. Journal of Accounting and Management 13, 77-90 (2023).

At European level, several institutions are promoting better mechanisms to deal with present and possible future crises like social inequalities, or the preservation of the environment, since traditional accounting systems of public and private entities still fail to capture these issues into actual figures and narratives. Therefore, in order to face these challenges, several families of indicators have emerged.3Barroso, J. G., Muñoz, F. F., García, A. J. B., Valentinetti, D. & de la Cruz Modino, R. The Role of Sustainability Indicators in Managing State-Owned Enterprises at the Regional Level: An Exploration on Disclosures for Better Policymaking in Financing Regions Toward Sustainability in the Midst of Climate Change Risks and Uncertainty (eds Beata Zofia Filipiak, Dominika Kordela, & Izabela Nawrolska) 221-234 (IGI Global, 2023).

Nowadays, the idea of a “Sustainability Corporate Governance” supposed to be realized in practice.4Baumüller, J. & Scheid, O. Die European Sustainability Reporting Standards (ESRS) als Zeitenwende für die Unternehmensberichterstattung?: Implikationen für den Mittelstand. StuB-Unternehmensteuern und Bilanzen 25, 742-747 (2023). The Corporate Sustainability Reporting Directive now requires all companies to report in accordance with the European Sustainability Reporting Standards (ESRS), therefore solving the problem of the not defined reporting form.5Ribeiro, C. & Carmo, C. Business Conduct Incidents: Promoting Transparency Through Sustainability Standardsin Addressing Corporate Scandals and Transgressions Through Governance and Social Responsibility 141-176 (IGI Global, 2023). Furthermore, it supposed to lead to a harmonization of sustainability reporting across the European Union and to an increase in comparability and relevance of the information reported, as well as in completeness and reliability4Baumüller, J. & Scheid, O. Die European Sustainability Reporting Standards (ESRS) als Zeitenwende für die Unternehmensberichterstattung?: Implikationen für den Mittelstand. StuB-Unternehmensteuern und Bilanzen 25, 742-747 (2023).,5Ribeiro, C. & Carmo, C. Business Conduct Incidents: Promoting Transparency Through Sustainability Standardsin Addressing Corporate Scandals and Transgressions Through Governance and Social Responsibility 141-176 (IGI Global, 2023).. This way it deals with the key criticisms of the current reporting practices of European companies.

The CSRD regulates the new obligations’ scope of application and their context-regulations, including e.g. the disclosure and the external audit.4Baumüller, J. & Scheid, O. Die European Sustainability Reporting Standards (ESRS) als Zeitenwende für die Unternehmensberichterstattung?: Implikationen für den Mittelstand. StuB-Unternehmensteuern und Bilanzen 25, 742-747 (2023). Since CSRD only broaches the reporting content, ESRS has created to further concretize the demanded information.4Baumüller, J. & Scheid, O. Die European Sustainability Reporting Standards (ESRS) als Zeitenwende für die Unternehmensberichterstattung?: Implikationen für den Mittelstand. StuB-Unternehmensteuern und Bilanzen 25, 742-747 (2023). ESRS will ensure standardization through creating a consistent and comparable sustainability reporting language across Europe4Baumüller, J. & Scheid, O. Die European Sustainability Reporting Standards (ESRS) als Zeitenwende für die Unternehmensberichterstattung?: Implikationen für den Mittelstand. StuB-Unternehmensteuern und Bilanzen 25, 742-747 (2023).,6Schnabel, J., Bareth, M. & Rathfelder, A. CSRD: Wettbewerbsnachteil oder Chance für den Mittelstand? PiR-Internationale Rechnungslegung, 242-250 (2023).. It is considered to be a crucial component of EU’s effort to standardise ESG reporting, representing the center of the EU’s sustainability drive and propelling its ESG journey.7Foley, M. Looking to the ESRS for clues on the future of ESG regulation International Financial Law Review (2023).,8Adam, O. Education and resourcing crucial to mastering Europe’s ESRS. International Financial Law Review(2023).

More precisely, ESG reporting is known as sustainability reporting with a focus on the environment, society and governance of the company. The covered environmental topics answer questions on how exposed an organization is and how it manages risks and chances concerning among others climate, scarcity of natural resources, pollution waste and more. It also describes how the organization impacts the environment with its activities. Societal topics show the companies’ values and principles, the societal issues like labor and supply chain information, production quality and safety as well as human capital issues like employee health, safety, diversity, inclusion efforts and policies. Last, governance includes data on organizations’ corporate governance and information on the composition and diversity of the board of directors, executive compensation, bribery, corruption and more.1Kamenšek, D. & Gornjak, M. Organisational Reporting in the EU on Sustainability. Journal of Accounting and Management 13, 77-90 (2023).

With the ESRS the organization EFRAG has developed a literal guidebook of 10 approved final draft standards addressing all aspects of ESG, hence becoming a fixture of future legislation and showing what aspects on ESG will be focused on. ESRS will become standards for global ESG reporting, with also round about 10,000 foreign companies predicted to be affected by these rules.7Foley, M. Looking to the ESRS for clues on the future of ESG regulation International Financial Law Review (2023).

Accordingly, ESRS also furnish investors with insights into the companies’ sustainability impacts and therefore enriching their investment comprehension.8Adam, O. Education and resourcing crucial to mastering Europe’s ESRS. International Financial Law Review(2023).

The invention of the ESRS is still new, with the reporting standards being finished since July 2023 and starting to be applicable in 2024, the first reporting year, with few exempted companies having a later reporting start. There is only little literature on the reporting standards itself which deals with breaking down and explaining their creation, content and application.

In this regard, after now having introduced the relevance of the ESRS, this work will start with a short definition of the CSRD and a longer one of the ESRS. After that, the entire development process will be explained, starting with the background information on the development and the introduction of the main participants, then following with the actual timeline and the further planning. Afterwards, this work will focus on the content and the structure of the ESRS by giving an overview of every individual standard. Last, the practical implementation will be explained. This also contains the materiality assessment, the LEAP-Process and information on the external audit of the sustainability report.

The entire work based on a literature review concerning the above-mentioned topics. Additionally, The research itself will be done in a process including three phases. The first phase involves research on Google Scholar and Orbis plus, with the keywords being “European Sustainability Reporting Standards” and “ESRS”, as well as “CSRD” and “Corporate Sustainability Reporting Directive”. As mentioned, since the ESRS are still new and therefore there is only a limited amount of available literature, this will be done through a broad search without restrictions in time periods or specific scientific journals. The second phase of research will be done on the search platforms “EBSCO” and “Scopus”. Additionally, The search on “EBSCO” includes an advanced search, scanning titles, abstracts and keywords for the terms “European Sustainability Reporting Standard” and “ESRS”. On Scopus, the carried out basic search focuses on the same terms. Again, there are no restrictions in time period and journals. The last phase focuses on the commentary “Haufe ESRS-Kommentar”. Additionally, The majority of the following work concentrates on the content of said commentary, especially the chapters describing the content and the materiality assessment.

2 Definitions

2.1 Corporate Sustainability Reporting Directive (CSRD)

The Corporate Sustainability Reporting Directive fully replaces the Non-Financial Reporting Directive (NFRD) and amends the Accounting Directive9Mezzanotte, F. E. Corporate sustainability reporting: double materiality, impacts, and legal risk. Journal of Corporate Law Studies 23, 633-663 (2023).. It obliges round about 50,000 European companies to perform a broad sustainability report and creates the framework for ESRS by determining the area of application of the later given standards and their obligations as well as the external audit of the generated sustainability reports6Schnabel, J., Bareth, M. & Rathfelder, A. CSRD: Wettbewerbsnachteil oder Chance für den Mittelstand? PiR-Internationale Rechnungslegung, 242-250 (2023).,10Baumüller, J. European Sustainability Reporting Standards (ESRS) Set 1–Die Endfassungen vom Juli 2023: Überblick und Würdigung. KoR: Zeitschrift für internationale und kapitalmarktorientierte Rechnungslegung 23, 411-415 (2023).. The CSRD also includes the development of the ESRS and their minimum requirements.10Baumüller, J. European Sustainability Reporting Standards (ESRS) Set 1–Die Endfassungen vom Juli 2023: Überblick und Würdigung. KoR: Zeitschrift für internationale und kapitalmarktorientierte Rechnungslegung 23, 411-415 (2023).

2.2 European Sustainability Reporting Standards (ESRS)

ESRS considered to be a reporting framework complementing CSRD.11Kirchhoff, K. R., Niefünd, S. & von Pressentin, J. A. CSRD: Die Neufassung der Non-Financial Reporting Directive in ESG: Nachhaltigkeit als strategischer Erfolgsfaktor 47-60 (Springer, 2024). Therefore, they are based on its instructions and have to be applied as soon as the reporting obligation of CSRD arises.4Baumüller, J. & Scheid, O. Die European Sustainability Reporting Standards (ESRS) als Zeitenwende für die Unternehmensberichterstattung?: Implikationen für den Mittelstand. StuB-Unternehmensteuern und Bilanzen 25, 742-747 (2023).,11Kirchhoff, K. R., Niefünd, S. & von Pressentin, J. A. CSRD: Die Neufassung der Non-Financial Reporting Directive in ESG: Nachhaltigkeit als strategischer Erfolgsfaktor 47-60 (Springer, 2024). In that regard, while other standards rely heavily on voluntary compliance, ESRS enforces compliance with minimal manoeuvring space for companies, and consequently distinguishing themselves from other initiatives.8Adam, O. Education and resourcing crucial to mastering Europe’s ESRS. International Financial Law Review(2023). Furthermore, ESRS stands as a legal mandate.8Adam, O. Education and resourcing crucial to mastering Europe’s ESRS. International Financial Law Review(2023).

