Authors: Lukas Aehle, Jonas Ebeling, Benedikt Zimmer, Mattes Leibenath

Edited by: –

Last updated: October 2, 2025

Executive summary

The EU Taxonomy is a classification system that defines environmentally sustainable economic activities. It aims to guide investments toward activities that align with the EU’s climate neutrality goals under the European Green Deal. The taxonomy sets clear criteria for sustainability, including substantial contribution to environmental objectives, no significant harm to other objectives, and compliance with minimum social safeguards.

The framework enhances transparency in financial markets, mitigates greenwashing, and supports regulatory compliance. It requires companies to disclose the extent of their alignment with taxonomy criteria, influencing corporate reporting and investment strategies. Six environmental objectives form the foundation: climate change mitigation, climate change adaptation, sustainable use of water and marine resources, transition to a circular economy, pollution prevention and control, and biodiversity protection.

The taxonomy evolved through EU policy milestones, including the Paris Agreement and the EU Green Deal. It is implemented via Delegated Acts that define technical screening criteria. Practical application involves reporting obligations for large companies and financial institutions, supported by tools like the Taxonomy Navigator and User Guide.

Key drivers include alignment with policy goals, harmonization of sustainability standards, and improved market integrity. Barriers include data gaps, complexity, legal uncertainty, and conflicting requirements with other EU legislation. Despite challenges, the taxonomy is central to sustainable finance and is expected to expand its scope to SMEs and non-EU companies operating in Europe.

Recommendations for companies include integrating taxonomy reporting with regulatory training and ensuring accurate KPI aggregation. Legislative recommendations focus on flexibility, proportionality, and adapting criteria for global applicability.

Overall, the EU Taxonomy is a cornerstone of sustainable finance, promoting transparency, comparability, and investment certainty across the EU and potentially influencing global standards.

1 Definition and relevance

The EU taxonomy is a regulatory framework established by the European Union to create a single classification system that defines what constitutes environmentally sustainable economic activity. The taxonomy, which came into force in 2022, aims to support the EU’s transition to climate neutrality by 2050, as outlined in the European Green Deal. The taxonomy provides a detailed and standardized set of criteria for assessing the environmental sustainability of different economic activities. To be considered sustainable, an activity must meet certain requirements, including making a significant contribution to one or more of the six environmental objectives, avoiding significant harm to other objectives, and complying with minimum social safeguards.1Seán O’Reilly, L. G., Ciarán Mac An Bhaird & Niamh M. Brennan. Implementing the European Union Green Taxonomy: implications for small- and medium- sized enterprises. (2023). https://doi.org/10.1080/01559982.2023.2272394

The operational aspect of the EU taxonomy is implemented through Delegated Acts (DAs), which provide the Technical Screening Criteria (TSC) necessary to classify economic activities. These DAs serve to translate the general principles set out in the Taxonomy Regulation (TR) into specific criteria that companies are expected to follow. The first Climate Delegated Act, in force since January 2022, addresses economic activities related to climate change adaptation and mitigation, focusing on those that contribute to the reduction of greenhouse gas emissions in Europe. A second Delegated Act was introduced in June 2023, extending the criteria to the remaining environmental objectives. These developments aim to ensure that the taxonomy remains comprehensive and relevant to ongoing environmental objectives.2Ostojic, S., Simone, L., Edler, M. & Traverso. How Practically Applicable Are the EU Taxonomy Criteria for Corporates?—An Analysis for the Electrical Industry. 24 (2024). https://doi.org/https://doi.org/10.3390/su16041575

The framework also aims to bring consistency to financial markets by establishing standards for sustainability, which is considered important for preventing greenwashing – the practice of falsely representing products or activities as environmentally friendly. According to the Platform on Sustainable Finance, the taxonomy’s guidelines are intended to help investors, companies and policymakers align investments with environmental goals. This alignment is considered critical to promoting transparency and accountability in sustainable finance, with the goal of directing capital flows to activities that contribute to environmental sustainability while avoiding those that may cause significant harm.3Platform on Sustainable Finance. The Extended Environmental Taxonomy: Final Report on Taxonomy extension options supporting a sustainable transition. 133 (2022).

Overall, the EU taxonomy aims to guide sustainable investment, support regulatory compliance and promote transparency in financial markets, in line with the EU’s climate and environmental objectives. However, the effectiveness and practical impact of this framework remains subject to ongoing analysis and debate.

1.1 Relevance of the EU taxonomy

The EU taxonomy has significant relevance in several areas, including sustainable finance, corporate transparency, and regulatory compliance, all of which are integral to the global fight against climate change.

Guiding sustainable investment: The EU taxonomy is a critical tool for guiding investment towards truly sustainable activities. By providing a clear and scientifically validated classification system, it enables investors to make informed decisions and ensures that capital is directed in line with the EU’s environmental and climate goals. This is increasingly important as the global demand for sustainable finance grows, with the taxonomy serving as a key benchmark for assessing the sustainability of investments. According to the OECD (2020), the EU taxonomy plays an important role in shaping investment strategies by providing a consistent and reliable framework for identifying and supporting activities that contribute to environmental sustainability.4OECD. Developing Sustainable Finance Definitions and Taxonomies. Report No. 978-92-64-97779-2, (2020).

Regulatory compliance and corporate reporting: In addition to guiding investment, the EU taxonomy is critical for regulatory compliance, particularly in the area of corporate sustainability reporting. Companies operating in the EU are now required to disclose the extent to which their activities align with the taxonomy’s criteria, thereby increasing transparency and accountability. This requirement is particularly important for companies in the supply chains of larger companies that are also subject to the rules of the taxonomy. The requirement for detailed disclosure helps standardize how companies report their environmental impacts, making it easier for stakeholders to assess and compare sustainability performance across companies. According to the Task Force on Climate-related Financial Disclosures (TCFD) 2023 Status Report, the widespread adoption of TCFD-aligned frameworks, including the EU taxonomy, has significantly improved the consistency and comparability of corporate sustainability reporting across industries, supporting informed decision-making by investors and regulators.5Task Force on Climate-related Financial Disclosures. 2023 Status Report. 161 (2023).

Achieving climate and environmental goals: The role of the EU taxonomy in achieving its climate and environmental goals is complex and not without challenges. Recent studies have highlighted significant difficulties in applying the taxonomy’s Technical Screening Criteria (TSC), particularly in the electrical manufacturing sector. These challenges are particularly evident in the Substantial Contributions (SC) criteria, which are designed to support the transition to a low-carbon economy. The usability issues highlighted in these criteria suggest that further refinement and additional guidance may be needed to make them workable across industries. These challenges raise questions about the practicality of the taxonomy in its current form and whether it can effectively guide investment towards activities that truly contribute to the EU’s broader climate and environmental goals.2Ostojic, S., Simone, L., Edler, M. & Traverso. How Practically Applicable Are the EU Taxonomy Criteria for Corporates?—An Analysis for the Electrical Industry. 24 (2024). https://doi.org/https://doi.org/10.3390/su16041575

The relevance of the EU taxonomy in addressing the challenges for SMEs: Small and medium-sized enterprises (SMEs) are under increasing pressure to be environmentally responsible, especially as discussions at the EU level suggest that the requirements of the Corporate Sustainability Reporting Directive (CSRD) may be extended to more companies, potentially including SMEs by 2026. While SMEs do not currently have the same regulatory reporting obligations as larger companies, they are likely to gradually adopt sustainability disclosures due to economic, environmental and supply chain pressures. The implementation of the EU taxonomy presents both challenges and opportunities for SMEs, particularly in terms of the costs and resources associated with compliance. Accounting practitioners emphasize the need for educational, technological, and financial support to help SMEs meet these challenges. There is a strong call for government grants and incentives to help SMEs implement the taxonomy, as well as a desire for increased education to improve environmental literacy among accounting professionals. Despite the challenges, there is cautious optimism about the feasibility of taxonomy disclosures for SMEs, provided that appropriate support mechanisms are put in place.1Seán O’Reilly, L. G., Ciarán Mac An Bhaird & Niamh M. Brennan. Implementing the European Union Green Taxonomy: implications for small- and medium- sized enterprises. (2023). https://doi.org/10.1080/01559982.2023.2272394

