Authors: Joost Horstmann

Edited by: –

Last updated: October 8, 2025

Executive summary

Organizational incentives for sustainability align individual behavior and corporate systems with environmental objectives. They include financial rewards, performance recognition, training, employee participation, negative incentives, and green nudges. Research links these incentives to higher pro‑environmental behavior (PEB) and improved environmental performance (EP), especially when goals and metrics are clear and supported by credible leadership and culture. A balanced approach that combines extrinsic motivators (e.g., bonuses) with intrinsic drivers (autonomy, competence, relatedness) produces more durable change than money alone.

External pressures—policy, regulation, investor demands, customer expectations, and civil society—push firms to operationalize sustainability. Internally, green organizational culture, sustainable leadership, EP monitoring, and knowledge sharing enable incentives to work. ISO 14001 and Sustainability Balanced Scorecards (SBSC) help set targets, define KPIs, and translate environmental priorities into day‑to‑day decisions and compensation. Case examples from Interface (EcoSense Bonus Plan) and BMW show how clear targets, site‑level accountability, and training programs embed sustainability in performance systems.

Effective design addresses common barriers: attitude and resistance to change, crowding‑out of intrinsic motivation by poorly framed monetary rewards, lack of knowledge, and limited resources. Practical recommendations include: co‑creating a sustainability identity and culture, establishing transparent targets and evaluation systems, investing in training and knowledge‑sharing, and calibrating incentives to external requirements and internal capacity. The AMO framework (Ability–Motivation–Opportunity) and Green HRM provide actionable structures to integrate incentives across the workforce and connect PEB to EP and competitive advantage.

Future work should expand incentive measurement, deepen psychological mechanisms (e.g., attitude–behavior gaps), and strengthen social sustainability links. For practitioners, start with a status‑quo assessment, set measurable goals, implement a portfolio of incentives across roles, and evaluate and adjust through a PDCA cycle. Done well, green incentives become a strategic lever that improves environmental outcomes, engages employees, and builds resilient, competitive organizations.

1 Introduction

The responsibility of companies as major contributors to negative environmental impacts underscores the necessity of considering organizations as relevant actors in sustainable development.1Shahzad, M. A., Du Jianguo & Junaid, M. Impact of green HRM practices on sustainable performance: mediating role of green innovation, green culture, and green employees’ behavior. Environ Sci Pollut Res 30, 88524–88547; 10.1007/s11356-023-28498-6 (2023). In Europe, industry was responsible for approximately 20 percent of CO2 emissions in 2022, with the energy sector and agriculture not included in this figure.2Europäisches Parlament. Treibhausgasemissionen nach Ländern und Sektoren (Infografik) | Themen | Europäisches Parlament. Available at https://www.europarl.europa.eu/topics/de/article/20180301STO98928/treibhausgasemissionen-nach-landern-und-sektoren-infografik (2022). Concurrently, the various industries contribute to resource consumption, biodiversity loss, and climate change through energy-intensive processes, raw material extraction.3Hirschnitz-Garbers, M., Tan, A. R., Gradmann, A. & Srebotnjak, T. Key drivers for unsustainable resource use – categories, effects and policy pointers. Journal of Cleaner Production 132, 13–31; 10.1016/j.jclepro.2015.02.038 (2016).4Panwar, R., Ober, H. & Pinkse, J. The uncomfortable relationship between business and biodiversity: Advancing research on business strategies for biodiversity protection. Bus Strat Env 32, 2554–2566; 10.1002/bse.3139 (2023). The concept of corporate social responsibility (CSR) therefore broadens the discourse on organizational accountability by establishing social and environmental considerations as valid criteria alongside financial objectives.5Lindgreen, A. & Swaen, V. Corporate Social Responsibility. International Journal of Management Reviews 12, 1–7; 10.1111/j.1468-2370.2009.00277.x (2010). As a consequence of these issues, companies are subject to substantial external pressures to live up to their responsibility: Governments are implementing ambitious climate targets, investors are demanding transparency regarding environmental-, social- and governance-metrics, consumers are increasingly demanding sustainable products, and Non-Governmental Organizations are publicly exposing violations.6Zhao, Y. & Yang, Y. Sustainability target setting and incentive design: A literature review. BMTP 2, 3134; 10.54517/bmtp3134 (2025).7González‐Benito, J. & González‐Benito, Ó. A study of determinant factors of stakeholder environmental pressure perceived by industrial companies. Bus Strat Env 19, 164–181; 10.1002/bse.631 (2010).8Deegan, C. & Islam, M. A. An exploration of NGO and media efforts to influence workplace practices and associated accountability within global supply chains. The British Accounting Review 46, 397–415; 10.1016/j.bar.2014.10.002 (2014).

The external expectations together with this recent development led to the implementation of numerous incentives that motivate organizations sustainable transformations. Regulatory requirements, such as the obligation for large corporations to report on sustainability, CO2 pricing as well as government support programs, tax-benefits and subsidies, create a framework that rewards environmentally and socially responsible behavior, and penalizes irresponsible behavior.9Saka, N., Olanipekun, A. O. & Omotayo, T. Reward and compensation incentives for enhancing green building construction. Environmental and Sustainability Indicators 11, 100138; 10.1016/j.indic.2021.100138 (2021).10Khattak, M. S., Wu, Q., Ahmad, M. & Ullah, R. Exploring the knowledge structure between government incentives and corporate social responsibility. CR; 10.1108/CR-03-2024-0062 (2025).11Jiang, K., Leng, M., Jiang, Y. & Xu, L. From penalties to profits: how government regulation and cost-revenue trade-offs shape green production and marketing. Environ Dev Sustain, 1–37; 10.1007/s10668-025-06250-z (2025).12Anton, W. R. Q., Deltas, G. & Khanna, M. Incentives for environmental self-regulation and implications for environmental performance. Journal of Environmental Economics and Management 48, 632–654; 10.1016/j.jeem.2003.06.003 (2004). The mounting pressure from stakeholders and government incentives has led to a shift in perspective among companies, which now regard sustainability not only as a moral obligation, but also as a strategic consideration.13Sarkis, J., Gonzalez‐Torre, P. & Adenso‐Diaz, B. Stakeholder pressure and the adoption of environmental practices: The mediating effect of training. Journal of Operations Management 28, 163–176; 10.1016/j.jom.2009.10.001 (2010). A study from 2022 revealed, that at least 300 of the Fortune Global Top 500 companies are communicating their commitment to the Sustainable Development Goals (SDGs).14Song, L. et al. How much is global business sectors contributing to sustainable development goals? Sustainable Horizons 1, 100012; 10.1016/j.horiz.2022.100012 (2022). These goals, which were adopted in 2015 within the United Nations Agenda for Sustainable Development, encompass the social, environmental, and economic dimensions of sustainability.15United Nations. The Sustainable Development Goals. Available at https://www.un.org/sustainabledevelopment/development-goals/ (2025). However, the study also indicates that a significant number of companies are utilising sustainability in a rather superficial manner. Less than 23 percent of the sample used the SDGs to develop specific actions, and less than one percent developed tools to measure their progress.14Song, L. et al. How much is global business sectors contributing to sustainable development goals? Sustainable Horizons 1, 100012; 10.1016/j.horiz.2022.100012 (2022). Therefore, the efficacy of these external mechanisms and incentives is limited in terms of achieving comprehensive integration of sustainability into the decision-making processes, measures and cultural ethos of corporations.14Song, L. et al. How much is global business sectors contributing to sustainable development goals? Sustainable Horizons 1, 100012; 10.1016/j.horiz.2022.100012 (2022).16Graafland, J. & Bovenberg, L. Government regulation, business leaders’ motivations and environmental performance of SMEs. Journal of Environmental Planning and Management 63, 1335–1355 (2020).17He, Q. The influence of organizational policies on firm environmental performance through sustainable technologies and innovation and stakeholder concerns. Sci Rep 15, 10019; 10.1038/s41598-025-94499-9 (2025).

Consequently, internal organizational incentives for sustainability (hereinafter also referred to as “green incentives”) have been gaining increasing attention in recent decades as an effective tool, impelling organizational members at all hierarchical levels to proactively pursue the company’s environmental sustainability objectives.18Loedphacharakamon, N. & Worakittikul, W. TQM and sustainable hospitality: unpacking the link between green culture, employee behavior, and hotel performance. Cogent Business & Management 12, 2499948; 10.1080/23311975.2025.2499948 (2025).19Derchi, G.-B., Davila, A. & Oyon, D. Green incentives for environmental goals. Management Accounting Research 59, 100830; 10.1016/j.mar.2022.100830 (2023).20Johnstone, L. & Beusch, P. Motivating sustainable behaviour in the workplace through control. J Manag Control, 1–36; 10.1007/s00187-025-00390-z (2025).21Govindarajulu, N. & Daily, B. F. Motivating employees for environmental improvement. Industrial Management & Data Systems 104, 364–372; 10.1108/02635570410530775 (2004). It is important to acknowledge that, within the scope of this thesis, the concept of sustainability will be examined through the lenses of ecological and economic perspectives.1Shahzad, M. A., Du Jianguo & Junaid, M. Impact of green HRM practices on sustainable performance: mediating role of green innovation, green culture, and green employees’ behavior. Environ Sci Pollut Res 30, 88524–88547; 10.1007/s11356-023-28498-6 (2023).22Nikolaou, I. E., Tsagarakis, K. P. & Tasopoulou, K. An examination of ecopreneurs’ incentives through a combination between institutional and resource-based approach. MEQ 29, 195–215; 10.1108/MEQ-01-2017-0004 (2018). The social dimension is also highly relevant, however, with reference to green incentives, its integration is still in its beginnings, particularly in terms of measurability.19Derchi, G.-B., Davila, A. & Oyon, D. Green incentives for environmental goals. Management Accounting Research 59, 100830; 10.1016/j.mar.2022.100830 (2023).23Süßbauer, E. & Schäfer, M. Corporate strategies for greening the workplace: Findings from sustainability-oriented companies in Germany. Journal of Cleaner Production 226, 564–577; 10.1016/j.jclepro.2019.04.009 (2019).24Amrutha, V. N. & Geetha, S. N. A systematic review on green human resource management: Implications for social sustainability. Journal of Cleaner Production 247, 119131; 10.1016/j.jclepro.2019.119131 (2020). Organisational incentives for sustainability are therefore defined as the totality of financial and non-financial reward, control, and motivation mechanisms implemented by companies to align the behavior of organizational members with sustainability objectives and improve their competencies.20Johnstone, L. & Beusch, P. Motivating sustainable behaviour in the workplace through control. J Manag Control, 1–36; 10.1007/s00187-025-00390-z (2025).25Beck-Krala, E. & Klimkiewicz, K. Reward Programs Supporting Environmental Organizational Policy. Zarządzanie Zasobami Ludzkimi, 41–54 (2017).26Dahlmann, F., Branicki, L. & Brammer, S. ‘Carrots for Corporate Sustainability’: Impacts of Incentive Inclusiveness and Variety on Environmental Performance. Bus Strat Env 26, 1110–1131; 10.1002/bse.1971 (2017). According to the findings of the Carbon Disclosure Project, a survey conducted in 2013 revealed that. 77.5 percent of the sampled companies had already implemented compensation structures at various hierarchical levels as a form of green incentive systems.19Derchi, G.-B., Davila, A. & Oyon, D. Green incentives for environmental goals. Management Accounting Research 59, 100830; 10.1016/j.mar.2022.100830 (2023). In addition to such green rewards, which are among the most well-established incentive types, these also include negative incentives, performance recognition, environmental training, employee empowerment for participation and nudging.