ESRS cannot be defined as a singular set of standards, since there are different versions of sets planned.10Baumüller, J. European Sustainability Reporting Standards (ESRS) Set 1–Die Endfassungen vom Juli 2023: Überblick und Würdigung. KoR: Zeitschrift für internationale und kapitalmarktorientierte Rechnungslegung 23, 411-415 (2023). On the one hand, there are ESRS that have to be applied by large European companies subject to reporting.10Baumüller, J. European Sustainability Reporting Standards (ESRS) Set 1–Die Endfassungen vom Juli 2023: Überblick und Würdigung. KoR: Zeitschrift für internationale und kapitalmarktorientierte Rechnungslegung 23, 411-415 (2023). On the other hand, there will be sector-specific ESRS to be applied by companies working a specific sector, ESRS for SMEs and ESRS as recommendations for companies not obligated to report, including minimum content for reporting by third-country companies in accordance with Art. 40a of the Accounting Directive in the version of the CSRD.10Baumüller, J. European Sustainability Reporting Standards (ESRS) Set 1–Die Endfassungen vom Juli 2023: Überblick und Würdigung. KoR: Zeitschrift für internationale und kapitalmarktorientierte Rechnungslegung 23, 411-415 (2023). Therefore, ESRS are considered to be a system of different versions of ESRS.4Baumüller, J. & Scheid, O. Die European Sustainability Reporting Standards (ESRS) als Zeitenwende für die Unternehmensberichterstattung?: Implikationen für den Mittelstand. StuB-Unternehmensteuern und Bilanzen 25, 742-747 (2023). SMEs are micro, small and medium-sized enterprises, consisting of enterprises employing fewer than 250 persons, having an annual turnover not exceeding 50 million euros and an annual balance sheet total not exceeding 43 million euros.12Union, E. Benutzerleitfaden zur Definition von KMU Luxemburg 2015 (2020).

The newly developed ESRS are named Set 1 and include twelve standards independent from the companies’ sector.4Baumüller, J. & Scheid, O. Die European Sustainability Reporting Standards (ESRS) als Zeitenwende für die Unternehmensberichterstattung?: Implikationen für den Mittelstand. StuB-Unternehmensteuern und Bilanzen 25, 742-747 (2023). The disclosure requirements in those address among others remuneration systems, working methods in the Management Board and Supervisory Board and integration of stakeholder interests in the corporate strategy and business model.4Baumüller, J. & Scheid, O. Die European Sustainability Reporting Standards (ESRS) als Zeitenwende für die Unternehmensberichterstattung?: Implikationen für den Mittelstand. StuB-Unternehmensteuern und Bilanzen 25, 742-747 (2023). In general, ESRS includes specified information concerning the environment, social and human rights as well as the companies’ governance.5Ribeiro, C. & Carmo, C. Business Conduct Incidents: Promoting Transparency Through Sustainability Standardsin Addressing Corporate Scandals and Transgressions Through Governance and Social Responsibility 141-176 (IGI Global, 2023). More specifically, environmental topics include e.g. climate change mitigation, greenhouse gas emissions, marine and water resources, pollution, ecosystems, biodiversity, resource use and the circular economy.5Ribeiro, C. & Carmo, C. Business Conduct Incidents: Promoting Transparency Through Sustainability Standardsin Addressing Corporate Scandals and Transgressions Through Governance and Social Responsibility 141-176 (IGI Global, 2023). Governance topics include e.g. the management and supervisory bodies in relation to sustainability issues or ethics and corporate culture, including anti-corruption, whistleblower protection and animal welfare.5Ribeiro, C. & Carmo, C. Business Conduct Incidents: Promoting Transparency Through Sustainability Standardsin Addressing Corporate Scandals and Transgressions Through Governance and Social Responsibility 141-176 (IGI Global, 2023).

Additional ESRS are planned, and the adoption deadline has been postponed to 30 June 2026 (see section 3.1.3, timeline).13Sasfai, B., Mencher, M., Bichet, E., Eastwood, J. & Holm, S. European Union Adopts Long-Awaited Mandatory ESG Reporting Standards. Insights; the Corporate & Securities Law Advisor 37, 13-16 (2023).

3 The development of the ESRS

3.1 The development process

3.1.1 Background information

The European Commission (EC) has set very ambitious sustainability goals that it aspires to achieve. Given the range of the sustainability reporting standards and frameworks in the pre-COVID-19 ecosystems, it was thought that achieving these goals is only possible through EU’s own reporting standards. These standards are therefore tailored to the EU’s needs and demands. Additionally, for the first time, the EU is completely independent in the preparation and enforcement of those standards. Even though the EU already enforced the IFRS Accounting Standards prepared by the IASB in the field of financial reporting, and in the field of auditing the International Standards on Auditing prepared by IFAC’s International Auditing and Assurance Standards Board, namely with Directive 2006/43/EC on mandatory audits of financial statements, the EU only influences their content indirectly through various committees, forums and public deliberations. The decision to act independently for the first time emphasizes the EU’s autonomy. Furthermore, other major countries are reluctant to follow the EU’s example of standards enforcement. As above-mentioned, the EU has enforced different international standards. Other countries, such as the USA, China or India, may support the development and worldwide requirement of such standards, they do however not allow them to be used in their countries and have not required them for use in the last twenty centuries. As a consequence, it is unlikely that the EU will directly commit to the use of non-EU sustainability reporting standards and accordingly creates its own standards fitting its own independent needs.14Zdolšek, D. & Beloglavec, S. T. Sustainability reporting ecosystem: a once-in-a-lifetime overhaul during the COVID-19 pandemic. Additionally, Sustainability 15, 7349 (2023).

3.1.2 Participants in creating ESRS

3.1.2.1 EFRAG

The EFRAG, former European Financial Reporting Advisory Group, is responsible for the preparation of the ESRS.5Ribeiro, C. & Carmo, C. Business Conduct Incidents: Promoting Transparency Through Sustainability Standardsin Addressing Corporate Scandals and Transgressions Through Governance and Social Responsibility 141-176 (IGI Global, 2023). EFRAG is a private association established in 2001 in Brussels, following a request of the European Commission to the private sector to contribute to the growth of International Financial Reporting Standards (IFRS), issued by the International Accounting Standards Board (IASB), and to provide the EC with technical knowledge and advice on accounting matters3Barroso, J. G., Muñoz, F. F., García, A. J. B., Valentinetti, D. & de la Cruz Modino, R. The Role of Sustainability Indicators in Managing State-Owned Enterprises at the Regional Level: An Exploration on Disclosures for Better Policymaking in Financing Regions Toward Sustainability in the Midst of Climate Change Risks and Uncertainty (eds Beata Zofia Filipiak, Dominika Kordela, & Izabela Nawrolska) 221-234 (IGI Global, 2023).,5Ribeiro, C. & Carmo, C. Business Conduct Incidents: Promoting Transparency Through Sustainability Standardsin Addressing Corporate Scandals and Transgressions Through Governance and Social Responsibility 141-176 (IGI Global, 2023).. It funded predominantly by the EU and consists of different stakeholder organizations.15Kommission, E. Fragen und Antworten zur Annahme europäischer Standards für die Nachhaltigkeitsberichterstattung (2023). In detail, those include (I) Business Europe – European Business Federations, (II) the Federation des Experts Comptables Europeens (FEE), (III) the Comité European des Assurances (CEA), (IV) the European Federation of Financial Analysts Group (EFFAS), (V) the European Banking Federation (EBF), (VI) the European Savings Banks Group (ESBG), the European Association of Cooperative Banks (EACB), and (VII) the European Federation of Accountants and Auditors (EFAA).5Ribeiro, C. & Carmo, C. Business Conduct Incidents: Promoting Transparency Through Sustainability Standardsin Addressing Corporate Scandals and Transgressions Through Governance and Social Responsibility 141-176 (IGI Global, 2023). They support and contribute to EFRAG’s public interest mission and join EFRAG on a voluntary basis.5Ribeiro, C. & Carmo, C. Business Conduct Incidents: Promoting Transparency Through Sustainability Standardsin Addressing Corporate Scandals and Transgressions Through Governance and Social Responsibility 141-176 (IGI Global, 2023). Additionally, EFRAG brings together experts from various backgrounds, including academia, business, and accounting professions.3Barroso, J. G., Muñoz, F. F., García, A. J. B., Valentinetti, D. & de la Cruz Modino, R. The Role of Sustainability Indicators in Managing State-Owned Enterprises at the Regional Level: An Exploration on Disclosures for Better Policymaking in Financing Regions Toward Sustainability in the Midst of Climate Change Risks and Uncertainty (eds Beata Zofia Filipiak, Dominika Kordela, & Izabela Nawrolska) 221-234 (IGI Global, 2023). Therefore, EFRAG considered an independent advisory body, providing expertise on the development of accounting standards in the EU.3Barroso, J. G., Muñoz, F. F., García, A. J. B., Valentinetti, D. & de la Cruz Modino, R. The Role of Sustainability Indicators in Managing State-Owned Enterprises at the Regional Level: An Exploration on Disclosures for Better Policymaking in Financing Regions Toward Sustainability in the Midst of Climate Change Risks and Uncertainty (eds Beata Zofia Filipiak, Dominika Kordela, & Izabela Nawrolska) 221-234 (IGI Global, 2023).15Kommission, E. Fragen und Antworten zur Annahme europäischer Standards für die Nachhaltigkeitsberichterstattung (2023).