Mitigating greenwashing: Another important issue addressed by the EU taxonomy is the mitigation of greenwashing in the financial sector. The International Journal of Science writes that greenwashing remains a significant issue in the sustainable finance sector, with companies often exaggerating or fabricating their environmental credentials. This problem undermines genuine sustainability efforts, as highlighted by UN Secretary-General António Guterres, who has condemned some net-zero claims as deceptive.6Make businesses truly sustainable. The international journal of science, nature (2023). https://doi.org/https://doi.org/10.1038/d41586-023-02550-4 Tettamanzi et al. say that the EU taxonomy has the potential to reduce greenwashing by creating standardized requirements for environmental sustainability disclosure. This standardization is particularly important in areas such as green bonds, where there is currently a lack of consistent and robust methodologies for assessing environmental impact, which may hinder the growth of sustainable finance.7Tettamanzi, P. T., Riccardo Gotti. Murgolo, Michael. The European Union (EU) green taxonomy: codifying sustainability to provide certainty to the markets. 26 (2023). The EU taxonomy not only aims to reduce greenwashing by establishing standardized sustainability disclosure requirements, but also plays a critical role in shaping global investment patterns. By providing a clear framework for assessing and disclosing environmental impacts, the taxonomy helps to ensure that sustainable finance efforts are genuine and effective. This approach is particularly important because it can guide global financial markets toward more transparent and consistent investment practices. The study by Lucarelli et al. (2023) emphasizes that while the taxonomy has not universally boosted corporate investment in all sectors, it does influence investment decisions in areas where there is less uncertainty. The paper suggests that the EU taxonomy could serve as a model for other regions and countries, contributing to the global harmonization of sustainable finance practices by promoting similar frameworks worldwide.8LUCARELLI, C. M., CAMILLA. RANCAN, MICHELA. SEVERINI, SABRINA. THE IMPACT OF EU TAXONOMY ON CORPORATE INVESTMENTS. Journal of Financial Management, Markets and Institutions, 32 (2023). https://doi.org/10.1142/S2282717X23500044

The EU taxonomy acts as a regulatory framework influencing corporate transparency and sustainable investment strategies within the EU, with the potential to serve as a reference point for global financial markets. Its approach to standardizing sustainability criteria could contribute to more consistent practices in sustainable finance internationally. In addition, the Framework’s efforts to address greenwashing and influence investment decisions underscore its broader importance. With these considerations in mind, it is important to examine the background and development of the EU taxonomy to better understand its underlying principles and the context in which it was created.

2 Background

Sustainability in the EU’s history: The EU taxonomy can be understood as the result of various processes and is a product of various political developments.9Claringbould, D., Koch, M. & Philip, O. Vol. 88, Iss. 2 11-27 (Duncker & Humblot, Berlin, 2019).

The concept of sustainability has been a significant element in the evolution of the European Union (EU) since its inception in 1972. This was the year in which the first agreement on an EU environmental policy was reached, which was subsequently implemented in a preliminary action plan in 1973. Both agreements are preceding the formalization of the concept of sustainability as we understand it today, which was first defined in the 1987 Brundtland Report.9Claringbould, D., Koch, M. & Philip, O. Vol. 88, Iss. 2 11-27 (Duncker & Humblot, Berlin, 2019). The popularization of the debate on sustainability was followed by several significant events, including the Environmental Action Programme and the Single European Act in 1987, the UN meeting in 1992, which resulted in the Rio Declaration, and the Maastricht Treaty in 1993. The latter combined economic activity with sustainable growth and introduced this concept into the European Community in a way that no previous agreement had done. Sustainability finally reached the general public with the Environmental Action Plan in 1993.9Claringbould, D., Koch, M. & Philip, O. Vol. 88, Iss. 2 11-27 (Duncker & Humblot, Berlin, 2019).

In the following decades, a discourse developed that increasingly focused on the financial sector and the financing of sustainability. The “Roadmap for moving to a competitive low-carbon economy in 2050” and the “Energy Roadmap 2050”, published in 2011, highlighted this issue and pointed out that public funds would probably not be sufficient for the transition, but that private capital should also be made available for these processes. Both the EU and Member States have the means to make this possible by creating an environment that encourages sustainable financing. This can be done through short-term planning certainty and long-term goals. The latter reduces the long-term risks that could be associated with a change in economic activity.9Claringbould, D., Koch, M. & Philip, O. Vol. 88, Iss. 2 11-27 (Duncker & Humblot, Berlin, 2019). An example of such a measure is the “Investment Plan for Europe” presented by the European Commission under Jean-Claude Jucker in November 2014. It aims to mobilize more than € 315 billion of investment (private and public) in the European economy by 2018 and is based on three main pillars:

- the mobilization of €315 billion between 2015 and 2018, with a focus on activating private investment.

- targeted investments that meet the needs of the economy

- the creation of an investment-friendly environment by reducing barriers and uncertainties, thus enhancing the attractiveness of the EU.10European Commission. An Investment Plan for Europe. Report No. COM/2014/0903 final, (2014).

Recent international developments in the field of sustainability and their impact on sustainable finance: When the UN General Assembly adopted a new global framework for sustainable development (also known as Agenda 2030) on September 25, 2015, it created 17 Sustainable Development Goals (SDGs) that are intended to represent a global agenda for the next 15 years. They were adopted by all 193 UN member states, in part because a committee of experts (the Intergovernmental Committee of Experts on Sustainable Development Financing, or ICESDF) was tasked with addressing the issue of financing sustainable development. The result of this lengthy process is a document that sets far more ambitious goals than comparable previous agreements.11Martens, J. & Obenland, W. in Globale Zukunftsziele für nachhaltige Entwicklung, 30th edn. Global Policy Forum.

The Commission of the European Union responded to the requirements of the 2030 Agenda in November 2016 with a communication entitled “Next steps for a sustainable European future – European action for sustainability”.12Generalsekretariat der Europäische Kommission. Auf dem Weg in eine nachhaltige Zukunft Europäische Nachhaltigkeitspolitik. Report No. COM(2016) 739 final, (2016). It states that, in relation to the Agenda 2030 goal of a deeper and fairer single market with a strengthened industrial base, a “new and forward looking approach to achieving sustainable finance” should be promoted (p. 10).12Generalsekretariat der Europäische Kommission. Auf dem Weg in eine nachhaltige Zukunft Europäische Nachhaltigkeitspolitik. Report No. COM(2016) 739 final, (2016). This is why finance is a key issue, especially for UN SDGs 8, 9, 13, 14 and.13Janetschek, H., Brandi, C., Dzebo, A. & Hackmann, B. The 2030 Agenda and the Paris Agreement: voluntary contributions towards thematic policy coherence. Climate Policy 20 (2020-4-20). https://doi.org/10.1080/14693062.2019.1677549 This document also proposes, for the first time, a high-level expert group to develop a strategy for EU-wide sustainable finance. Two tasks are highlighted:

- to examine how European financial markets can be used to make the financial system more resilient.

- how the resulting recommendations might be transferred to other sectors.12Generalsekretariat der Europäische Kommission. Auf dem Weg in eine nachhaltige Zukunft Europäische Nachhaltigkeitspolitik. Report No. COM(2016) 739 final, (2016).

Another agreement that has already had a major impact on the sustainable finance debate, and thus on the EU taxonomy in 2015, is the Paris Agreement. This is one of the most famous agreements adopted at the 21st Conference of the Parties (COP21) of the United Nations Framework Convention on Climate Change in 2015.14Delbeke, J., Runge-Metzger, A., Slingenberg, Y. & Werksman, J. The Paris Agreement. Towards a Climate-Neutral Europe 1, 22 (2019/10/16). https://doi.org/10.4324/9789276082569-2 Originally signed by 174 countries and the EU, the treaty now has 184 parties. The agreement has a number of unique features. For example, the agreement applies equally to all countries, but they must set out their contributions to the joint emission reduction targets in their Nationally Determined Contributions. Transparency and accountability are intended to increase international pressure. A particularly ambitious goal of the Paris Agreement is the “2 degree climate target”, which states that the average global temperature increase must remain “well below 2°C” above pre-industrial levels. At a minimum, countries should be “pursuing efforts to limit the temperature increase to 1.5°C”(Article 2 of the Paris Agreement).14Delbeke, J., Runge-Metzger, A., Slingenberg, Y. & Werksman, J. The Paris Agreement. Towards a Climate-Neutral Europe 1, 22 (2019/10/16). https://doi.org/10.4324/9789276082569-215United Nations. Paris Agreement. (Paris, 2015). Of particular interest for the development of sustainable finance is the statement that governments should cooperate more and align financial flows with the goals. The potential of private investment, which should be redirected towards sustainable investments, is also highlighted. The Nationally Determined Contributions of the states for the Paris Agreement were often strongly linked to the UN SDGs, so that a strong connection can be assumed. We can speak of a radical shift towards voluntary commitments for all.13Janetschek, H., Brandi, C., Dzebo, A. & Hackmann, B. The 2030 Agenda and the Paris Agreement: voluntary contributions towards thematic policy coherence. Climate Policy 20 (2020-4-20). https://doi.org/10.1080/14693062.2019.1677549 The Paris Agreement is directly responsible for some of the measures implemented by the EU in the following years.13Janetschek, H., Brandi, C., Dzebo, A. & Hackmann, B. The 2030 Agenda and the Paris Agreement: voluntary contributions towards thematic policy coherence. Climate Policy 20 (2020-4-20). https://doi.org/10.1080/14693062.2019.1677549

