Authors: Natalie Jansen, Celina Stremkus, Tatjana Wiechers

Edited by: Philine Jörgensen, Lisann Kühling, Katharina Ros

Last updated: April 8, 2026

Executive summary

Materiality analysis is a core principle in sustainability reporting, helping organizations identify and prioritize ESG topics that significantly impact stakeholders and financial performance. The concept includes impact materiality (inside-out perspective) and financial materiality (outside-in perspective), combined under double materiality as required by the EU’s CSRD and ESRS standards. Conducting a materiality analysis ensures compliance with regulations, improves transparency, and strengthens stakeholder relationships. It also supports strategic decision-making by highlighting risks, opportunities, and sustainability goals. The process typically involves defining scope, engaging stakeholders, identifying potential topics, assessing impacts and financial implications, and consolidating results. Various frameworks such as GRI, ESRS, SASB, and ISO 26000 provide guidance, though methodologies differ. Drivers include regulatory compliance, risk management, and enhanced corporate reputation, while barriers involve complexity, resource constraints, and subjectivity. Overcoming these challenges requires clear governance, stakeholder engagement, and integration of sustainability into corporate strategy.

1 Definition and relevance

1.1 Materiality

According to Oll et al. (2024) the concept of materiality can be described as “a key principle of corporate reporting” (p.2).1Oll, J., Spandel, T., Schiemann, F. & Akkermann, J. The concept of materiality in sustainability reporting: From essential contestation to research opportunities. (2024). Nevertheless, its meaning is not rigidly defined and allows for varying interpretations, which is reflected in diverse definitions by different standards (see section 3.1). The goal of materiality is to differentiate between “material sustainability issues [that are] likely to influence the decision making of stakeholders […] and those issues that are non-material [which are] not likely to influence decision making” (Jorgensen et al. 2021, p. 343).2Jørgensen, S., Mjøs, A. & Pedersen, L. J. T. Sustainability reporting and approaches to materiality: Tensions and potential resolutions. Sustainability Accounting, Management and Policy Journal 13, 341-361 (2022). Another problem is that different stakeholders consider different information to be material depending on their background.3Global Reporting Initative. The materiality madness: why definitions matter. (2022).

For instance, the Global Reporting Initiative (GRI) Universal Standards 2021 approach materiality by focusing on the impacts of an organization’s on the economy, environment, and society.4Global Reporting Initiative. GRI Universal Standards 2021: Frequently Asked Questions (FAQs). (2022). According to this view, “material topics” are those where the organization’s business activities have the greatest impact on these areas.4Global Reporting Initiative. GRI Universal Standards 2021: Frequently Asked Questions (FAQs). (2022). The focus is therefore on corporate activities and analyses their impact on the environment and society, which is why impact materiality is also referred to as inside-out impact.5Shami, A. in 7 th French Conference On Social And Environmental Accounting Research (Montpellier, France, 2023). From this example, it can be concluded that impact materiality is particularly relevant in sustainability reporting, where issues are material where companies cause positive or negative externalities.

For this definition the term of impact materiality or single materiality is most widespread.6Baumüller, J. & Sopp, K. Double materiality and the shift from non-financial to European sustainability reporting: review, outlook and implications. Journal of Applied Accounting Research 23, 8-28 (2021). https://doi.org/https://doi.org/10.1108/JAAR-04-2021-0114 In the following it is referred to as impact materiality.

1.2 Double materiality

According to the double materiality approach, companies ought to combine impact materiality with financial materiality and report on topics that affect the financial value of the company as well as those that have an environmental, social or governance (ESG) impact.3Global Reporting Initative. The materiality madness: why definitions matter. (2022). From the financial point of view, information is material if its omission, concealment or misstatement could influence investors’ decisions.7IFRS. ISSB: Frequently Asked Questions, <https://www.ifrs.org/groups/international-sustainability-standards-board/issb-frequently-asked-questions/> (n.D.). Financial materiality is also known as outside-in impact, which considers the impact of an environmental event on the financial status or value of a company.5Shami, A. in 7 th French Conference On Social And Environmental Accounting Research (Montpellier, France, 2023).

Double materiality emerged with the Corporate Sustainability Reporting Directive (CSRD) coming to force in 2023 and requiring the implementation of reporting according to the European Sustainability Reporting Standards (ESRS)8 (insert link to the wiki for CSRD/ESRS).8DFGE Institute for Energy, E. a. E. TOP 5: Was Sie über CSRD wissen müssen. (2023). The importance for double materiality emerged from two assumptions: Firstly, the impacts of corporate activities are of central importance to various stakeholders and reporting is therefore necessary.3Global Reporting Initative. The materiality madness: why definitions matter. (2022). Secondly, every impact of business activities will always become financially relevant for a company over time.3Global Reporting Initative. The materiality madness: why definitions matter. (2022).

1.3 Materiality analysis

To this point, it has been shown that some companies are required to report on their particularly relevant topics due to CSRD (see chapter 1.2). A materiality analysis can be carried out, in order to identify these particularly relevant topics and to prioritize them.9Delebecque, A. A materiality analysis meeting non financial reporting requirements: With the combination of analytic hierarchy process and failure mode and effects analysis. (2019). A detailed description of the individual steps of a materiality analysis process can be found in chapter 3.

1.4 Relevance of materiality analysis

There are various reasons why conducting a materiality analysis is beneficial for companies:

On the one hand, there are regulatory requirements that mandate such analyses.

Companies exceeding specific thresholds in terms of size under accounting law, turnover and/or number of employees are obligated under the CSRD to report on their sustainability efforts.10Bundesministerium für Arbeit und Soziales (BMAS). Corporate Sustainability Reporting Directive (CSRD): Die neue EU-Richtlinie zur Unternehmens-Nachhaltigkeitsberichterstattung im Überblick, <https://www.csr-in-deutschland.de/DE/CSR-Allgemein/CSR-Politik/CSR-in-der-EU/Corporate-Sustainability-Reporting-Directive/corporate-sustainability-reporting-directive-art.html> (n.D.). As of 2024, these reports must be grounded in the principle of double materiality.10Bundesministerium für Arbeit und Soziales (BMAS). Corporate Sustainability Reporting Directive (CSRD): Die neue EU-Richtlinie zur Unternehmens-Nachhaltigkeitsberichterstattung im Überblick, <https://www.csr-in-deutschland.de/DE/CSR-Allgemein/CSR-Politik/CSR-in-der-EU/Corporate-Sustainability-Reporting-Directive/corporate-sustainability-reporting-directive-art.html> (n.D.).

On the other hand, companies that operate below these thresholds may also be required to conduct a materiality analysis under specific circumstances: For instance, this obligation may arise if they are part of the supply chain of a larger company that is mandated to conduct sustainability reporting, or if they receive financing from banks that are similarly obligated to report on sustainability.11Habermann, M. & Schmidt, K. in Unternehmerische Wertschöpfung neu aufstellen_ Volatile, disruptive, digitale Welt – Anforderungen an das Management der Zukunft (ed Marc Knoppe) (Springer Gabler, 2024).

Beyond legal obligations, there are also advantages with direct benefits for the company’s sustainability management. The materiality analysis shows how deeply and to what extent an organization needs to deal with certain topics.12Mervelskemper, L., Orbach, S., Jukas, A. & Köpper, J. in Mit Sustainable Finance die Transformation dynamisieren: Wie Finanzwirtschaft nachhaltiges wirtschaften ermöglicht (ed Yvonne; Jeromin Zwick, Kristina ) (SpringerGabler, 2023). Its results show the company which priorities should be set not only in management and strategy but also in the reporting and thus helps to move from a general presentation to targeted and relevant reporting.12Mervelskemper, L., Orbach, S., Jukas, A. & Köpper, J. in Mit Sustainable Finance die Transformation dynamisieren: Wie Finanzwirtschaft nachhaltiges wirtschaften ermöglicht (ed Yvonne; Jeromin Zwick, Kristina ) (SpringerGabler, 2023). The analysis enables companies to strengthen their responsibility towards various stakeholders and to improve sustainability efforts in a targeted manner.13Calabrese, A., Costa, R., Levialdi Ghiron, N. & Menchini, T. Materiality analysis in sustainability reporting: a tool for directing corporate sustainability towards emerging economic, environmental and social opportunities. Technological and Economic Development of Economy 25, 1016-1038 (2019). https://doi.org/https://doi.org/10.3846/tede.2019.10550 It addresses challenges such as evaluation subjectivity, complexity and uncertainty about sustainability issues and serves to ensure well-founded and relevant reporting.13Calabrese, A., Costa, R., Levialdi Ghiron, N. & Menchini, T. Materiality analysis in sustainability reporting: a tool for directing corporate sustainability towards emerging economic, environmental and social opportunities. Technological and Economic Development of Economy 25, 1016-1038 (2019). https://doi.org/https://doi.org/10.3846/tede.2019.10550 Materiality assessments are therefore crucial for sustainability reporting and strategy, because companies can identify not only their material topics but also what measures and targets to set, that have the most impact.2Jørgensen, S., Mjøs, A. & Pedersen, L. J. T. Sustainability reporting and approaches to materiality: Tensions and potential resolutions. Sustainability Accounting, Management and Policy Journal 13, 341-361 (2022).