As portrayed by the number of different incentive systems, the motivation to act in a sustainable manner is a multifaceted phenomenon. Empirical studies demonstrate that green incentive systems have the capacity to influence the pro-environmental behavior (PEB) and enhance environmental performance (EP).27Aftab, J., Abid, N., Cucari, N. & Savastano, M. Green human resource management and environmental performance: The role of green innovation and environmental strategy in a developing country. Bus Strat Env 32, 1782–1798; 10.1002/bse.3219 (2023).28Ojo, A. O., Tan, C. N.-L. & Alias, M. Linking green HRM practices to environmental performance through pro-environment behaviour in the information technology sector. Social Responsibility Journal 18, 1–18; 10.1108/SRJ-12-2019-0403 (2022). However, long-term effects can only be enabled when individual values and the workforce’s sense of purpose align with organizational structures. In the context of incentives intrinsic motives, such as environmental awareness and personal responsibility, interact with extrinsic organizational factors, including green incentive systems.20Johnstone, L. & Beusch, P. Motivating sustainable behaviour in the workplace through control. J Manag Control, 1–36; 10.1007/s00187-025-00390-z (2025).26Dahlmann, F., Branicki, L. & Brammer, S. ‘Carrots for Corporate Sustainability’: Impacts of Incentive Inclusiveness and Variety on Environmental Performance. Bus Strat Env 26, 1110–1131; 10.1002/bse.1971 (2017).29Rahman, M., Abd Wahab, S. & Abdul Latiff, A. S. The Underlying Theories of Organizational Sustainability: The Motivation Perspective. JBMS 5, 181–193; 10.32996/jbms.2023.5.1.18 (2023). Therefore, an effective incentive must take both levels into account to achieve sustainability not only as a duty but as an integral part of organizational identity.30Liu, J. & Liu, J. The greater the incentives, the better the effect? Interactive moderating effects on the relationship between green motivation and green creativity. IJCHM 35, 919–932; 10.1108/IJCHM-03-2022-0340 (2023). In such circumstances, the implementation of organizational incentive systems for sustainability can serve as an effective strategy to encourage PEB among all members.20Johnstone, L. & Beusch, P. Motivating sustainable behaviour in the workplace through control. J Manag Control, 1–36; 10.1007/s00187-025-00390-z (2025).31Maki, A., Burns, R. J., Ha, L. & Rothman, A. J. Paying people to protect the environment: A meta-analysis of financial incentive interventions to promote proenvironmental behaviors. Journal of Environmental Psychology 47, 242–255; 10.1016/j.jenvp.2016.07.006 (2016). This, in turn, facilitates the EP and the overall sustainability of the organization.27Aftab, J., Abid, N., Cucari, N. & Savastano, M. Green human resource management and environmental performance: The role of green innovation and environmental strategy in a developing country. Bus Strat Env 32, 1782–1798; 10.1002/bse.3219 (2023).28Ojo, A. O., Tan, C. N.-L. & Alias, M. Linking green HRM practices to environmental performance through pro-environment behaviour in the information technology sector. Social Responsibility Journal 18, 1–18; 10.1108/SRJ-12-2019-0403 (2022).

The objective of this thesis is to provide a comprehensive scientific and holistic overview of organizational incentives for sustainability, including their interdisciplinary perspectives and the practical application of such incentive systems. To that end, it addresses the following two questions:

- What are organizational incentives for sustainability and what is the current state of research?

- How can organizational incentives for sustainability be successfully implemented in practice?

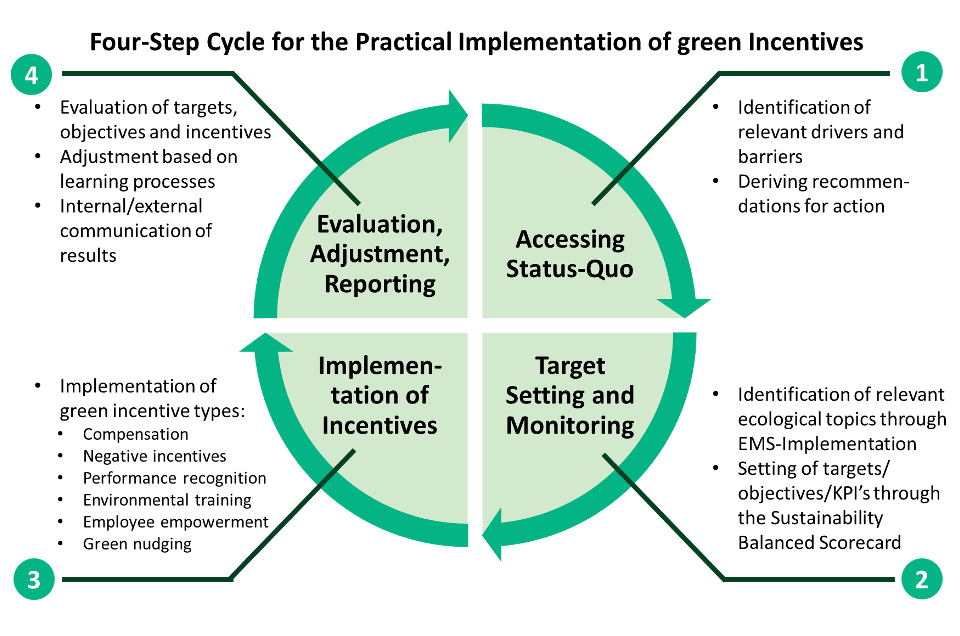

To answer these research questions, the structure of this thesis is as follows: After presenting the underlying methodology in Chapter 2, Chapter 3 provides a comprehensive literature review on the topic of organizational incentives for sustainability. Starting with a more detailed definition of organizational incentives for sustainability, their different forms, and the division of the concept of sustainability in Chapter 3.1, Chapter 3.2 examines historical developments. Chapter 3.3 explores relevant theories and literature to clarify how incentives function. To achieve this, the thesis first adopts an economic sustainability perspective and then divides ecological sustainability into individual and organizational perspectives. The literature review concludes with a discussion of future research opportunities. To address the second research question, Chapter 4 outlines the practical implementation of organizational incentives for sustainability using a four-step cycle process.

2 Literature review

In addition to providing relevant definitions and a historical overview, the literature review primarily focuses on the theoretical concepts that explain how organizational green incentive systems work. First, a few of these concepts are assigned to the economic perspective in form of organizational performance, and then the relevant theories and literature streams for ecological sustainability are presented. In the incentive context, sustainability performance can be viewed from individual and organizational perspectives, which is why the relevant theories are separated into these two categories.

2.1 Definition

This thesis proposes a comprehensive definition of “green incentives” by synthesising the three definitional approaches from Johnstone and Beusch (2025), Beck-Krala and Klimkiewicz (2017) and Dahlmann et al (2017).20Johnstone, L. & Beusch, P. Motivating sustainable behaviour in the workplace through control. J Manag Control, 1–36; 10.1007/s00187-025-00390-z (2025).25Beck-Krala, E. & Klimkiewicz, K. Reward Programs Supporting Environmental Organizational Policy. Zarządzanie Zasobami Ludzkimi, 41–54 (2017).26Dahlmann, F., Branicki, L. & Brammer, S. ‘Carrots for Corporate Sustainability’: Impacts of Incentive Inclusiveness and Variety on Environmental Performance. Bus Strat Env 26, 1110–1131; 10.1002/bse.1971 (2017). Therefore, organizational incentives for sustainability are defined as the totality of financial and non-financial reward, control, and motivation mechanisms implemented by companies to align the behavior of organizational members with sustainability objectives and improve their competencies.