Launched in 2015, the Capital Markets Union (CMU) was initially tasked with supporting the third pillar of the Investment Plan for Europe, namely creating an investment-friendly environment in the EU that can secure the necessary investment to meet the goals outlined in the Paris Agreement.16European Commission. Action Plan on Building a Capital Markets Union. Report No. COM(2015) 468 final, (2015).17Remer, S. High Level Expert Group on Sustainable Finance (HLEG). (2020). The Action Plan already indicated that the Commission intends to review previous regulatory reforms for coherence and consistency with the CMU, also to ensure that private investments are made as long-term sustainable investments. The “Capital Markets Union – Accelerating Reform” of September 2015 streamlined and clarified the CMU’s responsibilities and objectives. The reform should help to speed up the impact on the real economy. Among other things, sustainable finance is explicitly mentioned as a possible transformative force in the European capital market.18European Commission. Capital Markets Union – Accelerating Reform. Report No. COM(2016) 601 final, (2016).

The Commission therefore concluded that an expert group should be set up to develop a comprehensive European strategy on green finance. The High Level Expert Group on Sustainable Finance (HLEG) was established in December 2016 to advise the European Commission.19European Union. (Directorate-General for financial Stability, Financial Services and Capital Markets Union, 2020). The expert group consisted of 20 members from the public, the financial sector, academia and European institutions.17Remer, S. High Level Expert Group on Sustainable Finance (HLEG). (2020). They included representatives of NGOs and think tanks, insurance companies and banks, economists and financial experts, and observers from international and European institutions.19European Union. (Directorate-General for financial Stability, Financial Services and Capital Markets Union, 2020). The mandates given to the Expert Group were:

- to encourage public and private investors to move towards sustainable investment.

- to analyze the environmental impacts and risks on financial institutions and to identify necessary measures for greater resilience.

- to identify how these measures can be applied in a global context.19European Union. (Directorate-General for financial Stability, Financial Services and Capital Markets Union, 2020).

But the goals also included enabling an EU-wide sustainable financial system and economy, not jeopardizing the stability of CO2-intensive institutions, and contributing to the goals of the Paris Agreement and the 2030 Agenda. It was decided that the committee would work on the basis of regular exchanges and stakeholder meetings. An interim report with the results of the initial findings would be issued after approximately six months. The final report with proposals for policy actions and an outlook on the short-, medium- and long-term planning horizon was to be published in December 2017.20Secretariat within the Directorate General for Financial Stability, F. S. & Union, a. C. M. (2017).

Towards an EU taxonomy: The Interim Report of the High-Level Expert Group on Sustainable Finance was published in July 2017, and powerfully describes the need for a coherent EU-wide strategy that shows investors what sustainable investment opportunities could look like. In addition, the strategy needs to show exactly how the capital needed for the goals of the 2030 Agenda and the Paris Agreement will be achieved.21High-Level Expert Group on Sustainable Finance. Interim Report. (2017).

According to the expert group, a single EU-wide classification system is needed to make this possible. The lack of a standard in sustainable finance has already been criticized by many institutions and would hinder the implementation of measures in this critical area.21High-Level Expert Group on Sustainable Finance. Interim Report. (2017).

The interim report still refers to this as the “Sustainability Taxonomy”. According to the Expert Group, the benefits would be that investors would be assured that the investments they make are indeed understood as sustainable investments. In addition, consumers and policymakers would have greater transparency, including with regard to greenwashing. The benefit to companies and policymakers of having a better and more concrete understanding of their policies is also mentioned. It also allows for more objective reporting, both by companies and by the public and media. In particular, the taxonomy has the potential to become a reference point for financial product standards, as it makes it possible to objectively measure a company’s sustainability or share of sustainable activities.21High-Level Expert Group on Sustainable Finance. Interim Report. (2017).

This taxonomy would need to be accepted by the market by involving stakeholders in the process of developing the taxonomy. Such a taxonomy could then contribute to the development of other standards and help them to reach their full potential (e.g., an EU standard for green bonds). In this area in particular, stakeholders have already experienced the effects of a fragmented standards market. Different vendors and institutions have developed their own green bond taxonomies, creating uncertainty, lack of comparability and efficiency issues for investors, as these standards are not formally linked to EU or UN agreements and policy guidelines.21High-Level Expert Group on Sustainable Finance. Interim Report. (2017). According to the expert group, the taxonomy should also take into account all acceptable definitions of sustainability in order to ensure the widest possible support.21High-Level Expert Group on Sustainable Finance. Interim Report. (2017).

It is emphasized that the development of a common classification should focus on products/services that support the following policy objectives: 1. Climate change mitigation; 2. Climate change adaptation; 3. Biodiversity loss; 4. Natural Resource Depletion; 5. Pollution prevention and control.21High-Level Expert Group on Sustainable Finance. Interim Report. (2017).

The development of a taxonomy for the above policy objectives should be guided by a step-by-step approach, building on experts’ experience and existing standards. In addition, the taxonomy should differentiate between sustainability goals and sectors and be formulated with sufficient precision.21High-Level Expert Group on Sustainable Finance. Interim Report. (2017).

The final report in 2018 declares the taxonomy to be one of the most important goals that a sustainable European economy should pursue. Although the Expert Group emphasizes that there is no silver bullet that can be used to transform the European economy towards sustainability, the taxonomy is a top priority because it enables the discourse on other levers. If, as suggested in the interim report, the European Commission starts with a taxonomy focused on climate change mitigation, it will be possible to identify which areas require the most urgent investment.22High-Level Expert Group on Sustainable Finance. Final Report 2018. (2018).

The EU Commission naturally took note of these proposals of the High-Level Expert Group on Sustainable Finance and responded to the final report in March 2018 with the “Action Plan: Financing Sustainable Growth”, where the action plan directly addresses the eight proposals of the final report. The top priority and Action 1 of the plan is therefore the introduction of an EU-wide classification system for sustainable activities. Two tasks have been identified for this purpose:

- Develop a legislative proposal in the second quarter of 2018 that enables and ensures the development of the taxonomy, taking into account the work done so far. The taxonomy should be incorporated into European law as soon as possible.

- Establish a “Technical Expert Group on Sustainable Finance” to consult all relevant stakeholders and then develop a first proposal for a taxonomy with a focus on climate change mitigation. This should be presented in the first quarter of 2019 and extended to other key areas in the second quarter of 2019.

Some other actions in the plan build directly on the implementation of the taxonomy, such as actions on an EU Ecolabel framework, on sustainability benchmarks or on risk calculations for banks and insurance companies. Accordingly, the EU Commission has followed all recommendations of the HLEG on the taxonomy and has also mandated a new Technical Expert Group (TEG) to develop a first proposal for the taxonomy.23European Commission. Action Plan: Financing Sustainable Growth. Report No. COM(2018) 97 final, (2018). The preparatory work of the HLEG gave the TEG the necessary momentum and validity.24Tripathy, A., Mok, L. & House, K. Defining Climate-Aligned Investment: An Analysis of Sustainable Finance Taxonomy Development. 96 (2020).

It was possible to apply for a place in this Technical Expert Group. A total of 185 valid applications were received, from which the European Commission selected 35 people from various fields, such as the HLEG. Here, too, various working groups and discussions with experts from the various fields were to ensure a lively exchange over the course of a year.25European Commission. Commission announces members of the Technical Expert Group on Sustainable Finance. (2018).

Because the Commission gave the TEG such a short time to develop such a large concept, the development process had to be streamlined. Therefore, TEG members were assigned to chair specific sectors for which the taxonomy would be developed, and other members and experts were made available to assist. This approach is not uncommon and has been used in the development of the Climate Bonds Initiative Taxonomy. Other details of the process are also inspired by other past initiatives, such as the basic structure of the stakeholder meetings and discussions. In order to structure these, a guideline was developed that refers in particular to the sustainability impacts of the sector, principles and relevant legislation, thus allowing for a consistent parallel development in the different areas. A key difference in the development was the reference to the EU’s NACE classification of economic activities (Nomenclature des Activités Économiques dans la Communauté Européenne) in order to identify sectors and industries and thus to structure the subject matter from the outset.24Tripathy, A., Mok, L. & House, K. Defining Climate-Aligned Investment: An Analysis of Sustainable Finance Taxonomy Development. 96 (2020). In addition, the researchers believe that the face-to-face meetings in Brussels during the development process contributed to the rapid development.24Tripathy, A., Mok, L. & House, K. Defining Climate-Aligned Investment: An Analysis of Sustainable Finance Taxonomy Development. 96 (2020).

