Authors: Finja Kirchhoff, Meike Polonji, Hanna Schwuchow

Edited by: –

Last updated: October 9, 2025

Executive summary

SA 8000 is a globally recognized certification standard developed by Social Accountability International (SAI) to promote fair labor practices and ethical business conduct. It addresses nine key areas: child labor, forced labor, health and safety, freedom of association, discrimination, disciplinary practices, working hours, compensation, and management systems.

The standard is highly relevant due to growing societal expectations for corporate social responsibility and the need to restore trust in businesses. It provides a certifiable framework that complements other standards like ISO 26000 and the Corporate Sustainability Reporting Directive (CSRD), though SA 8000 focuses exclusively on social issues.

Implementation involves a structured certification process supported by tools such as Social Fingerprint, requiring significant investment and ongoing audits. While adoption can improve stakeholder trust, supply chain transparency, and workplace conditions, barriers include high costs, rigid requirements, and limited internal expertise. External drivers include client demands, reputation enhancement, and regulatory incentives, while internal drivers include productivity gains and improved employee relations.

Despite benefits, SA 8000 faces criticism for declining certifications, perceived CSR-washing, and weaknesses in auditing systems, as highlighted by incidents like the Ali Enterprises factory fire. To remain relevant, the standard must adapt to integrate environmental and governance aspects and improve transparency.

Overall, SA 8000 remains a valuable tool for organizations committed to social accountability, but its future depends on addressing implementation challenges and aligning with broader sustainability frameworks.

1 Relevance and definition

After explaining the relevance of the SA 8000 standard at the beginning of the wiki entry, the components and objectives of the standard are defined.

1.1 Relevance

In recent times society´s general trust in companies has significantly declined. This decline in trust is the result of numerous scandals that have come to light and the realization that economic activity is a major contributor to climate change.1Kreipl, C. (2020). Verantwortungsvolle Unternehmensführung: Corporate Governance, Compliance Management und Corporate Social Responsibility. Springer Gabler. https://doi.org/DOI: 10.1007/978-3-658-28140-3 Since the 1960s, movements such as the consumer rights movement, the environmental movement and the women’s movement have led to corporate social responsibility (CSR) coming to the center of attention.2Helmold, M., Dathe, R., Dathe, T., Groß, D.-P. & Hummel, F. (2020). Corporate Social Responsibility im internationalen Kontext: Wettbewerbsvorteile durch nachhaltige Wertschöpfung. Springer Fachmedien Wiesbaden. https://doi.org/DOI: 10.1007/978-3-658-30899-5 The social responsibility of modern companies extends far beyond profit maximization. Companies are expected to fulfill growing normative expectations, deal with systematically incomplete contracts and regulations and counteract the general loss of trust in the market economy by carefully weighing up the moral implications of their actions3Maurice, L. C. S. (2022). Corporate social responsibility: the co-responsibility of business along global supply chains. Springer Gabler.

Various instruments can be used to show stakeholders that companies are aware of this responsibility and act accordingly. For example, companies can publish sustainability reports, report in accordance with the Corporate Sustainability Reporting Directive (CSRD) or introduce codes of conduct to communicate to the public that they take on social responsibility.4Lerner, M. (2023b). Taxonomie und CSRD und ihre Wirkung auf KMU. In M. Lerner (Ed.), Einfluss der EU-Taxonomie auf den Mittelstand (pp. 71-86). Springer Fachmedien Wiesbaden.,5Wickert, C. & Risi, D. (2019). Corporate Social Responsibility. Cambridge University Press. https://doi.org/DOI: 10.1017/9781108775298 Voluntary certifications and standards are another way to demonstrate the compliance with social requirements. Some of the many certifications and standards in this area include the ISO 26000, an international guideline for corporate social responsibility, environmental certifications such as the ISO 14001 or the Eco-Management and Audit Scheme. The SA 8000 standard, which demonstrates a company’s commitment to fair working conditions and ethical business practices, is also part of this field.2Helmold, M., Dathe, R., Dathe, T., Groß, D.-P. & Hummel, F. (2020). Corporate Social Responsibility im internationalen Kontext: Wettbewerbsvorteile durch nachhaltige Wertschöpfung. Springer Fachmedien Wiesbaden. https://doi.org/DOI: 10.1007/978-3-658-30899-5

The developments described are the reason for the high relevance that can be attributed to the SA 8000 standard. According to Social Accountability International (SAI), the international non-governmental organization (NGO) that developed the standard, it is the world’s leading certification program.6Social Accountability International. (n. d.-a). About SA 8000. Retrieved 03.08.2024 from https://sa-intl.org/programs/sa8000/ The standard is also significant because it was the first verifiable social standard aimed at promoting workers labor rights.7Gilbert, D. U., Rasche, A. & Waddock, S. (2011). Accountability in a Global Economy: The Emergence of International Accountability Standards. Business Ethics Quarterly, 21, 23-44. http://www.jstor.org/stable/25763050

1.2 Definition

The SA 8000 standard is defined as a “Standard and Certification System [that] provide[s] a framework for organizations of all types, in any industry, and in any country to conduct business in a way that is fair and decent for workers and to demonstrate their adherence to the highest social standards”.6Social Accountability International. (n. d.-a). About SA 8000. Retrieved 03.08.2024 from https://sa-intl.org/programs/sa8000/

The standard was developed by Social Accountability International, a global non-governmental organization that promotes respect for human rights in the workplace. The organization is formed by many different stakeholders, including NGOs, consulting firms and multinational companies.8Turzo, T., Montrone, A. & Chirieleison, C. (2024). Social accountability 8000: A quarter century review. Journal of Cleaner Production, 441, 140960. https://doi.org/10.1016/j.jclepro.2024.140960 SAI developed the standard based on the universal declaration of human rights and the conventions of the International Labour Organization and is supplemented by national labor laws from around the world.9Social Accountability International. (n. d.-f). SA8000: 2014 Standard. Retrieved 22.07.2024 from https://sa-intl.org/resources/sa8000-standard/

Companies aiming to be certified with the SA 8000 standard must meet certain requirements in the areas of child labor, forced labor, health and safety, freedom of association and the right to collective bargaining, discrimination, disciplinary practices, working hours and compensation. The degree of fulfilment is not verified by SAI, but by a third party.10Göbbels, M. & Jonker, J. (2003). AA1000 and SA8000 compared: a systematic comparison of contemporary accountability standards. Managerial Auditing Journal, 18, 54-58. https://doi.org/10.1108/02686900310454246 The current version of the standard was published in 2014. The content is outlined in a sixteen-page document which, in addition to an introduction describing the objectives, the scope and the management system, includes a section on various normative elements, definitions of the most important terms and the requirements of the standard, which make up the majority of the document.11Social Accountability International. (2014). Social Accountability 8000 International Standard. Retrieved 15.08.2024 from https://sa-intl.org/wp-content/uploads/2020/02/SA8000Standard2014.pdf

2 Background and in-depth assessment

In addition to describing the development of the SA 8000 standard, the following chapter analyzes the areas of application – both at a global and sectoral level. It also describes the requirements of the standard in more detail and distinguishes it from the ISO 26000 and the Corporate Sustainability Reporting Directive.

2.1 Historical background

The standard has its roots in a cooperation initiated in 1994 by the International Labour Organization and the Council of Economic Priorities (CEP). As a non-profit organization, CEP is dedicated to analyzing the social and environmental responsibility of companies. The cooperation aimed to reduce child labor and attracted the attention of many companies. Based on this reputation, the cooperation was expanded to include other stakeholders, and the goal was set to develop a standard that improves working conditions globally. On 15 October 1997, the SA 8000 standard was published by the Council on Economic Priorities Accreditation Agency, the multi-stakeholder initiative founded by the CEP. It was renamed SAI in 2000.12Chirieleison, C. & Rizzi, F. (2023). SA8000 Standard. In S. O. Idowu, R. Schmidpeter, N. Capaldi, L. Zu, M. Del Baldo, & R. Abreu (Eds.), Encyclopedia of Sustainable Management (pp. 2843-2849). Springer International Publishing. https://doi.org/DOI: 10.1007/978-3-031-25984-5 The standard has been revised several times. Revisions have taken place in 2001, 2004, 2008 and 2014. The current version is based on the latest 2014 revision.13Ćwiklicki, M. (2023). SA8000 Standard II. In S. O. Idowu, R. Schmidpeter, N. Capaldi, L. Zu, M. Del Baldo, & R. Abreu (Eds.), Encyclopedia of Sustainable Management (pp. 2850-2853). Springer international Publishing. https://doi.org/DOI: 10.1007/978-3-031-25984-5

