Authors: Dascha Kinder

Edited by: –

Last updated: January 2, 2026

Executive summary

Short-termism refers to prioritizing short-term gains over long-term value creation, often at the expense of sustainability, innovation, and social responsibility. This article explores its definition, drivers, cultural and industry influences, consequences, and potential solutions.

Key drivers include investor behavior, such as speculative trading and earnings-based investment, and managerial practices influenced by market pressure, career incentives, compensation structures, and cognitive biases. Cultural factors like temporal orientation and individualism, as well as industry characteristics, further shape susceptibility to short-termism.

Consequences are profound: companies sacrifice R&D, innovation, and employee well-being, while society faces reduced economic growth and ecological harm. At the macro level, widespread short-termism undermines competitiveness and sustainability efforts.

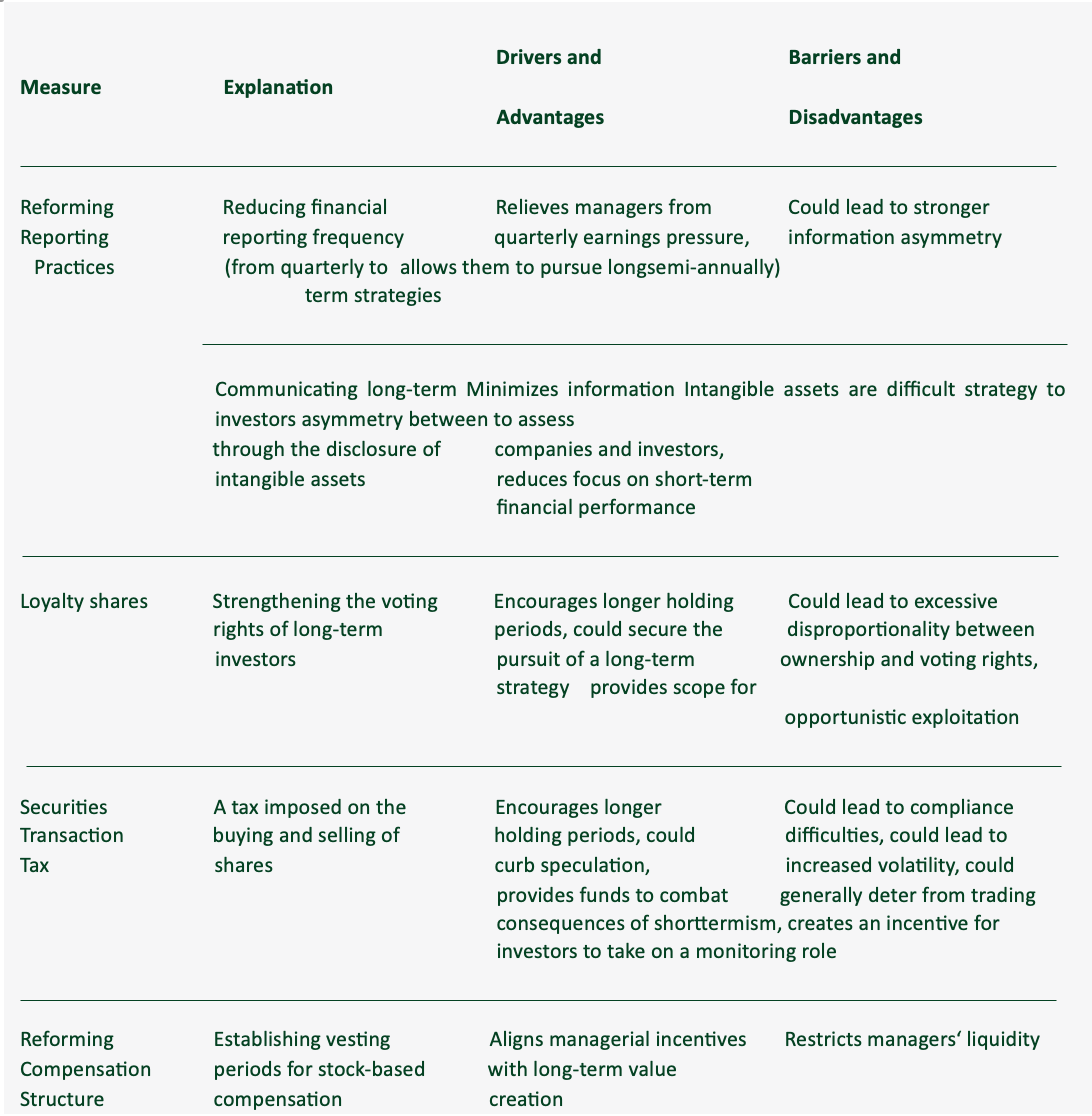

Solutions include reforming reporting practices to reduce pressure from quarterly earnings, introducing loyalty shares to reward long-term investors, implementing securities transaction taxes to discourage speculation, and restructuring executive compensation to align with long-term goals. Enhanced disclosure of intangible assets and promoting green innovation are also critical.

Future research should refine measurement methods, explore cross-cultural differences, and examine social and ecological impacts in greater depth. Addressing short-termism is essential for organizations seeking sustainable success and resilience in a dynamic global economy.

1 Introduction

Over the past few decades, the topic of short-termism has received increasing attention. Short-termism arises when companies prioritize short-term profit maximization at the expense of long-term development.1Laverty, K. J. Economic “Short-Termism”: The Debate, The Unresolved Issues, and The Implications for Management Practice and Research. The Academy of Management Review, 21, 825–860 (1996). The 2008 financial crisis demonstrated on a large scale the impact that this behavior can have on both the economy and society, leading to adverse effects on disposable income, employment, real estate and retirement plans.2Dallas, L. L. Short-Termism, the Financial Crisis, and Corporate Governance. The Journal of Corporation Law 37, 265 (2012). But how can this seemingly irrational behavior be explained? What drives companies to continue engaging in practices that actively harm their future prospects? And can something be done about it? This paper sets out to address these questions. The motivation lies in gaining an understanding of the influence that short-termism has on economic decision-making and the problems that arise from it.

The debate surrounding short-termism is particularly relevant in light of the sustainability movement. Sustainable development is naturally linked to a long-term perspective. An excessive short-term orientation can therefore have adverse effects. This applies to companies and the economy on the one hand, and to efforts in corporate social responsibility on the other.3Galbreath, J. The Impact of Board Structure on Corporate Social Responsibility: A Temporal View. Business Strategy and the Environment 26, 358–370 (2017).,4Terry, S. J. The Macro Impact of Short‐Termism. Econometrica 91, 1881–1912 (2023). Corporate social responsibility requires companies to broaden their perspective beyond profit maximization and address ethical concerns, including investments in environmental and social sustainability, which often conflict with short-term profitability.3Galbreath, J. The Impact of Board Structure on Corporate Social Responsibility: A Temporal View. Business Strategy and the Environment 26, 358–370 (2017).,5Barnett, M. L. Stakeholder influence capacity and the variability of financial returns to corporate social responsibility. The Academy of Management Review 32, 794–816 (2007). To ensure sustainable development and facilitate sustainable business practices, it is essential to understand and address the influence of short-termism.