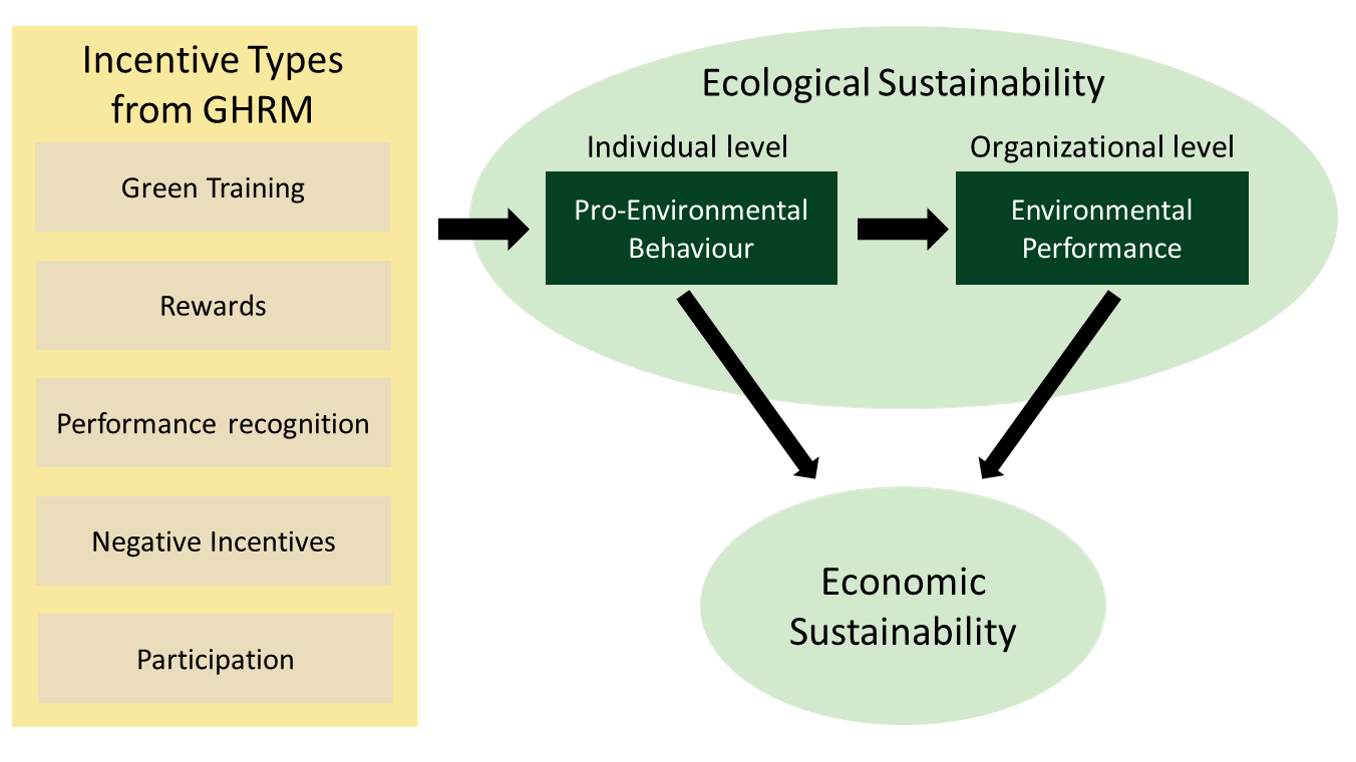

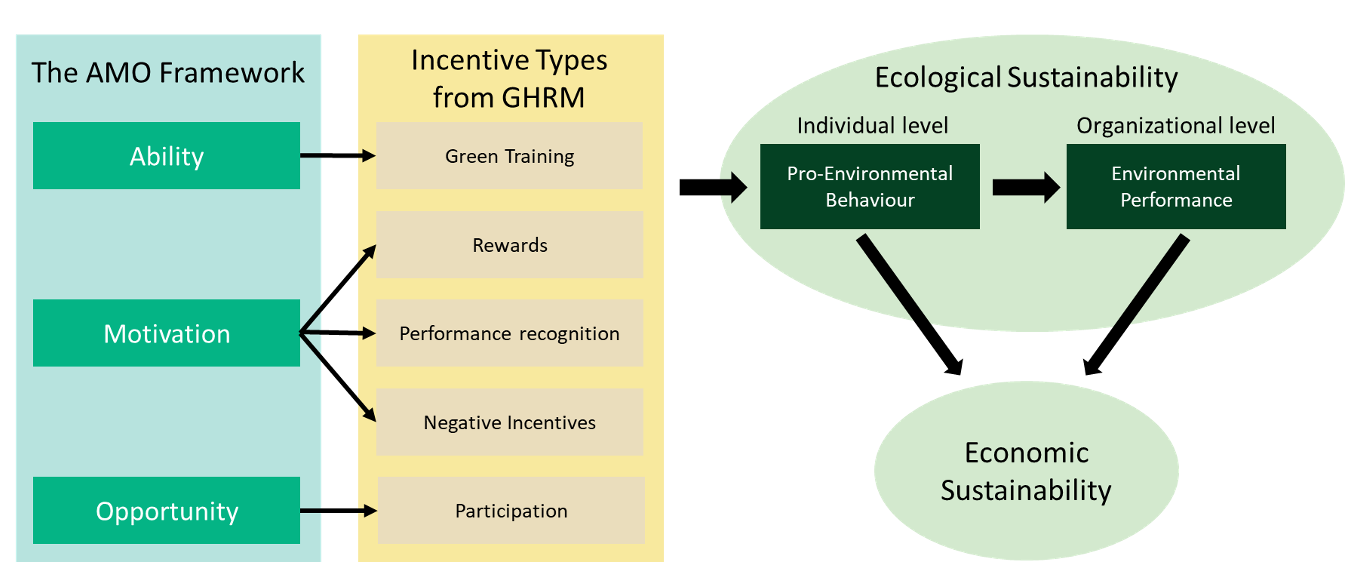

The majority of literature pertaining to the green incentive therefore focuses on the activation of PEB among organizational members and the improvement of EP at the organizational level.27Aftab, J., Abid, N., Cucari, N. & Savastano, M. Green human resource management and environmental performance: The role of green innovation and environmental strategy in a developing country. Bus Strat Env 32, 1782–1798; 10.1002/bse.3219 (2023).28Ojo, A. O., Tan, C. N.-L. & Alias, M. Linking green HRM practices to environmental performance through pro-environment behaviour in the information technology sector. Social Responsibility Journal 18, 1–18; 10.1108/SRJ-12-2019-0403 (2022).32Ren, S., Tang, G. & E. Jackson, S. Green human resource management research in emergence: A review and future directions. Asia Pac J Manag 35, 769–803; 10.1007/s10490-017-9532-1 (2018). These two central target units for the ecological sustainability of green incentives will be further elaborated upon in Chapter 3.1.2.

Nonetheless, organizational performance also plays a role in implementing such green incentive systems. The focus of green incentive systems on human resources enables the generation of intangible competitive advantages, alongside the enhancement of employee performance and sustainable knowledge capital.1Shahzad, M. A., Du Jianguo & Junaid, M. Impact of green HRM practices on sustainable performance: mediating role of green innovation, green culture, and green employees’ behavior. Environ Sci Pollut Res 30, 88524–88547; 10.1007/s11356-023-28498-6 (2023).33Amjad, F. et al. Effect of green human resource management practices on organizational sustainability: the mediating role of environmental and employee performance. Environ Sci Pollut Res 28, 28191–28206; 10.1007/s11356-020-11307-9 (2021). Therefore, sustainability incentive systems should be designed to improve knowledge transfer, information absorption, and competence development with respect to ecological objectives.26Dahlmann, F., Branicki, L. & Brammer, S. ‘Carrots for Corporate Sustainability’: Impacts of Incentive Inclusiveness and Variety on Environmental Performance. Bus Strat Env 26, 1110–1131; 10.1002/bse.1971 (2017).

Johnstone and Beusch (2025) address the different incentive type systems and their target groups in their own definition of incentives for sustainable development in organizations:

“The regulatory processes put in place by organizations and/or individuals therein to ensure the behavio[u]ral alignment between individual employees and the organization and/or other (groups of) employees throughout the hierarchy. These can include both tangible incentives such as monetary bonuses and benefits and/or intangible incentives such as feelings of belonging, autonomy and competence, among others, for employees throughout the hierarchy.” (p. 28).20Johnstone, L. & Beusch, P. Motivating sustainable behaviour in the workplace through control. J Manag Control, 1–36; 10.1007/s00187-025-00390-z (2025).

This definition emphasizes that the target group for incentives is not exclusively employees but that incentive systems for sustainability can be implemented throughout the entire organizational hierarchy, extending to all individuals. The key factors are the systematic design and targeted distribution of incentives across different levels and functional areas to achieve collective ecological effects.19Derchi, G.-B., Davila, A. & Oyon, D. Green incentives for environmental goals. Management Accounting Research 59, 100830; 10.1016/j.mar.2022.100830 (2023).20Johnstone, L. & Beusch, P. Motivating sustainable behaviour in the workplace through control. J Manag Control, 1–36; 10.1007/s00187-025-00390-z (2025). For this reason, in the following this thesis refers to organizational members rather than just employees or managers.

Moreover, this definition underscores the significance of a broader array of mechanisms in sustainability incentive systems. Evidently formalised and structured control mechanisms, such as reward and punishment systems and measurable targets, are not the only factors that play a role.25Beck-Krala, E. & Klimkiewicz, K. Reward Programs Supporting Environmental Organizational Policy. Zarządzanie Zasobami Ludzkimi, 41–54 (2017). Less visible forms of motivation, such as social norms, collective values, role models, and peer pressure, are also central. Motivation for sustainable action comes from both external incentives and the fulfillment of basic psychological needs, such as autonomy, competence, and belonging.20Johnstone, L. & Beusch, P. Motivating sustainable behaviour in the workplace through control. J Manag Control, 1–36; 10.1007/s00187-025-00390-z (2025).26Dahlmann, F., Branicki, L. & Brammer, S. ‘Carrots for Corporate Sustainability’: Impacts of Incentive Inclusiveness and Variety on Environmental Performance. Bus Strat Env 26, 1110–1131; 10.1002/bse.1971 (2017). Accordingly, the effectiveness of such incentive systems depends on how well they align with the individual needs, motives, and goals of organizational members, as well as credible organizational commitment from company management.34Kang, Y.-C., Hsiao, H.-S. & Ni, J.-Y. The Role of Sustainable Training and Reward in Influencing Employee Accountability Perception and Behavior for Corporate Sustainability. Sustainability 14, 11589; 10.3390/su141811589 (2022).