2.2 Areas of application

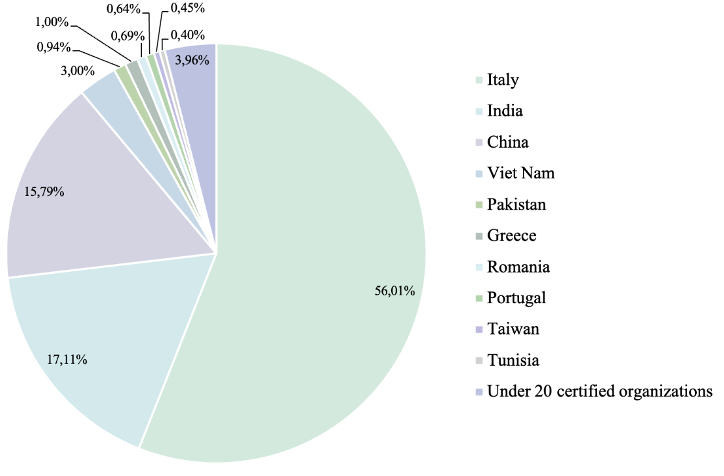

As of August 2024, 5504 facilities worldwide are certified with the SA 8000 standard. In the current year, 559 new certificates were issued and 654 facilities were recertified while 307 facilities cancelled their certification or allowed it to expire. In total, the certified facilities are spread across 52 countries and can be located in 69 different industries.14Social Accountability International. (n. d.-e). SA8000 Certified Organizations List. Retrieved 19.08.2024 from https://sa-intl.org/sa8000-search/

Source: Own elaboration based on Social Accountability International, n. d.-e

It is noteworthy that with 3083 certified organizations, more than half of the certificates were issued in Italy.14Social Accountability International. (n. d.-e). SA8000 Certified Organizations List. Retrieved 19.08.2024 from https://sa-intl.org/sa8000-search/ One reason for this strong dominance is that child labor and wages were a huge problem in Italy in the past.15Rasche, A. (2009). Toward a model to compare and analyze accountability standards – the case of the UN Global Compact. Corporate Social Responsibility and Environmental Management, 16, 192-205. https://doi.org/10.1002/csr.202 For this reason, the standard was strongly supported and promoted by the national and regional governments. As a result, the number of certified organizations in Italy is still very high.16Llach, J., Marimon, F. & Alonso-Almeida, M. D. M. (2015). Social Accountability 8000 standard certification: analysis of worldwide diffusion. Journal of Cleaner Production, 93, 288-298. https://doi.org/10.1016/j.jclepro.2015.01.044 In addition, there were various national incentives for certification to the standard in Italy, and cultural factors also spoke in favor of certification.17Ciliberti, F., Potrandolfo, P. & Scozzi, B. (2008). Logistics social responsibility: standard adoption and practices in Italian companies. International Journal of Production Economics, 113.

After Italy, the largest number of certified companies are located in India, China, Vietnam and Pakistan.14Social Accountability International. (n. d.-e). SA8000 Certified Organizations List. Retrieved 19.08.2024 from https://sa-intl.org/sa8000-search/ This distribution is due to the fact that poor working conditions are a key and widely recognized problem in these countries. For this reason, organizations in these countries try to use certification to demonstrate that their working conditions are good.15Rasche, A. (2009). Toward a model to compare and analyze accountability standards – the case of the UN Global Compact. Corporate Social Responsibility and Environmental Management, 16, 192-205. https://doi.org/10.1002/csr.202 As a result of this situation, the list of countries with certification organizations is dominated by developing countries. It can therefore be said that, with the exception of Italy, SA 8000 is mainly used in countries known for their poor working conditions.16Llach, J., Marimon, F. & Alonso-Almeida, M. D. M. (2015). Social Accountability 8000 standard certification: analysis of worldwide diffusion. Journal of Cleaner Production, 93, 288-298. https://doi.org/10.1016/j.jclepro.2015.01.044

Source: Own elaboration based on Social Accountability International, n. d.-e

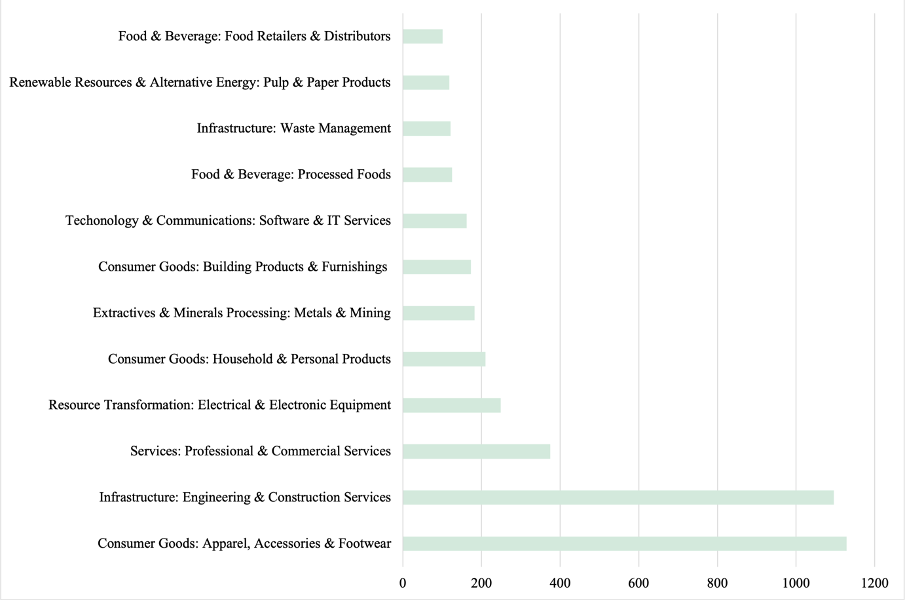

Looking at the distribution of certifications by sector, the consumer goods and infrastructure sectors stand out with 1128 and 1096 certifications respectively. This distribution can be explained by the fact that clothing, textiles and construction are particularly labor-intensive sectors where the standard is well applied. Apart from these two sectors, figure 2, which shows the sectors with over 20 certifications, shows that the distribution of certified companies is quite even, which shows the potential for cross-sectoral application.16Llach, J., Marimon, F. & Alonso-Almeida, M. D. M. (2015). Social Accountability 8000 standard certification: analysis of worldwide diffusion. Journal of Cleaner Production, 93, 288-298. https://doi.org/10.1016/j.jclepro.2015.01.044,14Social Accountability International. (n. d.-e). SA8000 Certified Organizations List. Retrieved 19.08.2024 from https://sa-intl.org/sa8000-search/

2.3 Requirements

The SA 8000 standard consists of nine requirements that are intended to ensure social standards and fair and safe working conditions in companies and their supply chains.

First, organizations are strictly prohibited from engaging in or supporting child labor. A child is defined as any person under the age of 15 unless local laws stipulate a higher age. To ensure this, companies must establish clear policies and procedures to address any instances of child labor. This includes that certified companies must also provide funds for the education of children who may lose their jobs as a result of this standard. In contrast, “young workers” are persons above the age of childhood but under the age of 18, who may be employed by companies. Secondly, forced and compulsory labor must not be used or supported in certified companies. Forced and compulsory labor refers to any involuntary work or service performed by a person, including any work performed under duress, threat, punishment, or as a means of paying off debts. Organizations may not retain workers’ identification documents or require workers to pay deposits. In addition, employees must have the freedom to leave their workplace premise after completing the standard workday.11Social Accountability International. (2014). Social Accountability 8000 International Standard. Retrieved 15.08.2024 from https://sa-intl.org/wp-content/uploads/2020/02/SA8000Standard2014.pdf

The third requirement for SA 8000 compliance is that companies must ensure basic standards for maintaining a safe and healthy working environment. This includes measures to prevent accidents and injuries as well as access to drinking water, sanitary facilities, suitable safety equipment at no cost to employees and the necessary safety training. Another requirement ensures that employees are entitled to form and join associations and engage in collective bargaining. Companies are prohibited from discriminating against employees who exercise these rights.11Social Accountability International. (2014). Social Accountability 8000 International Standard. Retrieved 15.08.2024 from https://sa-intl.org/wp-content/uploads/2020/02/SA8000Standard2014.pdf

Moreover, the standard prohibits any form of discrimination in employment, compensation, training, promotion, termination or retirement. This includes discrimination based on race, caste, national origin, religion, disability, gender, sexual orientation, trade union membership or political affiliation. Moreover, disciplinary measures involving corporal punishment, mental or physical duress, physical threats or verbal abuse are incompatible with the standard. All disciplinary measures should be fair and appropriate and not violate human rights.11Social Accountability International. (2014). Social Accountability 8000 International Standard. Retrieved 15.08.2024 from https://sa-intl.org/wp-content/uploads/2020/02/SA8000Standard2014.pdf

Another requirement of the SA 8000 is dedicated to its working hours. The working hours for employees of a company must be in accordance with national laws and industry standards. The maximum weekly working time is limited to 48 hours, break times must be provided and one day off per week must be guaranteed. In addition, overtime must be voluntary and should not exceed 12 hours per week or be regularly required. The SA 8000 also requires the payment of an appropriate remuneration, the so-called “living wage”, which means that the weekly wage paid must at least correspond to the legal or industry-specific minimum wage. The living wage should be sufficient to ensure the minimum needs of the employees and allow an additional amount for free disposal. Deductions from wages for disciplinary purposes are not allowed, unless permitted by law and agreed upon in a collective bargaining agreement.11Social Accountability International. (2014). Social Accountability 8000 International Standard. Retrieved 15.08.2024 from https://sa-intl.org/wp-content/uploads/2020/02/SA8000Standard2014.pdf

The final requirement of SA 8000 is to establish a management system that ensures the implementation, compliance and monitoring of the behavioral guidelines of the SA 8000. During the implementation the management system documents the status quo. Later any changes can be transparently recorded and subsequently communicated.11Social Accountability International. (2014). Social Accountability 8000 International Standard. Retrieved 15.08.2024 from https://sa-intl.org/wp-content/uploads/2020/02/SA8000Standard2014.pdf Chapter 3.2 explains the requirements and components of the management system in more detail.