This is the subject of this paper. To this end, short-termism is first defined to provide an overall understanding of the phenomenon. In this context, it is examined how shortterm and long-term goals can diverge and why they are not necessarily compatible. Then, it is described what specific measures are taken as a result of short-termism. To provide a comprehensive understanding of the concept, political short-termism will also be briefly explored. After a historical overview of the academic debate is outlined, a literature review presents the key findings of that debate. First, the drivers of shorttermism are systematically explored. Then, the influence of culture and industry affiliation on short-termism is analyzed. The literature review concludes with an examination of the consequences and future research directions. The subsequent chapter is devoted to measures that are discussed as possible solutions to short-termism.

The work primarily refers to the American economic system and its companies, as this constitutes the main research subject examined in the literature.

2 Understanding short-termism

2.1 Definition

The most sensible course of action in the short term does not always coincide with the ideal long-term strategy.1Laverty, K. J. Economic “Short-Termism”: The Debate, The Unresolved Issues, and The Implications for Management Practice and Research. The Academy of Management Review, 21, 825–860 (1996). Decision-makers are therefore often faced with a trade-off, having to decide which strategy to pursue.1Laverty, K. J. Economic “Short-Termism”: The Debate, The Unresolved Issues, and The Implications for Management Practice and Research. The Academy of Management Review, 21, 825–860 (1996). Short-termism refers to the situation where actions primarily focused on the short term have a negative impact in the long run.1Laverty, K. J. Economic “Short-Termism”: The Debate, The Unresolved Issues, and The Implications for Management Practice and Research. The Academy of Management Review, 21, 825–860 (1996). This raises the question of what this trade-off entails. How can a decision be the best option in the short term but lead to a poor outcome in the future, and vice versa?

The answer lies in the nature of intertemporal choices, a type of decision that is characterized by a time-lagged separation of costs and benefits.6Loewenstein, G. & Thaler, R. H. Anomalies: Intertemporal Choice. The Journal of Economic Perspectives 3, 181–193 (1989). Intertemporal choices are commonplace for managers, as they typically occur in connection with technology investments, workforce training, and the development of new markets.1Laverty, K. J. Economic “Short-Termism”: The Debate, The Unresolved Issues, and The Implications for Management Practice and Research. The Academy of Management Review, 21, 825–860 (1996). In the context of corporate short-termism, such choices generally involve costs that are incurred immediately while payoffs lie in the distant future.1Laverty, K. J. Economic “Short-Termism”: The Debate, The Unresolved Issues, and The Implications for Management Practice and Research. The Academy of Management Review, 21, 825–860 (1996). Therein lies the central conflict of objectives. Investing in long-term-oriented projects compromises the prospects of short-term profit maximization without offering immediate returns.1Laverty, K. J. Economic “Short-Termism”: The Debate, The Unresolved Issues, and The Implications for Management Practice and Research. The Academy of Management Review, 21, 825–860 (1996). If a manager pursues the optimal short-term strategy, they are therefore incentivized to cut costs by rejecting long-term-oriented investments.7Smulowitz, S.J. & Cossin, D. & Lu, H. Managerial Short-Termism and Corporate Social Performance: The Moderating Role of External Monitoring. Journal of Business Ethics 188, 759–778 (2023). The inherent characteristics of long-term investments reinforce this dynamic, as they require an extended planning horizon. However, future developments can only be predicted and accounted for to a limited extent.8Holmstrom, B. Agency costs and innovation. Journal of Economic Behavior & Organization, 12, 305–327 (1989). The results are therefore uncertain and may fail to occur completely.1Laverty, K. J. Economic “Short-Termism”: The Debate, The Unresolved Issues, and The Implications for Management Practice and Research. The Academy of Management Review, 21, 825–860 (1996).,7Smulowitz, S.J. & Cossin, D. & Lu, H. Managerial Short-Termism and Corporate Social Performance: The Moderating Role of External Monitoring. Journal of Business Ethics 188, 759–778 (2023).

Nevertheless, these long-term initiatives have the potential to increase the value of the company.1Laverty, K. J. Economic “Short-Termism”: The Debate, The Unresolved Issues, and The Implications for Management Practice and Research. The Academy of Management Review, 21, 825–860 (1996).,2Dallas, L. L. Short-Termism, the Financial Crisis, and Corporate Governance. The Journal of Corporation Law 37, 265 (2012). If such initiatives are forgone in favor of short-term gains, there might be negative consequences for the overall long-term development.2Dallas, L. L. Short-Termism, the Financial Crisis, and Corporate Governance. The Journal of Corporation Law 37, 265 (2012).,7Smulowitz, S.J. & Cossin, D. & Lu, H. Managerial Short-Termism and Corporate Social Performance: The Moderating Role of External Monitoring. Journal of Business Ethics 188, 759–778 (2023). Therefore, the most beneficial strategy for the long run is to invest in long-term expenditure, while cutting costs is more desirable in the short term.7Smulowitz, S.J. & Cossin, D. & Lu, H. Managerial Short-Termism and Corporate Social Performance: The Moderating Role of External Monitoring. Journal of Business Ethics 188, 759–778 (2023). In summary, short-termism manifests itself primarily through the avoidance of value-enhancing initiatives that reduce profits in the short term. In practice, this is particularly evident in the reduction of discretionary expenditure.9Graham, J. R. & Harvey, C. R. & Rajgopal, S. Value Destruction and Financial Reporting Decisions. Financial Analysts Journal 62, 27–39 (2006).

2.2 Operational expressions of short-termism

In particular, a sharp reduction in discretionary research and development (R&D) investments is considered a clear indicator of short-termism.10Wiersema, M. & Koo, H. & Chen, W. & Zhang, Y. Corporate Short-Termism: A Review and Research Agenda. Journal of Management 51, 2389–2418 (2025). Indeed, a large part of empirical research relies on R&D expenditure as a means to determine the prevalence of short-termism.10Wiersema, M. & Koo, H. & Chen, W. & Zhang, Y. Corporate Short-Termism: A Review and Research Agenda. Journal of Management 51, 2389–2418 (2025). The reason companies target R&D as a cost-cutting measure is that these costs must be expensed immediately in accordance with US accounting guidelines.4Terry, S. J. The Macro Impact of Short‐Termism. Econometrica 91, 1881–1912 (2023).,11Bushee, B. J. The Influence of Institutional Investors on Myopic R&D Investment Behavior. The Accounting Review 73, 305–333 (1998). This does not apply to tangible, which are depreciated over several years.4Terry, S. J. The Macro Impact of Short‐Termism. Econometrica 91, 1881–1912 (2023). R&D expenditures, therefore, negatively impact short-term financial performance. The benefits, however, unfold over time and could even fail to occur entirely.4Terry, S. J. The Macro Impact of Short‐Termism. Econometrica 91, 1881–1912 (2023). Consequently, R&D offers considerable scope for opportunistic cutbacks. Nevertheless, efficient investments in R&D are central to future success.12Shen, C. H. & Zhang, H. CEO risk incentives and firm performance following R&D increases. Journal of Banking & Finance 37, 1176–1194 (2013). If companies cut these costs, they display a discernible preference for the short-term at the expense of the long-term.10Wiersema, M. & Koo, H. & Chen, W. & Zhang, Y. Corporate Short-Termism: A Review and Research Agenda. Journal of Management 51, 2389–2418 (2025).