Publishing an informative sustainability report provides significant advantages for companies, especially in relation to their diverse stakeholders: Firstly, there are customers who are increasingly aligning their purchasing decisions with ecological, economic, and social considerations.11Habermann, M. & Schmidt, K. in Unternehmerische Wertschöpfung neu aufstellen_ Volatile, disruptive, digitale Welt – Anforderungen an das Management der Zukunft (ed Marc Knoppe) (Springer Gabler, 2024). In a 2021 survey conducted in Germany, 58 % of respondents indicated that sustainability is an important or even a very important purchasing criterion for them.14Statista. Relevanz von Nachhaltigkeit als Kaufkriterium in Deutschland im Jahr 2021, <https://de.statista.com/statistik/daten/studie/1285879/umfrage/nachhaltigkeit-als-kaufkriterium/> (2024). Secondly, investors are increasingly prioritizing sustainable investments.11Habermann, M. & Schmidt, K. in Unternehmerische Wertschöpfung neu aufstellen_ Volatile, disruptive, digitale Welt – Anforderungen an das Management der Zukunft (ed Marc Knoppe) (Springer Gabler, 2024). As a result, a company’s commitment to sustainability has become a critical factor in securing future financial success for those reliant on investor support.11Habermann, M. & Schmidt, K. in Unternehmerische Wertschöpfung neu aufstellen_ Volatile, disruptive, digitale Welt – Anforderungen an das Management der Zukunft (ed Marc Knoppe) (Springer Gabler, 2024). Finally, employees play a critical role. In times of skilled labor shortages and the competitive market for talent, transparent and sustainable practices are essential for attracting and retaining the right personnel.11Habermann, M. & Schmidt, K. in Unternehmerische Wertschöpfung neu aufstellen_ Volatile, disruptive, digitale Welt – Anforderungen an das Management der Zukunft (ed Marc Knoppe) (Springer Gabler, 2024).

2 Background

The origin of the materiality principle lies in financial reporting.1Oll, J., Spandel, T., Schiemann, F. & Akkermann, J. The concept of materiality in sustainability reporting: From essential contestation to research opportunities. (2024). Here, materiality is regarded as a threshold for economic decisions made by investors or other individuals who use the company’s budget.15Calabrese, A., Costa, R., Levialdi Ghiron, N. & Menchini, T. Materiality Analysis in Sustainability Reporting: A Method for Making it Work in Practice. European Journal of Sustainable Development 6, 439-447 (2017). https://doi.org/10.14207/ejsd.2017.v6n3p439 The target group for the financial reporting is therefore mainly investors and other stakeholder groups with financial interests.6Baumüller, J. & Sopp, K. Double materiality and the shift from non-financial to European sustainability reporting: review, outlook and implications. Journal of Applied Accounting Research 23, 8-28 (2021). https://doi.org/https://doi.org/10.1108/JAAR-04-2021-0114

Financial materiality assesses sustainability issues in terms of their impact on the company’s financial position.15Calabrese, A., Costa, R., Levialdi Ghiron, N. & Menchini, T. Materiality Analysis in Sustainability Reporting: A Method for Making it Work in Practice. European Journal of Sustainable Development 6, 439-447 (2017). https://doi.org/10.14207/ejsd.2017.v6n3p439 Opportunities and risks with financial impact can develop for a company, for example as a result of regulations, climate change and other effects or dependencies.16EFRAG. EFRAG IG 1 – Materiality Assesment. (2024). In the financial context, the definition of a topic or a field of action as material is often based on specific benchmarks, such as percentage of net income.17Mio, C. & Fasan, M. Materiality from financial towards non-financial reporting. (2013). For instance, a common threshold might be 10% of net income, meaning that any matter affecting at least 10% of net income would be considered material and taken into account in the audit.17Mio, C. & Fasan, M. Materiality from financial towards non-financial reporting. (2013). The International Sustainability Standards Board (ISSB) standards of the International Financial Reporting Standards (IFRS) Foundation, for example, focus on a financial point of view to materiality, spotlighting the information requirements of investors.7IFRS. ISSB: Frequently Asked Questions, <https://www.ifrs.org/groups/international-sustainability-standards-board/issb-frequently-asked-questions/> (n.D.).

One example of the impact on the company’s financial situation is the price of CO.18218 Production costs can increase due to rising CO2 prices, which in turn can affect the financial situation.19Kirchhoff, K., Niefünd, S. & von Pressentin, J. ESG: Nachhaltigkeit als strategischer Erfolgsfaktor. (2024). Furthermore, the financial situation of the company can also be influenced indirectly.19Kirchhoff, K., Niefünd, S. & von Pressentin, J. ESG: Nachhaltigkeit als strategischer Erfolgsfaktor. (2024). More and more investors are showing increased interest in a company’s strong sustainability performance.19Kirchhoff, K., Niefünd, S. & von Pressentin, J. ESG: Nachhaltigkeit als strategischer Erfolgsfaktor. (2024). However, if the company places less emphasis on sustainability activities, investors are more likely to choose other companies, which in turn means that the company has higher costs.19Kirchhoff, K., Niefünd, S. & von Pressentin, J. ESG: Nachhaltigkeit als strategischer Erfolgsfaktor. (2024).

In recent decades, stakeholders have become increasingly interested in the environmental and social impact of companies, which has put pressure on companies to report on these issues.20Zhou, Y. Materiality Approach in Sustainability Reporting: Applications, Dilemmas, and Challenges. (2011). In 2003, the Modernisation Directive (2003/51/EC) officially required reporting on non-financial matters for the first time, which included “information relating to environmental and employee matters” (The European Parliament and the Council of the European Union 2003, p.3).6Baumüller, J. & Sopp, K. Double materiality and the shift from non-financial to European sustainability reporting: review, outlook and implications. Journal of Applied Accounting Research 23, 8-28 (2021). https://doi.org/https://doi.org/10.1108/JAAR-04-2021-0114,21Union, T. E. P. a. t. C. o. t. E. Directive 2003/51/EC of the European Parliament and of the Council. (2003).

These new sustainability reports, mostly prepared and published on a voluntary basis, focus on the impact a company has on the economy, the environment and society.22Beske, F., Haustein, E. & Lorson, P. Materiality analysis in sustainability and integrated reports. Sustainability Accounting, Management and Policy Journal 11, 162-186 (2020). https://doi.org/https://doi.org/10.1108/SAMPJ-122018-0343 As a result, the scope of reporting expanded, and the target group no longer consisted solely of owners of the company’s capital, but has extended to a broad spectrum of diverse interest groups within a company.20Zhou, Y. Materiality Approach in Sustainability Reporting: Applications, Dilemmas, and Challenges. (2011). However, due to a lack of regulations and susceptibility to manipulation, the quality of these sustainability reports has often been declared inadequate.22Beske, F., Haustein, E. & Lorson, P. Materiality analysis in sustainability and integrated reports. Sustainability Accounting, Management and Policy Journal 11, 162-186 (2020). https://doi.org/https://doi.org/10.1108/SAMPJ-122018-0343 To counteract this, various guidelines, reporting standards etc. have been developed recently. The main steps towards the still relatively new principle of double materiality are summarised in the following.

The Integrated Reporting Council (IIRC), founded in 2010, was the first council to officially address the question of how companies can include not only financial but also other important aspects in their reporting.12Mervelskemper, L., Orbach, S., Jukas, A. & Köpper, J. in Mit Sustainable Finance die Transformation dynamisieren: Wie Finanzwirtschaft nachhaltiges wirtschaften ermöglicht (ed Yvonne; Jeromin Zwick, Kristina ) (SpringerGabler, 2023). The aim was to show how financial and non-financial factors are interrelated and influence each other.12Mervelskemper, L., Orbach, S., Jukas, A. & Köpper, J. in Mit Sustainable Finance die Transformation dynamisieren: Wie Finanzwirtschaft nachhaltiges wirtschaften ermöglicht (ed Yvonne; Jeromin Zwick, Kristina ) (SpringerGabler, 2023). Having previously taken rather small steps towards sustainability reporting, the year 2015 was marked by two major events that brought a significant shift in the EU Commission’s policies, on which future EU policies were based on: The launch of the 17 Sustainable Development Goals (SDGs) and the Paris Climate Agreement, signed in December.6Baumüller, J. & Sopp, K. Double materiality and the shift from non-financial to European sustainability reporting: review, outlook and implications. Journal of Applied Accounting Research 23, 8-28 (2021). https://doi.org/https://doi.org/10.1108/JAAR-04-2021-0114 Two years later, in 2017, the CSRD Implementation Act was introduced, according to which reporting on non-financial information is now a legal requirement for all companies that are required to report under the CSRD.12Mervelskemper, L., Orbach, S., Jukas, A. & Köpper, J. in Mit Sustainable Finance die Transformation dynamisieren: Wie Finanzwirtschaft nachhaltiges wirtschaften ermöglicht (ed Yvonne; Jeromin Zwick, Kristina ) (SpringerGabler, 2023). However, the EU Commission quickly raised the question of the scope and extent to which this information should now be reported, from which the principle of materiality arised.6Baumüller, J. & Sopp, K. Double materiality and the shift from non-financial to European sustainability reporting: review, outlook and implications. Journal of Applied Accounting Research 23, 8-28 (2021). https://doi.org/https://doi.org/10.1108/JAAR-04-2021-0114

The term of materiality already appeared in earlier generations of the GRI’s Sustainability Reporting Guidelines, however, its relevance and the advantage of identifying material topics were first clearly emphasised with the publication of the fourth generation of the guidelines in 2013.23KPMG. GRI’s G4 Guidelines: the impact on reporting. (2013). These state that instead of reporting on all possible topics, companies should focus only on the material topics and report comprehensively on their impact.23KPMG. GRI’s G4 Guidelines: the impact on reporting. (2013). The process for identifying these topics must involve stakeholder groups and be disclosed transparently.23KPMG. GRI’s G4 Guidelines: the impact on reporting. (2013).