2.4 Differentiation from other standards

In addition to the SA 8000, there are many other standards, certifications and guidelines in the field of corporate social responsibility. In the following section, the standard will be compared with the ISO 26000 standard and the Corporate Sustainability Reporting Directive (CSRD), as these two frameworks provide comprehensive, recognized guidelines for social responsibility and sustainability, they complement the SA 8000 standard in many ways.

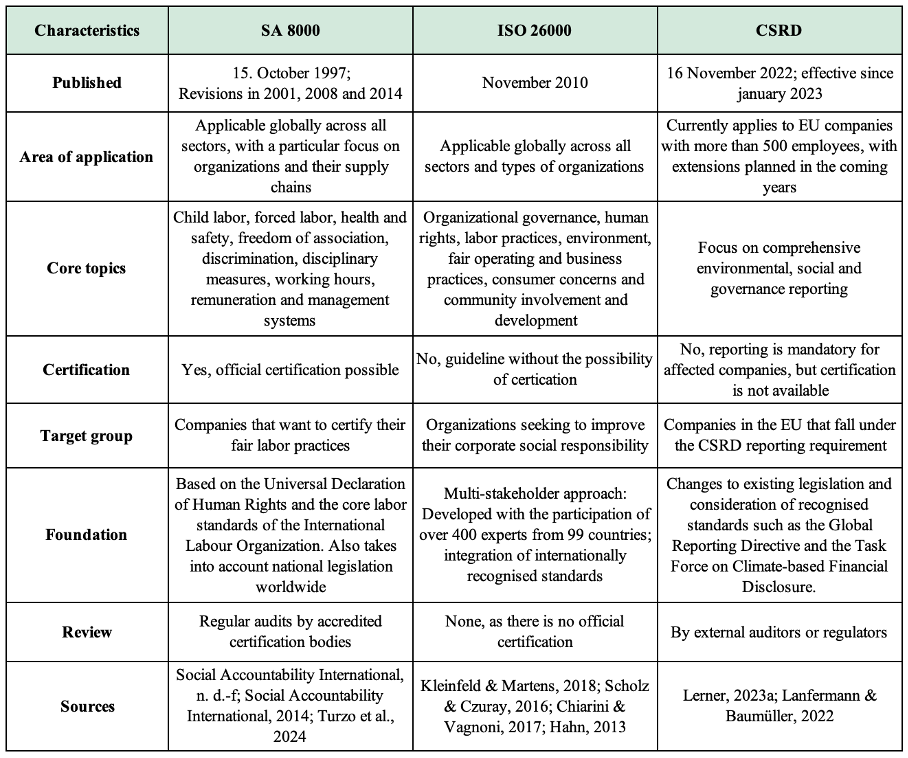

Table 1: Comparison of SA 8000, ISO 26000 and CSRD

Source: Own elaboration

The ISO 26000 is an international standard that provides guidance to companies and organizations on social responsibility. The standard was published in 2010 and covers the main topics human rights, labor practices, the environment, fair operations and business practices, consumer concerns and involvement as well as community development.18Kleinfeld, A. & Martens, A. (2018). CSR und Compliance im Kontext ihrer Bedeutungsentwicklung. In A. Kleinfeld & A. Martens (Eds.), CSR und Compliance: Synergien nutzen durch ein integriertes Management (pp. 3-35). Furthermore, the ISO 26000 was developed through a multi-stakeholder approach involving more than 400 experts from 99 countries.19Scholz, M. & Czuray, M. (2016). Die Normierung der gesellschaftlichen Verantwortung von Organisationen: ISO 26000 und ONR 192500. Springer Gabler.

Chiarini and Vagnoni (2017) have found through quantitative research that the ISO 26000 has a positive impact on the effectiveness of a company’s CSR system from a strategic perspective. The standard can therefore help to integrate CSR as part of the business strategy in the long term. SA 8000, by contrast, is more of a compliance strategy, where CSR is often seen as an obligation to meet external requirements, which can sometimes have a negative impact on strategic behavior.20Chiarini, A. & Vagnoni, E. (2017). Differences in implementing corporate social responsibility through SA8000 and ISO 26000 standards: research from European manufacturing. Journal of Manufacturing Technology Management,28.4, 438-457. https://www.emerald.com/insight/content/doi/10.1108/JMTM-12-2016-0170/full/pdf?title=differences-in-implementing-corporate-social-responsibility-through-sa8000-and-iso-26000-standards-research-from-european-manufacturing While ISO 26000 focuses on the environment, social issues and governance, SA 8000 focuses only on social issues.21Hahn, R. (2013). Zur Normierung gesellschaftlicher Verantwortung ISO 26000 im analytischen Vergleich mit ISO 14000 und SA8000/Standardizing Social Responsibility – Comparing ISO 26000 with ISO 14000 and SA8000. Journal for Business, Economics and Ethics, 14 (3), 378 – 400. In addition, ISO 26000 considers the needs of customers as stakeholders, whereas SA 8000 tends to neglect them. Furthermore, SA 8000 considers and positively impacts supply chain management, whereas ISO 26000 is used more for internal purposes and does not consider the supply chain20Chiarini, A. & Vagnoni, E. (2017). Differences in implementing corporate social responsibility through SA8000 and ISO 26000 standards: research from European manufacturing. Journal of Manufacturing Technology Management,28.4, 438-457. https://www.emerald.com/insight/content/doi/10.1108/JMTM-12-2016-0170/full/pdf?title=differences-in-implementing-corporate-social-responsibility-through-sa8000-and-iso-26000-standards-research-from-european-manufacturing

However, the main difference between the two standards is that ISO 26000 is not certifiable. Although there are certifiable national standards, for example in Brazil, Spain and Denmark, which are based on the standard, certification is not actually intended. The purpose of the ISO 26000 standard is to create a common understanding of social responsibility and to promote it in companies and organizations, not to officially certify its implementation. In contrast, certification is a central feature of the SA 8000 standard.21Hahn, R. (2013). Zur Normierung gesellschaftlicher Verantwortung ISO 26000 im analytischen Vergleich mit ISO 14000 und SA8000/Standardizing Social Responsibility – Comparing ISO 26000 with ISO 14000 and SA8000. Journal for Business, Economics and Ethics, 14 (3), 378 – 400.

The CSRD is a Directive that was published in 2022. When it came into force in January 2023, companies were given 18 months to implement its requirements. The CSRD focuses on environmental, social and governance issues.22Lerner, M. (2023a). Die Corporate Sustainability Reporting Directive (CSRD). In M. Lerner (Ed.), Einfluss der EU-Taxonomie auf den Mittelstand (pp. 59-70). Springer Gabler.

Unlike the SA 8000 standard, the CSRD is not applied globally, but only by companies in the European Union. While currently only companies with more than 500 employees are required to implement it, from 2025 companies with more than 250 employees, a turnover of more than 40 million € and/or a balance sheet total of more than 20 million € will also be required to do so. From 2026, the reporting obligation will also apply to small and medium-sized enterprises and listed companies.23Europäische Union. (2022). Richtlinie (EU) 2022/2464 des europäischen Parlaments und des Rates. https://eur-lex.europa.eu/legal-content/DE/TXT/PDF/?uri=CELEX:32022L2464&from=DE Despite this extension of reporting requirements, the CSRD has a much narrower scope than the SA 8000 standard. Despite these differences the CSRD is much more widespread because of the reporting requirement. In the future, approximately 49,000 companies in the EU will be subject to the CSRD. Although the SA 8000 standard can be applied by more companies due to its global orientation, there are currently only 5504 certified companies.24Lanfermann, G. & Baumüller, J. (2022). Die Endfassung der Corporate Sustainability Reporting Directive. DER BETRIEB, 47/2022, 2745-2755.,14Social Accountability International. (n. d.-e). SA8000 Certified Organizations List. Retrieved 19.08.2024 from https://sa-intl.org/sa8000-search/ The large difference in the number of participating companies can be explained by the fact that, unlike the SA 8000 standard, the Directive is mandatory and not voluntary.