However, short-termism is not limited to cuts in R&D expenditure. Typical measures also include reducing other discretionary expenses, such as marketing, employee training, and maintenance.2Dallas, L. L. Short-Termism, the Financial Crisis, and Corporate Governance. The Journal of Corporation Law 37, 265 (2012).,9Graham, J. R. & Harvey, C. R. & Rajgopal, S. Value Destruction and Financial Reporting Decisions. Financial Analysts Journal 62, 27–39 (2006).,13Mizik, N. The Theory and Practice of Myopic Management. Journal of Marketing Research 47, 594–611 (2010). Additionally, downsizing initiatives could be pursued, resulting in the loss of qualified personnel.2Dallas, L. L. Short-Termism, the Financial Crisis, and Corporate Governance. The Journal of Corporation Law 37, 265 (2012). The underlying principle remains the same, as these intangible investments are expensed instead of capitalized.2Dallas, L. L. Short-Termism, the Financial Crisis, and Corporate Governance. The Journal of Corporation Law 37, 265 (2012). They pose significant value-enhancing potential, which is disregarded due to short-term unprofitability.2Dallas, L. L. Short-Termism, the Financial Crisis, and Corporate Governance. The Journal of Corporation Law 37, 265 (2012). Moreover, the resulting benefits are often intangible, making their contributions to future success hard to assess.2Dallas, L. L. Short-Termism, the Financial Crisis, and Corporate Governance. The Journal of Corporation Law 37, 265 (2012). By cutting such expenditures, companies impair the cash flow that would otherwise be expected in the future.14Milano, G. Corporate Short‐Termism and How It Happens. Journal of Applied Corporate Finance 30, 27–35 (2018).

One practice that is also attributable to short-termism but is of a different nature is stock buybacks. By buying back their shares on a large scale, companies artificially increase their earning per share and share price. However, this is problematic because the financial resources could otherwise have been invested in long-term growth.15Martin, R. L. Yes, short-termism really is a problem. Harvard Business Review October (2015). To illustrate the scope of the problem: from 2003 to 2012, US companies in the S&P 500 collectively spent over $2.4 trillion on stock buybacks.16Lazonick, W. Profits Without Prosperity. Harvard Business Review September (2014). That constitutes 54% of their earnings.16Lazonick, W. Profits Without Prosperity. Harvard Business Review September (2014). Short-termism, therefore, has a significant influence on prevailing economic practices and strategies.

2.3 Political short-termism

However, short-termism is not purely an economic phenomenon, as it can also be observed in a political context. Corporate short-termism refers to internal company decisions characterized by long-term financial investments in tension with short-term profitability.1Laverty, K. J. Economic “Short-Termism”: The Debate, The Unresolved Issues, and The Implications for Management Practice and Research. The Academy of Management Review, 21, 825–860 (1996). Political short-termism, on the other hand, focuses on policymakers. The tension here is that long-term policies with societal benefits often require short-term consumer sacrifices. Voters are thus burdened in the short term, often during a transition phase, but only experience the benefits later.17Gersbach, H. Incentive Contracts and Elections for Politicians and the DownUp Problem. Studies in Economic Design: Advances in Economic Design, edited by Sertel, M. R. and Koray, S. Springer-Verlag Berlin Heidelberg, 65-76 (2003). An example of this is the restructuring of the labor market, which would lead to job losses in the short term but reduce the unemployment rate in the long term.17Gersbach, H. Incentive Contracts and Elections for Politicians and the DownUp Problem. Studies in Economic Design: Advances in Economic Design, edited by Sertel, M. R. and Koray, S. Springer-Verlag Berlin Heidelberg, 65-76 (2003). Politicians, aiming to be re-elected, might not want to pursue such initiatives. The reason for this lies in the inefficiency of political processes, as elections in their current form do not sufficiently motivate longterm behavior.18Müller, M. Motivation of Politicians and Long-Term Policies. Public Choice 132, 273–289 (2007). Due to information asymmetries, voters cannot see what efforts are being invested in long-term policies.19Bonfiglioli, A. & Gancia, G. Uncertainty, Electoral Incentives and Political Myopia. The Economic Journal (London) 123, 373–400 (2013). Therefore, voters evaluate politicians based on their performance in the current and past legislative period.19Bonfiglioli, A. & Gancia, G. Uncertainty, Electoral Incentives and Political Myopia. The Economic Journal (London) 123, 373–400 (2013). With regard to re-election, politicians are, therefore, incentivized to act in a short-term-oriented manner. Shortterm performance signals their competence to voters, making re-election more likely.19Bonfiglioli, A. & Gancia, G. Uncertainty, Electoral Incentives and Political Myopia. The Economic Journal (London) 123, 373–400 (2013). Political and corporate short-termism are therefore closely linked, characterized by adiscrepancy between long-term and short-term benefits. Nevertheless, the academic debate on short-termism is divided into two strands of research. This paper focuses on the debate on corporate short-termism, which commenced over 40 years ago.