The advisory board’s structure consists of the EFRAG Supervisory Group, the EFRAG Technical Expert Group (EFRAG TEG), and the EFRAG Consultation Forum of Standards Setters (EFRAG CFSS). EFRAG’s Supervisory Board appoints the members of EFRAG TEG. In doing so, it achieves a broad geographical balance from prepares, accountants, users of financial statements and academics.5Ribeiro, C. & Carmo, C. Business Conduct Incidents: Promoting Transparency Through Sustainability Standardsin Addressing Corporate Scandals and Transgressions Through Governance and Social Responsibility 141-176 (IGI Global, 2023).

Core activities include the upstream influence, meaning the contribution to the future shape of international financial reporting.5Ribeiro, C. & Carmo, C. Business Conduct Incidents: Promoting Transparency Through Sustainability Standardsin Addressing Corporate Scandals and Transgressions Through Governance and Social Responsibility 141-176 (IGI Global, 2023). Additionally, it improves IFRS by providing European views on financial reporting.5Ribeiro, C. & Carmo, C. Business Conduct Incidents: Promoting Transparency Through Sustainability Standardsin Addressing Corporate Scandals and Transgressions Through Governance and Social Responsibility 141-176 (IGI Global, 2023). This covers the phases from their inception to the revision of existing standards.5Ribeiro, C. & Carmo, C. Business Conduct Incidents: Promoting Transparency Through Sustainability Standardsin Addressing Corporate Scandals and Transgressions Through Governance and Social Responsibility 141-176 (IGI Global, 2023). Moreover, EFRAG also gives endorsement advice by counselling the EC on whether the application of and compliance with IFRS agree with the criteria set out for use in Europe.5Ribeiro, C. & Carmo, C. Business Conduct Incidents: Promoting Transparency Through Sustainability Standardsin Addressing Corporate Scandals and Transgressions Through Governance and Social Responsibility 141-176 (IGI Global, 2023). All in all, it has been instrumental in bringing international standards like the IFRS to the EU.3Barroso, J. G., Muñoz, F. F., García, A. J. B., Valentinetti, D. & de la Cruz Modino, R. The Role of Sustainability Indicators in Managing State-Owned Enterprises at the Regional Level: An Exploration on Disclosures for Better Policymaking in Financing Regions Toward Sustainability in the Midst of Climate Change Risks and Uncertainty (eds Beata Zofia Filipiak, Dominika Kordela, & Izabela Nawrolska) 221-234 (IGI Global, 2023). Now, EFRAG becomes a central part in enhancing public policymaking by developing sustainability reporting standards.3Barroso, J. G., Muñoz, F. F., García, A. J. B., Valentinetti, D. & de la Cruz Modino, R. The Role of Sustainability Indicators in Managing State-Owned Enterprises at the Regional Level: An Exploration on Disclosures for Better Policymaking in Financing Regions Toward Sustainability in the Midst of Climate Change Risks and Uncertainty (eds Beata Zofia Filipiak, Dominika Kordela, & Izabela Nawrolska) 221-234 (IGI Global, 2023).

Furthermore, the activities can be divided into two pillars. Additionally, The first one deals with financial reporting and consequently working on the development or amendment of the IFRS and advising the EC on their endorsement, so that they contribute to the efficiency of European capital markets. The second pillar consists of sustainability reporting, which includes the development of draft versions of ESRS and related amendments.5Ribeiro, C. & Carmo, C. Business Conduct Incidents: Promoting Transparency Through Sustainability Standardsin Addressing Corporate Scandals and Transgressions Through Governance and Social Responsibility 141-176 (IGI Global, 2023). The second pillar has established during the development process of the ESRS and therefore will be explained further later on.

3.1.2.2 Global Reporting Initiative (GRI)

De Villiers, La Torre and Molinari (2022) define GRI as “…an independent international organization, established in 1997 as a joint initiative of the Coalition for Environmentally Responsible Economies, an American non-government organization and the United Nations (UN) Environmental Programme” (p. 730).16de Villers, C., La Torre, M. & Molinari, M. The Global Reporting Initiative’s (GRI) past, present and future: critical reflections and a research agenda on sustainability reporting (standard-setting). Pacific accounting review 34, 728-747 (2022). Its purpose was to set the first accountability mechanism to guarantee organizations adhere to responsible environmental principles which were then broadened to include social, economic and governance issues.16de Villers, C., La Torre, M. & Molinari, M. The Global Reporting Initiative’s (GRI) past, present and future: critical reflections and a research agenda on sustainability reporting (standard-setting). Pacific accounting review 34, 728-747 (2022). GRI has published a pilot version of a public supplement specifically to address the reporting needs of these organizations.17Dumay, J., Guthrie, J. & Farneti, F. Gri Sustainability Reporting Guidelines For Public And Third Sector Organizations: A critical view. Public management review 12, 531-548 (2010). Specifically, the Sustainability Reporting Guidelines created by GRI are the first international framework for comprehensive corporate sustainability reporting with a particular focus on environmental matters.16de Villers, C., La Torre, M. & Molinari, M. The Global Reporting Initiative’s (GRI) past, present and future: critical reflections and a research agenda on sustainability reporting (standard-setting). Pacific accounting review 34, 728-747 (2022).,17Dumay, J., Guthrie, J. & Farneti, F. Gri Sustainability Reporting Guidelines For Public And Third Sector Organizations: A critical view. Public management review 12, 531-548 (2010). They are the result of co-operation between researchers, industry and consultants and the output of a multi-stakeholder approach.17Dumay, J., Guthrie, J. & Farneti, F. Gri Sustainability Reporting Guidelines For Public And Third Sector Organizations: A critical view. Public management review 12, 531-548 (2010).

GRI Guidelines are the most used guidelines worldwide. This reinforced by the fact that they are applicable to every kind of company, independent of their sector. In detail, those guidelines include reporting principles and step-by-step instructions on identifying relevant topics and their disclosure.18Kirchhoff, K. R., Niefünd, S. & von Pressentin, J. A. Nachhaltigkeit aus Kapitalmarktsicht in ESG: Nachhaltigkeit als strategischer Erfolgsfaktor 35-46 (Springer, 2024).

3.1.3 Timeline

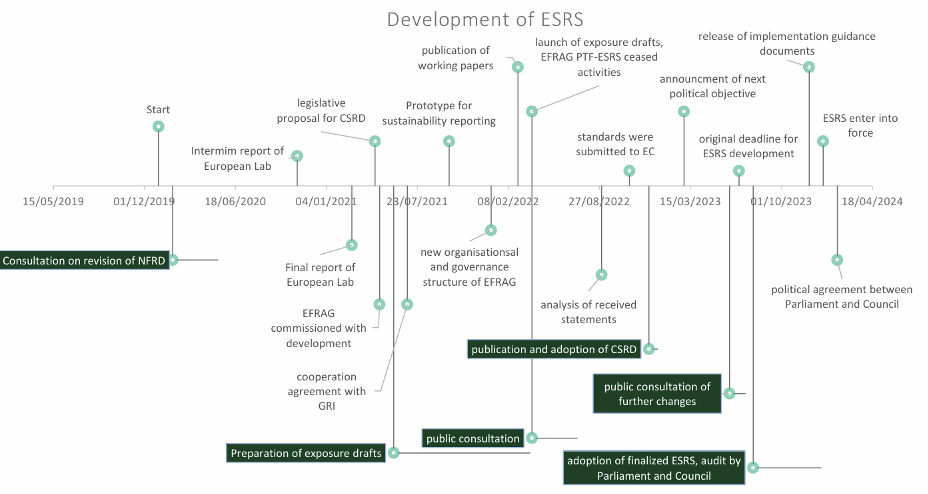

The following text describes the development of the first set of ESRS. Figure 1 provides an overview through a timeline.