In 2019, the European Commission cited the principle of double materiality, i.e. the determination of material topics from two different viewpoints, as a new benchmark for reporting for the first time.24Adams, C. A. et al. The double-materiality concept: Application and issues. (2021). Finally, the introduction of the CSRD in particular has made double materiality more relevant, as this is the first time that impact and financial materiality have been officially combined in a global standard.6Baumüller, J. & Sopp, K. Double materiality and the shift from non-financial to European sustainability reporting: review, outlook and implications. Journal of Applied Accounting Research 23, 8-28 (2021). https://doi.org/https://doi.org/10.1108/JAAR-04-2021-0114

Identifying material information based on the principle of double materiality offers several advantages: Firstly, double materiality allows for a more accurate and transparent assessment of the impacts of business activities.5Shami, A. in 7 th French Conference On Social And Environmental Accounting Research (Montpellier, France, 2023). This, in turn, provides a robust foundation for consistent reporting and supports the disclosure of sustainability issues.5Shami, A. in 7 th French Conference On Social And Environmental Accounting Research (Montpellier, France, 2023). Additionally, incorporating ESG factors into investment decisions can significantly influence both financial performance and sustainable development.5Shami, A. in 7 th French Conference On Social And Environmental Accounting Research (Montpellier, France, 2023).

3 Practical implementation

3.1 Overview materiality analysis in different standards

Internationally there are many different standards and frameworks for sustainability reporting, that also have requirements on how to find the material topics a company or organization should report on in their sustainability report. This chapter will give a short overview of some of the standards and frameworks and how they view materiality.

Table 1: The meaning and characteristics of materiality in different standards

| Definition of materiality according to different standards | Goal and/or process of materiality analysis | Pros and cons |

| ESRS | ||

| A matter is stated as material from:“an impact perspective when it pertains to the undertaking’s material actual or potential, positive or negative impacts on people or the environment over the short-, medium- and long-term. […]“ (EFRAG 2022, p.11)25EFRAG. ESRS 1 General Requirements. Draft European Sustainability Reporting Standards (2022)., or “a financial perspective if it triggers or could reasonably be expected to trigger material financial effects on the undertaking. This is the case when a sustainability matter generates risks or opportunities that have a material influence or that could reasonably be expected to have a material influence […]” (EFRAG 2022, p. 12).25EFRAG. ESRS 1 General Requirements. Draft European Sustainability Reporting Standards (2022). | Identify the material impacts, risks and opportunities (IROs) of a company and therefore determine what topical standards have to be reported.25EFRAG. ESRS 1 General Requirements. Draft European Sustainability Reporting Standards (2022). The process will be further elaborated in chapter 3. | Pro: Double approach: selection of material topics based on impact materiality and financial materiality.26Schütte-Biastoch, S. & Zieger, M. in Bank-und Finanzwirtschaft im Stress: Aktuelle Herausforderungen und Lösungsansätze (ed S.; Moch Schöning, N.; Schütte-Biastoch, S. ) 89-124 (Springer, 2023). Con: More topics are likely to be material for companies, which will increase reporting requirements.26Schütte-Biastoch, S. & Zieger, M. in Bank-und Finanzwirtschaft im Stress: Aktuelle Herausforderungen und Lösungsansätze (ed S.; Moch Schöning, N.; Schütte-Biastoch, S. ) 89-124 (Springer, 2023). |

| GRI | ||

| “Material topics are topics that represent an organization’s most significant impacts on the economy, environment, and people, including impacts on their human rights.” (GRI 2023, p.112).27Global Reporting Initiative. Consolidated Set of the GRI Standards. (2023). | The goal is identifying most significant impacts for each reporting period and also determine the topic standards used in the report (at least one topic standard for every material topic).27Global Reporting Initiative. Consolidated Set of the GRI Standards. (2023). The process will be further elaborated in chapter 3. | Pro: Specifications about conducting the analysis are only recommendation,27Global Reporting Initiative. Consolidated Set of the GRI Standards. (2023). therefore companies are free to adapt their analysis. Con: GRI materiality analysis focuses only on impact materiality perspective.26Schütte-Biastoch, S. & Zieger, M. in Bank-und Finanzwirtschaft im Stress: Aktuelle Herausforderungen und Lösungsansätze (ed S.; Moch Schöning, N.; Schütte-Biastoch, S. ) 89-124 (Springer, 2023). |

| Sustainability Accounting Standards Board (SASB) | ||

| “For the purpose of SASB’s standard-setting process, information is financially material if omitting, misstating, or obscuring it could reasonably be expected to influence investment or lending decisions that users make on the basis of their assessments of short-, medium-, and long-term financial performance and enterprise value.” (SASB 2020, p.7)28Corcoran, P. PROPOSED CHANGES TO THE SASB CONCEPTUAL FRAMEWORK & RULES OF PROCEDURE BASES FOR CONCLUSIONS & INVITATION TO. (2020).,29Sustainability Accounting Standards Board. Proposed changes to the SASB conceptual framework & rules of procedure bases for conclusions & invitation to comment on exposure drafts. (2020). | To identify material issues, SASB provides a materiality map that comprises material sustainability issues within various industries.30Schwoy, S. & Dutzi, A. Materiality analysis as the basis for sustainability strategies and reporting-A systematic review of approaches and recommendations for practice. Handbook of Sustainability-Driven Business Strategies in Practice, 35-58 (2021). Therefore, determination of material topics is based on the industry type. | Pro: Companies can use the materiality map to quickly recognise which sustainability issues are the most material in the respective sector or industry.31Mayer, K. Nachhaltigkeit: 125 Fragen und Antworten: Wegweiser für die Wirtschaft der Zukunft. (2020). Therefore, this might require comparatively little effort. Con: The focus is only on financial materiality.28Corcoran, P. PROPOSED CHANGES TO THE SASB CONCEPTUAL FRAMEWORK & RULES OF PROCEDURE BASES FOR CONCLUSIONS & INVITATION TO. (2020).,29Sustainability Accounting Standards Board. Proposed changes to the SASB conceptual framework & rules of procedure bases for conclusions & invitation to comment on exposure drafts. (2020). |

| Integrated Reporting | ||

| “An integrated report should disclose information about matters that substantively affect the organization’s ability to create value over the short, medium and long term.”(Integrated Reporting 2021, p. 29).32Reporting, I. International | In order to prepare a materiality analysis within an integrated report, four steps must be performed:311. Filter out topics that influence the company’s value creation.32Reporting, I. International | Pro: Financial and non-financial perspectives are part of integrated reporting. Positive and negative developments are also highlighted.33Kirchhoff, K. R. Integrierte Berichterstattung–die wertschaffende Reporting-Alternative. Integrated Reporting für die Praxis: Wertschaffend berichten, 1-12 (2019). |

| UN Global Compact | ||

| The UN Global Compact supports the European Commission in the principle of double materiality (see definition ESRS), but only asks about impact materiality its questionaire.34Compact, U. N. G. Frequently Asked Questions: Communication on Progress. (2022). | The UN Global Compact does not expect its member companies to conduct a materiality analysis.34Compact, U. N. G. Frequently Asked Questions: Communication on Progress. (2022). The Conformity of Production has defined ten principles; these topics are set to be material for all companies.34Compact, U. N. G. Frequently Asked Questions: Communication on Progress. (2022). For example, in the area of human rights, companies can select the sub-topics that are material to them individually.34Compact, U. N. G. Frequently Asked Questions: Communication on Progress. (2022). | Due to the fact that companies are not required to carry out a materiality analysis as part of the UN Global Compact, no list of advantages and disadvantages is provided here. |

| ISO 26000 | ||

| ISO 26000 emphasises that organisations cannot tackle all areas of activity at the same time. The fields of action must be evaluated and prioritized in terms of their materiality – in particular, the impact of company activities on stakeholders is considered (impact materiality).35Bundesministerium für Arbeit und Soziales. Die DIN ISO 26000: „Leitfaden zur gesellschaftlichen Verantwortung von Organisationen“ – Ein Überblick. (2011). | The aim of the materiality analysis is to break down all possible topics/fields of action into those that are really relevant for stakeholder groups.35Bundesministerium für Arbeit und Soziales. Die DIN ISO 26000: „Leitfaden zur gesellschaftlichen Verantwortung von Organisationen“ – Ein Überblick. (2011). With defining stakeholders, the standard clarifies that only stakeholder interests that are directly related to the organisation’s core social responsibility issues are relevant.35Bundesministerium für Arbeit und Soziales. Die DIN ISO 26000: „Leitfaden zur gesellschaftlichen Verantwortung von Organisationen“ – Ein Überblick. (2011). | Pro: The guidelines are compatible with other international frameworks and standards such as GRI.36VOREST AG. Was ist die ISO 26000?, |