2.4 Historic overview

Hayes and Abernathy (1980) were among the first to raise the issue that would come to be known as short-termism. In their influential 1980 article, they discuss the decline of American competitive vigor. In particular, they criticize the excessive focus on short-term cost reduction among American companies, leading them to fall behind their international competitors.20Hayes, R. H. & Abernathy, W. J. Managing Our Way to Economic Decline. Harvard Business Review 58, 67-77 (1980). Upon its publication, the article brought the topic into public consciousness.10Wiersema, M. & Koo, H. & Chen, W. & Zhang, Y. Corporate Short-Termism: A Review and Research Agenda. Journal of Management 51, 2389–2418 (2025). Over time, interest in the topic has repeatedly flared up due to socio-economic developments. These include the financial scandals of the early 2000s, namely those involving the companies Enron and WolrdCom. These incidents demonstrated the harmful consequences of short-term behavior.2Dallas, L. L. Short-Termism, the Financial Crisis, and Corporate Governance. The Journal of Corporation Law 37, 265 (2012). The societal shift towards sustainability has likewise increased interest in the short-termism debate, sparking research into its environmental effects.21Slawinski, N. & Pinkse, J. & Busch, T. & Banerjee, S. B. The Role of Short-Termism and Uncertainty Avoidance in Organizational Inaction on Climate Change: A Multi-Level Framework. Business & Society 56, 253–282 (2017). The general disquiet regarding shorttermism intensified in the course of the global economic crisis of 2008.22Marinovic, I. & Varas, F. CEO Horizon, Optimal Pay Duration, and the Escalation of Short-Termism. The Journal of Finance (New York) 74, 2011–2053 (2019). Leading up to the crisis, short-term oriented behavior became rampant.2Dallas, L. L. Short-Termism, the Financial Crisis, and Corporate Governance. The Journal of Corporation Law 37, 265 (2012). The inevitable crash had detrimental consequences for the economy as well as overall society.2Dallas, L. L. Short-Termism, the Financial Crisis, and Corporate Governance. The Journal of Corporation Law 37, 265 (2012).

However, the debate is complex. Short-termism does not arise from a simple causeand-effect structure but is instead multifaceted.15Martin, R. L. Yes, short-termism really is a problem. Harvard Business Review October (2015). The complexity of the dynamics leads to contradictory assessments and ambiguous results.15Martin, R. L. Yes, short-termism really is a problem. Harvard Business Review October (2015). Within the academic discourse, there is some disagreement regarding the existence of the phenomenon as well as its consequences.15Martin, R. L. Yes, short-termism really is a problem. Harvard Business Review October (2015). Nevertheless, a dominant research direction can be identified, as researchers generally conclude that short-termism is a real problem that is detrimental to long-term development. Their contributions to the academic debate aim to identify the causes of such behavior and provide empirical evidence for its existence. This paper sets out to reflect the current state of the discourse. To this end, the following chapters present the findings that have been consolidated to date.

3 Drivers of short-termism

The core of the debate revolves around identifying the causes of the issue. Summarizing the previous findings, short-termism manifests itself in short-sighted resource allocation. The drivers of short-termism can therefore be assumed to lie within capital allocation mechanisms. As early as 1992, Porter criticized the inefficient allocation of financial resources and identified it as the cause of short-termism.23Porter, M. E. Capital Disadvantage: America’s Failing Capital Investment System. Harvard Business Review 70, 65–83 (1992). A detailed look at said capital allocation mechanisms reveals a division into two distinct markets, the external and internal capital markets. Through the external market, companies obtain financial resources.23Porter, M. E. Capital Disadvantage: America’s Failing Capital Investment System. Harvard Business Review 70, 65–83 (1992). The short-termism debate primarily focuses on public equity providers, hereafter referred to as investors. The generated funds are then distributed within the company via the internal capital market. It falls within the remit of management to allocate these resources to particular investment programs.23Porter, M. E. Capital Disadvantage: America’s Failing Capital Investment System. Harvard Business Review 70, 65–83 (1992).

In view of this dual structure, an examination of short-termism drivers requires a bilateral perspective. Therefore, this paper sets out to examine the causes firstly at the investor level and then at the management level. This division coincides with the literary findings, as there is a general viewpoint that short-termism can be traced back to the interlocking practices of these two groups.24Palley, T. I. Managerial turnover and the theory of short-termism. Journal of Economic Behavior & Organization32, 547–557 (1997).,25Moore, M. T. & Walker-Arnott, E. A Fresh Look at Stock Market Shorttermism. Journal of Law and Society 41, 416–445 (2014).

3.1 Investors

The subject of this chapter is the short-sightedness of the external capital market. However, to examine the practices of investors, the market dynamics in which they operate must first be analyzed, as these provide the framework for possible investment behavior and strategic approaches.

3.1.1 Capital market dynamics

An examination of these market dynamics leads to the central insight that technological progress has caused structural change on a market-wide scale. Specifically, the establishment of highly automated computer-driven trading networks has made markets globally accessible and accelerated trade. These market evolutions enable investors to considerably increase their stock turnover.2Dallas, L. L. Short-Termism, the Financial Crisis, and Corporate Governance. The Journal of Corporation Law 37, 265 (2012).,26Roe, M. J. Corporate Short-Termism-In the Boardroom and in the Courtroom. The Business Lawyer 68, 977–1006 (2013).,27Jacobs, M. Short-term America: The Causes and Cures of Our Business Myopia. Boston: Harvard Business School Press (1991). In 2016, stocks were being held for an average of eight months, a significant decrease compared to the pre-digital age. To put this into perspective, in 1960, stocks were held for an average of seven years.28Ortiz‐de‐Mandojana, N. & Bansal, P. & Aragón‐Correa, J.A. Older and Wiser: How CEOs’ Time Perspective Influences Long‐Term Investments in Environmentally Responsible Technologies. British Journal of Management 30, 134–150 (2019). Such shortened holding periods are naturally linked to increased trading. The volume of shares traded over three months in 1960 is the same as the volume traded on a single day in 1990.27Jacobs, M. Short-term America: The Causes and Cures of Our Business Myopia. Boston: Harvard Business School Press (1991). The American tax structure enables this practice, as the transactions themselve are not taxed at all.2Dallas, L. L. Short-Termism, the Financial Crisis, and Corporate Governance. The Journal of Corporation Law 37, 265 (2012).,29Schwert, G. W. & Seguin, P. J. Securities Transaction Taxes: An Overview of Costs, Benefits and Unresolved Questions. Financial Analysts Journal 49, 27–35 (1993). The prevalence of such rapid trading has led to stocks being treated as commodities instead of long-term investments rooted in ongoing business relationships.27Jacobs, M. Short-term America: The Causes and Cures of Our Business Myopia. Boston: Harvard Business School Press (1991). As Jacobs (1991) observes “Simply buying and selling individual stocks to hold as long-term investments is a fading tradition.”27Jacobs, M. Short-term America: The Causes and Cures of Our Business Myopia. Boston: Harvard Business School Press (1991).(p.17).