The foundation for the development of ESRS has been laid by the European Corporate Reporting Lab @EFRAG (European Lab) in 2020.4Baumüller, J. & Scheid, O. Die European Sustainability Reporting Standards (ESRS) als Zeitenwende für die Unternehmensberichterstattung?: Implikationen für den Mittelstand. StuB-Unternehmensteuern und Bilanzen 25, 742-747 (2023). The entire process of the development of ESRS started with the EC launching a consultation on a possible revision of the NFRD which lasted from February 2020 to June 2020.19Directorate-General for Financial Stability, F. S. a. C. M. U. Corporate sustainability reporting <https://finance.ec.europa.eu/capital-markets-union-and-financial-markets/company-reporting-and-auditing/company-reporting/corporate-sustainability-reporting_en> (n.d.)[Accessed 28.05.2024]. In May 2020, the EC’s updated Work Programme included a possible publication of a legislative proposal to revise the NFRD.20EFRAG. PROGRESS REPORT OF THE PROJECT TASK FORCE ON PREPARATORY WORK FOR THE ELABORATION OF POSSIBLE EU NON-FINANCIAL REPORTING STANDARDS (PTF-NFRS). (2020). In this regard, the EC mandated EFRAG to carry out technical preparatory work for the development of possible European standards.20EFRAG. PROGRESS REPORT OF THE PROJECT TASK FORCE ON PREPARATORY WORK FOR THE ELABORATION OF POSSIBLE EU NON-FINANCIAL REPORTING STANDARDS (PTF-NFRS). (2020). Then, EFRAG established a dedicated task force to work on the elaboration of possible EU non-financial reporting standards.3Barroso, J. G., Muñoz, F. F., García, A. J. B., Valentinetti, D. & de la Cruz Modino, R. The Role of Sustainability Indicators in Managing State-Owned Enterprises at the Regional Level: An Exploration on Disclosures for Better Policymaking in Financing Regions Toward Sustainability in the Midst of Climate Change Risks and Uncertainty (eds Beata Zofia Filipiak, Dominika Kordela, & Izabela Nawrolska) 221-234 (IGI Global, 2023).,20EFRAG. PROGRESS REPORT OF THE PROJECT TASK FORCE ON PREPARATORY WORK FOR THE ELABORATION OF POSSIBLE EU NON-FINANCIAL REPORTING STANDARDS (PTF-NFRS). (2020). Since this connects to the NFRD, the project task force has named the Project Task Force on NFRD (PTF-NFRD).4Baumüller, J. & Scheid, O. Die European Sustainability Reporting Standards (ESRS) als Zeitenwende für die Unternehmensberichterstattung?: Implikationen für den Mittelstand. StuB-Unternehmensteuern und Bilanzen 25, 742-747 (2023). Said working group consists of stakeholders from various sectors such as companies, public sector managers, investors, and academics, who provide input and feedback.3Barroso, J. G., Muñoz, F. F., García, A. J. B., Valentinetti, D. & de la Cruz Modino, R. The Role of Sustainability Indicators in Managing State-Owned Enterprises at the Regional Level: An Exploration on Disclosures for Better Policymaking in Financing Regions Toward Sustainability in the Midst of Climate Change Risks and Uncertainty (eds Beata Zofia Filipiak, Dominika Kordela, & Izabela Nawrolska) 221-234 (IGI Global, 2023). That task force has been conducting research and engaging with stakeholders to identify the key sustainability reporting requirements and to develop a framework for reporting that is in line with the EU’s sustainability policy. Additionally, The PTF-NFRD has also involved in consultations and workshops to ensure that the standards reflect the needs and expectations of all stakeholders.3Barroso, J. G., Muñoz, F. F., García, A. J. B., Valentinetti, D. & de la Cruz Modino, R. The Role of Sustainability Indicators in Managing State-Owned Enterprises at the Regional Level: An Exploration on Disclosures for Better Policymaking in Financing Regions Toward Sustainability in the Midst of Climate Change Risks and Uncertainty (eds Beata Zofia Filipiak, Dominika Kordela, & Izabela Nawrolska) 221-234 (IGI Global, 2023). By using a bottom-up approach, the working group ensures that the standards are robust and relevant to the needs of the market while promoting transparency and accountability in sustainability reporting.3Barroso, J. G., Muñoz, F. F., García, A. J. B., Valentinetti, D. & de la Cruz Modino, R. The Role of Sustainability Indicators in Managing State-Owned Enterprises at the Regional Level: An Exploration on Disclosures for Better Policymaking in Financing Regions Toward Sustainability in the Midst of Climate Change Risks and Uncertainty (eds Beata Zofia Filipiak, Dominika Kordela, & Izabela Nawrolska) 221-234 (IGI Global, 2023).

In November 2020, the working group of the European Lab publicized an interim report, followed by the final report in March 2021.4Baumüller, J. & Scheid, O. Die European Sustainability Reporting Standards (ESRS) als Zeitenwende für die Unternehmensberichterstattung?: Implikationen für den Mittelstand. StuB-Unternehmensteuern und Bilanzen 25, 742-747 (2023). These reports mention a proposal of a roadmap for the development of a comprehensive set of EU sustainability reporting standards.21Directorate-General for Financial Stability, F. S. a. C. M. U. Reports on development of EU sustainability reporting standards. (European Commission, 2021). As a result, sustainability standards for the EU are seen as necessary to meet the political ambition and urgent timetable of the European Green Deal. They should ensure the constancy of reporting rules at the core of the EU’s sustainability agenda.21Directorate-General for Financial Stability, F. S. a. C. M. U. Reports on development of EU sustainability reporting standards. (European Commission, 2021).

Following, on the 21st of April 2021, there was a legislative proposal for a Corporate Sustainability Reporting Directive, the CSRD.21Directorate-General for Financial Stability, F. S. a. C. M. U. Reports on development of EU sustainability reporting standards. (European Commission, 2021). It should amend the reporting requirements given in the NFRD and extend the scope to all large companies and all companies listed on regulated markets with the exception being micro-enterprises.19Directorate-General for Financial Stability, F. S. a. C. M. U. Corporate sustainability reporting <https://finance.ec.europa.eu/capital-markets-union-and-financial-markets/company-reporting-and-auditing/company-reporting/corporate-sustainability-reporting_en> (n.d.)[Accessed 28.05.2024].,22Directorate-General for Financial Stability, F. S. a. C. M. U. Sustainable finance package, <https://finance.ec.europa.eu/publications/sustainable-finance-package_en#csrd> (2021)[Accessed 28.05.2024]. Additionally, CSRD introduces more detailed reporting requirements in accordance with the mandatory ESRS, as well as the obligation to audit the reported information. While reporting, the companies now also have to digitally tag that information, so that the reports become machine readable and feed into the European single access point envisaged in the capital markets union action plan.22Directorate-General for Financial Stability, F. S. a. C. M. U. Sustainable finance package, <https://finance.ec.europa.eu/publications/sustainable-finance-package_en#csrd> (2021)[Accessed 28.05.2024].

Therefore, to ensure its own demands, the CSRD includes the obligation for the EC to develop a first set of ESRS with the deadline being the 30.06.2023.10Baumüller, J. European Sustainability Reporting Standards (ESRS) Set 1–Die Endfassungen vom Juli 2023: Überblick und Würdigung. KoR: Zeitschrift für internationale und kapitalmarktorientierte Rechnungslegung 23, 411-415 (2023). Prioritized should be ESRS that apply to all major companies of the EU obligated to report under the CSRD.10Baumüller, J. European Sustainability Reporting Standards (ESRS) Set 1–Die Endfassungen vom Juli 2023: Überblick und Würdigung. KoR: Zeitschrift für internationale und kapitalmarktorientierte Rechnungslegung 23, 411-415 (2023). This led to the creation of the Project Task Force on European Sustainability Reporting Standards (PTF-ESRS), commissioned by Mairead McGuiness and consisting of voluntary supporters of EU-member states.4Baumüller, J. & Scheid, O. Die European Sustainability Reporting Standards (ESRS) als Zeitenwende für die Unternehmensberichterstattung?: Implikationen für den Mittelstand. StuB-Unternehmensteuern und Bilanzen 25, 742-747 (2023).,23Lanfermann, G. Einführung in die European Sustainability Reporting Standards (ESRS) in Haufe ESRS-Kommentar 1. Auflage: Kommentar zu den European Sustainability Reporting Standards (eds Jens Freiberg & Georg Lanfermann) 17-50 (Haufe-Lexware, 2023). The PTF-ESRS established dedicated to the preparation of technical advice on potential ESRS.5Ribeiro, C. & Carmo, C. Business Conduct Incidents: Promoting Transparency Through Sustainability Standardsin Addressing Corporate Scandals and Transgressions Through Governance and Social Responsibility 141-176 (IGI Global, 2023). Later on, this group was also instructed to create ESRS and seek cooperation agreements with important European and international standard setters and initiatives like the GRI.5Ribeiro, C. & Carmo, C. Business Conduct Incidents: Promoting Transparency Through Sustainability Standardsin Addressing Corporate Scandals and Transgressions Through Governance and Social Responsibility 141-176 (IGI Global, 2023). Furthermore, it was seen as important that the development included different kinds of stakeholders, such as companies, investors, the civil society, auditors, trade unions, scientists and standardization bodies.15Kommission, E. Fragen und Antworten zur Annahme europäischer Standards für die Nachhaltigkeitsberichterstattung (2023).