| AA1000 Materiality Process | ||

| Materiality refers to the identifying and prioritising of the most important sustainability issues.37AccountAbility. AA1000: Die Prinzipien von Accountability. (2018). According to the AA1000 standards, material topics are those that have an impact on the decisions and actions of an organisation or its stakeholders (impact materiality) in the short, medium and/or long term.37AccountAbility. AA1000: Die Prinzipien von Accountability. (2018).,38Dayankac, A. AA1000 – Verifizierung von Nachhaltigkeitsberichten, | Materiality is one of the four principles on which the standard and the audit process are based and therefore plays a central role. The aim of the materiality analysis is to generate information on non-financial aspects that form the basis for further analyses.38Dayankac, A. AA1000 – Verifizierung von Nachhaltigkeitsberichten, | Pro: In addition to the actual effects, the materiality analysis also determines the possible and probable effects.37AccountAbility. AA1000: Die Prinzipien von Accountability. (2018). Con: The literature assigns the AA1000 standards a clear focus on impact materiality, from which it can be concluded that financial materiality is given little or no consideration in the standards. |

| Carbon Disclosure Project (CDP) | ||

| Materiality “regards relevant information that is (capable of) making a difference to the decisions made by users of the information.”(CDP, 2019)39CDP. Financial and non-financial reporting frameworks share common founding principles of transparency and accountability, | Building the materiality analysis on the CDP reporting framework, organisations can effectively evaluate environmental aspects such as their carbon footprint, water usage, or other environmental factors.40SWEEP. Materiality Assessments – what they are and how to conduct them, The materiality analysis aims to enable companies to prioritise areas of action and to provide transparency to their stakeholders.40SWEEP. Materiality Assessments – what they are and how to conduct them, | Con: CDP concentrates mainly on climate and environmental issues – for example, the website emphasises the four focus areas Climate, Water, Forests and Plastics.39CDP. Financial and non-financial reporting frameworks share common founding principles of transparency and accountability, |

3.2 A recipe – How to conduct a materiality analysis, including best practice examples

The next chapter will give a more detailed overview of the methods to conduct a materiality analysis according to two of the standards above. For the detailed discussion GRI and ESRS were chosen because GRI is one of the most commonly used frameworks and ESRS will be in the next years since it is obligated for specific companies in the EU.43Pizzi, S., Principale, S. & De Nuccio, E. Material sustainability information and reporting standards. Exploring the differences between GRI and SASB. Meditari Accountancy Research 31, 1654-1674 (2023).,44Bundesanstalt für Finanzdienstleistungsaufsicht. Nachhaltigkeitsberichterstattung – CSRD, <https://www.bafin.de/DE/Aufsicht/SF/CSRD/CSRD_node.html> (2023).

Since there is no universally accepted or standardised methodology to define material topics for companies, this chapter aims to generalize steps depicted in Figure 1 for a materiality analysis.45KPMG. Sustainable Insight The essentials of materiality assessment (2014). These could be used when reporting for GRI or ESRS and simultaneously point out the differences between the two standards. In addition to that, after each section, and only as far as possible, there will be a best-practice example to further understand how each step can be adapted in practice.

With regard to ESRS, it must be noted that there are still few examples of best practice due to the novelty of the standard. Furthermore, as the ESRS must be audited externally due to EU regulations and the lack of a guideline for external auditing in the various countries, this chapter can only serve as a guideline for carrying out the materiality analysis in accordance with ESRS but not guarantee external insurance.

Before explaining the steps it also has to be noted that both the ESRS an GRI require to perform a materiality analysis but the steps are only a suggestion and not mandatory.16EFRAG. EFRAG IG 1 – Materiality Assesment. (2024). 27Global Reporting Initiative. Consolidated Set of the GRI Standards. (2023). This is due to the fact, that there is no method, which would fit to every company size, sector or type, so companies have to adapt the procedure to their company needs.16EFRAG. EFRAG IG 1 – Materiality Assesment. (2024). For GRI the suggested steps can be found in GRI 3 and for the ESRS in ESRS 1, chapter 3.25EFRAG. ESRS 1 General Requirements. Draft European Sustainability Reporting Standards (2022).,27Global Reporting Initiative. Consolidated Set of the GRI Standards. (2023).

Figure 1 gives an overview of the steps that will be explained in the next chapters. Because GRI does not directly use the term of financial or double materiality, the steps on the right-hand side in yellow are only relevant for the ESRS and can be ignored for single materiality. The individual steps are not to be understood as a separate unit. In some cases, the transition between the steps is fluid or the specific sequence of steps is interchangeable (like for the steps of identifying impact, risks and opportunities and stakeholders).

3.2.1 Getting an overview and defining purpose and scope

The first step of a materiality analysis should be to define the purpose and scope of the materiality analysis.45KPMG. Sustainable Insight The essentials of materiality assessment (2014). To do that companies should get an overview of their business activities and stakeholders.46KPMG. Sustainable Insight. The essentials of materiality assessment (2014). In general, this can mean defining what materiality looks like for the company, which parts and/or regions of the company should be included in the assessment and perhaps deciding which standard or framework fits best for the company and its goals for a materiality analysis.45KPMG. Sustainable Insight The essentials of materiality assessment (2014).

For GRI the first step is called “Understand the organization’s context” and the focus is on getting an overarching view of the industry type, activities, the value chain, business relations and stakeholders to ensure that all the information a company needs for its materiality assessment is available.27Global Reporting Initiative. Consolidated Set of the GRI Standards. (2023). While collecting the information, the company also decides, based on the availability and their perception of materiality, what the scope of the materiality analysis should be. The purpose for GRI is already clear, since GRI is a reporting standard the company has to find the material topics in order to decide which of the topic standards to report on.27Global Reporting Initiative. Consolidated Set of the GRI Standards. (2023). As part of GRI 3 the material topics should also be taken into consideration when defining sustainability goals.27Global Reporting Initiative. Consolidated Set of the GRI Standards. (2023).

For ESRS this step would relate to step A “Understanding the context”, where especially the activities and business relationships, other contextual information and the affected stakeholders should be taken into account.16EFRAG. EFRAG IG 1 – Materiality Assesment. (2024). “Other contextual information” for ESRS means the relevant legal and regulatory landscape and also other published information e.g. media or scientific reports.16EFRAG. EFRAG IG 1 – Materiality Assesment. (2024). The ESRS emphasises the value and consideration of stakeholders when understanding the company’s context. This will be further elaborated in the next chapter “Identify relevant stakeholders”.

As this is a rather internal process no example is provided for this step.

3.2.2 Identify relevant stakeholders

The step of identifying relevant stakeholders is overlapping with the first step of defining purpose and scope and can also be realised simultaneously to the next step of defining potential topics. Stakeholder engagement is essential when understanding stakeholder’s expectations and thus for sustainability reporting.30Schwoy, S. & Dutzi, A. Materiality analysis as the basis for sustainability strategies and reporting-A systematic review of approaches and recommendations for practice. Handbook of Sustainability-Driven Business Strategies in Practice, 35-58 (2021). 47Kaspersen, M. & Johansen, T. R. in Measuring Sustainability and CSR: From Reporting to Decision-Making (eds Slobodan Kacanski, Johannes Kabderian Dreyer, & Kristian J. Sund) 73-83 (Springer International Publishing, 2023). 48Garst, J., Maas, K. & Suijs, J. Materiality Assessment Is an Art, Not a Science: Selecting ESG Topics for Sustainability Reports. California Management Review 65, 64-90 (2022). https://doi.org/10.1177/00081256221120692 Before engaging with stakeholders, a company has to define what the relevant stakeholder groups are and which representatives of the groups could be available for engaging with the company.47Kaspersen, M. & Johansen, T. R. in Measuring Sustainability and CSR: From Reporting to Decision-Making (eds Slobodan Kacanski, Johannes Kabderian Dreyer, & Kristian J. Sund) 73-83 (Springer International Publishing, 2023). Typically important stakeholders for materiality assessments are e.g. employees, customers, shareholders, suppliers, industry associations, non-governmental organizations (NGOs), local community and politics or media.48Garst, J., Maas, K. & Suijs, J. Materiality Assessment Is an Art, Not a Science: Selecting ESG Topics for Sustainability Reports. California Management Review 65, 64-90 (2022). https://doi.org/10.1177/00081256221120692 Companies should also determine if there are other non-typical stakeholders.47Kaspersen, M. & Johansen, T. R. in Measuring Sustainability and CSR: From Reporting to Decision-Making (eds Slobodan Kacanski, Johannes Kabderian Dreyer, & Kristian J. Sund) 73-83 (Springer International Publishing, 2023). In general, the criteria for selecting stakeholders should be whether they could potentially offer relevant information to the company.30Schwoy, S. & Dutzi, A. Materiality analysis as the basis for sustainability strategies and reporting-A systematic review of approaches and recommendations for practice. Handbook of Sustainability-Driven Business Strategies in Practice, 35-58 (2021). When interacting with stakeholders it is important, that they are part of a two-way dialogue and are not influenced in their opinion.47Kaspersen, M. & Johansen, T. R. in Measuring Sustainability and CSR: From Reporting to Decision-Making (eds Slobodan Kacanski, Johannes Kabderian Dreyer, & Kristian J. Sund) 73-83 (Springer International Publishing, 2023). There are different methods that can be used in stakeholder engagement like interviews, surveys, workshops or focus groups that generate primary data due to direct dialog with stakeholders.46KPMG. Sustainable Insight. The essentials of materiality assessment (2014). It is also possible to use media reports or other analyses to understand stakeholder views, but this is often perceived as less valuable information.48Garst, J., Maas, K. & Suijs, J. Materiality Assessment Is an Art, Not a Science: Selecting ESG Topics for Sustainability Reports. California Management Review 65, 64-90 (2022). https://doi.org/10.1177/00081256221120692 The expertise of stakeholders can then be used in the next steps to gather information about the topics and ranking them.30Schwoy, S. & Dutzi, A. Materiality analysis as the basis for sustainability strategies and reporting-A systematic review of approaches and recommendations for practice. Handbook of Sustainability-Driven Business Strategies in Practice, 35-58 (2021). 47Kaspersen, M. & Johansen, T. R. in Measuring Sustainability and CSR: From Reporting to Decision-Making (eds Slobodan Kacanski, Johannes Kabderian Dreyer, & Kristian J. Sund) 73-83 (Springer International Publishing, 2023). 48Garst, J., Maas, K. & Suijs, J. Materiality Assessment Is an Art, Not a Science: Selecting ESG Topics for Sustainability Reports. California Management Review 65, 64-90 (2022). https://doi.org/10.1177/00081256221120692