2.1.1 Incentive types

A more thorough examination of the second part of the definition proposed by Johnstone and Beusch (2025) is necessary to further refine the understanding of organizational incentives for sustainability.20Johnstone, L. & Beusch, P. Motivating sustainable behaviour in the workplace through control. J Manag Control, 1–36; 10.1007/s00187-025-00390-z (2025). In this regard, it is imperative to acknowledge that incentives can be categorised into various types. In the definition, the distinction between tangible and intangible is employed; however, in GHRM- and green incentive-theory, the classic distinction separates green incentives into financial and non-financial categories.21Govindarajulu, N. & Daily, B. F. Motivating employees for environmental improvement. Industrial Management & Data Systems 104, 364–372; 10.1108/02635570410530775 (2004).26Dahlmann, F., Branicki, L. & Brammer, S. ‘Carrots for Corporate Sustainability’: Impacts of Incentive Inclusiveness and Variety on Environmental Performance. Bus Strat Env 26, 1110–1131; 10.1002/bse.1971 (2017).35Leidner, S., Baden, D. & Ashleigh, M. J. Green (environmental) HRM: aligning ideals with appropriate practices. PR 48, 1169–1185; 10.1108/PR-12-2017-0382 (2019). Monetary incentives can be summarised under the term “Compensation”, while non-monetary incentives exhibit a greater degree of diversity in their different motivational types.20Johnstone, L. & Beusch, P. Motivating sustainable behaviour in the workplace through control. J Manag Control, 1–36; 10.1007/s00187-025-00390-z (2025).36Renwick, D. W., Redman, T. & Maguire, S. Green Human Resource Management: A Review and Research Agenda*. Int J Management Reviews 15, 1–14; 10.1111/j.1468-2370.2011.00328.x (2013).37Arulrajah, A. A., Opatha, H. & Nawaratne, N. Green Human Resource Management Practices: A Review. SLJHRM 5 (2015). For this reason, non-monetary incentive types are considered individually and are not grouped under a single term. The following Table 1 provides an initial overview of the incentive types, accompanied by their respective definitions. The six incentive types were selected based on the previously formulated definition and through the synthesis of the relevant literature from GHRM as well as the literature specifically focused on green incentives. This overview will be expanded upon in greater detail in the practical section of this thesis in Chapter 4.3, where a more comprehensive table and additional information will be provided.

Incentive Type

Definition

Financial

Rewards

Monetary benefits that are designed to encourage PEB or sustainable decisions and achieve green organizational goals38Das, S. & Dash, M. Green Compensation And Reward System: A Novel Approach Towards The Growth And Sustainability Of Organisation. Journal of Advanced Zoology 45, 1213–1219 (2024).39Yin, Y., Wang, Y. & Lu, Y. How to Design Green Compensation to Promote Managers’ Pro-Environmental Behavior? A Goal-Framing Perspective. J Bus Ethics 197, 341–353; 10.1007/s10551-024-05762-4 (2025).

Non-financial

Negative incentives

Measures such as warnings, suspensions or disciplinary penalties that sanction undesirable behaviour37Arulrajah, A. A., Opatha, H. & Nawaratne, N. Green Human Resource Management Practices: A Review. SLJHRM 5 (2015).40Mandip, G. Green HRM: People Management Commitment to Environmental Sustainability. Research Journal of Recent Sciences 1, 244–252 (2012).

Performance recognition

Methodical feedback and appreciation of PEB and EP for organizational members35Leidner, S., Baden, D. & Ashleigh, M. J. Green (environmental) HRM: aligning ideals with appropriate practices. PR 48, 1169–1185; 10.1108/PR-12-2017-0382 (2019).41Saeed, B. B. et al. Promoting employee’s proenvironmental behavior through green human resource management practices. Corp Soc Responsibility Env 26, 424–438; 10.1002/csr.1694 (2019).42Milne, P. Motivation, incentives and organisational culture. Journal of Knowledge Management 11, 28–38; 10.1108/13673270710832145 (2007).

Environmental training

Provision of systematic educational measures aimed at expanding the knowledge, skills and awareness of organizational members about ecological issues34Kang, Y.-C., Hsiao, H.-S. & Ni, J.-Y. The Role of Sustainable Training and Reward in Influencing Employee Accountability Perception and Behavior for Corporate Sustainability. Sustainability 14, 11589; 10.3390/su141811589 (2022).43Pham, N. T., Vo-Thanh, T., Shahbaz, M., Duc Huynh, T. L. & Usman, M. Managing environmental challenges: Training as a solution to improve employee green performance. Journal of Environmental Management 269, 110781; 10.1016/j.jenvman.2020.110781 (2020).44Teixeira, A. A., Jabbour, C. J. C., Sousa Jabbour, A. B. L. de, Latan, H. & Oliveira, J. H. C. de. Green training and green supply chain management: evidence from Brazilian firms. Journal of Cleaner Production 116, 170–176; 10.1016/j.jclepro.2015.12.061 (2016).

Employee empowerment for participation

Integration of employees within decision-making processes, problem-solving methodologies, and the development of green initiatives45Tariq, S., Jan, F. A. & Ahmad, M. S. Green employee empowerment: a systematic literature review on state-of-art in green human resource management. Qual Quant 50, 237–269; 10.1007/s11135-014-0146-0 (2016).46Markey, R., McIvor, J., O’Brien, M. & Wright, C. F. Reducing carbon emissions through employee participation: evidence from Australia. Industrial Relations Journal 50, 57–83; 10.1111/irj.12238 (2019).47Ye, P., Liu, L. & Tan, J. Influence of leadership empowering behavior on employee innovation behavior: The moderating effect of personal development support. Front. Psychol. 13, 1022377; 10.3389/fpsyg.2022.1022377 (2022).

Green nudging

Implementation of targeted modifications (subtle influencing of decision-making), aiming to increase the probability of sustainable behavior, while ensuring the preservation of individual autonomy48Decrinis, L., Freibichler, W., Kaiser, M., Sunstein, C. R. & Reisch, L. A. Sustainable behaviour at work: How message framing encourages employees to choose electric vehicles. Bus Strat Env 32, 5650–5668; 10.1002/bse.3441 (2023).49Paolis, G. de, Tiberio, L. & Caffaro, F. More sustainable choices in the workplace: a systematic review of nudge theory applications. Front. Psychol. 16, 1556796; 10.3389/fpsyg.2025.1556796 (2025).

| Incentive Type | Definition | |

| Financial | Rewards | Monetary benefits that are designed to encourage PEB or sustainable decisions and achieve green organisational goals40,41 |

| Non-financial | Negative incentives | Measures such as warnings, suspensions or disciplinary penalties that sanction undesirable behaviour39,42 |

| Performance recognition | Methodical feedback and appreciation of PEB and EP for organisational members37,43,44 | |

| Environmental training | Provision of systematic educational measures aimed at expanding the knowledge, skills and awareness of organisational members about ecological issues36,45,46 | |

| Employee empowerment for participation | Integration of employees within decision-making processes, problem-solving methodologies, and the development of green initiatives47–49 | |

| Green nudging | Implementation of targeted modifications (subtle influencing of decision-making), aiming to increase the probability of sustainable behaviour, while ensuring the preservation of individual autonomy50,51 |

2.1.2 Definition of sustainability in a green incentive context

The concept of sustainability has grown steadily over the past few decades, making it difficult to arrive at a definition that capture its multifaceted nature. Contemporary research fundamentally considers sustainability from three interdependent dimensions, as set out in the Brundtland Report, the Triple Bottom Line and the United Nations Agenda:15United Nations. The Sustainable Development Goals. Available at https://www.un.org/sustainabledevelopment/development-goals/ (2025).50Brundtland, G. H. Our Common Future: Report of the World Commission on Environment and Development, 1987.51Goldsmith, P. D. & Basak, R. Incentive Contracts and Environmental Performance Indicators. Environmental and Resource Economics 20, 259–279; 10.1023/A:1013065801547 (2001).52Elkington, J. Accounting for the triple bottom line. Measuring Business Excellence 2, 18–22; 10.1108/eb025539 (1998).

- Ecological sustainability: Addresses the careful use of resources, the limitation of emissions and waste, and the protection of biodiversity and ecosystems,

- Economic sustainability: Encompasses securing prosperity and economic performance. Sustainable management considers the resilience of companies and markets across generations, rather than focusing solely on short-term profit maximisation.

- Social sustainability: Involves promoting social justice, participation, and fair working and living conditions to create social stability.53Elkington, J. Towards the Sustainable Corporation: Win-Win-Win Business Strategies for Sustainable Development.California Management Review 36, 90–100; 10.2307/41165746 (1994).54Purvis, B., Mao, Y. & Robinson, D. Three pillars of sustainability: in search of conceptual origins. Sustain Sci 14, 681–695; 10.1007/s11625-018-0627-5 (2019).