In summary, the comparison between SA 8000, ISO 26000 and CSRD shows that although all three deal with aspects of corporate social responsibility, they differ greatly in their application and objectives. While the SA 8000 focuses more on compliance and leads to certification, which companies can use to communicate their efforts in this area to the outside world, ISO 26000 is a voluntary standard designed to help companies with their internal organization. The CSRD differs from the others in that it requires a commitment from specific companies. Unlike the other two, it therefore represents a demand for greater transparency on CSR at government level.

3 Practical implementation

The following chapter discusses the practical implementation of SA 8000 in companies. Firstly, the certification process that a company goes through is explained. Next, the management system required by the standard is discussed, which helps companies to successfully implement the social conditions. Finally, both a successful and an unsuccessful example of the implementation of SA 8000 is given.

3.1 Certification process

Source: Own illustration based on Chirieleison & Rizzi, 2023; Social Accountability International, n. d.-d

The SA 8000 certification process can be divided into six main steps that are partially supported by two specific SAI tools. The first tool – and therefore the first step towards the certification – is the self-assessment of the company. This step is designed to help the company become more familiar with the content and requirements of the standard and to assess the extent to which the company already meets the requirements of SA 8000. It is also intended to show what improvements are needed in advance to have a chance of certification. This step is supported by SAI’s Social Fingerprint system, which provides an up-to-date assessment of the level of implementation of SA 8000 issues within the organization. The Social Fingerprint is designed to help organizations measure their current implementation status and increase their understanding of SA 8000 management systems.26Social Accountability International. (2020). SAI Database (Phase 1) Instructions for SA8000 Clients. Retrieved 06.08.2024 from https://sa-intl.org/wp-content/uploads/2020/07/SA8000-Database-Client-Instructions_EN-Update-July-2020.pdf The self-assessment takes approximately 60 to 90 minutes.25Social Accountability International. (n. d.-d). SA8000 Certification: Getting Started. Retrieved 06.08.2024 from https://sa-intl.org/resources/sa8000-getting-started/

The second step is for the company to select and contact one of about thirty certification bodies.27Social Accountability International. (n. d.-b). SA8000 Accredited Certification Bodies. Retrieved 12.08.2024 from https://sa-intl.org/resources/sa8000-accredited-certification-bodies/ This is the start of the official certification process. In the third step, the selected certification body conducts a pre-audit, based on a site visit, to assess the company’s readiness to be certified to the standard. This step takes one to two days.25Social Accountability International. (n. d.-d). SA8000 Certification: Getting Started. Retrieved 06.08.2024 from https://sa-intl.org/resources/sa8000-getting-started/

After a successful pre-audit, companies then undergo the full certification audit in the fourth stage. This takes between two and ten days, depending on the size and scope of the company. The second SAI tool is used in this step. The independent assessment is a review of the maturity of the system in the company and is designed to help identify strengths and weaknesses. The application of both tools – the self-assessment and the independent assessment – then results in a score that shows the maturity level of the company on a rating chart, which should help the company to draw up a plan for future adjustments. The scale ranges from 1 (no awareness) to 5 (created and executed a fully developed management system).28Social Accountability International. (n. d.-h). Social Fingerprint. Retrieved 05.08.2024 from https://sa-intl.org/services/social-fingerprint/ In addition to working practices, individual employee opinions and other key components of the company’s internal processes are also taken into account during the independent assessment. Finally, the points resulting from the analysis are used to draw up recommendations for action that the companies must implement in order to achieve official certification.25Social Accountability International. (n. d.-d). SA8000 Certification: Getting Started. Retrieved 06.08.2024 from https://sa-intl.org/resources/sa8000-getting-started/

Once these recommendations have been implemented, the fifth step of the certification process follows. After the certification body has reviewed and approved the adjustments, the official certificate is issued for a period of three years. The sixth step involves the monitoring of companies during the certification period. This includes announced and unannounced visits to the company by the certification bodies at intervals of about six months. At the end of the three-year period, companies can choose to be recertified.12Chirieleison, C. & Rizzi, F. (2023). SA8000 Standard. In S. O. Idowu, R. Schmidpeter, N. Capaldi, L. Zu, M. Del Baldo, & R. Abreu (Eds.), Encyclopedia of Sustainable Management (pp. 2843-2849). Springer International Publishing. https://doi.org/DOI: 10.1007/978-3-031-25984-5

The costs associated with official certification vary greatly depending on the companies’ size and scope as well as the certification body. While $300 is set for self-assessment, the cost of the official certification cycle is approximately $400 to $1500 per day, according to the SAI.29Social Accountability International. (n. d.-c). SA8000 Certification Costs. Retrieved 08.08.2024 from https://sa-intl.org/resources/sa8000-certification-costs/ These costs depend on location and market prices. In addition to direct payments to the SAI and certification bodies, there are also internal costs for companies. Depending on the status of the company, these costs may be incurred before the certification cycle for preventive measures or initial adjustments, or during the certification cycle to correct processes that were criticized during the official certification and need to be improved. In addition to these costs, there are also administrative costs for the companies.30Olejniczak-Szuster, K. (2019). The Implementation of the SA8000 Standard by Contemporary Enterprises. Problemy Zarządzania, 17.2 (82), 170-185. https://doi.org/http://dx.doi.org/10.7172/1644-9584.82.9 As all costs depend on the company and the certification body, it is not possible to quantify the final cost to a company, but it can be said that the certification process as a whole requires a high level of investment.31Stigzelius, I. & Mark-Herbert, C. (2009). Tailoring corporate responsibility to suppliers: Managing SA8000 in Indian garment manufacturing. Scandinavian Journal of Management, 25, 46-56.https://doi.org/10.1016/j.scaman.2008.04.003

3.2 Implementation of management system

The most important implementation tool of SA 8000 can already be found in the standard itself. Implementing a management system is the final requirement of the SA 8000:2014 standard. The management system outlines a comprehensive framework for organizations to follow in order to comply with social accountability standards. This framework focuses not only on meeting standards, but also on continuously improving the social performance of organizations. The management system includes ten important key components.

The first key component of the management system is the development and implementation of policies, procedures and records. An important aspect here is a policy statement drafted by senior management that explicitly declares the organization’s commitment to the SA 8000 standard. It must be effectively communicated throughout the organization in all relevant languages to ensure that every employee understands the commitment. In addition, the organization is responsible for maintaining comprehensive documentation that demonstrates ongoing compliance with SA 8000 standards and for conducting regular management reviews to improve performance.11Social Accountability International. (2014). Social Accountability 8000 International Standard. Retrieved 15.08.2024 from https://sa-intl.org/wp-content/uploads/2020/02/SA8000Standard2014.pdf

Additionally, another key aspect of the management system is the establishment of a social performance team (SPT). This team should consist of a balanced representation of management and employee representatives. The primary role of the SPT is to oversee the implementation of all elements of SA 8000. This includes ensuring that the organization’s practices are consistent with the standard’s requirements and that workers’ rights are protected. While senior management bears the ultimate responsibility for compliance with the standard, the SPT serves as an operational body that facilitates active collaboration between workers and management and promotes transparency and accountability throughout the organization.11Social Accountability International. (2014). Social Accountability 8000 International Standard. Retrieved 15.08.2024 from https://sa-intl.org/wp-content/uploads/2020/02/SA8000Standard2014.pdf An important task of the SPT is the identification and assessment of risks. This is realized by conducting regular written risk assessments to identify areas of potential or actual non-conformance to the SA 8000 standard. Based on their findings, the SPT recommends actions to mitigate these risks, prioritizing them based on severity and potential impact on worker welfare. The SPT is also responsible for monitoringworkplace activities to ensure compliance with SA 8000, implementing measures based on risk assessment and ensuring the effectiveness of these measures and systems. Moreover, the SPT gathers information from stakeholders and works with departments to resolve non-conformities. Furthermore, the SPT conducts routine internal audits, reports to management on compliance activities and documents corrective actions.11Social Accountability International. (2014). Social Accountability 8000 International Standard. Retrieved 15.08.2024 from https://sa-intl.org/wp-content/uploads/2020/02/SA8000Standard2014.pdf

Another important feature of the management system is the internal involvement and communication. Organizations must actively involve employees and ensure that they understand the requirements of SA 8000 through regular communication and training. Moreover, companies are required to implement a system for their complaint and resolution management.Organizations must establish a written complaint management procedure that is accessible to all employees and interested parties. This procedure should be confidential, unbiased and non-retaliatory, allowing employees to report complaints or non-conformance issues without fear of retribution. The outcomes of complaint investigations should be communicated transparently to ensure that corrective action are implemented and that all parties are informed of the resolution process.11Social Accountability International. (2014). Social Accountability 8000 International Standard. Retrieved 15.08.2024 from https://sa-intl.org/wp-content/uploads/2020/02/SA8000Standard2014.pdf