In March 2020, the TEG published its “Final Report of the Technical Expert Group on Sustainable Finance”. This is a proposal for the implementation of a taxonomy regulation, which includes very specific proposals in an annex with Technical Screening Criteria.26EU Technical Expert Group On Sustainable Finance. Taxonomy: Final report of the Technical Expert Group on Sustainable Finance. (2020).27EU Technical Expert Group On Sustainable Finance. Taxonomy Report: Technical Annex. 593 (2020). Together, the two documents are often referred to as the “EU Taxonomy”. Meanwhile, under Ursula von der Leyen, the EU presented the EU Green Deal, which is a comprehensive plan of various EU actions to both mitigate climate change and implement the 2030 Agenda, as well as a growth strategy to create a competitive economy.28Fetting, C. (ESDN Office, Vienna, December 2020). The EU Green Deal is closely aligned with the objectives of the Action Plan on Financing Sustainable Growth, which also initiated the development of the EU taxonomy.29Dudout, A., Vitulano, C. & François, C. EXPLORING THE IMPLEMENTATION OF THE EU TAXONOMY FOR FINANCIAL INSTITUTIONS. (AVANTAGE REPLY, September 2021). It is therefore clear that the EU taxonomy is considered an essential component of the EU Green Deal.30Directorate-General for Financial Stability & Financial Services and Capital Markets Union. EU taxonomy for sustainable activities.

The EU taxonomy was also implemented quickly in the context of the EU Green Deal. In December 2019, before the publication of the final report of the TEG, an agreement was reached between the European Council and the European Parliament on a taxonomy regulation. This was published on June 22, 2020 as “Regulation (EU) 2020/852 of the European Parliament and of the Council of 18 June 2020 on the establishment of a framework to facilitate sustainable investment, and amending Regulation (EU) 2019/2088” and entered into force on July 12, 2020.31List, P., Schiappacasse, M. & Dechert LLP. Overview of the EU taxonomy regulation, <https://www.aima.org/article/overview-of-the-eu-taxonomy-regulation.html> (30.11.2020).

The regulation itself provides the legal framework, setting out general principles, definitions and obligations. The final report of the TEG is a technical document that provides specific criteria and recommendations for putting the concepts defined in the Regulation into practice. The technical screening criteria contained therein form the basis for the subsequent delegated acts. The Regulation instructs the European Commission to adopt delegated acts, which make these specific criteria and measures binding. These delegated acts may be updated over time to take account of scientific progress and market changes. The Platform on Sustainable Finance will further develop these delegated acts by building on the work of the TEG and seeking expert views on the necessary technical screening criteria.

3 Content of the law

The first chapter of the Regulation (EU) 2020/85232 sets out the subject matter, scope and definitions. Article 1 defines the Regulation’s subject matter, “establishing criteria for determining whether an economic activity qualifies as environmentally sustainable”, which helps assess the degree of environmental sustainability of an investment. Article 1, paragraph 2 addresses three groups: 1) EU member states and the EU itself, 2) financial market participants who offer financial products, and 3) companies obligated to publish non-financial statements, with a particular focus on European issuers of securities traded on capital markets. Article 2 defines key terms used in the Regulation, including basic terms such as “good status” up to “soil”. These definitions are essential to ensure a common understanding of the environmental and climate change criteria.27EU Technical Expert Group On Sustainable Finance. Taxonomy Report: Technical Annex. 593 (2020).

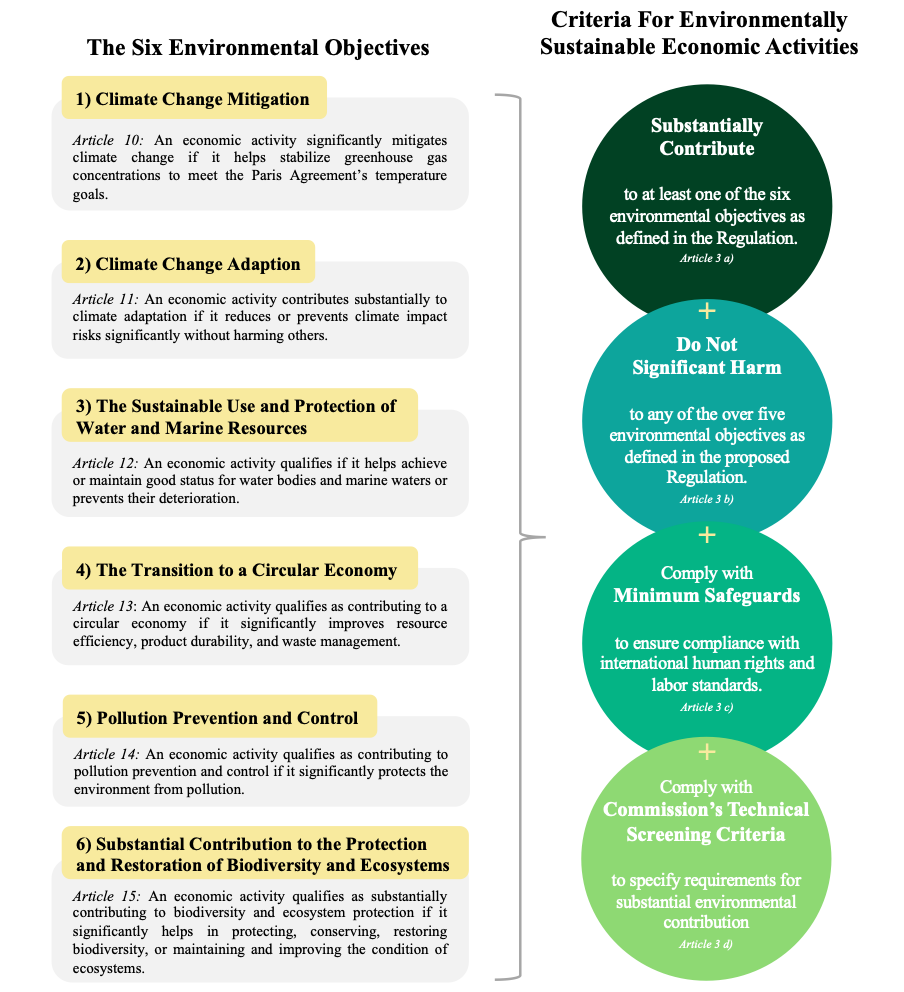

The second chapter deals with environmentally sustainable economic activities. For an economic activity to be considered environmentally sustainable, Article 3 requires that it “contributes substantially to one or more of the environmentally objectives”, “does not significantly harm (DNSH) any of these […] objectives”, “is carried out in compliance with the minimum safeguard”, and meet the technical assessment criteria established by the Commission. This article is explained in more detail when Figure 1 is explained.

Articles 5 to 8 set out the transparency requirements for financial products and companies in relation to environmental sustainability. Financial products must disclose in their ex-ante and periodic reports how their investments meet environmental objectives (Article 5) and, where applicable, which parts of their investments meet the EU sustainability criteria (Article 6). Financial products that do not fall into these categories must state that their investments do not meet these criteria (Article 7). Companies required to disclose non-financial information must explain how their activities are environmentally sustainable, including financial expenditure and turnover in this area (Article 8).

The six environmental objectives: The six environmental objectives (EO) are set out in Article 9 and are 1) to mitigate climate change, 2) to adapt to climate change, 3) to use and protect water and marine resources sustainably, 4) to move towards a circular economy, 5) to prevent and control pollution, 6) to contribute significantly to the protection and restoration of biodiversity and ecosystems. These objectives are relevant to the scheme and are illustrated in Figure 1.

As can be seen in Figure 1, each of the environmental objectives has its own article with subsections for explanation and scope. These help to categorize sustainable activities and refer to further regulations, directives or annexes where necessary. In the following each article of the EO are explained in detail.

EO 1: Article 10 focuses on climate change mitigation: Activities must stabilize greenhouse gas (GHG) concentrations to meet the Paris Agreement goals. This includes advancing renewable energy, improving energy efficiency, and implementing carbon capture technologies. Activities should be exemplary in their field, support green technologies, and avoid locking in carbon.

EO 2: Article 11 covers climate change adaptation: Activities qualify if they significantly reduce climate impact risks without harming other environmental goals. Solutions must be evaluated with climate projections to ensure they address specific risks effectively. The European Commission set criteria for substantial adaptation, ensuring no significant harm to other goals, with these criteria in place by January 2022.