Stakeholders play a crucial role in the GRI Standards, and are marked as one of four key concepts in GRI 1.27Global Reporting Initiative. Consolidated Set of the GRI Standards. (2023). They are defined as “individuals or groups that have interests that are affected or could be affected by an organization’s activities “ (GRI 2023, p.13).27Global Reporting Initiative. Consolidated Set of the GRI Standards. (2023). In step 2 of the materiality analysis, GRI states that companies should seek to understand the concerns of its stakeholders.27Global Reporting Initiative. Consolidated Set of the GRI Standards. (2023). GRI especially mentions to engage in direct dialogue with vulnerable groups, to reduce barriers when engaging and to prioritize severely affected stakeholders, but GRI does not give specifications on how to engage with stakeholders.27Global Reporting Initiative. Consolidated Set of the GRI Standards. (2023).

The ESRS classify stakeholders into 1) affected stakeholders and 2) users of the sustainability statement.16EFRAG. EFRAG IG 1 – Materiality Assesment. (2024). According to ESRS the engagement with them is central to the impact analysis, but there is no obligation on engagement with stakeholders, nevertheless the ESRS require all users to be transparent on whether and how stakeholders were consulted.16EFRAG. EFRAG IG 1 – Materiality Assesment. (2024).

Practical example

As an example, Arla carried out a stakeholder analysis to identify their key stakeholders for the materiality analysis.49Arla. Annual Report 2023. (2024). <https://www.arla.com/493575/globalassets/arla-global/company—overview/investor/annual-reports/2023/arla_annual-report-2023_uk_v2.pdf>. These were “farmer owners, nature, customers, consumers, affected communities, workforce, NGOs, financial institutions, the media and governments” (Arla 2024, p. 32).49Arla. Annual Report 2023. (2024). <https://www.arla.com/493575/globalassets/arla-global/company—overview/investor/annual-reports/2023/arla_annual-report-2023_uk_v2.pdf>. Arla states that they were not able to reach certain stakeholders and therefore used proxies for their assessment of material topics, which is not a direct dialogue and can therefore be criticised.49Arla. Annual Report 2023. (2024). <https://www.arla.com/493575/globalassets/arla-global/company—overview/investor/annual-reports/2023/arla_annual-report-2023_uk_v2.pdf>. But they assured their results externally afterwards with the help of their stakeholders.49Arla. Annual Report 2023. (2024). <https://www.arla.com/493575/globalassets/arla-global/company—overview/investor/annual-reports/2023/arla_annual-report-2023_uk_v2.pdf>.

The German mobility provider BSAG also states that they carried out two workshops to find their relevant stakeholders and then did interviews to consult them on their material topics.50Bremer Straßenbahn AG. Nachhaltigkeitsbericht 2023. (2024). <https://www.bsag.de/fileadmin/user_upload/redakteure/unternehmen/berichte/NHB_2023_paraphiert.pdf>. These interviews are a good example for direct consultation of stakeholders.

3.2.3 Impact materiality

The following steps for identifying impact materiality are relevant for both GRI and ESRS materiality assessment.

Identify potential topics

The first step for assessing material topics in context of impact materiality is to identify all topics, that could potentially be relevant for a company. In practice a company can create a long-list of all potential topics.45KPMG. Sustainable Insight The essentials of materiality assessment (2014). To find these, different methods can be helpful. Some of them are fluent with the first step of getting an overview of the context. For example a company can analyse media reports, internal data, scientific publications, sector-specific regulations or research on current sustainability trends and challenges.45KPMG. Sustainable Insight The essentials of materiality assessment (2014). It can also be helpful to include external stakeholders, that were previously defined in step two, to ensure all areas are covered.45KPMG. Sustainable Insight The essentials of materiality assessment (2014). Depending on the extent of the long-list it can also be beneficial to cluster the topics into groups and make sure there are no identical topics with different terms so that the next steps will not be too complex to execute.45KPMG. Sustainable Insight The essentials of materiality assessment (2014). For example, when the issues of working hours, wages and collective bargaining come up, a company could decide to cluster them into one topic of “working conditions”. When clustering the topics it should always be clearly documented which smaller topics are clustered together so that stakeholders can make the right assumptions about the topics.51Systain. 7 success factors for a good materiality analysis. (2018). It is also important to include topics concerning the value chain of a company, because especially companies with value chains that go beyond EU boarders face challenges e.g. about social aspects or corruption in the value chain, that are legally regulated inside the EU.51Systain. 7 success factors for a good materiality analysis. (2018).

For GRI this step is called “Identify actual and potential impacts”.27Global Reporting Initiative. Consolidated Set of the GRI Standards. (2023). As can be seen in the headline GRI differentiates between potential (“those that could occur, but have not yet occurred”(GRI 2023, p.105) and actual impacts (“those that have already occurred” (GRI 2023, p.105).27Global Reporting Initiative. Consolidated Set of the GRI Standards. (2023). Furthermore, GRI states that these impacts should include “positive and negative [as well as] short-term and long-term[…], intended and unintended[…], reversible and irreversible impacts” (GRI 2023, p. 105).27Global Reporting Initiative. Consolidated Set of the GRI Standards. (2023). When a company wants to report according to the GRI Standards it should also take in account the sector standards by GRI, because they give insights about the topics likely to be among the material topics for companies in that sector.52Global Reporting Initiative. GRI Standards English Language, <https://www.globalreporting.org/how-to-use-the-gri-standards/gri-standards-english-language> (2024). Furthermore, the long list could be based on all the topic standards (GRI 101 – GRI 418) as the materiality assessment for GRI should be used to determine which of the topic standards a company has to report on.27Global Reporting Initiative. Consolidated Set of the GRI Standards. (2023). This also reduces the risk of leaving out important topics.30Schwoy, S. & Dutzi, A. Materiality analysis as the basis for sustainability strategies and reporting-A systematic review of approaches and recommendations for practice. Handbook of Sustainability-Driven Business Strategies in Practice, 35-58 (2021).

Step B in the ESRS “Identification of the actual and potential IROs related to sustainability matters” combines defining topics for impact and financial materiality.16EFRAG. EFRAG IG 1 – Materiality Assesment. (2024). In order to be more precise about these steps, this chapter focuses on the impact perspective while a later chapter will focus on financial materiality.

ESRS states that the outcome of this step should be a long-list of all potential IROs whereas impacts are used to determine material topics for the impact perspective and risks and opportunities for the financial perspective.16EFRAG. EFRAG IG 1 – Materiality Assesment. (2024). For the long list of impacts the ESRS recommend to use the sustainability matters in ESRS 1, which are the sustainability matters covered in topical ESRS clustered in ESG-topics.16EFRAG. EFRAG IG 1 – Materiality Assesment. (2024). There are no concrete specifications as to how this long list should be compiled or obligatory methods that companies must use.

Gather information about the topics and ranking them

This step is about ranking the topics according to their economic, social and environmental impact, so that the company can define the topics with the highest impact as material.45KPMG. Sustainable Insight The essentials of materiality assessment (2014). For this step it is important to define a methodology that is used to rank the topics, for example this could be to evaluate the topics according to their importance on a scale from one to five or to compare different topics and let the stakeholder decide which are more important than others.45KPMG. Sustainable Insight The essentials of materiality assessment (2014).,51Systain. 7 success factors for a good materiality analysis. (2018). In this step it is important to explain the meaning of “impact” and the purpose of the survey to stakeholders so they can answer adequately.48Garst, J., Maas, K. & Suijs, J. Materiality Assessment Is an Art, Not a Science: Selecting ESG Topics for Sustainability Reports. California Management Review 65, 64-90 (2022). https://doi.org/10.1177/00081256221120692 While online surveys are a good way of involving a large number of stakeholders, interviews can be used in order to obtain more specific information that may be required for the subsequent design of a sustainability strategy.51Systain. 7 success factors for a good materiality analysis. (2018). However, these can probably only be conducted with a smaller number of stakeholders.51Systain. 7 success factors for a good materiality analysis. (2018).