A significant number of scientific research has criticised these three dimensions for failing to grasp the complexity and interdisciplinary nature of sustainability.55Kuhlman, T. & Farrington, J. What is Sustainability? Sustainability 2, 3436–3448; 10.3390/su2113436 (2010).56Giovannoni, E. & Fabietti, G. What Is Sustainability? A Review of the Concept and Its Applications. In Integrated reporting. Concepts and cases that redefine corporate accountability, edited by C. Busco (Springer, Cham, Heidelberg, 2013), pp. 21–40. This development will also be seen in the following chapters, which demonstrate how different theoretical approaches on the economic and ecological sustainability shape the impacts of green incentives. However, as outlined in the introduction, social sustainability is not a consideration within the framework of green incentive systems. One reason for this is that the social perspective is generally given little attention in the literature on green incentives.24Amrutha, V. N. & Geetha, S. N. A systematic review on green human resource management: Implications for social sustainability. Journal of Cleaner Production 247, 119131; 10.1016/j.jclepro.2019.119131 (2020). Conversely, social performance indicators have been found to be lacking in terms of standardization and objectivity in measurement, a factor that is of considerable significance with regard to the practical implementation and monitoring of green incentives.19Derchi, G.-B., Davila, A. & Oyon, D. Green incentives for environmental goals. Management Accounting Research 59, 100830; 10.1016/j.mar.2022.100830 (2023).23Süßbauer, E. & Schäfer, M. Corporate strategies for greening the workplace: Findings from sustainability-oriented companies in Germany. Journal of Cleaner Production 226, 564–577; 10.1016/j.jclepro.2019.04.009 (2019).24Amrutha, V. N. & Geetha, S. N. A systematic review on green human resource management: Implications for social sustainability. Journal of Cleaner Production 247, 119131; 10.1016/j.jclepro.2019.119131 (2020).57Maas, K. & Rosendaal, S. Sustainability Targets in Executive Remuneration: Targets, Time Frame, Country and Sector Specification. Bus Strat Env 25, 390–401; 10.1002/bse.1880 (2016). The issue of economic sustainability will be addressed in Chapter 3.3.1, which will examine perspectives on intangible competitive advantages and organizational performance in the context of green incentives.1Shahzad, M. A., Du Jianguo & Junaid, M. Impact of green HRM practices on sustainable performance: mediating role of green innovation, green culture, and green employees’ behavior. Environ Sci Pollut Res 30, 88524–88547; 10.1007/s11356-023-28498-6 (2023).22Nikolaou, I. E., Tsagarakis, K. P. & Tasopoulou, K. An examination of ecopreneurs’ incentives through a combination between institutional and resource-based approach. MEQ 29, 195–215; 10.1108/MEQ-01-2017-0004 (2018).

Nonetheless, the existing literature on organizational incentives for sustainability primarily focuses on the dimension of ecological sustainability. This is why the two most used theoretical target variables in form of PEB and EP are defined below – first at the individual level and then derived from this at the organizational level. This enables a better understanding of ecological sustainability in the context of green incentive systems, as the division into individual and organizational perspectives will be a reoccurring theme. As shown in Chapter 3.3.2 where this thesis dives deeper into green incentives and ecological sustainability, the consideration of these two perspectives plays a central role in the relevant literature for green incentives.27Aftab, J., Abid, N., Cucari, N. & Savastano, M. Green human resource management and environmental performance: The role of green innovation and environmental strategy in a developing country. Bus Strat Env 32, 1782–1798; 10.1002/bse.3219 (2023).58Elshaer, I. A., Sobaih, A. E. E., Aliedan, M. & Azazz, A. M. S. The Effect of Green Human Resource Management on Environmental Performance in Small Tourism Enterprises: Mediating Role of Pro-Environmental Behaviors.Sustainability 13, 1956; 10.3390/su13041956 (2021).59Marrucci, L., Daddi, T. & Iraldo, F. Creating environmental performance indicators to assess corporate sustainability and reward employees. Ecological Indicators 158, 111489; 10.1016/j.ecolind.2023.111489 (2024).

2.1.2.1 Pro-environmental behaviour

Before examining the desired effect of incentives for sustainability from an organizational perspective, it is important to first consider the effect on an individual level. Various terms are used in the literature to describe the internalization of sustainable awareness among organizational members, including employee green behavior, green attitude, environmental consciousness, sustainable behavior and numerous further terminology.60Hameed Aldulaimi, S., Mohammed Yousif Abo Keir & Abdeldayem, M. M. Implementing Green Human Resources Management to Promote Sustainability Development: Application from Telecommunication Companies in Kingdom of Bahrain. Journal of Statistics Applications & Probability 11, 321–330; 10.18576/jsap/110125 (2022).61Hnin, S. W., Javed, A., Karnjana, J., Jeenanunta, C. & Kohda, Y. Workplace sustainability: energy-saving behaviors in office environments of Thailand. Front. Psychol. 16, 1400410; 10.3389/fpsyg.2025.1400410 (2025).62Zacher, H., Rudolph, C. W. & Katz, I. M. Employee Green Behavior as the Core of Environmentally Sustainable Organizations. Annu. Rev. Organ. Psychol. Organ. Behav. 10, 465–494; 10.1146/annurev-orgpsych-120920-050421 (2023).63Liaquat, M. et al. Impact of motivational factors and green behaviors on employee environmental performance. Research in Globalization 8, 100180; 10.1016/j.resglo.2023.100180 (2024).

However, one term is most widely referred to in the literature: “Pro-Environmental Behaviour”.41Saeed, B. B. et al. Promoting employee’s proenvironmental behavior through green human resource management practices. Corp Soc Responsibility Env 26, 424–438; 10.1002/csr.1694 (2019).64Odhiambo, G. M., Waiganjo, E. & Simiyu, A. N. Incentivizing Employee Pro-Environmental Behaviour: Harnessing the Potential of Green Rewards. AJER 4, 601–611; 10.51867/ajernet.4.2.60 (2023).65Ahuja, J., Yadav, M. & Sergio, R. P. Green leadership and pro-environmental behaviour: a moderated mediation model with rewards, self-efficacy and training. International Journal of Ethics and Systems 39, 481–501; 10.1108/IJOES-02-2022-0041 (2023).66Grace Mwamburi Odhiambo, Esther Wangithi Waiganjo & Alice Nanjala Simiyu. Incentivizing Employee Pro-Environmental Behaviour: Harnessing the Potential of Green Rewards. AJER 4, 601–611-601–611 (2023). PEB incorporates the aforementioned alternatives and holistically summarizes the goal of sustainable incentive systems at the individual level. Woo (2021) describes PEB as the actions and routines individuals take to minimize negative environmental impacts and promote sustainable practices.67Woo, E. J. The Necessity of Environmental Education for Employee Green Behavior. East Asian Journal of Business Economics (EAJBE) 9, 29–41; 10.20498/eajbe.2021.9.4.29 (2021). Ture and Ganesh (2014), on the other hand, limit PEB to indirect activities in the workplace and to the natural environment.68Ture, R. S. & Ganesh, M. P. Understanding Pro-environmental Behaviours at Workplace: Proposal of a Model. Asia-Pacific Journal of Management Research and Innovation 10, 137–145; 10.1177/2319510X14536219 (2014). Johnstone and Beusch (2025) take a more integrative approach, considering PEB a target variable alongside traditional organizational economic performance and incorporating both into their definition: “[…] any activity that contributes to an environmentally friendly […] workplace, lifestyle, or society, in addition to the traditional financial security of the organization” (p. 2).20Johnstone, L. & Beusch, P. Motivating sustainable behaviour in the workplace through control. J Manag Control, 1–36; 10.1007/s00187-025-00390-z (2025).

To better understand individual sustainable behaviors in a corporate context, the “Green Five Taxonomy” by Ones et al. (2018) provides a detailed analysis of PEB’s structure. It consists of five meta-categories directly related to incentive systems:

- Transforming behaviours: Adapting and changing products and processes for sustainability,

- Conserving behaviours: Conserving resources through the “3 Rs” (reduce, reuse, recycle),

- Avoiding harm behaviours: Preventing negative environmental impacts,

- Green leadership behaviours: Motivating others to act sustainably,

- Green program behaviours: Initiatives and programs with sustainable goals.64Odhiambo, G. M., Waiganjo, E. & Simiyu, A. N. Incentivizing Employee Pro-Environmental Behaviour: Harnessing the Potential of Green Rewards. AJER 4, 601–611; 10.51867/ajernet.4.2.60 (2023).69Ones, D. S., Wiernik, B. M., Dilchert, S. & Klein, R. M. Multiple domains and categories of employee green behaviours: more than conservation. Chapters, 13–38 (2018).

Thus, PEB encompasses a broad spectrum of actions, ranging from small resource conservation measures to strategic process innovations. By comprehending the factors that influence and promote pro-environmental actions in the workplace, organizations can formulate effective green incentive strategies to encourage PEB.70Aan Hardiyana, Manik, E. & Komara, A. T. Exploring the Impact of Eco-Friendly Leadership and Motivation on Sustainable Workplace Culture and Environmental Effectiveness to Support the Sustainable Development Goals (SDG’s). jlsdgr 5, e02447; 10.47172/2965-730X.SDGsReview.v5.n01.pe02447 (2024). Improved PEB functions as a direct driver for EP which is further elaborated in the following chapter.28Ojo, A. O., Tan, C. N.-L. & Alias, M. Linking green HRM practices to environmental performance through pro-environment behaviour in the information technology sector. Social Responsibility Journal 18, 1–18; 10.1108/SRJ-12-2019-0403 (2022).58Elshaer, I. A., Sobaih, A. E. E., Aliedan, M. & Azazz, A. M. S. The Effect of Green Human Resource Management on Environmental Performance in Small Tourism Enterprises: Mediating Role of Pro-Environmental Behaviors.Sustainability 13, 1956; 10.3390/su13041956 (2021).