EO 3: Article 12 addresses the sustainable use of water and marine resources: Economic activities must help maintain or improve the status of water bodies and marine waters or prevent their deterioration. This involves better water management, protecting aquatic ecosystems, and reducing pollution in marine environments.

EO 4: Article 13 promotes the transition to a circular economy: Activities should enhance resource efficiency, product durability, and waste management. This includes improving product longevity, increasing recyclability, and minimizing waste through better recycling and disposal methods.

EO 5: Article 14 deals with pollution prevention and control: Activities must significantly reduce environmental pollution. The European Commission has defined specific criteria, which were finalized at the end of 2021 and will be applied from January 2023, to ensure that the activities do not have a negative impact on other environmental objectives.

EO 6: Article 15 focuses on biodiversity and ecosystem protection: Economic activities must contribute significantly to protecting, conserving, or restoring biodiversity and improving ecosystem conditions. Criteria were to be adopted by December 31, 2021, and implemented from January 1, 2023, to prevent significant harm to other environmental goals.

Criteria for environmentally sustainable economic activities: According to the Regulation and as shown in the right part of Figure 1, an economic activity is environmentally sustainable if it cumulatively meets the following criteria (shown as circles in Figure 1). According to the “substantial contribution” (Article 3a), the economic activity must contribute to at least one of the six environmental objectives. Furthermore, an economic activity shall qualify as environmentally sustainable where that economic activity “does not significantly harm any of the environmental objectives set out in Article 9”. This means that the activity must not only have positive effects, but also not cause significant damage to the environmental objectives (Article 3b). Economic activities must be conducted in compliance with a defined minimum level of protection. This minimum level of protection is defined in Article 18 and sets out basic environmental standards that must be respected. Companies must fulfil minimum requirements for the protection of human rights and workers’ rights by complying with the OECD Guidelines for Multinational Enterprises and the UN Guiding Principles on Business and Human Rights (Article 3c, Article 18). In addition, the activity must comply with the technical assessment criteria established by the European Commission in accordance with Articles 10-15 and their sub-paragraphs. These criteria serve to define the environmental requirements in concrete and measurable terms and to ensure that the economic activity fulfils the required standards (Article 3d). The technical screening criteria are laid down in delegated acts. The performance thresholds are based on scientific evidence, have been developed using a valid methodology and consider the current state of the art and are therefore referred to as “dynamic documents”.32European Commission. Implementing and delegated acts – Taxonomy Regulation. These can be viewed, for example, in an annex to the delegated act mentioned above. As an example, the criteria for the manufacturing of plastic packaging products can be found on pages 2 to 7. They are designed to encourage sectors to adapt to the EU’s climate and environmental objectives.33European Commission. Annex 2 To The Commission Delegated Regulation (EU) 2020/852. 77 (Brussels, 2023).

Article 16 describes enabling activities as those that pave the way for other environmentally beneficial activities without creating long-term environmentally harmful lock-in effects and that have an overall positive environmental impact based on life-cycle considerations. Lock-in means that the enabling activity must not contribute to the continued use or promotion of environmentally damaging assets, even if they are detrimental to long-term environmental objectives.34Schütze, F., Stede, J., Blauert, M. & Erdmann, K. EU taxonomy increasing transparency of sustainable investments. Report No. ISSN 2568-7697, 485-492 (Deutsches Institut für Wirtschaftsforschung (DIW), Berlin, 2020). Article 16 applies to a company that produces energy-efficient components for wind turbines. Article 17 defines which criteria qualify an economic activity as significantly harmful to environmental objectives by considering negative impacts on the six environmental objectives, including the entire life cycle of products and services. Article 19 stipulates that these criteria must be technology-neutral, based on scientific evidence and consider the entire life cycle of the activities. They must be regularly reviewed and updated to keep pace with scientific and technological developments. The criteria set out in the taxonomy define economic activities that either contribute directly to environmental objectives or enable others to do so. They also include transitional activities in Article 19 1) h) ii), such as cement and steel production, which will be adapted to the EU’s climate targets through new technologies. These criteria will be reviewed every three years and adjusted as necessary.35Umweltbundesamt. Eine Taxonomie als Schlüssel zum Erfolg von Sustainable Finance, <https://www.umweltbundesamt.de/eine-taxonomie-als-schluessel-erfolg-von-0#die-taxonomie-als-herzstuck-des-aktionsplans-sustainable-finance> (2023). Article 20 establishes the Platform on Sustainable Finance, which advises the Commission on the technical criteria and analyzes their impact. Under Article 21, Member States are responsible for monitoring compliance with the requirements and establishing appropriate measures and penalties (Article 22). Article 23 regulates the powers of the Commission to adopt and amend delegated acts, while Article 24 introduces the Member States’ expert group on sustainable finance to improve exchange and consultation. Finally, Article 26 provides for regular evaluations of the Regulation to review its effectiveness and make adjustments.

Example: Annex 2 to the Commission Delegated Regulation (EU) 2020/852 can be used as an example of how companies can put theory into practice. A plastic packaging manufacturer is used as an example. According to article 13, the production of plastic packaging can make a significant contribution to the circular economy if companies meet certain sustainability criteria. According to the EU taxonomy, companies producing plastic packaging must ensure that by 2028 at least 35% of the packaging weight is made of recycled material for non-contact sensitive packaging and at least 10% for contact sensitive packaging. By 2032, these requirements will increase to 65% and 50%, respectively. These requirements encourage the use of recycled materials and reduce dependence on primary raw materials. Packaging must also be designed to be recyclable at the end of its life cycle. This means that packaging should either be made from a single material, or all components should be recyclable. Packaging that contains design elements or additives that are difficult to recycle does not meet the technical criteria of the taxonomy. In addition, packaging materials must be practically recyclable on a large scale and achieve the minimum recycling rates set out in Directive 94/62/EC. The raw materials used shall not contain hazardous substances as defined in Regulation (EC) No. 1272/2008, to avoid risks to health and the environment. As part of the DNSH assessment, GHG emissions of materials made from chemically recycled plastic shall be lower than those of comparable plastics made from fossil raw materials. For instance, in order not to harm the first environmental objective, climate change mitigation, greenhouse gas emissions must be quantified and verified by an independent body in accordance with ISO 14067:2018 or ISO 14064-1:2018.33European Commission. Annex 2 To The Commission Delegated Regulation (EU) 2020/852. 77 (Brussels, 2023).

Policy making timeline: The EU taxonomy is essentially dependent on the further development of Delegated Acts, which will deepen and define how market players and authorities can implement the Taxonomy Regulation. In order to facilitate this development, Article 8 and Articles 10 to 15 of the Regulation provide for the adoption of these delegated acts by the Commission. Prior to adoption, the Commission should seek advice from the Sustainable Finance Platform and the Member State Expert Group on Sustainable Finance.36European Parliament. REGULATION (EU) 2020/852 OF THE EUROPEAN PARLIAMENT AND OF THE COUNCIL of 18 June 2020 on the establishment of a framework to facilitate sustainable investment, and amending Regulation (EU) 2019/2088. 31 (Brussels, 2020).

The Sustainable Finance Platform is described in Article 20 of the Taxonomy Regulation. It also consists of experts from various groups, such as European Authorities, private market stakeholders, experts representing civil society, experts of this legislation and from academia.33European Commission. Annex 2 To The Commission Delegated Regulation (EU) 2020/852. 77 (Brussels, 2023). It was initially mandated for 2 years, with a call for applications for the new mandate in October 2022. The main task of the Platform is to advise the EU Commission on the design, implementation and usability of the EU taxonomy through dialogue and close cooperation.37Directorate-General for Financial Stability – Financial Services and Capital Markets Union.

The Member State Expert Group on Sustainable Finance was also set up under Article 24 of the Regulation to advise the Commission on the adoption of the technical screening criteria. The focus is on coordinating the views of EU Member States on projects in the taxonomy.36European Parliament. REGULATION (EU) 2020/852 OF THE EUROPEAN PARLIAMENT AND OF THE COUNCIL of 18 June 2020 on the establishment of a framework to facilitate sustainable investment, and amending Regulation (EU) 2019/2088. 31 (Brussels, 2020).