Furthermore, the external verification and stakeholder engagement plays a significant role in the management system of the SA 8000. Organizations are expected to fully cooperate with external auditors during both announced and unannounced audits to verify compliance with SA 8000. These audits assess the severity and frequency of any issues that arise and ensure that corrective measures are being effectively implemented. Additionally, active engagement with stakeholders, including workers, trade unions and other interested parties, is essential to achieve and sustain compliance with the standard. Also, organizations must establish policies and procedures for the implementation of corrective and preventive actions. Here, the SPT has a crucial part in ensuring that these actions are carried out effectively by maintaining detailed records that document non-conformities, root causes and the results of corrective actions. Another fundamental component of the management system is the implementation of a training and capacity building plan. The training plan is designed to equip personnel with the requisite knowledge and skills to ensure compliance with SA 8000 standards based on the result if the risk assessments.11Social Accountability International. (2014). Social Accountability 8000 International Standard. Retrieved 15.08.2024 from https://sa-intl.org/wp-content/uploads/2020/02/SA8000Standard2014.pdf

At last, the management of suppliers and subcontractors is another fundamental requirement. Organizations must ensure that these partners comply with SA 8000 standards, particularly regarding labor rights and ethical practices. The due diligence involves assessing risks within the supply chain and implementing monitoring activities to track compliance. Organizations should work with suppliers to address significant risks and ensure that all workers, including those employed by subcontractors, enjoy protections equivalent to those afforded to direct employees.11Social Accountability International. (2014). Social Accountability 8000 International Standard. Retrieved 15.08.2024 from https://sa-intl.org/wp-content/uploads/2020/02/SA8000Standard2014.pdf

Once the SA 8000 standard has been successfully implemented, it can have various practical consequences for the company. As the SA 8000 focuses exclusively on social labor conditions, it is not possible for companies to fully and effectively implement their entire CSR strategy in line with SA 8000. However, the standard significantly supports the management of CSR within the supply chain by setting specific requirements and standards for labor conditions. In addition, the SA 8000 helps companies to develop detailed Key Performance Indicators (KPIs) that are used to ensure compliance with and improvement of social standards. These KPIs make it possible to monitor performance and demonstrate compliance with the standard through external audits.20Chiarini, A. & Vagnoni, E. (2017). Differences in implementing corporate social responsibility through SA8000 and ISO 26000 standards: research from European manufacturing. Journal of Manufacturing Technology Management,28.4, 438-457. https://www.emerald.com/insight/content/doi/10.1108/JMTM-12-2016-0170/full/pdf?title=differences-in-implementing-corporate-social-responsibility-through-sa8000-and-iso-26000-standards-research-from-european-manufacturing

In conclusion, the SA 8000 standard itself can be seen as an objective that companies should aim for. The management system gives a framework with a step-by-step guide how companies can achieve this.11Social Accountability International. (2014). Social Accountability 8000 International Standard. Retrieved 15.08.2024 from https://sa-intl.org/wp-content/uploads/2020/02/SA8000Standard2014.pdf However, it is also evident in the literature, that there are no alternative tools or measures described that can be used to implement the SA 8000.

3.3 Best practice

The next chapter discusses best practice examples. However, in the literature there are no case studies that deal specifically with the successful implementation of SA 8000 at one company. Therefore, the following section examines the general factors that have contributed to a successful implementation and provides a practical example.

A study conducted by Ciliberti et al. (2009) analyzed the experiences of small and medium enterprises (SME) with the implementation of the SA 8000 standard. In particular the study looked at how the often lower bargaining power of smaller companies affects the implementation of the SA 8000 along the supply chain. It was found that the implementation of the SA 8000 was successful when the dominant player in the supply chain (chain director) initiated the implementation of SA 8000. When SMEs with less bargaining power in the supply chain initiated the implementation of the SA 8000, they were often not successful because they lacked power over their suppliers. Often these companies found other ways to ensure humane working conditions without implementing SA 8000 .32Ciliberti, F., de Groot, G., de Haan, J. & Pontrandolfo, P. (2009). Codes to coordinate supply chains: SMEs’ experiences with SA8000. Supply Chain Management: An International Journal, 14. https://doi.org/10.1108/13598540910941984

A practical example of this dynamic can be observed in the case of Walmart and their supplier Tropical Cheese. This example is presented on the website of the SAI and is therefore also used for promotional purposes. Therefore, given statements can only be used as individual example with limited to non representative value as they are not the result of scientific research.

Tropical Cheese, headquartered in New Jersey, produces and distributes a variety of dairy products, such as soft cheese and yogurt. The company primarily targets Mexican, Caribbean and Central and South American consumers. Tropical Cheese was first certified with the SA 8000 standard in 2018 and recertified in 2022.33Social Accountability International. (2023). SA8000 Spotlight: Worker Engagement with Tropical Cheese. Retrieved 06.08.2024 from https://sa-intl.org/sa8000-spotlight-worker-engagement-with-tropical-cheese/ The company became interested in SA 8000 certification because one of its largest customers, Walmart, decided in 2018 to transition from their own social compliance audits to third-party social schemes, including SA 8000.34Social Accountability International. (n. d.-g). SA 8000 & Walmart. Retrieved 12.08.2024 from https://sa-intl.org/resources/sa8000-and-walmart/ Therefore, Tropical Cheese’s motivation for certification was largely driven by the chain director’s (Walmart’s) demand for certification. This demonstrates the critical role that powerful stakeholders, such as chain directors, play in encouraging companies to adopt and successfully implement social responsibility standards such as SA 8000.32Ciliberti, F., de Groot, G., de Haan, J. & Pontrandolfo, P. (2009). Codes to coordinate supply chains: SMEs’ experiences with SA8000. Supply Chain Management: An International Journal, 14. https://doi.org/10.1108/13598540910941984

The SA 8000 certification itself has affected Tropical Cheese in various aspects. Firstly, Tropical Cheese already had many structures and management systems related to social performance in place. However, these were often quite informal. The SA 8000 certification helped Tropical Cheese formalize their processes and elevate their existing structures. For example, through SA 8000, routine department meetings are held to facilitate regular exchanges between management and employees regarding health, safety and productivity improvements. This ultimately led to improved communication with employees and strengthened procedures.33Social Accountability International. (2023). SA8000 Spotlight: Worker Engagement with Tropical Cheese. Retrieved 06.08.2024 from https://sa-intl.org/sa8000-spotlight-worker-engagement-with-tropical-cheese/

3.4 Worst practice

One of the most serious accidents in connection with the SA 8000 was a fire in 2012 in Pakistan. On September 11, 2012, a devastating fire occurred at the Ali Enterprises textile factory in Karachi, Pakistan, claiming over 250 lives. This event is particularly noteworthy because it occurred just three weeks after the factory was certified to the SA 8000 standard by the Italian auditing firm RINA. Naturally, this led to criticism of how the certification was obtained and the effectiveness of the SA 8000 standard in ensuring safe working conditions.35Rafay, A. (2024). Baldia Factory Fire Tragedy: A Black Spot for Workplace Safety Standards in Pakistan. Workplace & Health 72(2), 61-67. https://www.researchgate.net/publication/378039489_Baldia_Factory_Fire_Tragedy_A_Black_Spot_for_Workplace_Safety_Standards_in_Pakistan

The incident was among the most tragic workplace fires in the world, primarily caused by poor compliance with safety laws and ineffective safety inspections. Contributing factors included illegal construction, unregistered infrastructure, a lack of escape routes, and the nonavailability of safety equipment such as locked exit doors, grilled windows, and an inaccessible basement. As a result of the fire 259 workers died, 40 workers were seriously injured and 150 workers suffered minor injuries. Out of the total casualties, 122 workers were between the ages of 16 and 22.35Rafay, A. (2024). Baldia Factory Fire Tragedy: A Black Spot for Workplace Safety Standards in Pakistan. Workplace & Health 72(2), 61-67. https://www.researchgate.net/publication/378039489_Baldia_Factory_Fire_Tragedy_A_Black_Spot_for_Workplace_Safety_Standards_in_Pakistan

The SA 8000 certification ensures the upholding of “[…] a safe and healthy workplace environment and shall take effective steps to prevent potential health and safety incidents and occupational injury or illness arising out of, associated with or occurring in the course of work. It shall minimise or eliminate, so far as is reasonably practicable, the causes of all hazards in the workplace environment, based upon the prevailing safety and health knowledge of the industry sector and of any specific hazards”.11Social Accountability International. (2014). Social Accountability 8000 International Standard. Retrieved 15.08.2024 from https://sa-intl.org/wp-content/uploads/2020/02/SA8000Standard2014.pdf In the present case, the company did not comply with these standards, despite certification.35Rafay, A. (2024). Baldia Factory Fire Tragedy: A Black Spot for Workplace Safety Standards in Pakistan. Workplace & Health 72(2), 61-67. https://www.researchgate.net/publication/378039489_Baldia_Factory_Fire_Tragedy_A_Black_Spot_for_Workplace_Safety_Standards_in_Pakistan