2.1.2.2 Environmental performance

In the extant literature, the EP of a company is regarded as a pivotal, overarching objective in the context of organizational incentives for sustainability.26Dahlmann, F., Branicki, L. & Brammer, S. ‘Carrots for Corporate Sustainability’: Impacts of Incentive Inclusiveness and Variety on Environmental Performance. Bus Strat Env 26, 1110–1131; 10.1002/bse.1971 (2017).59Marrucci, L., Daddi, T. & Iraldo, F. Creating environmental performance indicators to assess corporate sustainability and reward employees. Ecological Indicators 158, 111489; 10.1016/j.ecolind.2023.111489 (2024).71Paillé, P., Chen, Y., Boiral, O. & Jin, J. The Impact of Human Resource Management on Environmental Performance: An Employee-Level Study. Journal of Business Ethics 121, 451–466; 10.1007/s10551-013-1732-0 (2014). As research on EP has increased significantly in recent decades, it represents a relevant benchmark for performance evaluation in the measurement of incentive systems.26Dahlmann, F., Branicki, L. & Brammer, S. ‘Carrots for Corporate Sustainability’: Impacts of Incentive Inclusiveness and Variety on Environmental Performance. Bus Strat Env 26, 1110–1131; 10.1002/bse.1971 (2017).59Marrucci, L., Daddi, T. & Iraldo, F. Creating environmental performance indicators to assess corporate sustainability and reward employees. Ecological Indicators 158, 111489; 10.1016/j.ecolind.2023.111489 (2024).72Ali, S., Jiang, J., Rehman, R. u. & Khan, M. K. Tournament incentives and environmental performance: the role of green innovation. Environ Sci Pollut Res 30, 17670–17680; 10.1007/s11356-022-23406-w (2023). This shift in focus means that the evaluation of ecological sustainability moves from the individual to the organizational level.26Dahlmann, F., Branicki, L. & Brammer, S. ‘Carrots for Corporate Sustainability’: Impacts of Incentive Inclusiveness and Variety on Environmental Performance. Bus Strat Env 26, 1110–1131; 10.1002/bse.1971 (2017).27Aftab, J., Abid, N., Cucari, N. & Savastano, M. Green human resource management and environmental performance: The role of green innovation and environmental strategy in a developing country. Bus Strat Env 32, 1782–1798; 10.1002/bse.3219 (2023). Through the use of EP

As posited by Paillé et al. (2014,), the term is defined as “[…] an output demonstrating the degree to which firms are committed to protecting the natural environment” (p. 451), with a particular focus on the efficient use of resources and the reduction of greenhouse gas emissions.71Paillé, P., Chen, Y., Boiral, O. & Jin, J. The Impact of Human Resource Management on Environmental Performance: An Employee-Level Study. Journal of Business Ethics 121, 451–466; 10.1007/s10551-013-1732-0 (2014). In the context of green incentives, these are, for example, standards such as recycling rates, CO2 reduction or energy efficiency.19Derchi, G.-B., Davila, A. & Oyon, D. Green incentives for environmental goals. Management Accounting Research 59, 100830; 10.1016/j.mar.2022.100830 (2023).59Marrucci, L., Daddi, T. & Iraldo, F. Creating environmental performance indicators to assess corporate sustainability and reward employees. Ecological Indicators 158, 111489; 10.1016/j.ecolind.2023.111489 (2024).71Paillé, P., Chen, Y., Boiral, O. & Jin, J. The Impact of Human Resource Management on Environmental Performance: An Employee-Level Study. Journal of Business Ethics 121, 451–466; 10.1007/s10551-013-1732-0 (2014). Nevertheless, a more diverse array of objectives, including new processes or product designs, risk mitigation strategies, and alterations in individual behavior, such as PEB itself, can also be regarded as components of the EP.19Derchi, G.-B., Davila, A. & Oyon, D. Green incentives for environmental goals. Management Accounting Research 59, 100830; 10.1016/j.mar.2022.100830 (2023). As shown in the literature, PEB has a positive influence on EP. It acts as a mediator between the use of green incentives and the enhancement of EP, highlighting the importance of the interplay between EP and PEB.27Aftab, J., Abid, N., Cucari, N. & Savastano, M. Green human resource management and environmental performance: The role of green innovation and environmental strategy in a developing country. Bus Strat Env 32, 1782–1798; 10.1002/bse.3219 (2023).28Ojo, A. O., Tan, C. N.-L. & Alias, M. Linking green HRM practices to environmental performance through pro-environment behaviour in the information technology sector. Social Responsibility Journal 18, 1–18; 10.1108/SRJ-12-2019-0403 (2022).58Elshaer, I. A., Sobaih, A. E. E., Aliedan, M. & Azazz, A. M. S. The Effect of Green Human Resource Management on Environmental Performance in Small Tourism Enterprises: Mediating Role of Pro-Environmental Behaviors.Sustainability 13, 1956; 10.3390/su13041956 (2021). Furthermore, an overarching EP system to measure sustainable progress results in a strengthening of the legitimacy of corresponding decisions, thereby improving the efficiency of incentives and, consequently, the PEB.26Dahlmann, F., Branicki, L. & Brammer, S. ‘Carrots for Corporate Sustainability’: Impacts of Incentive Inclusiveness and Variety on Environmental Performance. Bus Strat Env 26, 1110–1131; 10.1002/bse.1971 (2017).59Marrucci, L., Daddi, T. & Iraldo, F. Creating environmental performance indicators to assess corporate sustainability and reward employees. Ecological Indicators 158, 111489; 10.1016/j.ecolind.2023.111489 (2024).

In contrast to social sustainability dimensions, EP is regarded as comparatively objective, standardised and easily measurable.19Derchi, G.-B., Davila, A. & Oyon, D. Green incentives for environmental goals. Management Accounting Research 59, 100830; 10.1016/j.mar.2022.100830 (2023). It is supported by internationally recognised frameworks such as the Greenhouse Gas Protocol or International Organisation for Standardisation (ISO) 14001 certification, as well as strategic management tools such as the Sustainability Balanced Scorecard (SBSC).73Mio, C., Costantini, A. & Panfilo, S. Performance measurement tools for sustainable business: A systematic literature review on the sustainability balanced scorecard use. Corporate Social Responsibility and Environmental Management 29, 367–384; 10.1002/csr.2206 (2022).74Campos, L. M., Melo Heizen, D. A. de, Verdinelli, M. A. & Cauchick Miguel, P. A. Environmental performance indicators: a study on ISO 14001 certified companies. Journal of Cleaner Production 99, 286–296; 10.1016/j.jclepro.2015.03.019 (2015).75Ali, I., Sami, S., Senan, N. A. M., Baig, A. & Khan, I. A. A study on corporate sustainability performance evaluation and management: The sustainability balanced scorecard. CGOBR 6, 150–162; 10.22495/cgobrv6i2p15 (2022). This enables a company to define quantitative environmental goals and monitor them systematically.19Derchi, G.-B., Davila, A. & Oyon, D. Green incentives for environmental goals. Management Accounting Research 59, 100830; 10.1016/j.mar.2022.100830 (2023).57Maas, K. & Rosendaal, S. Sustainability Targets in Executive Remuneration: Targets, Time Frame, Country and Sector Specification. Bus Strat Env 25, 390–401; 10.1002/bse.1880 (2016).59Marrucci, L., Daddi, T. & Iraldo, F. Creating environmental performance indicators to assess corporate sustainability and reward employees. Ecological Indicators 158, 111489; 10.1016/j.ecolind.2023.111489 (2024).

Evidently EP plays a pivotal role in the operationalisation of environmental sustainability among organizational members. As a control variable in green incentive systems, such as compensation, or as a basis for praise and recognition, it enables the implementation of targeted incentives.19Derchi, G.-B., Davila, A. & Oyon, D. Green incentives for environmental goals. Management Accounting Research 59, 100830; 10.1016/j.mar.2022.100830 (2023).59Marrucci, L., Daddi, T. & Iraldo, F. Creating environmental performance indicators to assess corporate sustainability and reward employees. Ecological Indicators 158, 111489; 10.1016/j.ecolind.2023.111489 (2024).76Paillé, P., Valéau, P. & Carballo-Penela, A. Green rewards for optimizing employee environmental performance: examining the role of perceived organizational support for the environment and internal environmental orientation.Journal of Environmental Planning and Management 66, 2810–2831; 10.1080/09640568.2022.2092723 (2023).

2.2 Historical background

This historical review provides a comprehensive overview of the development of green incentive systems. The review commences with an examination of the origin of classic organizational incentive systems and their subsequent evolution through the lenses of psychology and economics. It then proceeds to demonstrate the gradual integration of sustainability with incentive concepts over the course of several decades, leading up to the present day.

Incentive systems originated from the work of Taylor (1911), who exclusively discussed monetary incentives offered to workers in exchange for increased performance and productivity. The theory assumes that workers are fundamentally unwilling to work and can only be motivated by financial incentives.77Taylor, F. W. The principles of scientific management (Harper & Brothers, New York, 1911).

1950s–1970s

From the mid-20th century onward, this one-dimensional view of incentive systems underwent a fundamental change. Scholars began exploring new theoretical approaches, viewing workers as having needs more complex than just money. Self-fulfillment and the desire for professional and personal growth became important factors in literature on incentives. For example, Herzberg’s (1959) two-factor theory distinguishes between extrinsic motivators, such as pay and working conditions, and intrinsic motivators, such as recognition from organizational members and the assumption of responsibility.78Herzberg, F. The Motivation to Work (John Wiley & Sons, New York, 1959). In his expectancy theory, Vroom (1964) emphasizes that rewards are evaluated subjectively from the perspective of the recipient.79Vroom, V. H. Work and motivation (Wiley, New York, 1964). Exclusive financial incentive systems are increasingly being criticized. New perspectives emerged that focused on the psychological basis of motivation, distinguished between individual and group incentives, and addressed the timing of rewards.80Caudill, H. L. & Porter, C. D. An Historical Perspective of Reward Systems: Lessons Learned from the Scientific Management Era. International Journal of Human Resource Studies 4, 127; 10.5296/ijhrs.v4i4.6605 (2014). Jensen and Meckling (1976) show the role of incentives in their agency theory, where they align the interests of the principals (corporate management) and agents (lower management) by motivating agents to act according to the economic goals of the company.81Jensen, M. C. & Meckling, W. H. Theory of the firm: Managerial behavior, agency costs and ownership structure.Journal of Financial Economics 3, 305–360; 10.1016/0304-405X(76)90026-X (1976).