In May 2021, the EC officially commissioned EFRAG with the development of ESRS.4Baumüller, J. & Scheid, O. Die European Sustainability Reporting Standards (ESRS) als Zeitenwende für die Unternehmensberichterstattung?: Implikationen für den Mittelstand. StuB-Unternehmensteuern und Bilanzen 25, 742-747 (2023). Following that, in June 2021, EFRAG started with a public consultation concerning the development process of the standardisation of European sustainability reporting.4Baumüller, J. & Scheid, O. Die European Sustainability Reporting Standards (ESRS) als Zeitenwende für die Unternehmensberichterstattung?: Implikationen für den Mittelstand. StuB-Unternehmensteuern und Bilanzen 25, 742-747 (2023). Since June 2021, EFRAG PTF-ESRS subsequently started the preparation of exposure drafts of ESRS.5Ribeiro, C. & Carmo, C. Business Conduct Incidents: Promoting Transparency Through Sustainability Standardsin Addressing Corporate Scandals and Transgressions Through Governance and Social Responsibility 141-176 (IGI Global, 2023). In July 2021, EFRAG also started a cooperation agreement with the GRI concerning a co-construction of the ESRS 5. Thus, the technical groups of EFRAG and GRI came together to share information to establish sustainability standards.5Ribeiro, C. & Carmo, C. Business Conduct Incidents: Promoting Transparency Through Sustainability Standardsin Addressing Corporate Scandals and Transgressions Through Governance and Social Responsibility 141-176 (IGI Global, 2023). Next, in Autumn 2021 during the project phase, EFRAG PTF-ESRS introduced a prototype for sustainability reporting which gained a lot of criticism concerning the amount and complexity of disclosure obligations planned.23Lanfermann, G. Einführung in die European Sustainability Reporting Standards (ESRS) in Haufe ESRS-Kommentar 1. Auflage: Kommentar zu den European Sustainability Reporting Standards (eds Jens Freiberg & Georg Lanfermann) 17-50 (Haufe-Lexware, 2023). Shortly afterwards, in the first quarter of 2022, working papers published as stakeholder-information.4Baumüller, J. & Scheid, O. Die European Sustainability Reporting Standards (ESRS) als Zeitenwende für die Unternehmensberichterstattung?: Implikationen für den Mittelstand. StuB-Unternehmensteuern und Bilanzen 25, 742-747 (2023). In detail, those constituted of 24 ESRS working papers with round about 200 disclosure requirements, introducing the envisioned structure and content of ESRS.23Lanfermann, G. Einführung in die European Sustainability Reporting Standards (ESRS) in Haufe ESRS-Kommentar 1. Auflage: Kommentar zu den European Sustainability Reporting Standards (eds Jens Freiberg & Georg Lanfermann) 17-50 (Haufe-Lexware, 2023).

The year 2022 also led to the launch of a new organisational and governance structure by the General Assembly of EFRAG. The new organisational and governance structure led to the creation of a sustainability pillar as part of EFRAG’s activities, next to the already existing pillar on financial reporting. This new structure should support the EFRAG in developing ESRS and realizing the demanded conditions in CSRD. In general, the sustainability pillar reflects the financial pillar in its structure. The sustainability pillar led to the creation of subject-related committees, such as the Sustainability Reporting Technical Expert Group (SR TEG) and the Sustainability Reporting Board (SR Board), similar to the Financial Reporting Board and Financial Reporting TEG already existing in the financial reporting pillar. Additionally, considering the number of different stakeholders now addressed in sustainability reporting, the membership range of EFRAG widened. Now it also covers more different organizations, especially ones relating to the civil society, users, trade unions and science.23Lanfermann, G. Einführung in die European Sustainability Reporting Standards (ESRS) in Haufe ESRS-Kommentar 1. Auflage: Kommentar zu den European Sustainability Reporting Standards (eds Jens Freiberg & Georg Lanfermann) 17-50 (Haufe-Lexware, 2023).

The SR TEG and the SRB are intended to take over the development of ESRS. In detail, SR TEG supposed to work on further ESRS drafts with the support of the EFRAG Secretary. SRB then has to evaluate the created drafts and decide on their content for submission to the EC. Furthermore, the following development of ESRS supposed to follow Due Process Procedures.23Lanfermann, G. Einführung in die European Sustainability Reporting Standards (ESRS) in Haufe ESRS-Kommentar 1. Auflage: Kommentar zu den European Sustainability Reporting Standards (eds Jens Freiberg & Georg Lanfermann) 17-50 (Haufe-Lexware, 2023).

April 2022, EFRAG PTF-ESRS finished and launched 13 exposure drafts on ESRS as conclusion of its activities. Afterwards, the already established SRB and SR TEG took over the development process as mentioned above. Following, they started a public consultation with the drafts being open for comments until the 8th of August 2022.1Kamenšek, D. & Gornjak, M. Organisational Reporting in the EU on Sustainability. Journal of Accounting and Management 13, 77-90 (2023).5Ribeiro, C. & Carmo, C. Business Conduct Incidents: Promoting Transparency Through Sustainability Standardsin Addressing Corporate Scandals and Transgressions Through Governance and Social Responsibility 141-176 (IGI Global, 2023). The drafts relate to the first set of standards and therefore cover environmental, social and governance aspects as well as cross-cutting standards.5Ribeiro, C. & Carmo, C. Business Conduct Incidents: Promoting Transparency Through Sustainability Standardsin Addressing Corporate Scandals and Transgressions Through Governance and Social Responsibility 141-176 (IGI Global, 2023). Incoming input and comments by stakeholders uploaded on EFRAG’s website, with the exception being cases in which stakeholders requested confidentiality.5Ribeiro, C. & Carmo, C. Business Conduct Incidents: Promoting Transparency Through Sustainability Standardsin Addressing Corporate Scandals and Transgressions Through Governance and Social Responsibility 141-176 (IGI Global, 2023). In total, the public consultation led to round about 750 statements from different stakeholders.23Lanfermann, G. Einführung in die European Sustainability Reporting Standards (ESRS) in Haufe ESRS-Kommentar 1. Auflage: Kommentar zu den European Sustainability Reporting Standards (eds Jens Freiberg & Georg Lanfermann) 17-50 (Haufe-Lexware, 2023). Then, the EFRAG SRB, advised by the EFRAG Sustainability Reporting Technical Expert Group (EFRAG SRTEG), addressed the given feedback.5Ribeiro, C. & Carmo, C. Business Conduct Incidents: Promoting Transparency Through Sustainability Standardsin Addressing Corporate Scandals and Transgressions Through Governance and Social Responsibility 141-176 (IGI Global, 2023). More precisely, in September 2022 EFRAG published a qualitative and quantitative analysis of the comments received which consists of several steps, starting with the development of core categories and themes based on the responses of the stakeholders, with the main categories being reservations, suggestions for improvement and support.5Ribeiro, C. & Carmo, C. Business Conduct Incidents: Promoting Transparency Through Sustainability Standardsin Addressing Corporate Scandals and Transgressions Through Governance and Social Responsibility 141-176 (IGI Global, 2023). Furthermore, politicians also decided to ease the complexity and content of the standards.4Baumüller, J. & Scheid, O. Die European Sustainability Reporting Standards (ESRS) als Zeitenwende für die Unternehmensberichterstattung?: Implikationen für den Mittelstand. StuB-Unternehmensteuern und Bilanzen 25, 742-747 (2023). Because of this, the Exposure Drafts underwent substantial changes, especially having led to a further simplification by having reduced the disclosure obligations to half the amount and reducing companies’ administrative expenses.4Baumüller, J. & Scheid, O. Die European Sustainability Reporting Standards (ESRS) als Zeitenwende für die Unternehmensberichterstattung?: Implikationen für den Mittelstand. StuB-Unternehmensteuern und Bilanzen 25, 742-747 (2023).,24EFRAG. EFRAG delivers the first set of draft ESRS to the European Commission Brussels 1-2 (2022).

All in all, this could be described as carrying out the demanded Due Process Procedures. This covers the publication and the consultation as well as the public comment analysis, the finalization of Technical Advice to the European Commission, the submission to the EC and the post-implementation review.5Ribeiro, C. & Carmo, C. Business Conduct Incidents: Promoting Transparency Through Sustainability Standardsin Addressing Corporate Scandals and Transgressions Through Governance and Social Responsibility 141-176 (IGI Global, 2023).

In November 2022, the explained process above led to the next draft of the first set of ESRS being finalized, consisting of twelve draft standards.7Foley, M. Looking to the ESRS for clues on the future of ESG regulation International Financial Law Review (2023). They approved and supported by the ESRS SRB. Furthermore, Patrick de Cambourg, head of EFRAG’s sustainability board, expressed that the goal of wide acceptance and practical implementation could be achieved through the in ESRS given cross-sectorial content. Then, they submitted to the EC.25Fischer, D. T. EFRAG: Zukunft der Unternehmensberichterstattung PiR-Internationale Rechnungslegung, 141-142 (2023). Consequently, the Commission consulted the Member States as well as various EU organizations.15Kommission, E. Fragen und Antworten zur Annahme europäischer Standards für die Nachhaltigkeitsberichterstattung (2023). This includes supervisory authorities, like the European Securities and Markets Authority, the European Banking Authority and the European Insurance And Occupational Pensions Authority, as well as the European Environment Agency, the European Union Agency for Fundamental Rights, the Committee of European Auditing Oversight Bodies and the Platform on Sustainable Finance.26Kommission, E. Additionally, Fragen und Antworten zur Annahme europäischer Standards für die Nachhaltigkeitsberichterstattung (2023).

After being published in the Official Journal of the European Union on the 14th of December 2022, the Directive (EU) 2022/2464 on sustainability reporting, the CSRD, became effective on the 5th of January 2023, therefore mandating the adoption of ESRS as a Delegated Act.25Fischer, D. T. EFRAG: Zukunft der Unternehmensberichterstattung PiR-Internationale Rechnungslegung, 141-142 (2023). ,27EFRAG. The first set of ESRS – journey from PTF to delegated act (adopted on 31 July 2023), <https://www.efrag.org/lab6> (n.d.)[Accessed 28.05.2024].