The Clean Clothes Campaign (CCC), which is an international alliance of non-governmental organizations, trade unions and other stakeholders working to improve working conditions in the global garment industry has been highly critical of SA 8000 and social standards in the wake of the incident.36Clean Clothes Campaign. (2020). Faulty Pakistan factory audit: Italian social auditor RINA yet again disregards families harmed by textile factory fire. Retrieved 10.08.2024 from https://cleanclothes.org/news/2020/faulty-pakistan-factory-audit-italian-social-auditor-rina-yet-again-disregards-families-harmed-by-textile-factory-fire- According to the CCC the Ali Enterprises fire in Karachi is a strong illustration of the failures within the social auditing sector, specifically highlighting how auditing firms may prioritize corporate profits over the welfare of workers. As this incident underscores deep-rooted issues in the industry that compromise the integrity of social audits. An investigative analysis of RINA’s operational methods revealed that, despite claims of aiming to enhance working conditions in the clothing sector, the firm has often favoured financial gain over meaningful improvements in labor standards. To address these deficiencies, the CCC demand a comprehensive overhaul of the entire social auditing system, emphasizing significantly enhanced transparency and establishing strict legal accountability for audit practices. This reform is crucial to ensure that social audits genuinely benefit the workforce they purport to protect.36Clean Clothes Campaign. (2020). Faulty Pakistan factory audit: Italian social auditor RINA yet again disregards families harmed by textile factory fire. Retrieved 10.08.2024 from https://cleanclothes.org/news/2020/faulty-pakistan-factory-audit-italian-social-auditor-rina-yet-again-disregards-families-harmed-by-textile-factory-fire-

Another major point of criticism was the organization of the accreditation itself. It was not the SAI, who conducted the inspections themselves. Instead, those on-site audits were normally carried out by a third parties, so called “certification bodies”. The Social Accountability Accreditation Services (SAAS), accredits these external certification bodies.37Clean Clothes Campaign. (2018). Time Line of the Ali Enterprises Case. Retrieved 10.08.2024 from https://cleanclothes.org/file-repository/safety-ali-enterprises-time-line-for-the-ali-enterprises-case/@@download/file/Ali%20Time%20Line%20Public%20version%20-%20Final.pdf The certification of Ali Enterprises was carried out by the certification body RINA Services S.p.A. from Italy. However, RINA never actually visited the site themselves. Instead they subcontracted the audit to RI&CA.38European Center for Constitutional and Health. (2016). RINA certifies safety before factory fire in Pakistan. https://www.ecchr.eu/fileadmin/Fallbeschreibungen/CaseReport_KiK_RINA_December2020.pdf However, RI&CA is not accredited by SAAS itself and has a controversial reputation, because the company has a high approval rate in Pakistan.37Clean Clothes Campaign. (2018). Time Line of the Ali Enterprises Case. Retrieved 10.08.2024 from https://cleanclothes.org/file-repository/safety-ali-enterprises-time-line-for-the-ali-enterprises-case/@@download/file/Ali%20Time%20Line%20Public%20version%20-%20Final.pdf

In conclusion this incidence exposed the weakness of factory monitoring systems of international auditing groups as the system can be used to obtain the desired approval of safety standards in suppliers without actually fulfilling the requirements.35Rafay, A. (2024). Baldia Factory Fire Tragedy: A Black Spot for Workplace Safety Standards in Pakistan. Workplace & Health 72(2), 61-67. https://www.researchgate.net/publication/378039489_Baldia_Factory_Fire_Tragedy_A_Black_Spot_for_Workplace_Safety_Standards_in_Pakistan

4 Drivers & barriers

The implementation process of the SA 8000 is influenced by several internal and external drivers and barriers. In this part of the wiki the drivers for certification will be explained first. The certification’s barriers will be explained after that.

4.1 Drivers for certification

The adoption of the SA 8000 can be driven by a combination of internal and external factors, first the external drivers will be examined. After that, the internal drivers will be looked at.

External drivers

A primary motivator for companies to adopt the SA 8000 standard is to meet client requests. Koster et al. (2019) state that customer-related factors are often important when companies choose to apply this standard. Adapting to the standard is typically seen as the minimum requirement to gain the trust of suppliers, for instance, for global exporting countries trading with large European or American buyers.39Marcuzzi, I., Podrecca, M., Sartor, M. & Nassimbeni, G. (2023). Out of social accountability: Reasons and alternative paths for SA8000 decertification. Corporate Social Responsibility and Environmental Management, 30, 3140-3158. https://doi.org/10.1002/csr.2543,40Murmura, F. & Bravi, L. (2020). Developing a Corporate Social Responsibility Strategy in India Using the SA 8000 Standard. Sustainability, 12, 3481. https://doi.org/10.3390/su12083481,31Stigzelius, I. & Mark-Herbert, C. (2009). Tailoring corporate responsibility to suppliers: Managing SA8000 in Indian garment manufacturing. Scandinavian Journal of Management, 25, 46-56.https://doi.org/10.1016/j.scaman.2008.04.003 In fact, according to a study conducted in Thailand by Rohitratana (2002) the lack of this norm would make it very difficult for local companies to interact with foreign companies. This suggests that the supplier may have a limited perspective on the SA 8000, mainly given by the fear of not meeting the customer’s requirements. Therefore, it may not be seen as an opportunity to improve the performance of the company.41Koster, M., Vos, B. & Van Der Walk, W. (2019). Drivers and barriers for adoption of a leading social management standard (SA8000) in developing economies. International Journal of Physical Distribution & Logistics Management, 49, 534-551. https://doi.org/10.1108/IJPDLM-01-2018-0037

Another external driver that may lead companies to the implementation of the standard is the desire to enhance their corporate image and the reputation of its company. It can be argued that the standard serves as a type of “social stamp” that enables the company to project a more reassuring image to stakeholders and therefore win the trust of those who are involved with the company, whether directly or indirectly.42Santos, G., Murmura, F. & Bravi, L. (2018). SA 8000 as a Tool for a Sustainable Development Strategy. Corporate Social Responsibility and Environmental Management, 25, 95-105. https://doi.org/10.1002/csr.1442 Therefore, the implementation can lead to reducing reputational risks and sending a positive signal to the financial market about the adoption of CSR measures, regardless of how fully the policies are internalized within the company.43Boiral, O., Heras‐Saizarbitoria, I. & Testa, F. (2017). SA8000 as CSR‐Washing? The Role of Stakeholder Pressures. Corporate Social Responsibility and Environmental Management, 24, 57-70. https://doi.org/10.1002/csr.1391

Furthermore, the pressure from certain stakeholders can lead to the implementation of standards, such as the SA 8000.44Lannelongue, G. & González-Benito, J. (2012). Opportunism and environmental management systems: Certification as a smokescreen for stakeholders. Ecological Economics, 82, 11-22. https://doi.org/10.1016/j.ecolecon.2012.08.003 Implementing the SA 8000 standard can therefore lead to a positively influenced stakeholder relationship. Gilbert & Rasche (2008) stated that the certification of this standard can positively shape the dialogue with stakeholders, including suppliers and customers.

From a supply chain perspective, implementing SA 8000 can significantly reduce information asymmetries by improving transparency into labor conditions. This transparency can ensure that all parties within the supply chain understand and follow these standards, making interactions easier and more transparent. Consequently, the adoption of the SA 8000 can not only help companies shape the dialogue with stakeholders but also help improve the overall efficiency and ethical compliance of their supply chains.32Ciliberti, F., de Groot, G., de Haan, J. & Pontrandolfo, P. (2009). Codes to coordinate supply chains: SMEs’ experiences with SA8000. Supply Chain Management: An International Journal, 14. https://doi.org/10.1108/13598540910941984

In addition to an improved stakeholder relationship another essential driver can be incentives and legislations by national governments. As previously indicated, the majority of businesses adopting the SA 8000 standard globally, are in Italy. Beyond all other factors, this has to do with the availability of regional and local incentives provided by the Italian government. This can be seen as one of the main drivers for Italian companies. Therefore, it may be argued that Italian law encourages certification because it gives complying companies tax incentives.45Murmura, F., Bravi, L. & Palazzi, F. (2017). Evaluating companies’ commitment to corporate social responsibility: Perceptions of the SA 8000 standard. Journal of Cleaner Production, 164, 1406-1418. https://doi.org/10.1016/j.jclepro.2017.07.073

Lastly, one external driver can be recognized in financial areas. SA 8000 certification is expected to make it easier for companies to get a reasonable credit score by improving their relationship with financial institutions. Moreover, companies complying with the SA 8000 are likely to attract more investors, similar to the benefits seen with other sustainability certifications like the ISO 14001.46Sartor, M., Orzes, G., Di Mauro, C., Ebrahimpour, M. & Nassimbeni, G. (2016). The SA8000 social certification standard: Literature review and theory-based research agenda. International Journal of Production Economics,175, 164-181. https://doi.org/10.1016/j.ijpe.2016.02.018 Even though this benefit is expected, it has not been empirically verified yet.