The publication of The Limits to Growth in 1972, combined with the growing debate on CSR, increased pressure on companies for the first time to take responsibility for their environmental and social impacts.82Meadows, D. H., Meadows, D. L. & Randers, J. The limits to growth: A report for the Club of Rome’s project on the predicament of mankind (Universe Books, New York, 1972). Simultaneously, the US and Europe began setting the first external policy incentives in the form of regulations with mandatory standards, and integrating non-financial aspects into incentive policy became more prevalent.83Gerard, D. & Lave, L. B. Implementing technology-forcing policies: The 1970 Clean Air Act Amendments and the introduction of advanced automotive emissions controls in the United States. Technological Forecasting and Social Change 72, 761–778; 10.1016/j.techfore.2004.08.003 (2005).84Turnock, S. T. et al. The impact of European legislative and technology measures to reduce air pollutants on air quality, human health and climate. Environ. Res. Lett. 11, 24010; 10.1088/1748-9326/11/2/024010 (2016).

1980s – 1990s

In the early 1980s, there was a shift in focus toward companies, which led to the integration of environmental management systems (EMS) for the first time. The aim of this integration was to operationalize environmental goals and integrate them into corporate processes. The successful implementation of an EMS necessitates the motivation and behavioural changes of employees, actively directing attention to internal processes and thus also to an organization’s workforce.51Goldsmith, P. D. & Basak, R. Incentive Contracts and Environmental Performance Indicators. Environmental and Resource Economics 20, 259–279; 10.1023/A:1013065801547 (2001).85Florida, R. & Davison, D. Gaining from Green Management: Environmental Management Systems inside and outside the Factory. California Management Review 43, 64–84; 10.2307/41166089 (2001). Concurrent with the publication of the Brundtland Report by the UN in 1987, there was a marked increase in the integration of EMS.50Brundtland, G. H. Our Common Future: Report of the World Commission on Environment and Development, 1987.51Goldsmith, P. D. & Basak, R. Incentive Contracts and Environmental Performance Indicators. Environmental and Resource Economics 20, 259–279; 10.1023/A:1013065801547 (2001). In the early 1990s, the EU’s Eco-Management and Audit Scheme (EMAS) Regulation, one of the first voluntary, legally regulated EMS, was published.86Franke, J. Political evolution of EMAS: Perspectives from the EU, national governments and industrial groups. Eur. Env. 5, 155–159; 10.1002/eet.3320050602 (1995). Wehrmeyer (1996) emphasizes that the success or failure of companies that wish to integrate environmentally friendly approaches into their business activities is contingent upon the actions of employees.87Wehrmeyer, W. Greening People. Human Resources and Environmental Management (Taylor and Francis, London, 1996). This trend is reinforced on the practical side by the publication of ISO 14001-Norm in 1996 as another internationally applicable EMS, as well as the triple bottom line, which further promotes the development of sustainability-related performance indicators and thus also incentives.52Elkington, J. Accounting for the triple bottom line. Measuring Business Excellence 2, 18–22; 10.1108/eb025539 (1998).88Rondinelli, D. & Vastag, G. Panacea, common sense, or just a label? European Management Journal 18, 499–510; 10.1016/S0263-2373(00)00039-6 (2000). Moreover, during the 1990s, the incorporation of sustainability into business models was increasingly recognized as a strategic asset, enabling companies to enhance their competitiveness and generate additional profits.89Gallarotti, G. M. It pays to be green: The managerial incentive structure and environmentally sound strategies. The Columbia Journal of World Business 30, 38–57; 10.1016/0022-5428(95)90004-7 (1995).

Following this development, leading companies initiated the systematic incorporation of traditional sustainability incentives within their internal compensation structures.90Eccles, R. G., Ioannou, I. & Serafeim, G. The Impact of Corporate Sustainability on Organizational Processes and Performance. Management Science 60, 2835–2857 (2014). One notable example is that of Interface Inc., which incorporated its corporate waste reduction objective into the remuneration of its managers and employees through the implementation of a financial bonus system.91DuBose, J. R. Sustainability and Performance at Interface, Inc. Interfaces 30, 190–201; 10.1287/inte.30.3.190.11665 (2000). Organisation members were incentivized to engage in environmentally friendly activities or activities that support the process of achieving the waste reduction quota. These activities included training and collecting necessary waste data. Furthermore, since 1993, Patagonia has encouraged its employees to engage in environmental initiatives and pursue further education in the domain of sustainability, offering paid time off and bonuses as incentives.92Rattalino, F. Circular advantage anyone? Sustainability‐driven innovation and circularity at Patagonia, Inc.Thunderbird Intl Bus Rev 60, 747–755; 10.1002/tie.21917 (2018).93Ims, K. J. Caring Entrepreneurship and Ecological Conscience—The Case of Patagonia Inc. Caring Management in the New Economy, 197–220; 10.1007/978-3-030-14199-8_11 (2019).

2000s

By the early 2000s, these developments had resulted in more than 14,000 companies worldwide obtaining ISO 14001 certification, indicating a growing commitment to integrating sustainability internally among their workforces.51Goldsmith, P. D. & Basak, R. Incentive Contracts and Environmental Performance Indicators. Environmental and Resource Economics 20, 259–279; 10.1023/A:1013065801547 (2001). Additionally, sustainability goals are increasingly being incorporated into organizational target agreements, Key Performance Indicators (KPI), and compensation systems.94McElhaney, K. A., Toffel, M. W. & Hill, N. Designing a Sustainability Management System at BMW Group: The Designworks/USA Case Study. Greener Management International, 102–116 (2004).95Berrone, P. & Gomez-Mejia, L. R. Environmental Performance and Executive Compensation: An Integrated Agency-Institutional Perspective. AMJ 52, 103–126; 10.5465/amj.2009.36461950 (2009). This emerging trend is also reflected in the development of the first sustainability standard for compensation in the voluntary reporting standard of the Global Reporting Initiative (GRI). In 2002, the initiative published the first standard requiring disclosures on the “[…] linkage between executive compensation and the achievement of the organization’s financial and non-financial goals (e.g., environmental performance, labor practices)” (p. 42).96Global Reporting Initiative. GRI Sustainability Reporting Guidelines 2002, 2002. In the mid-2000s, initial scientific work on the term GHRM made an appearance, drawing attention to human resources as a central force in implementing sustainable strategies.97Jabbour, C. J. C. & Santos, F. C. A. The central role of human resource management in the search for sustainable organizations. The International Journal of Human Resource Management 19, 2133–2154; 10.1080/09585190802479389 (2008).98Renwick, D., Redman, T. & Maguire, S. Green HRM: A review, process model, and research agenda. University of Sheffield Management School Discussion Paper 1, 1–46 (2008). This makes motivating organizational members even more important for sustainability since GHRM largely consists of incentive mechanisms, such as green rewards, recognition, empowerment and training.36Renwick, D. W., Redman, T. & Maguire, S. Green Human Resource Management: A Review and Research Agenda*. Int J Management Reviews 15, 1–14; 10.1111/j.1468-2370.2011.00328.x (2013).97Jabbour, C. J. C. & Santos, F. C. A. The central role of human resource management in the search for sustainable organizations. The International Journal of Human Resource Management 19, 2133–2154; 10.1080/09585190802479389 (2008).98Renwick, D., Redman, T. & Maguire, S. Green HRM: A review, process model, and research agenda. University of Sheffield Management School Discussion Paper 1, 1–46 (2008). The BMW Group is an example of this, as it has had an EMS in accordance with ISO 14001 in all its production facilities worldwide since 1999.94McElhaney, K. A., Toffel, M. W. & Hill, N. Designing a Sustainability Management System at BMW Group: The Designworks/USA Case Study. Greener Management International, 102–116 (2004). The EMS was further expanded into a sustainability management system based on the triple bottom line, which was intended to integrate social and economic aspects in addition to environmental ones. This resulted in incentives for increased performance, as well as non-monetary incentives such as employee empowerment and opportunities for participation. In these programs, employees could contribute their own sustainability ideas to product development or supplier requirements.94McElhaney, K. A., Toffel, M. W. & Hill, N. Designing a Sustainability Management System at BMW Group: The Designworks/USA Case Study. Greener Management International, 102–116 (2004). Concurrently, the performance appraisal system was revised, incorporating sustainability aspects into employee recognition programs.94McElhaney, K. A., Toffel, M. W. & Hill, N. Designing a Sustainability Management System at BMW Group: The Designworks/USA Case Study. Greener Management International, 102–116 (2004). Overall, there has been a shift from purely short-term monetary incentives to non-monetary, participatory incentives, which usually accompanies longer-term changes in the workforce and general corporate culture regarding sustainability.94McElhaney, K. A., Toffel, M. W. & Hill, N. Designing a Sustainability Management System at BMW Group: The Designworks/USA Case Study. Greener Management International, 102–116 (2004).99Fernández, E., Junquera, B. & Ordiz, M. Organizational culture and human resources in the environmental issue: a review of the literature. The International Journal of Human Resource Management 14, 634–656; 10.1080/0958519032000057628 (2003).100Hanna, M. D., Rocky Newman, W. & Johnson, P. Linking operational and environmental improvement through employee involvement. International Journal of Operations & Production Management 20, 148–165; 10.1108/01443570010304233 (2000).

2010s – today

Since the 2010s until the present day, many other large companies have integrated organizational incentive systems into their sustainability strategies.

Patagonia is once again a leading example. In 2011, for instance, the company offered monetary incentives to encourage employees to use bicycles or public transportation instead of private cars. Patagonia also promotes non-monetary incentives, giving its workforce eight weeks off each year to work with environmental groups and gain direct experience with sustainability issues.93Ims, K. J. Caring Entrepreneurship and Ecological Conscience—The Case of Patagonia Inc. Caring Management in the New Economy, 197–220; 10.1007/978-3-030-14199-8_11 (2019). Since 2012, Henkel, a consumer goods and adhesives company, has used the “Sustainability Ambassador Program” as its largest global training program, through which over 50,000 employees have received sustainability training and can contribute their ideas to the planning process.101Henkel. Sustainability ambassador program. Available at https://www.henkel.in/sustainability/initiatives-and-partnerships/sustainability-ambassador-program (2025).