The taxonomy provides for the publication of several delegated acts to be adopted and applied at different times. Article 8, which deals with transparency, should be adopted by 1 June 2021. Articles 10 and 11, which deal with climate change mitigation and adaptation, should be adopted by 31 December 2020 and apply from 1 January 2022. Articles 12, 13, 14 and 15, which deal with the sustainable use and protection of water and marine resources, the circular economy, pollution prevention and control, and the protection and restoration of biodiversity and ecosystems, should be adopted by 31 December 2021 and apply from 1 January 2023.36European Parliament. REGULATION (EU) 2020/852 OF THE EUROPEAN PARLIAMENT AND OF THE COUNCIL of 18 June 2020 on the establishment of a framework to facilitate sustainable investment, and amending Regulation (EU) 2019/2088. 31 (Brussels, 2020).

The first two Delegated Acts were adopted in June 2021: The Climate Delegated Act, which provides the necessary technical screening criteria for climate change mitigation and adaptation, and the Disclosure Delegated Act, which refines Article 8 of the Taxonomy Regulation.32European Commission. Implementing and delegated acts – Taxonomy Regulation. In July 2022, the Complementary Climate Delegated Act was passed, dealing in particular with the controversial issue of the inclusion of nuclear energy and natural gas in the taxonomy, which previously had to be omitted from the first Climate Delegated Act.38Riasat, A. in THE NORMATIVE IMPERATIVE – SOCIOPOLITIAL CHALLENGES OF STRATEGIC AND ORGANIZATIONAL COMMUNICATION (eds EVANDRO OLIVEIRA & GISELA GONÇALVES) 35-44 (2023).32European Commission. Implementing and delegated acts – Taxonomy Regulation. In June 2023, the requirements of the last four Environmental Objectives were implemented in the Environmental Delegated Act.32European Commission. Implementing and delegated acts – Taxonomy Regulation. Accordingly, not all target deadlines set were met.39Gortsos, C. V. & Kyriazis, D. The Taxonomy Regulation and Its Implementation. Sustainable Finance in Europe(2024). https://doi.org/10.1007/978-3-031-53696-0_13

In order to comply with Article 20 (2c) of the Taxonomy Regulation (i.e. the obligation of the Platform on Sustainable Finance to process stakeholder requests for changes and adjustments to the Technical Screening Criteria), the Stakeholder Request Mechanism was introduced in October 2023. This allows companies to use an online tool to submit low-threshold proposals for new additions or changes to the Technical Screening Criteria to the Platform on Sustainable Finance.30Directorate-General for Financial Stability & Financial Services and Capital Markets Union. EU taxonomy for sustainable activities.40European Commission. EU taxonomy stakeholder request mechanism, <https://finance.ec.europa.eu/sustainable-finance/overview-sustainable-finance/platform-sustainable-finance/stakeholder-request-mechanism_en> (

4 Practical implementation

Overview of reporting obligations: In accordance with Article 8 of the EU Taxonomy Regulation, which defines the main reporting obligations, the companies concerned must disclose the scope of their environmentally sustainable business activities. A distinction is made between financial and capital market-oriented companies.36European Parliament. REGULATION (EU) 2020/852 OF THE EUROPEAN PARLIAMENT AND OF THE COUNCIL of 18 June 2020 on the establishment of a framework to facilitate sustainable investment, and amending Regulation (EU) 2019/2088. 31 (Brussels, 2020).41Schnabel, J. & Dr. Schmidt, R. Nachhaltiges Wirtschaften wird messbar Controlling & Management Review 66, 50-53 (2022).

Capital market-oriented companies with more than 500 employees must disclose taxonomy ratios for the key performance indicators (KPIs) share of revenue, share of capital expenditure (CapEx) and share of operating expenses (OpEx) in the non-financial report. The content requirements have been CSRD-compliant since 2023.41Schnabel, J. & Dr. Schmidt, R. Nachhaltiges Wirtschaften wird messbar Controlling & Management Review 66, 50-53 (2022).

Financial companies such as banks, insurance companies and investment funds must also disclose investments in sustainable activities. In order to fulfil the reporting obligations, financial companies require taxonomy-relevant information on the companies in their portfolios. This means that other companies may also be indirectly affected by the EU taxonomy.41Schnabel, J. & Dr. Schmidt, R. Nachhaltiges Wirtschaften wird messbar Controlling & Management Review 66, 50-53 (2022). Based on this information, financial institutions must report the Green Asset Ratio (GAR) in accordance with Article 4 of the Second Delegated Act. Garcia-Torea et al. (2024) describe the GAR as “the required metric to measure the extent to which these entities are exposed to taxonomy-aligned economic activities“ (p. 7).42Garcia-Torea, N., Luque-Vílchez, M. & Rodríguez-Gutiérrez, P. The EU Taxonomy, sustainability reporting and financial institutions: understanding the elements driving regulatory uncertainty. ACCOUNTING FORUM, 1-28 (2024). https://doi.org/10.1080/01559982.2024.2364953

The taxonomy is subject to ongoing expansion. In the 2025 reporting year, the EU resolved to categorize companies that satisfy two or more of the following criteria as subject to reporting requirements: a balance sheet total exceeding 20 million euros, net sales in excess of 40 million euros, or a workforce of over 250 employees. From the 2026 financial year onwards, the scope of the taxonomy will be expanded to include listed small and medium-sized enterprises (KMUs in German). In addition, companies that are not European but have an EU branch or a subsidiary based in the EU, and that generate net sales of at least 150 million euros, will be subject to reporting requirements from 2028 onwards.43Prof. Dr. von Düsterlho, J.-E. & Mohr, M. Sustainable FInance – Neue Regelwerke stellen Unternehmen vor anspruchsvolle Berichtspflichten. (HAW Hamburg, Hamburg, 2023).

EU-given implementation tools: The European Commission itself provides users a platform to understand the Taxonomy reporting obligations and support companies in their implementation. This platform, the so called “Taxonomy Navigator”, consists of three tools to help navigate through the taxonomy – Taxonomy Compass, Taxonomy Calculator, Taxonomy User Guide.44Commission, E. EU Taxonomy Navigator, <https://ec.europa.eu/sustainable-finance-taxonomy/> (n.d.).

The Taxonomy Compass provides a visual representation of the content of the taxonomy. The objective is to facilitate the conveyance of content in a more lucid and accessible manner to users. It thus provides an overview of the capabilities and conformity of the taxonomy.44Commission, E. EU Taxonomy Navigator, <https://ec.europa.eu/sustainable-finance-taxonomy/> (n.d.).

The European Commission (n.d.) states that the EU Taxonomy Calculator “is an interactive, educational tool that aims to help users understand and support with the reporting obligations laid down in the Disclosures Delegated Act under Article 8 of the Taxonomy Regulation” (n.p.). The Commission provides various examples to illustrate the steps a non-financial undertaking would have to go through to determine taxonomy suitability and alignment, as well as its KPIs for turnover, CapEx and OpEx (only for climate mitigation objective). The interactive tool visualizes nine different sectors including energy, construction and real estate activities, forestry and information and communication.44Commission, E. EU Taxonomy Navigator, <https://ec.europa.eu/sustainable-finance-taxonomy/> (n.d.).

Another useful tool, offered by the EU Commission, is the Taxonomy User Guide, as they (2023) call it “a practical reference, focusing on key implementation steps and specific illustrative ‘use cases’ to support organizations tackling expected challenges and potential benefits” (p. 6).45European Commission. A USER GUIDE TO NAVIGATE THE EU TAXONOMY FOR SUSTAINABLE ACTIVITIES. Report No. 978-92-76-40678-5, (Publications Office of the European Union, Luxembourg, 2023).

A four-phase plan is proposed to successfully implement the taxonomy. These phases consist of: Identify, Asses, Check, Apply. Each phase contains tips and questions that a company can ask itself in order to check whether it whether it meets the requirements or not.45European Commission. A USER GUIDE TO NAVIGATE THE EU TAXONOMY FOR SUSTAINABLE ACTIVITIES. Report No. 978-92-76-40678-5, (Publications Office of the European Union, Luxembourg, 2023).

Phase 1: Identify

The first step in phase 1 is to determine suitability or eligibility. To find out which economic activities are covered by the taxonomy, the Commission advises using the previously mentioned Taxonomy Compass. This includes all activities that are also covered by the Climate Delegated Act and the Complementary Climate Delegated Act.45European Commission. A USER GUIDE TO NAVIGATE THE EU TAXONOMY FOR SUSTAINABLE ACTIVITIES. Report No. 978-92-76-40678-5, (Publications Office of the European Union, Luxembourg, 2023).