In March 2023, the EC announced the next relating political objective.10Baumüller, J. European Sustainability Reporting Standards (ESRS) Set 1–Die Endfassungen vom Juli 2023: Überblick und Würdigung. KoR: Zeitschrift für internationale und kapitalmarktorientierte Rechnungslegung 23, 411-415 (2023). EU Commissioner Mairead McGuiness demanded EFRAG to prioritize development of further guidelines concerning Set 1 of ESRS. At the same time, President of the Commission Ursula von der Leyen demanded to reduce the given disclosure requirements by a further 25%.23Lanfermann, G. Einführung in die European Sustainability Reporting Standards (ESRS) in Haufe ESRS-Kommentar 1. Auflage: Kommentar zu den European Sustainability Reporting Standards (eds Jens Freiberg & Georg Lanfermann) 17-50 (Haufe-Lexware, 2023). Those changes incorporated into the next version of ESRS and made available for another consultation.28Baumüller, J. Die Auswahl von Metriken in der Nachhaltigkeitsberichterstattung gemäß ESRS: Über welche Nachhaltigkeits-Kennzahlen müssen europäische Unternehmen fortan berichten? PiR-Internationale Rechnungslegung 19, 329-336 (2023). Since this period started on the 9th of June 2023 and supposed to be four-weeks long, ending on the 7th of July 2023, the given deadline of adopting the final ESRS version within the end of June could not be met.4Baumüller, J. & Scheid, O. Die European Sustainability Reporting Standards (ESRS) als Zeitenwende für die Unternehmensberichterstattung?: Implikationen für den Mittelstand. StuB-Unternehmensteuern und Bilanzen 25, 742-747 (2023).15Kommission, E. Fragen und Antworten zur Annahme europäischer Standards für die Nachhaltigkeitsberichterstattung (2023).,29Baumüller, J. & Sopp, K. European Sustainability Reporting Standards: Die EU-Konsultationsfassung vom Juni 2023: Überblick und kritische Würdigung. PiR-Internationale Rechnungslegung 19, 258-263 (2023).

The end of the consultation came with more adjustments to be made. Those led to every disclosure requirement of the thematical standards now being subjected to the materiality assessment. The materiality assessment has thus been further emphasized.23Lanfermann, G. Einführung in die European Sustainability Reporting Standards (ESRS) in Haufe ESRS-Kommentar 1. Auflage: Kommentar zu den European Sustainability Reporting Standards (eds Jens Freiberg & Georg Lanfermann) 17-50 (Haufe-Lexware, 2023).

On the 31st of July 2023, the final version of ESRS has adopted and therefore becomes mandatory for all companies subject to the CSRD.30Directorate-General for Financial Stability, F. S. a. C. M. U. The Commission adopts the European Sustainability Reporting Standards, <https://finance.ec.europa.eu/news/commission-adopts-european-sustainability-reporting-standards-2023-07-31_en> (2023)[Accessed 28.05.2024]. The ESRS published on the official Homepage of the EC.10Baumüller, J. European Sustainability Reporting Standards (ESRS) Set 1–Die Endfassungen vom Juli 2023: Überblick und Würdigung. KoR: Zeitschrift für internationale und kapitalmarktorientierte Rechnungslegung 23, 411-415 (2023). This followed by a fourth month period in which the European Parliament and the European Council have the chance to object against the given draft of ESRS.10Baumüller, J. European Sustainability Reporting Standards (ESRS) Set 1–Die Endfassungen vom Juli 2023: Überblick und Würdigung. KoR: Zeitschrift für internationale und kapitalmarktorientierte Rechnungslegung 23, 411-415 (2023). That step is also considered to be the last step in the actual development process.29Baumüller, J. & Sopp, K. European Sustainability Reporting Standards: Die EU-Konsultationsfassung vom Juni 2023: Überblick und kritische Würdigung. PiR-Internationale Rechnungslegung 19, 258-263 (2023). If there are no objections, they will become effective at the beginning of the business year 2024.10Baumüller, J. European Sustainability Reporting Standards (ESRS) Set 1–Die Endfassungen vom Juli 2023: Überblick und Würdigung. KoR: Zeitschrift für internationale und kapitalmarktorientierte Rechnungslegung 23, 411-415 (2023).

In December 2023, EFRAG released draft Implementation Guidance.31EFRAG. The first set of ESRS – the journey from PTF to delegated act (adopted on 31 July 2023). <https://efrag-website.azurewebsites.net/lab6#:~:text=On%2031%20July%202023%2C%20the,2464)%20adopted%20in%20December%202022.> (n.d.). The final versions of IG 1 – IG 3 were published on May 31, 2024, followed by an IG 3 Addendum in December 2024.32EFRAG. ESRS implementation guidance document. <https://www.efrag.org/en/projects/esrs-implementation-guidance-documents> (n.d.). These non-binding documents provide practical support on materiality assessment, value chain implementation, and ESRS datapoint guidance.32EFRAG. ESRS implementation guidance document. <https://www.efrag.org/en/projects/esrs-implementation-guidance-documents> (n.d.).

In January 2024, the ESRS entered into force as a Delegated Act.33Lanfermann, G. & Liepe, M. § 1 Einführung in die European Sustainability Reporting Standards (ESRS). <https://www.haufe.de/id/beitrag/1-einfuehrung-in-die-european-sustainability-reporting-standards-esrs-HI15701746.html> (n.d.). In February 2024, the European Parliament and the Council agreed to postpone the deadline for sector-specific standards from mid-2024 to mid-2026.34European Commission. Daily News 08 / 02 / 2024. <https://ec.europa.eu/commission/presscorner/detail/en/mex_24_707> (2024).

This regression was further exploited in February 2025. The European Commission proposed the Omnibus simplification package for the EU legislation.35European Council. Simplification: Council gives final green light on the ‘Stop-the-clock’ mechanism to boost EU competitiveness and provide legal certainty to businesses. <https://www.consilium.europa.eu/en/press/press-releases/2025/04/14/simplification-council-gives-final-green-light-on-the-stop-the-clock-mechanism-to-boost-eu-competitiveness-and-provide-legal-certainty-to-businesses/> (2025). The goal is to simplify EU rules, enhance competitiveness and to attract investment.36European Commission. Omnibus package. <https://finance.ec.europa.eu/news/omnibus-package-2025-04-01_en> (2025). In relation to this, the EU adopted the Stop-the-Clock Directive (EU 2025/794) in April 2025.35European Council. Simplification: Council gives final green light on the ‘Stop-the-clock’ mechanism to boost EU competitiveness and provide legal certainty to businesses. <https://www.consilium.europa.eu/en/press/press-releases/2025/04/14/simplification-council-gives-final-green-light-on-the-stop-the-clock-mechanism-to-boost-eu-competitiveness-and-provide-legal-certainty-to-businesses/> (2025). It postpones the starting dates for reporting and due diligence for wave two and wave three companies (previously required to report in 2025/2026) that were set by the CSRD and the CSDDD.37Deloitte. EU Omnibus explained. <https://www.deloitte.com/nl/en/issues/climate/omnibus-csrd-csddd-eu-taxonomy.html> (2025).38European Commission. Corporate sustainability reporting. <https://finance.ec.europa.eu/financial-markets/company-reporting-and-auditing/company-reporting/corporate-sustainability-reporting_en> (2025). In July 2025 the Commission additionally issued a ‘Quick Fix’ delegated act providing transitional relief for wave one companies, permitting simplified disclosure in financial years 2025–2026 without additional information compared to the financial year 2024.39RÖDL. Omnibus Initiative in motion: How far along is the EU with its course correction? <https://www.roedl.com/en/insights/omnibus-initiative-in-motion-eu-course-correction/> (2025).40European Commission. Commission adopts “quick fix” for companies already conducting corporate sustainability reporting. <https://finance.ec.europa.eu/publications/commission-adopts-quick-fix-companies-already-conducting-corporate-sustainability-reporting_en> (2025).

In July 2025 the EC adopted a recommendation for small and medium-sized companies (SMEs) on voluntary sustainability reporting.41European Commission. Commission presents voluntary sustainability reporting standard to ease burden on SMEs. <https://finance.ec.europa.eu/publications/commission-presents-voluntary-sustainability-reporting-standard-ease-burden-smes_en> (2025). This addition is intended to reduce the administrative burden on SMEs, as they are often part of the value chains of larger companies, which are obliged to report, and therefore the SMEs must provide them with requested sustainability information.41European Commission. Commission presents voluntary sustainability reporting standard to ease burden on SMEs. <https://finance.ec.europa.eu/publications/commission-presents-voluntary-sustainability-reporting-standard-ease-burden-smes_en> (2025).

3.2 Ongoing development and future adjustments of ESRS

Further development of ESRS has already begun alongside the development of the first set. On the one hand, this covers the development of Set 2 of ESRS which includes sector-specific standards as well as standards specifically for SMEs.29Baumüller, J. & Sopp, K. European Sustainability Reporting Standards: Die EU-Konsultationsfassung vom Juni 2023: Überblick und kritische Würdigung. PiR-Internationale Rechnungslegung 19, 258-263 (2023). The sector-specific standards particularly will be connected to the first set of ESRS which covers cross-sectorial standards.23Lanfermann, G. Einführung in die European Sustainability Reporting Standards (ESRS) in Haufe ESRS-Kommentar 1. Auflage: Kommentar zu den European Sustainability Reporting Standards (eds Jens Freiberg & Georg Lanfermann) 17-50 (Haufe-Lexware, 2023). On the other hand, this means the adoption of application guidelines supporting the implementation including e.g. guidelines concerning the materiality assessment, the establishment of an official mechanism for a legally binding interpretation of the ESRS in the event of a question of interpretation or the extent of value chain information required under ESRS.13Sasfai, B., Mencher, M., Bichet, E., Eastwood, J. & Holm, S. European Union Adopts Long-Awaited Mandatory ESG Reporting Standards. Insights; the Corporate & Securities Law Advisor 37, 13-16 (2023).29Baumüller, J. & Sopp, K. European Sustainability Reporting Standards: Die EU-Konsultationsfassung vom Juni 2023: Überblick und kritische Würdigung. PiR-Internationale Rechnungslegung 19, 258-263 (2023). Regarding this, EFRAG already published three implementation guidance documents. The first two include guidance on the implementation of the materiality assessment and the value chain. The third deals with a guidance on the implementation of detailed ESRS datapoints.42EFRAG. ESRS implementation guidance documents, <https://www.efrag.org/en/projects/esrs-implementation-guidance-documents> (2024)[Accessed 01.08.2024].