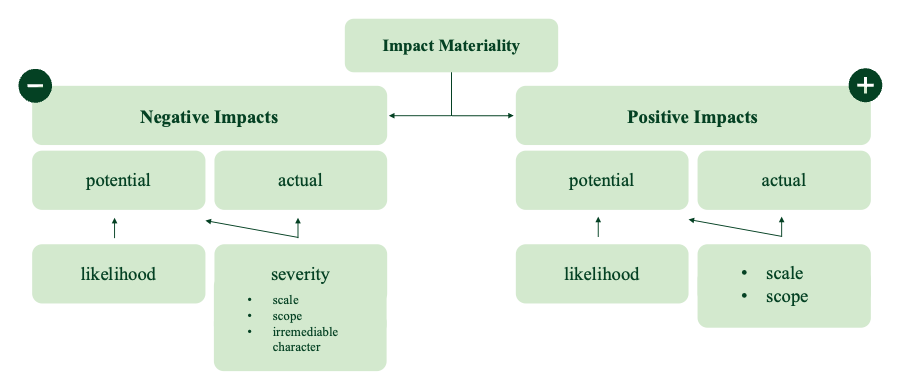

GRI calls this step “Assess the significance of the impacts” and gives guidelines what criteria should be used to assess the impacts.27Global Reporting Initiative. Consolidated Set of the GRI Standards. (2023). For actual negative impacts companies should evaluate the severity of the impact.27Global Reporting Initiative. Consolidated Set of the GRI Standards. (2023). Moreover the severity is defined by scale (how grave), scope (how widespread) and irremediable character (how hard it is to counteract).27Global Reporting Initiative. Consolidated Set of the GRI Standards. (2023). GRI emphasizes the importance on human rights when assessing negative impacts. For positive impacts a company should take into account the significance, that is only defined by scale and scope.27Global Reporting Initiative. Consolidated Set of the GRI Standards. (2023). For potential positive and negative impacts the likelihood of it becoming an actual impact also defines the overall significance.27Global Reporting Initiative. Consolidated Set of the GRI Standards. (2023). The potential negative and positive impacts can also be seen as risks and opportunities (which will be relevant for assessing the financial materiality perspective), but in GRI they are not framed to be used for financial materiality, and they do not have to be assessed in the same extent as for the ESRS.27Global Reporting Initiative. Consolidated Set of the GRI Standards. (2023). According to GRI, stakeholders should be consulted in this step, but this is not further elaborated.27Global Reporting Initiative. Consolidated Set of the GRI Standards. (2023).

For the ESRS step “Assessment and determination of material IROs related to sustainability matters” the part of “Impact Materiality assessment” will be the basis.16EFRAG. EFRAG IG 1 – Materiality Assesment. (2024). For assessing the severity the criteria set by GRI are exactly the same for ESRS (see Figure 2).16EFRAG. EFRAG IG 1 – Materiality Assesment. (2024). ESRS sets more specific criteria for assessing the potential negative and positive impacts (risks and opportunities), that are used to determine financial materiality (further information in chapter 3.2.4).25EFRAG. ESRS 1 General Requirements. Draft European Sustainability Reporting Standards (2022). In ESRS 1 it is proposed to map the actual impacts by first evaluating each of the above criteria for negative and positive impacts individually, and then combining the results with each other.16EFRAG. EFRAG IG 1 – Materiality Assesment. (2024). For the potential impacts the same methodology can be adapted by also adding likelihood afterwards on a different axis (see Figure 3).16EFRAG. EFRAG IG 1 – Materiality Assesment. (2024).

Determine material impact topics

To finally determine the material topics on the side of impact materiality a company has to apply threshold values.46KPMG. Sustainable Insight. The essentials of materiality assessment (2014). 48Garst, J., Maas, K. & Suijs, J. Materiality Assessment Is an Art, Not a Science: Selecting ESG Topics for Sustainability Reports. California Management Review 65, 64-90 (2022). https://doi.org/10.1177/00081256221120692 In the previous step all potential topics have been ranked, so now it is possible to use a value to differentiate at what point of the list the topics will be considered as material. In practice it is recommended to set the threshold values simultaneously to the scale for ranking the potential topics.48Garst, J., Maas, K. & Suijs, J. Materiality Assessment Is an Art, Not a Science: Selecting ESG Topics for Sustainability Reports. California Management Review 65, 64-90 (2022). https://doi.org/10.1177/00081256221120692 This ensures greater objectivity, as the limit is set in advance and not when the company knows the results of the ranking.48Garst, J., Maas, K. & Suijs, J. Materiality Assessment Is an Art, Not a Science: Selecting ESG Topics for Sustainability Reports. California Management Review 65, 64-90 (2022). https://doi.org/10.1177/00081256221120692 In this last step this threshold value then defines the material topics of the impact materiality perspective.

This relates to the fourth step in the GRI Standards, named “Prioritize the most significant impacts for reporting”.27Global Reporting Initiative. Consolidated Set of the GRI Standards. (2023). GRI recommends to set the cut-off point according to how many topics should be discussed in the sustainability report.27Global Reporting Initiative. Consolidated Set of the GRI Standards. (2023). If a company gathered and clustered their potential topics, that have been ranked in the previous step, into 30 categories, and the company wants to report on ten topics, then, according to GRI, it should set the threshold at the appropriate value.

When defining the threshold value ESRS states that “priority should be given to any supportable evidence that provides as much objectivity as possible to the materiality conclusion” (EFRAG 2024, p.28).16EFRAG. EFRAG IG 1 – Materiality Assesment. (2024). Nevertheless, it is recognised that this is not always possible.16EFRAG. EFRAG IG 1 – Materiality Assesment. (2024). Setting a cut-off point is therefore a very individual decision for every company.

Practical example

In practice these three steps are closely linked. BSAG started their materiality analysis with an overview of internal data as well as an analysis of their environment to conduct a long list of potential material topics, whose content was based on the ESRS topical standards.50Bremer Straßenbahn AG. Nachhaltigkeitsbericht 2023. (2024). <https://www.bsag.de/fileadmin/user_upload/redakteure/unternehmen/berichte/NHB_2023_paraphiert.pdf>. After that they let their stakeholders evaluate their topics and finalized their analysis with another workshop to determine the material topics.50Bremer Straßenbahn AG. Nachhaltigkeitsbericht 2023. (2024). <https://www.bsag.de/fileadmin/user_upload/redakteure/unternehmen/berichte/NHB_2023_paraphiert.pdf>.

Orsted describes in more detail how they evaluated their potential topics, and their methodology is very similar to the requirements of GRI and the ESRS.53Orsted. Orsted Annual Report 2023. (2024). <https://orstedcdn.azureedge.net/-/media/annual-report-2023/orsted-ar-2023.pdf?rev=526307f68e2047b3a1df8dd2cdf719ec&hash=E6069E12C1792AD620FA12898587394C>. First, they consulted internal data like impact reports and stakeholder findings to predefine their potential topics.53Orsted. Orsted Annual Report 2023. (2024). <https://orstedcdn.azureedge.net/-/media/annual-report-2023/orsted-ar-2023.pdf?rev=526307f68e2047b3a1df8dd2cdf719ec&hash=E6069E12C1792AD620FA12898587394C>. During workshops Orsted scored the severity of their actual topics with taking scale, scope and irremediable character and adding likelihood for their potential topics.53Orsted. Orsted Annual Report 2023. (2024). <https://orstedcdn.azureedge.net/-/media/annual-report-2023/orsted-ar-2023.pdf?rev=526307f68e2047b3a1df8dd2cdf719ec&hash=E6069E12C1792AD620FA12898587394C>. In total they evaluated 120 impacts.53Orsted. Orsted Annual Report 2023. (2024). <https://orstedcdn.azureedge.net/-/media/annual-report-2023/orsted-ar-2023.pdf?rev=526307f68e2047b3a1df8dd2cdf719ec&hash=E6069E12C1792AD620FA12898587394C>. Final results were defined during a workshop and reviewed by management.53Orsted. Orsted Annual Report 2023. (2024). <https://orstedcdn.azureedge.net/-/media/annual-report-2023/orsted-ar-2023.pdf?rev=526307f68e2047b3a1df8dd2cdf719ec&hash=E6069E12C1792AD620FA12898587394C>. After setting a threshold value Orsted defined 25 material impact topics.53Orsted. Orsted Annual Report 2023. (2024). <https://orstedcdn.azureedge.net/-/media/annual-report-2023/orsted-ar-2023.pdf?rev=526307f68e2047b3a1df8dd2cdf719ec&hash=E6069E12C1792AD620FA12898587394C>.