This change in the status quo constitutes the core of the short-termism problem on the part of the investors.26Roe, M. J. Corporate Short-Termism-In the Boardroom and in the Courtroom. The Business Lawyer 68, 977–1006 (2013). Short holding periods decouple the interests of investors from the long-term development of the firms. Since investors sell their shares after brief periods of time, there is no incentive for them to be concerned with the future of the company beyond their holding duration.14Milano, G. Corporate Short‐Termism and How It Happens. Journal of Applied Corporate Finance 30, 27–35 (2018). The commoditization of share trading has led investors to become increasingly detached from the actual businesses they fund, often being unaware of business details.1Laverty, K. J. Economic “Short-Termism”: The Debate, The Unresolved Issues, and The Implications for Management Practice and Research. The Academy of Management Review, 21, 825–860 (1996). Instead, their focus lies on strong corporate results achieved during their limited time as shareholders.26Roe, M. J. Corporate Short-Termism-In the Boardroom and in the Courtroom. The Business Lawyer 68, 977–1006 (2013). In contrast, research shows that a high proportion of long-term investors is linked to long-term strategic measures. The measures include entering new markets, launching new products, and creating a unique corporate strategy.10Wiersema, M. & Koo, H. & Chen, W. & Zhang, Y. Corporate Short-Termism: A Review and Research Agenda. Journal of Management 51, 2389–2418 (2025). It can therefore be concluded that the rise of limited equity holding periods leads to short-termism. To give an accurate picture of market dynamics, it must be emphasized that not all investors are short-term oriented. However, due to the possibilities arising from technological change, short-term strategies are becoming increasingly dominant.

In addition to high turnover, the modern capital market is also characterized by institutional investors, a type of investor who manages capital investments on behalf of third parties. Institutional investors include investment funds, hedge funds, banks, pension funds, and insurance companies, among others.30Johnson, R. A. & Schnatterly, K. & Johnson, S. G. & Chiu, S.C. Institutional Investors and Institutional Environment: A Comparative Analysis and Review. Journal of Management Studies 47, 1590–1613 (2010).,31Lewellen, J. Institutional investors and the limits of arbitrage. Journal of Financial Economics 102, 62–80 (2011). This type of investor is becoming increasingly common on stock markets worldwide.30Johnson, R. A. & Schnatterly, K. & Johnson, S. G. & Chiu, S.C. Institutional Investors and Institutional Environment: A Comparative Analysis and Review. Journal of Management Studies 47, 1590–1613 (2010). In 1950, their combined share of US corporate equity was 8% and it has steadily risen since.23Porter, M. E. Capital Disadvantage: America’s Failing Capital Investment System. Harvard Business Review 70, 65–83 (1992). By 1990, their collective share of equity had reached 60%.23Porter, M. E. Capital Disadvantage: America’s Failing Capital Investment System. Harvard Business Review 70, 65–83 (1992). As of 2017, institutional investors collectively held around 80% of the S&P. Consequently, they now constitute the majority of equity shareholders.

It is argued that the increased influence of institutional investors has led to a greater degree of short-termism.11Bushee, B. J. The Influence of Institutional Investors on Myopic R&D Investment Behavior. The Accounting Review 73, 305–333 (1998). This can be explained by the separation of capital management and ownership. Proponents of this view argue that institutional investors primarily act as traders and therefore have an exessive focus on short-term results.11Bushee, B. J. The Influence of Institutional Investors on Myopic R&D Investment Behavior. The Accounting Review 73, 305–333 (1998). The specific incentives for institutional investors to prioritize short-term gains may vary by investor type. Mutual funds may be interested in achieving strong short-term results to attract new clients. Pension funds may be inclined to do so to renew their management contracts and secure new ones. Meanwhile, hedge fund compensation is often based on short-term results.26Roe, M. J. Corporate Short-Termism-In the Boardroom and in the Courtroom. The Business Lawyer 68, 977–1006 (2013).

Institutional investors typically own a relatively large share of a company’s stock, which entitles them to corresponding voting rights. Compared to “dispersed individual investors”32 (p.1276), they therefore have more influence on corporate strategy. They can thus take an activist role and push for short-term performance.32Anabtawi, I. & Stout, L. Fiduciary Duties for Activist Shareholders. Stanford Law Review 60, 1255–1308 (2008).

However, empirical evidence suggests that a more nuanced view is required. Bushee (1998) provides empirical research showing that a high proportion of institutional ownership is associated with less reduction in R&D expenditure. This is due to the fact that institutional investors oftentimes take on a monitoring role. He also finds that this does not apply to institutional investors with high portfolio turnover that engage in momentum trading. These investors increase the probability of reducing long-term oriented investments. The widespread assumption that institutional investors facilitate short-termism can therefore only be partially confirmed. The results suggest that institutional investors are not a homogeneous group and employ different investment strategies.11Bushee, B. J. The Influence of Institutional Investors on Myopic R&D Investment Behavior. The Accounting Review 73, 305–333 (1998). Accordingly, the practices they use should be examined in particular to understand the causes of short-termism.

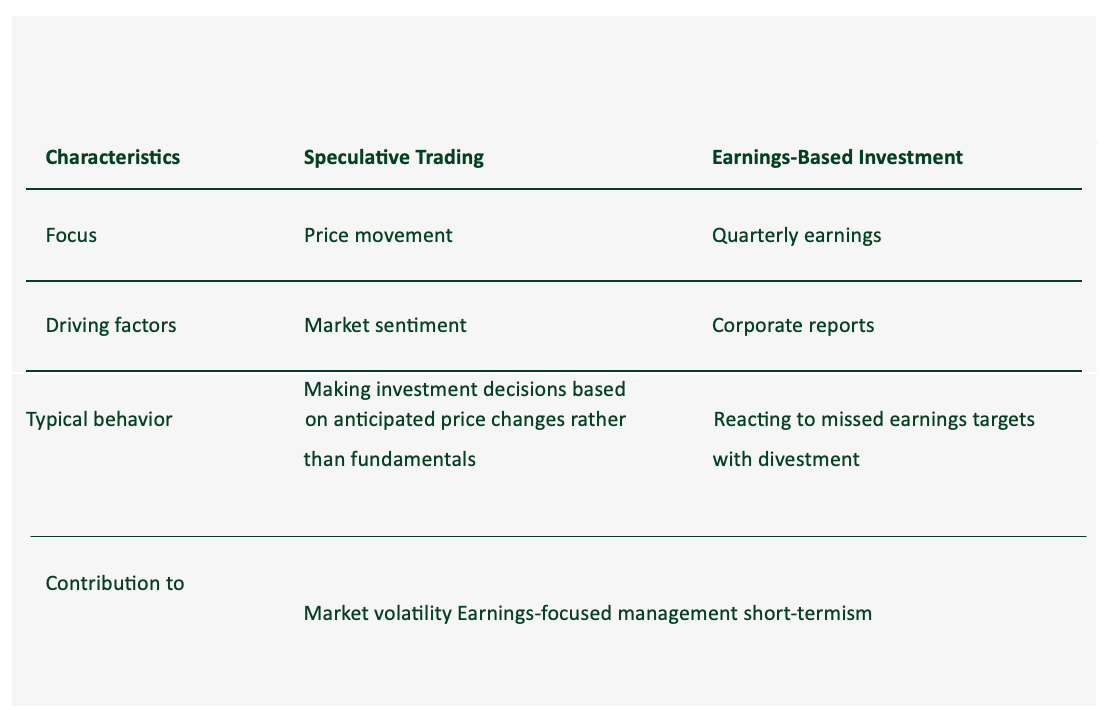

Among the practices used by investors, two are particularly relevant for investor shorttermism. As Moore and Walker-Arnott (2014) explain, investors’ short-termism generally takes form in either speculative trading or earnings-based investment. Although there is a partial overlap between these two practices, they can nevertheless be distinguished from each other. They each contribute to the short-termism problem in different ways.25Moore, M. T. & Walker-Arnott, E. A Fresh Look at Stock Market Shorttermism. Journal of Law and Society 41, 416–445 (2014). These two practices are not exclusive to institutional investors. However, as demonstrated above, institutional investors have come to dominate the stock market. It can therefore be assumed that they play an important role in the prevalence of such practices. In the following, both practices are examined in more detail with regard to their respective behavioral patterns, underlying strategies, and contributions to short-termism. Figure 1 provides a concise overview of the two practices.