EFRAG will continue to focus on set 2 of draft ESRS.24EFRAG. EFRAG delivers the first set of draft ESRS to the European Commission Brussels 1-2 (2022). This set will apply in addition to the current ESRS and will cover sectors such as textiles, information technology, electronics, pharmaceuticals, and biotechnology.13Sasfai, B., Mencher, M., Bichet, E., Eastwood, J. & Holm, S. European Union Adopts Long-Awaited Mandatory ESG Reporting Standards. Insights; the Corporate & Securities Law Advisor 37, 13-16 (2023). Specifically, they will create additional disclosure requirements related to topics particularly material for specific industries.13Sasfai, B., Mencher, M., Bichet, E., Eastwood, J. & Holm, S. European Union Adopts Long-Awaited Mandatory ESG Reporting Standards. Insights; the Corporate & Securities Law Advisor 37, 13-16 (2023). Furthermore, EFRAG is already in the development of ESRS for listed SMEs which should become effective on 1st of January 2026 with an option of opting out for two years.43EFRAG. ESRS LSME (ESRS for Listed SMEs), <https://www.efrag.org/en/projects/esrs-lsme-esrs-for-listed-smes/exposure-draft-consultation> (2024)[Accessed 02.08.2024].

Since 2025, new political and practical initiatives have expanded the scope of ESRS development. After a request of the European Commission to simplify EU rules and boost competitiveness back in February, EFRAG released their Progress Report on ESRS Simplification in June.44European Commission. Omnibus I package ‒ Commission simplifies rules on sustainability and EU investments. <https://finance.ec.europa.eu/publications/omnibus-i-package-commission-simplifies-rules-sustainability-and-eu-investments-delivering-over-eu6_en> (2025) [Accessed 09.09.2025]. In this, EFRAG describes six key levers to reach a >50 % reduction in the number of mandatory datapoints:

- Simplification of the Double Materiality Assessment

- Better readability/conciseness of the sustainability statements and better inclusion in corporate reporting as a whole

- Critical modification of the relationship between Minimum Disclosure Requirements and topical specifications

- Improved understandability, clarity and accessibility of the standards

- Introduction of other suggested burden-reduction reliefs

- Enhanced interoperability45EFRAG. EFRAG Releases Progress Report on ESRS Simplification. <https://www.efrag.org/en/news-and-calendar/news/efrag-releases-progress-report-on-esrs-simplification> (2025) [Accessed 09.09.2025].

Furthermore, EFRAG released the revised and simplified Exposure Drafts of the ESRS in July 2025 together with a 60-day public consultation survey in order to gather feedback from stakeholders across the reporting ecosystem. The goal is to maintain the relevance and alignment of sustainability reporting within the European Green Deal while making it easier to manage under the Corporate Sustainability Reporting Directive (CSRD). These drafts propose a reduction of mandatory data points by around 57% and of total data points by approximately 68%.46EFRAG. Press Release: EFRAG Shares Revised ESRS Exposure Drafts and Launches 60-Day Public Consultation. <https://www.efrag.org/en/news-and-calendar/news/press-release-efrag-shares-revised-esrs-exposure-drafts-and-launches-60day-public-consultation> (2025) [Accessed 09.09.2025].

In addition to simplification, new transition mechanisms are under discussion. In April 2025, the European Council finally approved the “Stop-the-clock” directive which postpones the dates of certain reporting and due diligence requirements. The entry of application of CSRD requirements for large companies that have not yet started reporting, as well as listed SMEs, was delayed by two years; the transposition deadline and the first application of the Corporate Sustainability Due Diligence Directive was delayed by one year.47Council of the EU. Simplification: Council gives final green light on the ‘Stop-the-clock’ mechanism to boost EU competitiveness. <https://www.consilium.europa.eu/en/press/press-releases/2025/04/14/simplification-council-gives-final-green-light-on-the-stop-the-clock-mechanism-to-boost-eu-competitiveness-and-provide-legal-certainty-to-businesses/> (2025) [Accessed 09.09.2025].

Another major development is the implementation of the VSME Standard (Voluntary Standard for Micro and Small Enterprises). This new framework allows very small companies which are not directly subject to CSRD to voluntarily disclose sustainability information in a simplified manner. The aim is to foster transparency within supply chains while avoiding excessive administrative burdens for these businesses.48 European Commission. Commission presents voluntary sustainability reporting standard to ease burden on SMEs. <https://finance.ec.europa.eu/publications/commission-presents-voluntary-sustainability-reporting-standard-ease-burden-smes_en> (2025) [Accessed 09.09.2025].

In summary, the further development of ESRS no longer focuses solely on the adoption of new, sector-specific standards but also incorporates substantial simplifications in order to maintain and boost the competitiveness of EU companies.

4 Structure and content

The published set 1 of ESRS includes the Act’s main text, twelve draft standards and a glossary of abbreviations and definitions.29Baumüller, J. & Sopp, K. European Sustainability Reporting Standards: Die EU-Konsultationsfassung vom Juni 2023: Überblick und kritische Würdigung. PiR-Internationale Rechnungslegung 19, 258-263 (2023). The draft standards cover all kinds of sustainability aspects.15Kommission, E. Fragen und Antworten zur Annahme europäischer Standards für die Nachhaltigkeitsberichterstattung (2023). Every standard also contains an Annex A with Application requirements.29Baumüller, J. & Sopp, K. European Sustainability Reporting Standards: Die EU-Konsultationsfassung vom Juni 2023: Überblick und kritische Würdigung. PiR-Internationale Rechnungslegung 19, 258-263 (2023). Additionally, the architecture of the standards follows the ‘three times three’ rule. This means that there are three layers of reporting, three reporting areas and three reporting topics14Zdolšek, D. & Beloglavec, S. T. Sustainability reporting ecosystem: a once-in-a-lifetime overhaul during the COVID-19 pandemic. Additionally, Sustainability 15, 7349 (2023).. In this case, the term “three layers of reporting” refers to reporting information specific to all sectors, reporting information specific to a single sector and reporting information specific to an organization. The three reporting areas represent strategy, implementation and performance. Last, the three reporting areas covered are environmental, social and governance.14Zdolšek, D. & Beloglavec, S. T. Sustainability reporting ecosystem: a once-in-a-lifetime overhaul during the COVID-19 pandemic. Additionally, Sustainability 15, 7349 (2023).

In total, there are 82 disclosure requirements provided in the ESRS.23Lanfermann, G. Einführung in die European Sustainability Reporting Standards (ESRS) in Haufe ESRS-Kommentar 1. Auflage: Kommentar zu den European Sustainability Reporting Standards (eds Jens Freiberg & Georg Lanfermann) 17-50 (Haufe-Lexware, 2023). The disclosure requirements can be divided into four categories which are policies, actions, targets and metrics.28Baumüller, J. Die Auswahl von Metriken in der Nachhaltigkeitsberichterstattung gemäß ESRS: Über welche Nachhaltigkeits-Kennzahlen müssen europäische Unternehmen fortan berichten? PiR-Internationale Rechnungslegung 19, 329-336 (2023). The thematic range of disclosure requirements is shown in the ESRS included list of topics. This list is also to be used while performing the materiality assessment. However, independent from the materiality assessment, companies will still have to deal with a broad range of sustainability topics.6Schnabel, J., Bareth, M. & Rathfelder, A. CSRD: Wettbewerbsnachteil oder Chance für den Mittelstand? PiR-Internationale Rechnungslegung, 242-250 (2023).

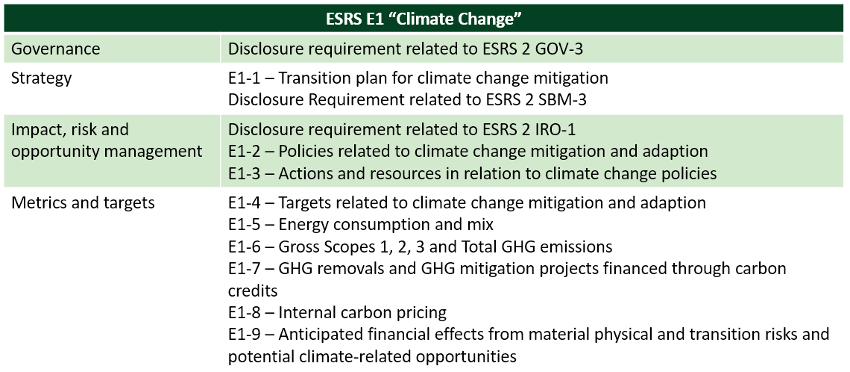

Disclosure requirements of the category metrics are defined at different levels of granularity. For example, ESRS E1-6 requires disclosure of the Gross Scopes 1, 2, and 3 and of the Total Greenhouse gas (GHG) emissions. Then, information concerning Scope 1 GHG emissions includes among others the following data points: The Scope 1 GHG emissions in metric tons of CO2 equivalent, the percentage of Scope 1 GHG emissions from regulated emissions trading schemes as well as disaggregated information for the Group consolidated for accounting purposes on the one hand and for further invested companies on the other hand.28Baumüller, J. Die Auswahl von Metriken in der Nachhaltigkeitsberichterstattung gemäß ESRS: Über welche Nachhaltigkeits-Kennzahlen müssen europäische Unternehmen fortan berichten? PiR-Internationale Rechnungslegung 19, 329-336 (2023).