In the domain of sustainability reporting, there is an emerging trend towards regulations that mandate companies to disclose information regarding the integration of sustainability into their compensation systems. In addition to the GRI standards, the European Union, as part of the Corporate Sustainability Reporting Directive, has also published standards for mandatory reporting by leading companies. The European Sustainability Reporting Standards (ESRS) mandate the disclosure of the correlation between the remuneration of administrative, managerial, and supervisory bodies and sustainability targets. Furthermore, they require the disclosure of any relevant training programs in which these bodies have participated.102EFRAG. ESRS 2 General Disclosures. Available at https://www.efrag.org/sites/default/files/media/document/2024-08/ESRS%202%20Delegated-act-2023-5303-annex-1_en.pdf (2025). Additionally, voices in the scientific community increasingly emphasize the effectiveness of incentive systems in anchoring sustainability in companies in the long term.30Liu, J. & Liu, J. The greater the incentives, the better the effect? Interactive moderating effects on the relationship between green motivation and green creativity. IJCHM 35, 919–932; 10.1108/IJCHM-03-2022-0340 (2023).103Ferretti, P., Gonnella, C. & Martino, P. Integrating sustainability in management control systems: an exploratory study on Italian banks. MEDAR 32, 1–34; 10.1108/MEDAR-03-2023-1954 (2024).

However, despite these developments, green incentives offered by companies to organizational members have not yet become a standard tool in corporate sustainability strategies. Studies show that reward and incentive systems are among the least used sustainability management practices.103Ferretti, P., Gonnella, C. & Martino, P. Integrating sustainability in management control systems: an exploratory study on Italian banks. MEDAR 32, 1–34; 10.1108/MEDAR-03-2023-1954 (2024).104Crutzen, N., Zvezdov, D. & Schaltegger, S. Sustainability and management control. Exploring and theorizing control patterns in large European firms. Journal of Cleaner Production 143, 1291–1301; 10.1016/j.jclepro.2016.11.135 (2017). This is particularly evident in the area of sustainability reporting, as one of the most advanced practical areas of organizational sustainability.105Benvenuto, M., Aufiero, C. & Viola, C. A systematic literature review on the determinants of sustainability reporting systems. Heliyon 9, e14893; 10.1016/j.heliyon.2023.e14893 (2023). Information on incentive systems for the workforce accounts for only a small proportion of sustainability reports, which usually only superficially address the remuneration systems of top management, thus hardly covering the extensive topic of incentives. This leaves a lot of room for improvement, considering the diversity of green incentives.106Obereder, L., Müller-Camen, M. & Renwick, D. W. S. GHRM in Sustainability Reporting: An Exploratory Analysis Across Six Countries Using the AMO Framework. Green Human Resource Management Research, 141–166; 10.1007/978-3-031-06558-3_7 (2022).

Overall, the development of organizational incentives for sustainability is still in its infancy and requires much more attention from companies, politicians, and academia in the future in order to be recognized as a classic component of a successful sustainability strategy.6Zhao, Y. & Yang, Y. Sustainability target setting and incentive design: A literature review. BMTP 2, 3134; 10.54517/bmtp3134 (2025).19Derchi, G.-B., Davila, A. & Oyon, D. Green incentives for environmental goals. Management Accounting Research 59, 100830; 10.1016/j.mar.2022.100830 (2023).107Zhu, C., Liu, X., Chen, D. & Yue, Y. Executive compensation and corporate sustainability: Evidence from ESG ratings. Heliyon 10, e32943; 10.1016/j.heliyon.2024.e32943 (2024).

2.3 Theoretical frameworks and literature streams for understanding green incentives

Chapter 3.1.2 shows that relevant theoretical perspectives on green incentive systems, as identified through a comprehensive literature review, can be categorized into two distinct dimensions of sustainability. The discussion commences with an examination of ecological sustainability, which initially encompasses the economic benefits of green incentive systems. Subsequent to this, fundamental theoretical concepts are presented, illustrating the anchoring of economic goals in green incentive systems.

The second relevant strand is ecological sustainability, within which the relevant theories can be divided into the two levels specified in Chapter 3.1.2: behavioural and motivational psychology theories at the individual level, and theories at the organizational level. The thesis aims to provide a comprehensive overview of the functioning and effects of green incentive systems within these two levels.

2.3.1 Green incentives and economic sustainability

In the recent literature, organizational incentives for sustainability are frequently associated with economic sustainability. This association is typically expressed in terms of improved organizational performance and the creation of competitive advantages.1Shahzad, M. A., Du Jianguo & Junaid, M. Impact of green HRM practices on sustainable performance: mediating role of green innovation, green culture, and green employees’ behavior. Environ Sci Pollut Res 30, 88524–88547; 10.1007/s11356-023-28498-6 (2023).45Tariq, S., Jan, F. A. & Ahmad, M. S. Green employee empowerment: a systematic literature review on state-of-art in green human resource management. Qual Quant 50, 237–269; 10.1007/s11135-014-0146-0 (2016).108AlKetbi, A. & Rice, J. The Impact of Green Human Resource Management Practices on Employees, Clients, and Organizational Performance: A Literature Review. Administrative Sciences 14, 78; 10.3390/admsci14040078 (2024). This process is subsequently addressed by the Natural Resource-Based View (NRBV) and employee retention, demonstrating why the use of green incentives can be economically lucrative for companies. In the following section, the various methodologies employed by green incentive systems will be delineated, with particular reference to the economic tenets of agency and stewardship theory. The final section of this study illustrates the possibility of jointly considering ecological and economic goals with the help of multi-task agency theory.

2.3.1.1 Economic sustainability: A natural resource-based view

Prior to an examination of fundamental theories, the economic sustainability perspective is presented in the context of organizational green incentive systems and their promotion of PEB and EP. In this regard, the NRBV perspective, as outlined by Hart (1995), is discussed.109Hart, S. L. A Natural-Resource-Based View of the Firm. AMR 20, 986; 10.2307/258963 (1995). This perspective links the economic implications of green incentives to the process of ecological transformation.109Hart, S. L. A Natural-Resource-Based View of the Firm. AMR 20, 986; 10.2307/258963 (1995).

The NRBV is predicated on the Resource Based View as conceptualised by Barney (1991).110Barney, J. Firm Resources and Sustained Competitive Advantage. Journal of Management 17, 99–120; 10.1177/014920639101700108 (1991). The theory posits that sustainable competitive advantages that assist organizations can be obtained through the utilisation of their unique internal resources. As Barney (1991) asserts, these resources must be valuable, difficult to imitate and embedded in the organization. In the context of incentive systems, the focus is primarily on strategically important human resources, more specifically on intangible, knowledge-based resources such as skills, experience and employee motivation, and the resulting positive effects on organizational performance.110Barney, J. Firm Resources and Sustained Competitive Advantage. Journal of Management 17, 99–120; 10.1177/014920639101700108 (1991).

This perspective is adopted by the NRBV, which builds upon the Resource Based View theory by contending that enterprises that incorporate environmental concerns into their fundamental strategy demonstrate enhanced resilience and competitiveness over the long term.89Gallarotti, G. M. It pays to be green: The managerial incentive structure and environmentally sound strategies. The Columbia Journal of World Business 30, 38–57; 10.1016/0022-5428(95)90004-7 (1995).109Hart, S. L. A Natural-Resource-Based View of the Firm. AMR 20, 986; 10.2307/258963 (1995). The key strategic implications of the NRBV are as follows:

- Pollution prevention: increasing efficiency by reducing waste and emissions,

- Product stewardship: responsibility throughout the entire life cycle of products,

- Sustainable development: building new skills and resources that secure the long-term relationship between companies and the environment.109Hart, S. L. A Natural-Resource-Based View of the Firm. AMR 20, 986; 10.2307/258963 (1995).

Green incentive systems promote all three of these perspectives in different ways, starting with pollution prevention. As outlined in Chapter 3.1.2.2, resource conservation and the reduction of energy usage are identified as pivotal objectives within green incentive systems.19Derchi, G.-B., Davila, A. & Oyon, D. Green incentives for environmental goals. Management Accounting Research 59, 100830; 10.1016/j.mar.2022.100830 (2023).59Marrucci, L., Daddi, T. & Iraldo, F. Creating environmental performance indicators to assess corporate sustainability and reward employees. Ecological Indicators 158, 111489; 10.1016/j.ecolind.2023.111489 (2024).71Paillé, P., Chen, Y., Boiral, O. & Jin, J. The Impact of Human Resource Management on Environmental Performance: An Employee-Level Study. Journal of Business Ethics 121, 451–466; 10.1007/s10551-013-1732-0 (2014). The PEB also places emphasis on the conservation of resources at the individual level.64Odhiambo, G. M., Waiganjo, E. & Simiyu, A. N. Incentivizing Employee Pro-Environmental Behaviour: Harnessing the Potential of Green Rewards. AJER 4, 601–611; 10.51867/ajernet.4.2.60 (2023).69Ones, D. S., Wiernik, B. M., Dilchert, S. & Klein, R. M. Multiple domains and categories of employee green behaviours: more than conservation. Chapters, 13–38 (2018). The potential financial benefits of energy savings have been well documented, and the same is true of the economic advantages of reducing waste, which can also lead to a reduction in material costs.25Beck-Krala, E. & Klimkiewicz, K. Reward Programs Supporting Environmental Organizational Policy. Zarządzanie Zasobami Ludzkimi, 41–54 (2017).65Ahuja, J., Yadav, M. & Sergio, R. P. Green leadership and pro-environmental behaviour: a moderated mediation model with rewards, self-efficacy and training. International Journal of Ethics and Systems 39, 481–501; 10.1108/IJOES-02-2022-0041 (2023).111Austrup, D. & Blomberg, C. von. Anreiz- und Vergütungssysteme: Verlockung zur Nachhaltigkeit. CSR und Finance, 83–94; 10.1007/978-3-642-54882-6_5 (2014).