3.2.4 Financial materiality

As explained in the previous chapter, the GRI looks at single materiality, which only focusses on impact perspective. The CSRD and related ESRS standards assess sustainability issues not only from an impact perspective, but also from a financial perspective – this results in the double materiality.16EFRAG. EFRAG IG 1 – Materiality Assesment. (2024). 19Kirchhoff, K., Niefünd, S. & von Pressentin, J. ESG: Nachhaltigkeit als strategischer Erfolgsfaktor. (2024). The next steps are therefore only relevant when carrying out the materiality analysis according to the ESRS.

While identifying the impacts of a company leads to the topics that are material from an impact perspective, identifying the risks and opportunities are essential when identifying the topics for financial materiality perspective. Nevertheless the steps are relatively similar to the identifying impact materiality.

Identify potential risks and opportunities

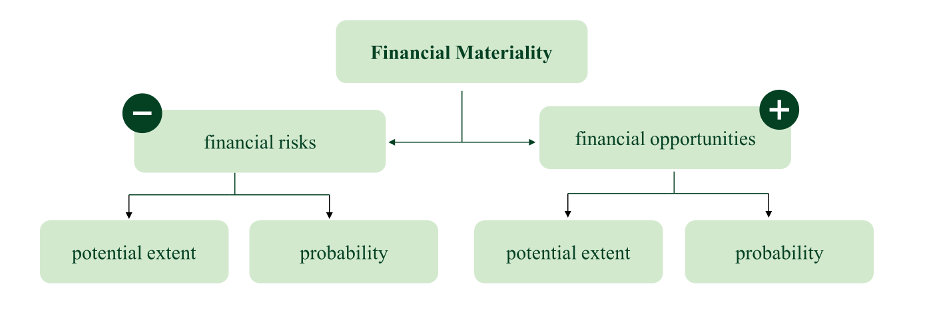

The following steps of financial materiality assessment relate the step C “Assessment and determination of material IROs related to sustainability matters” and especially the section about financial materiality of the ESRS.16EFRAG. EFRAG IG 1 – Materiality Assesment. (2024). First, the company evaluates various opportunities and risks according to objective criteria and the extent to which they impact the company’s financial position.16EFRAG. EFRAG IG 1 – Materiality Assesment. (2024). If the financial impact is material, the respective opportunities and risks are material.16EFRAG. EFRAG IG 1 – Materiality Assesment. (2024). The time horizon considered in the materiality analysis is crucial. Financial materiality considers short, medium and long term impacts.16EFRAG. EFRAG IG 1 – Materiality Assesment. (2024). In the case of financial materiality, the ESRS time horizon is considered in the sense that it is extended in relation to the annual financial statements or other financial reports.16EFRAG. EFRAG IG 1 – Materiality Assesment. (2024). When analysing sustainability opportunities and risks, longer time horizons are often considered and a long-term perspective is taken.16EFRAG. EFRAG IG 1 – Materiality Assesment. (2024).

Furthermore, the European Financial Reporting Advisory Group (EFRAG) makes it clear that companies should not only focus on impacts that are recognised in the financial reports in the context of financial materiality.16EFRAG. EFRAG IG 1 – Materiality Assesment. (2024). Companies are dependent on various social and environmental resources.16EFRAG. EFRAG IG 1 – Materiality Assesment. (2024). The dependencies of these resources are part of the analysis of financial materiality.16EFRAG. EFRAG IG 1 – Materiality Assesment. (2024). Companies can be dependent on various natural resources, such as water.54Baumüller, J. & Mayr, J. Quick Guide Wesentlichkeitsanalyse gemäss CSRD und ESRS. (2023). Due to the water shortage in particular, companies that are dependent on this resource must include this risk in their risk analysis.54Baumüller, J. & Mayr, J. Quick Guide Wesentlichkeitsanalyse gemäss CSRD und ESRS. (2023).

Deloitte provides guidance on identifying opportunities and risks as part of the materiality analysis with five steps.55Deloitte. A practical approach to assess financial materiality. Working paper on double materiality (2023). Opportunities and risks can be analysed by looking at the value chain.55Deloitte. A practical approach to assess financial materiality. Working paper on double materiality (2023). In addition, old opportunity and risk analyses can be used and stakeholders can be interviewed.55Deloitte. A practical approach to assess financial materiality. Working paper on double materiality (2023). Last but not least, the results of risk management should be used and, once the key sustainability issues have been analysed, further opportunities and risks can be derived from them.55Deloitte. A practical approach to assess financial materiality. Working paper on double materiality (2023).

At the end of this step, the companies have a longlist of opportunities and risks that are assessed in the next step.16EFRAG. EFRAG IG 1 – Materiality Assesment. (2024).

Gather information and ranking risks and opportunities

According to ESRS, it is relevant for the company to consider the identified opportunities and risks in an integrated manner.54Baumüller, J. & Mayr, J. Quick Guide Wesentlichkeitsanalyse gemäss CSRD und ESRS. (2023). This means that for each opportunity and each risk, the probability of the opportunity or risk is materialising and, on the other hand, the potential impact of the opportunity or risk should be shown (see figure 4).54Baumüller, J. & Mayr, J. Quick Guide Wesentlichkeitsanalyse gemäss CSRD und ESRS. (2023).

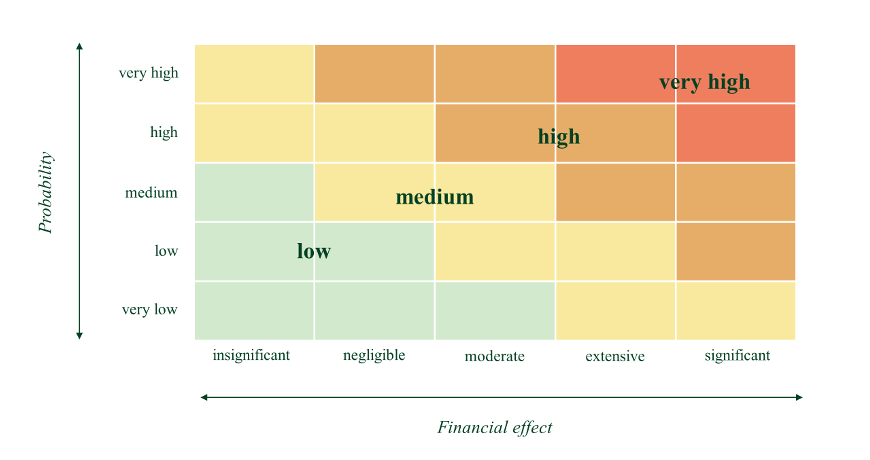

Companies can use a scale to assess the probabilities and financial effects of opportunities and risks and thus rank them (see Figure 5).55Deloitte. A practical approach to assess financial materiality. Working paper on double materiality (2023). The scale may look slightly different depending on the company.55Deloitte. A practical approach to assess financial materiality. Working paper on double materiality (2023).

The opportunities and risks identified can be quantitatively assessed.55Deloitte. A practical approach to assess financial materiality. Working paper on double materiality (2023). This makes it possible to recognise the impact of each opportunity and risk in the form of figures.55Deloitte. A practical approach to assess financial materiality. Working paper on double materiality (2023). For example, the net profit is noted for the opportunities.55Deloitte. A practical approach to assess financial materiality. Working paper on double materiality (2023). However, this process is not easy for companies as a lot of data is required.55Deloitte. A practical approach to assess financial materiality. Working paper on double materiality (2023).

External parties such as investors can also be involved in the process to validate the list of opportunities and risks.16EFRAG. EFRAG IG 1 – Materiality Assesment. (2024). If sustainability risks are also included in the company’s risk management, the results can be compared with them.16EFRAG. EFRAG IG 1 – Materiality Assesment. (2024).

Determine material financial topics

As described above, the time horizons are decisive in the materiality analysis, but especially in the financial materiality analysis. As part of the financial materiality analysis, companies must consider longer time horizons than in traditional risk management.54Baumüller, J. & Mayr, J. Quick Guide Wesentlichkeitsanalyse gemäss CSRD und ESRS. (2023). Long-term means that a period of more than five years is considered.54Baumüller, J. & Mayr, J. Quick Guide Wesentlichkeitsanalyse gemäss CSRD und ESRS. (2023). Risk management often considers periods of a maximum of three years, which is too short-term for CSRD.54Baumüller, J. & Mayr, J. Quick Guide Wesentlichkeitsanalyse gemäss CSRD und ESRS. (2023).

To finally determine the material risks and opportunities, threshold values are set that show the financial impact of the opportunities or risks on the company and differentiate material from non-material topics.16EFRAG. EFRAG IG 1 – Materiality Assesment. (2024). The threshold values are either quantitative or qualitative data. When using qualitive data and no total is set, there should be a description.16EFRAG. EFRAG IG 1 – Materiality Assesment. (2024). Either way, the results should be evidence based.16EFRAG. EFRAG IG 1 – Materiality Assesment. (2024). These threshold values then show how the sustainability issues affect the financial position, capital or cash flow, for example.16EFRAG. EFRAG IG 1 – Materiality Assesment. (2024). The ESRS does not specify any thresholds, but the companies themselves should develop them.16EFRAG. EFRAG IG 1 – Materiality Assesment. (2024).

If the company has summarised the financially material topics, each of these topics must be reported on.16EFRAG. EFRAG IG 1 – Materiality Assesment. (2024). If these topics are not clearly described, this can lead, for example, to investors making the wrong decisions. Investors may base their decisions on the information in the sustainability report, so it is important to provide complete information.16EFRAG. EFRAG IG 1 – Materiality Assesment. (2024).