Internal drivers

Despite the fact that when a company is asked why it chose to become certified with this standard, its external benefits, such as improving its corporate image, are frequently mentioned first.47Welford, R., Meaton, J. & Young, W. (2003). Fair trade as a strategy for international competitiveness. International Journal of Sustainable Development & World Ecology, 10, 1-13. https://doi.org/10.1080/13504500309469781 Businesses can also have a sincere desire to change their internal workspaces or to enhance their corporate values. Turzo et al. (2024) found different internal drivers companies face while considering whether to implement the SA 8000 standard.

The first internal driver is an increasement in workplace productivity. Some studies claim that the adoption of the SA 8000 can lead to reduced workplace risks, better trained employees and an increasing employee motivation which then can lead to an overall increasement of workplace productivity.40Murmura, F. & Bravi, L. (2020). Developing a Corporate Social Responsibility Strategy in India Using the SA 8000 Standard. Sustainability, 12, 3481. https://doi.org/10.3390/su12083481,45Murmura, F., Bravi, L. & Palazzi, F. (2017). Evaluating companies’ commitment to corporate social responsibility: Perceptions of the SA 8000 standard. Journal of Cleaner Production, 164, 1406-1418. https://doi.org/10.1016/j.jclepro.2017.07.073,42Santos, G., Murmura, F. & Bravi, L. (2018). SA 8000 as a Tool for a Sustainable Development Strategy. Corporate Social Responsibility and Environmental Management, 25, 95-105. https://doi.org/10.1002/csr.1442 This aspect is especially seen in developing countries implementing this standard as Orzes et al. (2017)examined in their study.

Additionally, an important internal driver for companies to implement the SA 8000 standard is the potential enhancement of the working environment. By adapting to the standard, companies aim to reduce risks through improved working conditions, worker training and increased employee participation. For some companies this includes providing safety equipment or training workers in first aid. This can help companies to have fewer worker accidents and a reduced risk of labor law violations.42Santos, G., Murmura, F. & Bravi, L. (2018). SA 8000 as a Tool for a Sustainable Development Strategy. Corporate Social Responsibility and Environmental Management, 25, 95-105. https://doi.org/10.1002/csr.1442 Furthermore, this improved working environment may strengthen the relationship between the company and its employees, leading to better communication and collaboration. In the garment industry, where labor turnover rates, so the rate at which employees leave the company and are replaced by other employees, are typically high, improving the working environment is a strategic move. Companies hope to reduce turnover rates over time with these improvements, ultimately creating a more stable and productive workforce.31Stigzelius, I. & Mark-Herbert, C. (2009). Tailoring corporate responsibility to suppliers: Managing SA8000 in Indian garment manufacturing. Scandinavian Journal of Management, 25, 46-56.https://doi.org/10.1016/j.scaman.2008.04.003

As noted by Marcuzzi et al. (2023) in their examination of SA 8000 drivers and barriers, companies also use the standard as a platform to demonstrate their moral values as opposed to simply adapting it as a marketing tool. The implementation of such a standard can be driven by an individual’s personal beliefs, depending on their role in the company and their ability to influence organizational structures.48Hemingway, C. A. & Maclagan, P. W. (2004). Managers’ Personal Values as Drivers of Corporate Social Responsibility. Journal of Business Ethics, 50, 33-44. https://doi.org/10.1023/B:BUSI.0000020964.80208.c9 For managers, adopting the SA 8000 can reflect their personal values, demonstrating their commitment to social responsibility that can further motivate and link the organization’s goals with these principles.

However, despite the presence of internal drivers among some companies, Koster et al. (2019) highlights in his study that these motivations are relatively rare and the majority of companies adopt the standard primarily for other reasons.

4.2 Barriers for certification

The certification process of the SA 8000 standard is hindered by several external and internal barriers, which impact the adoption of the standard across various industries and regions. First off, the external barriers will be examined. Afterwards the internal barriers will be discussed.

External barriers

The difficulties in the buyer-supplier relationship are one of the main obstacles in the implementation of the SA 8000 standard. As mentioned before customers’ expectations are frequently the main reason for the standard’s adoption. Multinational corporations frequently mandate SA 8000 compliance from suppliers, yet they often do so without considering the impact on those suppliers. These businesses are unwilling to pay extra for goods from approved suppliers, placing a higher priority on lead time and pricing. In order to satisfy these demands, SME´s may turn to simplified compliance strategies or give false information, which ultimately has the impact of undermining the norm.41Koster, M., Vos, B. & Van Der Walk, W. (2019). Drivers and barriers for adoption of a leading social management standard (SA8000) in developing economies. International Journal of Physical Distribution & Logistics Management, 49, 534-551. https://doi.org/10.1108/IJPDLM-01-2018-0037 Furthermore, Stigzelius and Mark-Herbert (2009) found that one significant barrier to implementing labor standards like SA 8000 is the lack of external incentives due to the uncertainty of future orders. Buyers may require suppliers to meet certain standards. But suppliers are often unsure if meeting these standards will guarantee continued business. They may also be unsure whether they will get better prices or help from buyers in meeting these standards. Many buyers are unwilling to pay a premium for products, even when factories are SA 8000 compliant, which is a major concern for most managers.31Stigzelius, I. & Mark-Herbert, C. (2009). Tailoring corporate responsibility to suppliers: Managing SA8000 in Indian garment manufacturing. Scandinavian Journal of Management, 25, 46-56.https://doi.org/10.1016/j.scaman.2008.04.003

Additionally, there are challenges that occur regarding the stakeholder dialogue as the SA 8000 recognizes the importance of stakeholder dialogue but doesn’t provide clear instructions on how to organize it or which stakeholders to include. This lack of guidance leads to operational concerns. Dialogue often focuses mainly on employees, customers and shareholders, neglecting other important stakeholders. Additionally, the absence of clear guidelines makes it difficult to structure the dialogue and evaluate the legitimacy of different stakeholder claims.49Gilbert, D. U. & Rasche, A. (2008). Opportunities and Problems of Standardized Ethics Initiatives – a Stakeholder Theory Perspective. Journal of Business Ethics, 83, 755-773. https://doi.org/10.1007/s10551-007-9591-1 Supporting these aspects, a study conducted by Abboubi et al. (2022) highlighted the importance of stakeholder engagement since they experienced major reluctance coming from certain stakeholders while implementing the SA 8000 standard.

As for any standard that needs to be applicable to a vast variety of sectors or companies, the SA 8000 is considered to be rather rigid. This rigidity is rooted in predefined, universal rules meant to be generalizable across various facilities. Implementing the same standards globally often conflicts with local conditions, which creates implementation challenges.50Rasche, A. (2010). The limits of corporate responsibility standards. Business Ethics: A European Review, 19, 280-291. https://doi.org/10.1111/j.1467-8608.2010.01592.x Furthermore, for accreditation bodies’ audit procedures to be effective, they must maintain somewhat of their flexibility. Auditors are unable to confirm a company’s compliance with SA 8000 by using a checklist that is designed to fit all companies. Since each company operates under different circumstances, adjusted evaluations are necessary to meet the standard’s objectives. However, this flexibility can introduce subjectivity into the auditing process, which may undermine the credibility of the certification.50Rasche, A. (2010). The limits of corporate responsibility standards. Business Ethics: A European Review, 19, 280-291. https://doi.org/10.1111/j.1467-8608.2010.01592.x

Internal barriers

In addition to the existing external barriers regarding the implementation of the standard there are also some internal barriers hindering the integration process.