3.1.2 Speculative trading

Speculative traders typically hold their shares for short periods of time, often less than a day.25Moore, M. T. & Walker-Arnott, E. A Fresh Look at Stock Market Shorttermism. Journal of Law and Society 41, 416–445 (2014). Moreover, they base their decisions not on the fundamentals and long-term prospects of the company but on movements in the share price that they try to predict.2Dallas, L. L. Short-Termism, the Financial Crisis, and Corporate Governance. The Journal of Corporation Law 37, 265 (2012).,25Moore, M. T. & Walker-Arnott, E. A Fresh Look at Stock Market Shorttermism. Journal of Law and Society 41, 416–445 (2014). The exact mechanism can be represente as follows: By monitoring the market sentiment, speculators try to predict how new developments will be received by the market. Specifically, speculators aim to recognize when a particular stock is moving into favor and enter the trade before it gains popularity. Once that stock is in high demand and its price rises, they sell it for a profit. Alternatively, they try to sell stock ahead of an expected loss in value.2Dallas, L. L. Short-Termism, the Financial Crisis, and Corporate Governance. The Journal of Corporation Law 37, 265 (2012).,25Moore, M. T. & Walker-Arnott, E. A Fresh Look at Stock Market Shorttermism. Journal of Law and Society 41, 416–445 (2014). The predictions and assessments made by speculators are not based on research regarding long-term economic performance such as business strategy and financial prospects. Their research activities are instead dedicated to the identification of trading patterns and volumes, as well as to the analysis of historical trends of share price movements.2Dallas, L. L. Short-Termism, the Financial Crisis, and Corporate Governance. The Journal of Corporation Law 37, 265 (2012).,25Moore, M. T. & Walker-Arnott, E. A Fresh Look at Stock Market Shorttermism. Journal of Law and Society 41, 416–445 (2014).

This approach can disconnect the share price from the company’s actual performance. The link between productive and financial dimensions of a company is particularly weak when many speculative high-frequency traders are involved.25Moore, M. T. & Walker-Arnott, E. A Fresh Look at Stock Market Shorttermism. Journal of Law and Society 41, 416–445 (2014). This is due to the fact that the share prices come to reflect short-term sentiment rather than long-term prospects. The price movements, therefore, respond strongly to market trends. Thus, the negative effects of speculative trading mainly manifest in high market volatility.25Moore, M. T. & Walker-Arnott, E. A Fresh Look at Stock Market Shorttermism. Journal of Law and Society 41, 416–445 (2014). This can be identified as the central contribution of speculative trading to shorttermism.25Moore, M. T. & Walker-Arnott, E. A Fresh Look at Stock Market Shorttermism. Journal of Law and Society 41, 416–445 (2014).

If the share price deviates considerably from the fundamentals and there is strong volatility, there may be a negative impact on investors’ willingness to invest. Investors consider the stock to be risky and expect higher returns as compensation. This leads to higher capital costs for the company, which can in turn cause a decline in investment.33Samuel, C. Does shareholder myopia lead to managerial myopia? A first look. Applied Financial Economics 10, 493–505 (2000).

Speculative investors, therefore, contribute to short-termism by distorting the equity mechanism, thereby increasing volatility and the cost of capital, to the detriment of investment initiatives.25Moore, M. T. & Walker-Arnott, E. A Fresh Look at Stock Market Shorttermism. Journal of Law and Society 41, 416–445 (2014).,33Samuel, C. Does shareholder myopia lead to managerial myopia? A first look. Applied Financial Economics 10, 493–505 (2000). However, by using performance-neutral practices, they do not directly influence the strategic decision-making of management. They are fundamentally indifferent to the success of the company. This is in stark contrast to the earnings-based investment approach.25Moore, M. T. & Walker-Arnott, E. A Fresh Look at Stock Market Shorttermism. Journal of Law and Society 41, 416–445 (2014).

3.1.3 Earnings-based investment

As the term suggests, earnings-based investors evaluate their shareholdings based on corporate earnings, with decisions about investment and divestment being made in response to actual or anticipated changes in periodic earnings.25Moore, M. T. & Walker-Arnott, E. A Fresh Look at Stock Market Shorttermism. Journal of Law and Society 41, 416–445 (2014). As opposed to speculators, earnings-based investors are thus concerned with the company’s performance.25Moore, M. T. & Walker-Arnott, E. A Fresh Look at Stock Market Shorttermism. Journal of Law and Society 41, 416–445 (2014). The focus on earnings stems from the investor’s need for some form of indicator regarding the company’s success. These investors seek genuine insight into the company’s situation, aiming to evaluate their investment.1Laverty, K. J. Economic “Short-Termism”: The Debate, The Unresolved Issues, and The Implications for Management Practice and Research. The Academy of Management Review, 21, 825–860 (1996).,27Jacobs, M. Short-term America: The Causes and Cures of Our Business Myopia. Boston: Harvard Business School Press (1991).

But investors face the central challenge of information asymmetry. Their relationship with the company is usually characterized by a lack of knowledge, communication, and involvement. They have no insight into the operational and strategic activities of management and therefore do not know whether their money is being used efficiently.1Laverty, K. J. Economic “Short-Termism”: The Debate, The Unresolved Issues, and The Implications for Management Practice and Research. The Academy of Management Review, 21, 825–860 (1996).,27Jacobs, M. Short-term America: The Causes and Cures of Our Business Myopia. Boston: Harvard Business School Press (1991). In addition, most investors have a high stock turnover rate as well as highly diversified portfolios. It is therefore simply not possible for them to keep up with all the business activities they are funding.27Jacobs, M. Short-term America: The Causes and Cures of Our Business Myopia. Boston: Harvard Business School Press (1991). Since investors have limited opportunities to obtain and evaluate complex technological information, they need a simple metric that represents company performance.9Graham, J. R. & Harvey, C. R. & Rajgopal, S. Value Destruction and Financial Reporting Decisions. Financial Analysts Journal 62, 27–39 (2006).,26Roe, M. J. Corporate Short-Termism-In the Boardroom and in the Courtroom. The Business Lawyer 68, 977–1006 (2013). This metric must be easy to understand, quantifiable, and comparable to other companies.9Graham, J. R. & Harvey, C. R. & Rajgopal, S. Value Destruction and Financial Reporting Decisions. Financial Analysts Journal 62, 27–39 (2006). This explains the overwhelming emphasis on reported earnings.9Graham, J. R. & Harvey, C. R. & Rajgopal, S. Value Destruction and Financial Reporting Decisions. Financial Analysts Journal 62, 27–39 (2006).,26Roe, M. J. Corporate Short-Termism-In the Boardroom and in the Courtroom. The Business Lawyer 68, 977–1006 (2013).