Phase 2: Asses

The second step is to determine whether the company’s taxonomy-eligible activities also meet the actual criteria of the taxonomy. These criteria include compliance with both the Technical Screening Criteria and the DNSH requirements, as shown in Figure 1.45European Commission. A USER GUIDE TO NAVIGATE THE EU TAXONOMY FOR SUSTAINABLE ACTIVITIES. Report No. 978-92-76-40678-5, (Publications Office of the European Union, Luxembourg, 2023). Phase two is significantly supported by the Technical Annex, which is also published by the EU. This contains detailed information on whether an economic activity meets the requirements of the taxonomy or not. Furthermore, the Technical Annex includes threshold values for CO₂ emissions that are consistent with the objective of achieving climate neutrality by 2050.46Wendland, L., Zeranski, S. H. & Reuse, S. H. Nachhaltigkeit grüner Geldanlagen gemäß der EU Green Taxonomy – Kritische Bestandsaufnahme, Greenwashing und Analyse der Grenzen bei der Zertifizierung. (Springer Gabler, 2023). For instance, the production of cement must not exceed a threshold value of 0.498 tCO₂e/t, while the production of cement clinker must not exceed a threshold value of 0.766 tCO₂e/t in order to be considered taxonomy-compliant.25European Commission. Commission announces members of the Technical Expert Group on Sustainable Finance. (2018). Nevertheless, the aforementioned thresholds are not yet applicable to all relevant sectors.46Wendland, L., Zeranski, S. H. & Reuse, S. H. Nachhaltigkeit grüner Geldanlagen gemäß der EU Green Taxonomy – Kritische Bestandsaufnahme, Greenwashing und Analyse der Grenzen bei der Zertifizierung. (Springer Gabler, 2023).

Phase 3: Check

The third step is to ascertain whether the economic activities in question comply with the minimum safeguards set forth in Article.18European Commission. Capital Markets Union – Accelerating Reform. Report No. COM(2016) 601 final, (2016). This encompasses fundamental conventions on labor rights and rights and principles derived from the Human Rights Ordinance. This is further supported by the CSRD guidelines, which also take social aspects into account in their reporting.45European Commission. A USER GUIDE TO NAVIGATE THE EU TAXONOMY FOR SUSTAINABLE ACTIVITIES. Report No. 978-92-76-40678-5, (Publications Office of the European Union, Luxembourg, 2023).

Phase 4: Apply

In the fourth step, the pertinent reporting obligations are applied to the corresponding economic activities. The key performance indicators (KPIs) referenced in section 4.1 are calculated as part of the process. The abovementioned EU tools are made available to companies for their assistance.45European Commission. A USER GUIDE TO NAVIGATE THE EU TAXONOMY FOR SUSTAINABLE ACTIVITIES. Report No. 978-92-76-40678-5, (Publications Office of the European Union, Luxembourg, 2023).

In addition to the aforementioned tools, two Frequently Asked Questions (FAQs) Notices have been published by the EU Commission. Commission Notice C/2023/305 addresses the Disclosure Delegated Act of 6 July 2021 and contains 34 questions, while Commission Notice C/2023/267 contains 187 questions concerning the TSC for assessing the taxonomy conformity of the first two environmental objectives.47Amtsblatt der Europäischen Union. BEKANNTMACHUNG DER KOMMISSION C/2023/305. (2023).48Amtsblatt der Europäischen Union. BEKANNTMACHUNG DER KOMMISSION C/2023/267. (2023). Those are for example:

“What is meant by ‘state of the art climate projections’ mentioned in the substantial contribution criteria for adaptation to climate change?” – Question 175 from C/2023/26748Amtsblatt der Europäischen Union. BEKANNTMACHUNG DER KOMMISSION C/2023/267. (2023).

“Do advance payments count as taxonomy-compliant capital expenditure?” – Question 31 from C/2023/30547Amtsblatt der Europäischen Union. BEKANNTMACHUNG DER KOMMISSION C/2023/305. (2023).

The role of third parties: A survey conducted in 2022 identified the role of the Big Four (PwC, Deloitte, EY and KPMG) in the implementation of the EU taxonomy. The Big Four are the four largest auditing firms in the world. In addition to their core auditing activities, they have also assumed advisory and tax roles.49Statista Research Department. Umsatz der größten Wirtschaftsprüfungs- und Beratungsunternehmen weltweit (Big Four) im Geschäftsjahr 2023 nach Geschäftssegmenten, 2024). Husović and Kogstad identified four primary roles that can be attributed to the Big Four: advisory, interpretative, collaborative, and controlling. Consequently, the Big Four act as advisors for companies requiring assistance with the implementation of the taxonomy, providing clients with training courses that impart fundamental concepts and facilitate technical implementation services.50Husović, M. & Kogstad, P. The Implementation of the EU Taxonomy: the Big Fours’ perspective Master thesis, Lund University School of Economics and Management, (2022). One such technical implementation aid is PwC’s Taxonomy Calculator. The software is designed to assess the compliance of a bank portfolio with the relevant taxonomies.51PwC. Taxonomy Classification, <https://store.pwc.de/de/produkte/taxonomy-classification> (2024). The EY EU Taxonomy Barometer 2023, which provides information on corresponding reporting practices and their results, also serves to provide comprehensive information.50Husović, M. & Kogstad, P. The Implementation of the EU Taxonomy: the Big Fours’ perspective Master thesis, Lund University School of Economics and Management, (2022). Husović and Kogstad (2023) state that „the interviewees described that the legislative texts are unclear, poorly written and open for interpretation“(p. 33).50Husović, M. & Kogstad, P. The Implementation of the EU Taxonomy: the Big Fours’ perspective Master thesis, Lund University School of Economics and Management, (2022). This is why the Big Four also have an interpretative role. As a consequence of the lack of clarity in the formulations employed, the Big Four are actively engaged in the process of shaping the taxonomy. Despite their status as competitors, PwC, Deloitte, EY and KPMG collaborate closely and assume a collaborative role. Through regular audits, during which the taxonomy conformity of the clients’ economic activities is verified, the Big Four ultimately assume the role of controllers.50Husović, M. & Kogstad, P. The Implementation of the EU Taxonomy: the Big Fours’ perspective Master thesis, Lund University School of Economics and Management, (2022).

Best practice example: One of the biggest German energy supply companies, Energie Baden-Württemberg AG (EnBw), conducted a case study called “EU sustainable finance taxonomy case study – Application, experience and recommendations” and developed a step-by-step instruction in collaboration with Deloitte Touche Tohmatsu (aforementioned Big-Four-member) in 2021, which can be seen as an example of best practice in order to implement the taxonomy obligations. Their implementation plan consisted of four steps, which are analogous to the EU User Guide, but with certain discrepancies:52Dr. Rieth, L., Dr. Schmidt, M. & Warth, R. EU sustainable finance taxonomy case study: Application, experience, and recommendations. (2021).

Project setup: The purpose of this step is to achieve a common understanding of the taxonomy criteria and reporting requirements.52Dr. Rieth, L., Dr. Schmidt, M. & Warth, R. EU sustainable finance taxonomy case study: Application, experience, and recommendations. (2021). In this regard, the German Sustainable-Finance-Beirat recommends a comprehensive build-up of expertise through appropriate training and further education programmes.53Sustainable Finance-Beirat der Bundesregierung. (2023). Third parties such as the Big Four can support this with their advisory role in the form of training and technical implementation services.50Husović, M. & Kogstad, P. The Implementation of the EU Taxonomy: the Big Fours’ perspective Master thesis, Lund University School of Economics and Management, (2022). In the first step, a project management team will also be set up with members from different parts of the organization. Internal stakeholders should be involved, too.53Sustainable Finance-Beirat der Bundesregierung. (2023).

Analysis of business activities: In this step of the study, the German business activities were initially analyzed, pertinent information was gathered from the pre-prepared templates, and then interviews were conducted with the relevant departments within the company (e.g., environmental protection, occupational health and safety, procurement, project development). Subsequently, the considerable contribution to climate protection is aggregated (in this case, employing the overall generation method with a risk-oriented plausibility check). Furthermore, an assessment of “no significant harm” is conducted in phase two, wherein compliance with legal requirements is also evaluated on an aggregated basis. At EnBw at the Group level, minimum safeguards were analyzed. Subsequently, German activities were compared with activities in other EU countries to ascertain information on taxonomy compliance at foreign locations.52Dr. Rieth, L., Dr. Schmidt, M. & Warth, R. EU sustainable finance taxonomy case study: Application, experience, and recommendations. (2021).

Analyses of systems and processes: Following an initial examination of the potential scope of the EU taxonomy, all relevant data is now being collated and subjected to rigorous analysis. Ultimately, the results of the study were analyzed to derive revenue, capital expenditure (CapEx) and operating expenditure (OpEx) for the “environmentally sustainable” activities.52Dr. Rieth, L., Dr. Schmidt, M. & Warth, R. EU sustainable finance taxonomy case study: Application, experience, and recommendations. (2021).