One of the main internal barriers is conducted with the cost of the implementation of this standard. Sustaining the standard requires ongoing resources, and the costs associated with consultancy, certification and audits can be quite high.41Koster, M., Vos, B. & Van Der Walk, W. (2019). Drivers and barriers for adoption of a leading social management standard (SA8000) in developing economies. International Journal of Physical Distribution & Logistics Management, 49, 534-551. https://doi.org/10.1108/IJPDLM-01-2018-0037,40Murmura, F. & Bravi, L. (2020). Developing a Corporate Social Responsibility Strategy in India Using the SA 8000 Standard. Sustainability, 12, 3481. https://doi.org/10.3390/su12083481,31Stigzelius, I. & Mark-Herbert, C. (2009). Tailoring corporate responsibility to suppliers: Managing SA8000 in Indian garment manufacturing. Scandinavian Journal of Management, 25, 46-56.https://doi.org/10.1016/j.scaman.2008.04.003 For example, the initial audit for a company with 100 employees may range from $2000 to $3000. The certification remains valid for three years, but during this period, additional expenses are incurred due to biannual surveillance audits.31Stigzelius, I. & Mark-Herbert, C. (2009). Tailoring corporate responsibility to suppliers: Managing SA8000 in Indian garment manufacturing. Scandinavian Journal of Management, 25, 46-56.https://doi.org/10.1016/j.scaman.2008.04.003 As mentioned before in chapter 3.1 this is just an example, generally the cost of certification vary significally beyond firms. Beyond the direct costs of certification, companies also face financial burdens related to pre-certification efforts, such as enhancing workplace health and safety measures or establishing internal supervising systems.41Koster, M., Vos, B. & Van Der Walk, W. (2019). Drivers and barriers for adoption of a leading social management standard (SA8000) in developing economies. International Journal of Physical Distribution & Logistics Management, 49, 534-551. https://doi.org/10.1108/IJPDLM-01-2018-0037 The study conducted by Stigzelius & Mark-Herbert (2009) determined that labor costs increased by 20 % and overtime was reduced by three hours a day to meet the SA 8000 requirements, leaving companies with high costs and the need for financial investments. These findings were validated by Heras-Saizarbitoria (2018), who emphasized the financial challenges associated with implementing the SA 8000 standard. The study identified that the high costs involved in the implementation process present significant difficulties, particularly for smaller enterprises, due to their limited resources.51Heras‐Saizarbitoria, I., Boiral, O. & Allur, E. (2018). Three Decades of Dissemination of ISO 9001 and Two of ISO 14001: Looking Back and Ahead.

The second internal barrier relates to the integration and communication process within a company. Stigzelius & Mark-Herbert (2009) found that despite efforts to spread information about SA 8000 through training or posters in the local language, employees generally showed a low level of understanding of the standard. Additionally, many newly hired workers had not received any training on the standard. A common observation among managers was that the low level of education among workers created a substantial challenge to the training process.31Stigzelius, I. & Mark-Herbert, C. (2009). Tailoring corporate responsibility to suppliers: Managing SA8000 in Indian garment manufacturing. Scandinavian Journal of Management, 25, 46-56.https://doi.org/10.1016/j.scaman.2008.04.003 Merli et al. (2015) underlines this difficulty in ensuring personal involvement with the SA 8000, particularly in larger companies.

Lastly, another barrier commonly faced by companies in obtaining certification is the lack of internal expertise regarding the SA 8000.52Salomone, R. (2008). Integrated management systems: experiences in Italian organizations. Journal of Cleaner Production, 16, 1786-1806. https://doi.org/10.1016/j.jclepro.2007.12.003 While many managers are familiar with other certifications they often lack knowledge about the contents of SA 8000 and the specific challenges associated with achieving this certification.46Sartor, M., Orzes, G., Di Mauro, C., Ebrahimpour, M. & Nassimbeni, G. (2016). The SA8000 social certification standard: Literature review and theory-based research agenda. International Journal of Production Economics,175, 164-181. https://doi.org/10.1016/j.ijpe.2016.02.018

4.3 Drivers for decertification

Data through the third quarter of 2022 shows 356 new certifications to the SA 8000 standard, and a notable 767 decertifications or expirations. Although the decertification trend has slowed somewhat in the past year, with only 307 facilities decertifying, it is important to examine the drivers for decertification to better understand and mitigate the challenges organizations face in maintaining their certified status.39Marcuzzi, I., Podrecca, M., Sartor, M. & Nassimbeni, G. (2023). Out of social accountability: Reasons and alternative paths for SA8000 decertification. Corporate Social Responsibility and Environmental Management, 30, 3140-3158. https://doi.org/10.1002/csr.2543,14Social Accountability International. (n. d.-e). SA8000 Certified Organizations List. Retrieved 19.08.2024 from https://sa-intl.org/sa8000-search/ The reasons behind decertification will be examined in this area of the wiki. Despite the lack of research on this subject, the analysis that follows is based on two significant papers by Marcuzzi et al. (2023) and Podrecca et al. (2021). Both papers use empirical research involving multiple companies to evaluate the elements that contribute to decertification.

The main reason companies decide not to continue their certification to the SA 8000 standard is due the absence of commercial benefits. As mentioned before in chapter 4.1, implementing this standard can lead to several benefits regarding its corporate image and the relationship between buyer and costumer. However, these benefits seem to be “time-sensitive”. Marcuzzi et al. (2023) highlight that over time, the expected commercial advantages, such as attracting new clients and gaining competitive advantage, often fail to hold. At first, SA 8000 certification is seen as an important tool that can differentiate a company in the market and communicate its commitment to the standard. Companies assume that this will increase their business opportunities and that they may be able to charge higher prices for their products or services.39Marcuzzi, I., Podrecca, M., Sartor, M. & Nassimbeni, G. (2023). Out of social accountability: Reasons and alternative paths for SA8000 decertification. Corporate Social Responsibility and Environmental Management, 30, 3140-3158. https://doi.org/10.1002/csr.2543 But as more and more companies become SA 8000 certified, the certification may become less valuable. Companies such as those mentioned in the study by Podrecca at al. (2021) have reported that the anticipated sales-related benefits and premium pricing opportunities decrease over time. This loss of competitive advantage makes the certification seem less important.

Additionally, one of the main drivers of this standard is to meet customer requirements or to attract new ones. In some cases, however, clients and business partners may stop requiring SA 8000 certification to do business. Once the relationship between client and supplier is strengthened, clients may no longer see the certification as necessary.39Marcuzzi, I., Podrecca, M., Sartor, M. & Nassimbeni, G. (2023). Out of social accountability: Reasons and alternative paths for SA8000 decertification. Corporate Social Responsibility and Environmental Management, 30, 3140-3158. https://doi.org/10.1002/csr.2543 This assumption is underlined by a company interviewed by Podrecca et al. (2021) stating that none of the businesses that required adopting to the standard in the first place ended their business relationship with the company once they decided to decertify.

Other reasons for decertification include financial burdens. High costs are cited not only as a barrier to implementing the standard but also during recertification processes. The increased hourly wages and the ongoing investments required to meet the standards place a significant financial strain on companies, leading them to decide to leave the standard.39Marcuzzi, I., Podrecca, M., Sartor, M. & Nassimbeni, G. (2023). Out of social accountability: Reasons and alternative paths for SA8000 decertification. Corporate Social Responsibility and Environmental Management, 30, 3140-3158. https://doi.org/10.1002/csr.2543,53Podrecca, M., Orzes, G., Sartor, M. & Nassimbeni, G. (2021). The impact of abandoning social responsibility certifications: evidence from the decertification of SA8000 standard. International Journal of Operations & Production Management, 41, 100-126. https://doi.org/10.1108/IJOPM-10-2020-0698 In addition, the increasing number of work hours required to handle the extensive paperwork and document management makes it even more difficult to maintain certification status.

Other drivers of decertification listed in this paper include the limited influence of the standard, complexities in order and supplier management and a shortage of auditors. Additionally, a few companies cited mimicking behavior, following others who had left the standard. Factors such as employee discomfort, difficulties in integrating local laws with SA 8000 requirements and insufficient top management engagement also contributed to the decision to decertify.39Marcuzzi, I., Podrecca, M., Sartor, M. & Nassimbeni, G. (2023). Out of social accountability: Reasons and alternative paths for SA8000 decertification. Corporate Social Responsibility and Environmental Management, 30, 3140-3158. https://doi.org/10.1002/csr.2543

5 Critical analysis

The chapter beforehand highlighted a decline in the number of companies certified with the SA 8000 standard, leading to important questions about its relevance and effectiveness in today’s business environment. This chapter aims to provide a critical analysis of the SA 8000 standard. By exploring different aspects, the chapter seeks to determine whether SA 8000 continues to meet the needs of organizations or if it requires updates to maintain its significance in promoting social accountability.

One important point to consider is how the SA 8000 standard is implemented in different types of companies. Currently, most of the implementation is occurring in large companies. This trend can be attributed to the significant costs associated with implementing the standard, which can be challenging for smaller companies with limited resources to manage.51Heras‐Saizarbitoria, I., Boiral, O. & Allur, E. (2018). Three Decades of Dissemination of ISO 9001 and Two of ISO 14001: Looking Back and Ahead. Because of this, Llach et al. (2015) suggest that the standard should be adjusted to make it more accessible for small and medium-sized enterprises.

As discussed in Chapter 4.1, many companies implement the SA 8000 standard primarily due to external drivers, such as meeting customer demands or enhancing their corporate image. Boiral et al. (2017) argue that the implementation of SA 8000 is therefore frequently used as a strategic move within companies, serving as a form of CSR-washing. The adaption of the standard enables organizations to appear socially responsible even if they do not fully implement the standard internally. A major critique of the SA 8000 standard is therefore that it often fails to have a big effect on a company, as many organizations adopt it primarily due to external pressures.