Practical example

Arla carried out the double materiality analysis according to ESRS for the first time as part of its sustainability report for.56202348 Arla assessed the opportunities and risks in the context of financial materiality on two points.49Arla. Annual Report 2023. (2024). <https://www.arla.com/493575/globalassets/arla-global/company—overview/investor/annual-reports/2023/arla_annual-report-2023_uk_v2.pdf>. Firstly, how likely the opportunities and risks are to materialise and secondly, what impact they have on the company’s financial situation.49Arla. Annual Report 2023. (2024). <https://www.arla.com/493575/globalassets/arla-global/company—overview/investor/annual-reports/2023/arla_annual-report-2023_uk_v2.pdf>. It should be mentioned here that Arla was not yet able to use thresholds for the assessment of financial materiality, as these were not yet sufficiently developed at the time.49Arla. Annual Report 2023. (2024). <https://www.arla.com/493575/globalassets/arla-global/company—overview/investor/annual-reports/2023/arla_annual-report-2023_uk_v2.pdf>. Arla therefore had to use qualitative thresholds.49Arla. Annual Report 2023. (2024). <https://www.arla.com/493575/globalassets/arla-global/company—overview/investor/annual-reports/2023/arla_annual-report-2023_uk_v2.pdf>. As mentioned in the previous section, it can be helpful to link the materiality process with the company’s general risk management. This has not yet happened in the case of Arla.49Arla. Annual Report 2023. (2024). <https://www.arla.com/493575/globalassets/arla-global/company—overview/investor/annual-reports/2023/arla_annual-report-2023_uk_v2.pdf>.

Metsa on the other hand states that risks and opportunities (therefore the financial materiality assessment) were based on their monetary value, which was previously defined in their risk management.57Metsa Group. Metsä Group Annual review 2023. (2024). <https://www.metsagroup.com/globalassets/metsa-group/documents/investors/financial-reporting/annual-reports/2023/metsa-group-annual-review-2023.pdf>. In addition, they also used reputational impacts and remediability for the financial assessment and remediability was considered along the short to long term time Horizons.57Metsa Group. Metsä Group Annual review 2023. (2024). <https://www.metsagroup.com/globalassets/metsa-group/documents/investors/financial-reporting/annual-reports/2023/metsa-group-annual-review-2023.pdf>. Metsa also made sure to cover all ESRS topical standards for their analysis.57Metsa Group. Metsä Group Annual review 2023. (2024). <https://www.metsagroup.com/globalassets/metsa-group/documents/investors/financial-reporting/annual-reports/2023/metsa-group-annual-review-2023.pdf>.

3.2.5 Consolidation of impact and financial materiality

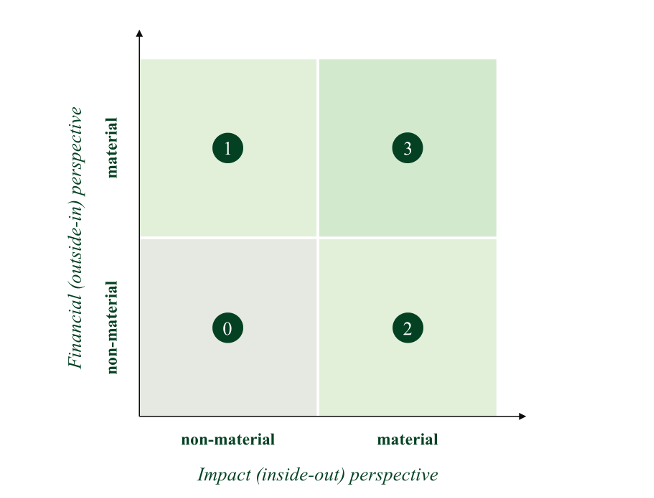

This step only applies, if companies used the double materiality approach. Otherwise, no consolidation of both perspectives is needed. For ESRS a company has to consolidate the material topics of both the impact and financial perspective.16EFRAG. EFRAG IG 1 – Materiality Assesment. (2024). The definition of double materiality states a topic as relevant, if it was determined as material in the impact and/or the financial analysis (see Figure 6).16EFRAG. EFRAG IG 1 – Materiality Assesment. (2024). It is recommended to validate the final results of all identified IROs with the management.16EFRAG. EFRAG IG 1 – Materiality Assesment. (2024).

In practice some companies use a materiality matrix to display their ranking of both materiality perspectives. Neither EFRAG nor GRI mention this presentation of material topics, but considering the definition of double materiality this visual representation is reasonable.16EFRAG. EFRAG IG 1 – Materiality Assesment. (2024).,25EFRAG. ESRS 1 General Requirements. Draft European Sustainability Reporting Standards (2022).,27Global Reporting Initiative. Consolidated Set of the GRI Standards. (2023). Considering the matrix below a topic would be material, if it was placed in areas one, two, or three of the matrix.

3.2.6 Reporting results and including results in corporate and/or sustainability strategy

A materiality analysis is the basis for developing an adequate sustainability strategy and successfully manage sustainability matters as well as for a transparent and reliable sustainability report.30Schwoy, S. & Dutzi, A. Materiality analysis as the basis for sustainability strategies and reporting-A systematic review of approaches and recommendations for practice. Handbook of Sustainability-Driven Business Strategies in Practice, 35-58 (2021). The results of the analysis can be used to determine the content of the sustainability report.30Schwoy, S. & Dutzi, A. Materiality analysis as the basis for sustainability strategies and reporting-A systematic review of approaches and recommendations for practice. Handbook of Sustainability-Driven Business Strategies in Practice, 35-58 (2021).

Throughout the whole process of materiality assessment it is important to document the steps because both GRI and the ESRS require to report on the process to give transparency about how the material topics were defined.16EFRAG. EFRAG IG 1 – Materiality Assesment. (2024). 27Global Reporting Initiative. Consolidated Set of the GRI Standards. (2023). When a company decided on their material topics it has to set goals and measures to mitigate their negative impacts and risks and to seize their opportunities.16EFRAG. EFRAG IG 1 – Materiality Assesment. (2024). 27Global Reporting Initiative. Consolidated Set of the GRI Standards. (2023).

In summary, the ESRS standards require companies to develop a sustainability strategy that considers both the impact perspective and the financial perspective. Only through this holistic analysis will all material sustainability issues be addressed and companies have a sufficient basis for CSRD reporting.58Urata, B.-M. Roadmap zur Entwicklung von Nachhaltigkeits- und Klimastrategien. Econic, 39-43 (2023).

Practical example

In the sustainability report of Arla it can be seen clearly that Arla used the results of their material topics not only to structure their sustainability report but also to set goals and measures for their sustainability strategy.49Arla. Annual Report 2023. (2024). <https://www.arla.com/493575/globalassets/arla-global/company—overview/investor/annual-reports/2023/arla_annual-report-2023_uk_v2.pdf>. The chapters of the report are clustered like their material topics and in the chapters Arla describes their measurements, goals and strategy for each topic.49Arla. Annual Report 2023. (2024). <https://www.arla.com/493575/globalassets/arla-global/company—overview/investor/annual-reports/2023/arla_annual-report-2023_uk_v2.pdf>.

4 Drivers and barriers

The following chapter presents the drivers and barriers of the materiality analysis. The focus here lies on drivers and barriers for companies that carry out a materiality analysis.

4.1 Drivers

Firm-internal drivers:

As shown in the previous chapter, the aim of the materiality analysis is to systematically identify material ESG topics for the company.19Kirchhoff, K., Niefünd, S. & von Pressentin, J. ESG: Nachhaltigkeit als strategischer Erfolgsfaktor. (2024). This means that the materiality analysis is the driver for filtering out the sustainability issues that are particularly important.30Schwoy, S. & Dutzi, A. Materiality analysis as the basis for sustainability strategies and reporting-A systematic review of approaches and recommendations for practice. Handbook of Sustainability-Driven Business Strategies in Practice, 35-58 (2021). By gaining a better understanding of the key issues, the company can seize opportunities in a more targeted manner and avoid risks at the same time.19Kirchhoff, K., Niefünd, S. & von Pressentin, J. ESG: Nachhaltigkeit als strategischer Erfolgsfaktor. (2024). These are precisely the first internal drivers of the materiality analysis.

In addition to the systematic identification of sustainability issues, the materiality analysis provides further internal drivers that companies can use. The impact analysis in particular is valuable for the company and is a driver to identify the topics that are not only important for the sustainability strategy, but also for the governance of the company and in relation to the supply chains and the implementation of the due diligence obligations.59Moock, P. Standortanalyse mit den SDGs. (Springer, 2024).

In addition to impact materiality, financial materiality is also an important driver for companies. Financial materiality analyses the opportunities and risks for companies in relation to different sustainability issues.55Deloitte. A practical approach to assess financial materiality. Working paper on double materiality (2023). This means that certain issues can have a significant impact on a company’s financial position.55Deloitte. A practical approach to assess financial materiality. Working paper on double materiality (2023). If the companies assumptions about this are correct, it can not only create value for stakeholders, but also influence the enterprise value.55Deloitte. A practical approach to assess financial materiality. Working paper on double materiality (2023).