Implementation and finalization: In step 4, all data is collated in reports that disclose both financial and non-financial key performance indicators (KPIs). These reports comply with legal requirements, such as the CSRD. As a result, stakeholders are able to evaluate the company based on the results.52Dr. Rieth, L., Dr. Schmidt, M. & Warth, R. EU sustainable finance taxonomy case study: Application, experience, and recommendations. (2021).

These four stages can be classified according to two distinct phases within the implementation project. The initial phaseof the process entails the evaluation of the environmental sustainability of the activities in question. Phase two, in contrast, addresses the transfer (and disclosure) of the sustainability assessment into key financial figures. In order to determine the greenhouse gas intensity of EnBw’s hydropower plants, a life cycle analysis was employed as an aid in phase one. This entailed calculating the emissions generated during the construction of the plant over the lifetime of the plant. This value was below the threshold value of 100g CO2e/kWh specified in the Technical Annex, which is permissible for energy generation by hydropower plants.27EU Technical Expert Group On Sustainable Finance. Taxonomy Report: Technical Annex. 593 (2020).54Zwick, Y. & Jeromin, K. Mit Sustainable Finance Die Transformation Dynamisieren. (Springer Gabler, 2023).

Recommendations for implementation:

Considering the potential challenges associated with the practical implementation of the EU taxonomy, it is imperative for companies to consider a number of critical attributes when determining the eligibility of their activities under this framework. Lykkesfeldt and Kjaergaard list the following recommendations:

To prevent the double counting and subsequent over-inflation of the taxonomy, it is essential to ensure that KPIs are clearly delineated from one another. The optimal methodology for achieving this is to apply the principle of best judgement, whereby reporters and analysts make decisions based on their most accurate assessment and professional judgement.

Furthermore, the company should incorporate economic activities that are both supportive and transitional. It is imperative that a comprehensive aggregation of the KPIs be conducted on a consistent basis, encompassing all subsidiaries and the parent company.55Lykkesfeldt, P. & Kjaergaard, L. L. Investor Relations and ESG Reporting in a Regulatory Perspective – A Practical Guide for Financial Market Participants. (Palgrave Macmillan, 2022).

In addition to that Lykkesfeldt and Kjaergaard (2022) state that companies “should integrate the taxonomy reporting process with general regulatory training and workshops” (p. 273)55Lykkesfeldt, P. & Kjaergaard, L. L. Investor Relations and ESG Reporting in a Regulatory Perspective – A Practical Guide for Financial Market Participants. (Palgrave Macmillan, 2022)., which is also recommended by the German Sustainable-Finance-Beirat and supported by the advisory role of the Big Four.50Husović, M. & Kogstad, P. The Implementation of the EU Taxonomy: the Big Fours’ perspective Master thesis, Lund University School of Economics and Management, (2022).53Sustainable Finance-Beirat der Bundesregierung. (2023).

Recommendations for the legislator:

In order to ensure the effective implementation of the EU taxonomy in practice and to address any potential issues that may arise, Altun and Pfaff put forward recommendations for consideration by legislators.56Pfaff, N., Altun, O. & Association, I. C. M. Ensuring the Usability of the EU Taxonomy. (International Capital Market Association, Zurich, 2022).

The first recommendation is an extension of the flexibility in the application of DNSH measures and minimum protection measures. This aims to fulfil the aforementioned criteria in a more pragmatic manner, without the necessity for more complex assessments, which would otherwise prevent companies from implementing them. It is crucial to consider the principle of proportionality, which would entail adapting the requirements in accordance with the size of the company in question. It is crucial to consider the principle of proportionality, which would entail adapting the requirements in accordance with the size of the company in question. Furthermore, the proposal suggests replacing the requisite criteria with company-specific analyses and ESG risk management processes, which would facilitate implementation for businesses. Another proposal is to adapt the TSC to non-EU countries in order to address the global consequences of climate change. It is crucial to consider regional differences (as outlined in the Paris Agreement) and to establish country-specific thresholds. Adapting the criteria in this way would make the EU taxonomy accessible to other countries.56Pfaff, N., Altun, O. & Association, I. C. M. Ensuring the Usability of the EU Taxonomy. (International Capital Market Association, Zurich, 2022). The study conducted by EnBw and Deloitte also made recommendations for legislation to take account of regional differences. According to the study, the limit of 100 g CO2e/kWh set in the Technical Annex for electricity generation in gas-fired power plants is too strict and would not be in line with the taxonomy. However, the authors argue that gas-fired power plants are an important factor in the transition from coal-fired power plants to renewables in some European countries. They are needed to ensure a steady supply of energy. For this reason, the authors of the study recommend, among other things, a redefinition of the limit value that still promotes decarbonization.52Dr. Rieth, L., Dr. Schmidt, M. & Warth, R. EU sustainable finance taxonomy case study: Application, experience, and recommendations. (2021).

Due to a lack of data availability, the German Sustainable-Finance-Beirat adds recommendations aimed at legislators. These include the

- Regulation of data providers to ensure minimum standards and correct comparative values,

- stablishment of the European Single Access Point (ESAP) to create an EU-wide access point for publicly available company and financial information,

- as well as the establishment of a public Life-Cycle-Assessment-Databases based on a product category level.53Sustainable Finance-Beirat der Bundesregierung. (2023).

Some of those recommendations are the results of the barriers for sustainability that are discussed in more detail in “Drivers & barriers”.

5 Drivers & barriers

5.1 Drivers

In order to assess the impact of the EU taxonomy on sustainable finance, it is important to examine the key drivers that led to its creation. These drivers illustrate the rationale behind the creation of the taxonomy and how it aims to align with the European Union’s sustainability goals. The taxonomy aims to increase investment certainty, provide a structured approach to sustainable finance, and improve market transparency and integrity. However, its effectiveness and the extent to which it achieves these goals remain the subject of ongoing debate and scrutiny.

Alignment with policy goals and national climate targets: The EU taxonomy is essential for aligning financial investments with the European Union’s sustainability goals, such as those set out in the European Green Deal and the Paris Agreement.7Tettamanzi, P. T., Riccardo Gotti. Murgolo, Michael. The European Union (EU) green taxonomy: codifying sustainability to provide certainty to the markets. 26 (2023). By providing a clear framework, it ensures that investments are aligned with EU and national climate goals and directs capital to projects that support long-term environmental objectives.4OECD. Developing Sustainable Finance Definitions and Taxonomies. Report No. 978-92-64-97779-2, (2020). This alignment harmonizes sustainability standards across Europe, making it easier for financial institutions to invest in truly sustainable activities.2Ostojic, S., Simone, L., Edler, M. & Traverso. How Practically Applicable Are the EU Taxonomy Criteria for Corporates?—An Analysis for the Electrical Industry. 24 (2024). https://doi.org/https://doi.org/10.3390/su16041575 In addition, the taxonomy’s alignment with national climate policies strengthens the integration of sustainability into financial systems.4OECD. Developing Sustainable Finance Definitions and Taxonomies. Report No. 978-92-64-97779-2, (2020). This approach ensures that all stakeholders, including governments and investors, are working towards the same goals, thereby enhancing the credibility and effectiveness of climate action across the EU. This alignment is further supported by its role in reducing greenwashing, as highlighted in other sources, by providing transparent criteria that increase investor confidence in sustainable finance.2Ostojic, S., Simone, L., Edler, M. & Traverso. How Practically Applicable Are the EU Taxonomy Criteria for Corporates?—An Analysis for the Electrical Industry. 24 (2024). https://doi.org/https://doi.org/10.3390/su16041575

Harmonization of sustainability standards and a systemic approach to sustainability: The EU taxonomy plays a critical role in harmonizing sustainability standards across member states, making it easier for companies and investors to meet and contribute to the EU’s climate change goals.2Ostojic, S., Simone, L., Edler, M. & Traverso. How Practically Applicable Are the EU Taxonomy Criteria for Corporates?—An Analysis for the Electrical Industry. 24 (2024). https://doi.org/https://doi.org/10.3390/su16041575 By providing a standardized framework, it ensures that economic activities are evaluated consistently across different regions, promoting a more integrated approach to sustainability.

In addition, the taxonomy takes a systemic approach to sustainability by recognizing that economic activities cannot be considered sustainable in isolation. It emphasizes the interdependencies between different environmental goals and ensures that activities that contribute to one goal do not harm others.4OECD. Developing Sustainable Finance Definitions and Taxonomies. Report No. 978-92-64-97779-2, (2020). This holistic approach is essential to achieving long-term sustainability because it promotes a comprehensive assessment of the environmental impacts of economic activities.