Below, the disclosure requirements will be labelled as e.g. ESRS E1-1, being the first Disclosure Requirement (DR) of ESRS E1, or ESRS S3-2, being the second DR of ESRS S3. However, sections of the individual standards will be labelled as e.g. ESRS G1.6, being the sixth paragraph of ESRS G1, or ESRS E2.5, being the fifth of ESRS E2.

The following content, explaining the individual standards in detail, is primarily based on the Commentary on the European Sustainability Reporting Standards “Haufe ESRS-Kommentar 1. Auflage”.

4.1 Cross-cutting standards

4.1.1 ESRS 1 “General requirements”

The first cross-cutting standard focuses on the general requirements for preparing and presenting the sustainability report. Different from the other standards, ESRS 1 does not include disclosure requirements.49Baumüller, J., Lopatta, K. & Hrinkow, M. ESRS 1 – Allgemeine Anforderungen in Haufe ESRS-Kommentar 1. Auflage: Kommentar zu den European Sustainability Reporting Standards (eds Jens Freiberg & Georg Lanfermann) 87-173 (Haufe-Lexware, 2023). ESRS 1 supposed to convey the structure of the ESRS, introduces the principles they are based on as well as other foundations, describes general formal requirements for the report and explains phase-in regulations for first use of ESRS.49Baumüller, J., Lopatta, K. & Hrinkow, M. ESRS 1 – Allgemeine Anforderungen in Haufe ESRS-Kommentar 1. Auflage: Kommentar zu den European Sustainability Reporting Standards (eds Jens Freiberg & Georg Lanfermann) 87-173 (Haufe-Lexware, 2023). Additionally, ESRS 1 explains the principle of double materiality which requests information concerning material impacts on environment and society as well as financial ones.23Lanfermann, G. Einführung in die European Sustainability Reporting Standards (ESRS) in Haufe ESRS-Kommentar 1. Auflage: Kommentar zu den European Sustainability Reporting Standards (eds Jens Freiberg & Georg Lanfermann) 17-50 (Haufe-Lexware, 2023). However, further explanation concerning the materiality assessment will be given in the chapter about the practical implementation process, including the materiality assessment, of this work.

Next, ESRS 1 includes further attachments. For example, Appendix B shows impacts concerning qualitative characteristics of information which presents definitions of classifications and terminology. It includes further description of some terms and differences between disclosure requirements and recommendations.49Baumüller, J., Lopatta, K. & Hrinkow, M. ESRS 1 – Allgemeine Anforderungen in Haufe ESRS-Kommentar 1. Auflage: Kommentar zu den European Sustainability Reporting Standards (eds Jens Freiberg & Georg Lanfermann) 87-173 (Haufe-Lexware, 2023).

The first standard also demands that a company’s sustainability report includes all parts of its value chain. This means that additionally the reporting company has to address the impacts of the upstream and downstream economic activities, not differentiating between a direct or indirect connection to the company subject to reporting. Moreover, ESRS 1 introduces “incorporation for reference”. According to that, a company can reference other parts of reports done by them, as long as those parts are published at the same time as the sustainability report, undergo at least one audit review and meet the same requirements for the digitization of information. Integrated sustainability reporting allows references to other parts of the (Group) management report, the annual consolidated financial statements and to a possibly separately prepared governance or renumeration report.23Lanfermann, G. Einführung in die European Sustainability Reporting Standards (ESRS) in Haufe ESRS-Kommentar 1. Auflage: Kommentar zu den European Sustainability Reporting Standards (eds Jens Freiberg & Georg Lanfermann) 17-50 (Haufe-Lexware, 2023).

4.1.1.1 Structure of the ESRS

ESRS’ designed structure described in detail in ESRS 1. In general, the first set of ESRS includes two cross-cutting standards, being ESRS 1 and 2. They introduce general foundations of all required sustainability aspects and explain reporting in accordance with ESRS as a whole. The other ten standards are topical standards and can be assigned to three reporting pillars: Environmental, Social, and Governance. They specify certain disclosure requirements of the different sustainability aspects. Finally, there will also be sector-specific standards. Those are not yet finalized but should add disclosure requirements for companies working in specific sectors after completion. They are expected to allow a more detailed view on certain circumstances e.g. within an industry sector.49Baumüller, J., Lopatta, K. & Hrinkow, M. ESRS 1 – Allgemeine Anforderungen in Haufe ESRS-Kommentar 1. Auflage: Kommentar zu den European Sustainability Reporting Standards (eds Jens Freiberg & Georg Lanfermann) 87-173 (Haufe-Lexware, 2023).

The general cross-cutting standards are always to be taken into account. Contrary, the topical standards are subject to a materiality assessment. Therefore, companies only need to include full reporting of a thematic standard if it identified as material. Furthermore, sector-specific standards only apply to companies of the industry sector these standards refer to. ESRS 1 also includes in the section “Application Requirements” guidelines on reporting of company-specific information.49Baumüller, J., Lopatta, K. & Hrinkow, M. ESRS 1 – Allgemeine Anforderungen in Haufe ESRS-Kommentar 1. Auflage: Kommentar zu den European Sustainability Reporting Standards (eds Jens Freiberg & Georg Lanfermann) 87-173 (Haufe-Lexware, 2023).

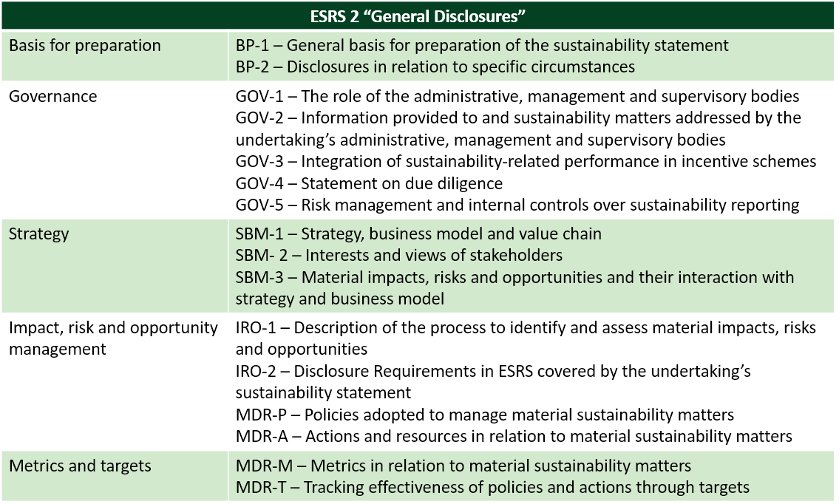

Next, ESRS 1 introduces the structure of the disclosure requirements given in the other standards. This structure will be reflected in the section “Disclosure Requirements” of ESRS 2 as well as in the topical and sector-specific standards. In detail, the disclosure requirements can be divided into four categories: (I) Governance (GOV), (II) Strategy and Business Model (SBM), (III) Impact, Riks and Opportunity Management (IRO) and (IV) Metrics and Targets (MT). First, GOV disclosure covers governance processes and the acts of controlling and monitoring. Second, SBM reflects the relationship of the reporting company with its material impacts, risks and opportunities. Third, IRO shows the processes of identifying impacts, risks and opportunities as well as materiality and manages sustainability matters. Last, MT disclosure is about measuring the company’s performance, including its set targets and its progress in reaching them.49Baumüller, J., Lopatta, K. & Hrinkow, M. ESRS 1 – Allgemeine Anforderungen in Haufe ESRS-Kommentar 1. Auflage: Kommentar zu den European Sustainability Reporting Standards (eds Jens Freiberg & Georg Lanfermann) 87-173 (Haufe-Lexware, 2023).

Disclosure requirements are not the smallest unit of ESRS. They are structured into datapoints which represent the smallest unit of requested qualitative or quantitative information. Additionally, disclosure requirements include “Application Requirements”, supplementing them with additional necessary interpretations or obligations at datapoint level.49Baumüller, J., Lopatta, K. & Hrinkow, M. ESRS 1 – Allgemeine Anforderungen in Haufe ESRS-Kommentar 1. Auflage: Kommentar zu den European Sustainability Reporting Standards (eds Jens Freiberg & Georg Lanfermann) 87-173 (Haufe-Lexware, 2023).

4.1.1.2 Further formal and content requirements for reporting

The Basis for Conclusions given in ESRS 1 explains that there might be further qualitative characteristics not explicitly featured in the ESRS but still to be considered by the company. Examples would be topics like “strategic focus and future orientation” or “Stakeholder inclusiveness”. Both are about the relationship between company and stakeholders. Another example would be the term “Connected Information” which refers back to the above-mentioned possible references and presents that the sustainability report should be connected with the financial one.49Baumüller, J., Lopatta, K. & Hrinkow, M. ESRS 1 – Allgemeine Anforderungen in Haufe ESRS-Kommentar 1. Auflage: Kommentar zu den European Sustainability Reporting Standards (eds Jens Freiberg & Georg Lanfermann) 87-173 (Haufe-Lexware, 2023).