However, it is not only the earnings themselves that are relevant to investors, but also their comparison with previously set earnings benchmarks. In accordance with capital market requirements, companies must disclose their earnings on a quarterly basis so that investors can assess the company’s situation.4Terry, S. J. The Macro Impact of Short‐Termism. Econometrica 91, 1881–1912 (2023).,25Moore, M. T. & Walker-Arnott, E. A Fresh Look at Stock Market Shorttermism. Journal of Law and Society 41, 416–445 (2014). It is a well-established practice for financial analysts to forecast earnings before the quarterly earnings reports are published. These consensus forecasts are announced to the public before the start of the earnings season.4Terry, S. J. The Macro Impact of Short‐Termism. Econometrica 91, 1881–1912 (2023). The estimates generally assume perpetual growth in earnings, which means earnings estimates typically create high expectations.25Moore, M. T. & Walker-Arnott, E. A Fresh Look at Stock Market Shorttermism. Journal of Law and Society 41, 416–445 (2014). Earnings-based investors often make their decisions explicitly with regard to forecasts, comparing expected and actual profits, and disinvesting when expectations are not met.25Moore, M. T. & Walker-Arnott, E. A Fresh Look at Stock Market Shorttermism. Journal of Law and Society 41, 416–445 (2014).

Relying on earnings as the dominant form of performance measure comes with implications regarding short-termism, as the metric is backward-looking in nature. Accounting information provides no information about the long-term consequences of decisions because performance is measured and evaluated before long-term developments become visible.34Marginson, D. & McAulay, L. Exploring the debate on short-termism: a theoretical and empirical analysis. Strategic Management Journal 29, 273–292 (2008). Intangible assets are also not reflected in financial reporting, with investors having no alternative means of obtaining this information.2Dallas, L. L. Short-Termism, the Financial Crisis, and Corporate Governance. The Journal of Corporation Law 37, 265 (2012).,35Vergauwen, P. G. M. C. & van Alem, F. J. C. Annual report IC disclosures in The Netherlands, France and Germany. Journal of Intellectual Capital 6, 89–104 (2005). Investors, therefore, make their investment decisions based solely on short-term financial information. Therefore, earnings-based investors contribute to short-termism by putting pressure on managers to deliver short-term results, as they do not reward long-term perspectives.

3.2 Managers

While investors can set short-term incentives, it is ultimately executives who make strategic decisions. They decide on the strategic approach and investments in long-term initiatives. Short-termism therefore follows from management decisions.10Wiersema, M. & Koo, H. & Chen, W. & Zhang, Y. Corporate Short-Termism: A Review and Research Agenda. Journal of Management 51, 2389–2418 (2025). The following section examines the factors that influence executives to manage in a shortterm manner.

3.2.1 External expectations and market pressure

A key finding of the previous chapter is that investors evaluate managers based on short-term performance. The prevailing view in the literature is that this puts pressure on managers and thus creates an incentive to engage in short-term practices.

The exact mechanism behind the pressure stems from the expectations created by consensus earnings. Terry (2023) examines the influence of forecast expectations on managers by conducting an empirical study. He analyses several thousand US companies regarding the difference between profit forecasts and actual profits. His results show that by far the most frequently observed value of the deviation is zero.4Terry, S. J. The Macro Impact of Short‐Termism. Econometrica 91, 1881–1912 (2023). This points to a strategic approach in which companies workspecifically toward meeting earnings benchmarks.4Terry, S. J. The Macro Impact of Short‐Termism. Econometrica 91, 1881–1912 (2023). From this, it can be concluded that managers attach great importance to earnings benchmarks. Graham et al. (2006) also offer insights in this direction. In their study, they surveyed 400 financial executives about which performance measure they considered most important. A large majority of about 60% cited earnings. Therefore, there is empirical evidence that managers place great value on earnings and meeting the consensus earnings.9Graham, J. R. & Harvey, C. R. & Rajgopal, S. Value Destruction and Financial Reporting Decisions. Financial Analysts Journal 62, 27–39 (2006).

The pressure to meet expectations arising from profit forecasts influences managerial behavior, as achieving certain profit targets requires strategic cost reduction measures.4Terry, S. J. The Macro Impact of Short‐Termism. Econometrica 91, 1881–1912 (2023). Fuller and Jensen (2024) note that forecasts have come to determine companies’ strategies instead of reflecting them.36Fuller, J. & Jensen, M. C. Just Say No to Wall Street: Putting a Stop to the Earnings Game. Journal of Applied Corporate Finance 22, 59–63 (2010). The study conducted by Graham et al. (2006) asked CFOs what measures they would take to ensure they meet their earnings targets. The results show that 80% of managers are willing to reduce discretionary spending to ensure that profit forecasts are met, an approach referred to as earnings management.9Graham, J. R. & Harvey, C. R. & Rajgopal, S. Value Destruction and Financial Reporting Decisions. Financial Analysts Journal 62, 27–39 (2006). Earnings management includes postponing long-term project and reducing expenditures on R&D, advertising, or maintenance.9Graham, J. R. & Harvey, C. R. & Rajgopal, S. Value Destruction and Financial Reporting Decisions. Financial Analysts Journal 62, 27–39 (2006).

However, the actions managers take to improve their short-term position harm the company in the long term.36Fuller, J. & Jensen, M. C. Just Say No to Wall Street: Putting a Stop to the Earnings Game. Journal of Applied Corporate Finance 22, 59–63 (2010). Graham et al (2006) argue that earnings management is almost always value-decreasing.9Graham, J. R. & Harvey, C. R. & Rajgopal, S. Value Destruction and Financial Reporting Decisions. Financial Analysts Journal 62, 27–39 (2006). Moreover, their study shows that managers, too, are aware of the negative consequences of their actions.9Graham, J. R. & Harvey, C. R. & Rajgopal, S. Value Destruction and Financial Reporting Decisions. Financial Analysts Journal 62, 27–39 (2006). Managers are thus knowingly willing to sacrifice long-term corporate value in order to meet profit expectations.

But why are managers so willing to engage in activities they know are valuedecreasing? To answer this question, one has to consider the consequences managers face if they fail to meet earnings benchmarks. If a company cannot meet its forecast figures, it is punished by the capital market in the form of stock price slumps.13Mizik, N. The Theory and Practice of Myopic Management. Journal of Marketing Research 47, 594–611 (2010). Even if a company only narrowly misses an earnings benchmark, this already leads to sharp price losses.9Graham, J. R. & Harvey, C. R. & Rajgopal, S. Value Destruction and Financial Reporting Decisions. Financial Analysts Journal 62, 27–39 (2006). Graham et al. (2006) offer empirical insight into the importance of meeting benchmarks and their signaling power to the market. 86.3% of surveyed managers agree that meeting benchmarks helps to convey credibility to the market. Furthermore, more than 80% state that targets must be met to maintain or increase the stock price. Missing earning targets, on the other hand, is interpreted as a sign of uncertainty regarding the company’s future by 80.7% of respondents. In addition, 60% agreed that the inability to meet forecasts conveys the notion that there are previously unknown issues within the company.9Graham, J. R. & Harvey, C. R. & Rajgopal, S. Value Destruction and Financial Reporting Decisions. Financial Analysts Journal 62, 27–39 (2006). The incentive to behave myopically, therefore, results from fear of negative market reactions and the desire to secure investor confidence.

3.2.2 Turnover risk and career-driven decision-making

However, there are reasons to believe that the consequences of missed earnings targets are not limited to the company. In fact, the majority of executives surveyed by Graham et al. (2006) state that their management skills are called into question when earnings do not meet expectations.9Graham, J. R. & Harvey, C. R. & Rajgopal, S. Value Destruction and Financial Reporting Decisions. Financial Analysts Journal 62, 27–39 (2006). Managers may therefore face negative career-related consequences. From this, it can be concluded that managers might take their own career prospects into account when making decisions. Building on this, a further dimension of managerial short-termism emerges, independent of investor demands and instead driven by career-oriented and opportunistic motives. These drivers are also discussed in the literature, with a particular focus on the misguided incentives created by high executive turnover rates.

Palley (1997) examines the influence of managerial turnover on investment behavior. He shows a negative correlation between employment duration and short-term-oriented behavior, which suggests that short-termism occurs more frequently when managerial turnover is high.24Palley, T. I. Managerial turnover and the theory of short-termism. Journal of Economic Behavior & Organization32, 547–557 (1997). These findings are particularly relevant in light of the shortening CEO tenures in the US, which have declined significantly since the 1970s and now average less than seven years.37Kaplan, S. N. & Minton, B.A. How Has CEO Turnover Changed? International Review of Finance 12, 57–87 (2012). It can therefore be assumed that CEOs are aware that their employment within a company is limited.26Roe, M. J. Corporate Short-Termism-In the Boardroom and in the Courtroom. The Business Lawyer 68, 977–1006 (2013). Building on this, Mannix and Loewenstein (1993) examine the link between short-termism and high inter-organizational mobility.38Mannix, E. A. & Loewenstein, G. F. Managerial Time Horizons and Interfirm Mobility: An Experimental Investigation. Organizational Behavior and Human Decision Processes 56, 266–284 (1993). They explain that “High levels of mobility have the effect of uncoupling an individual’s returns from the long-term performance of the particular company where he or she is employed at a particular time.”38Mannix, E. A. & Loewenstein, G. F. Managerial Time Horizons and Interfirm Mobility: An Experimental Investigation. Organizational Behavior and Human Decision Processes 56, 266–284 (1993).(p. 268). This implies that managers will prefer to pursue initiatives that show results within their tenure. This notion is further supported by Palley (1997), who comes to a similar conclusion.24Palley, T. I. Managerial turnover and the theory of short-termism. Journal of Economic Behavior & Organization32, 547–557 (1997). He states that “rational own-reward maximizing managers”24Palley, T. I. Managerial turnover and the theory of short-termism. Journal of Economic Behavior & Organization32, 547–557 (1997).(p. 548) may knowingly choose projects that yield high returns early on, even if they have lower net present values overall.24Palley, T. I. Managerial turnover and the theory of short-termism. Journal of Economic Behavior & Organization32, 547–557 (1997). From this, it can be concluded that managers may be incentivized to pursue strategies that are advantageous for themselves but suboptimal for their company.24Palley, T. I. Managerial turnover and the theory of short-termism. Journal of Economic Behavior & Organization32, 547–557 (1997).

In the context of short employment horizons, managers’ desire to secure personal financial gains is not the only driver of short-termism. Another commonly discussed factor is their effort to signal competence to the labor market.

As has been established, managers work in an environment characterized by high interorganizational mobility.37Kaplan, S. N. & Minton, B.A. How Has CEO Turnover Changed? International Review of Finance 12, 57–87 (2012). Consequently, they generally want to convince the labor market of their capabilities.39Campbell, T. S. & Marino, A. M. Myopic Investment Decisions and Competitive Labor Markets. International Economic Review 35, 855–875 (1994).,40Holmstrom, B. & i Costa, J. R. Managerial Incentives and Capital Management. The Quarterly Journal of Economics 101, 835–860 (1986). Holmstrom and Ricart i Costa (1986) contend that business leaders are aware of the labor market’s evaluation approach, which is based on past performance. They further argues that managers strategically change their decision-making behavior to enhance their external reputation and perceived abilities. Given the nature of the evaluation, a favorable impression requires them to deliver strong results during their tenure.40Holmstrom, B. & i Costa, J. R. Managerial Incentives and Capital Management. The Quarterly Journal of Economics 101, 835–860 (1986). It is widely acknowledged in the literature that managers strategically select myopic investments to improve their professional standing. Campbell and Marino (1994) provide evidence that supports this notion.39Campbell, T. S. & Marino, A. M. Myopic Investment Decisions and Competitive Labor Markets. International Economic Review 35, 855–875 (1994). It is therefore considered a driver of short-termism that managers omit investments whose payoffs will become apparent only after the manager has likely left the company. These results are usually not attributed to them and therefore do not improve their reputation.

3.2.3 Compensation structure

Executive compensation is also considered a driver of short-termism, particularly when it is linked to the share price. American CEOs generally hold only small shares in their companies.41Bertrand, M. & Mullainathan, S. Enjoying the Quiet Life? Corporate Governance and Managerial Preferences. The Journal of Political Economy 111, 1043–1075 (2003). The majority of American CEOs are thus financially detached from their companies’ performance.41Bertrand, M. & Mullainathan, S. Enjoying the Quiet Life? Corporate Governance and Managerial Preferences. The Journal of Political Economy 111, 1043–1075 (2003). Their personal financial prospects remain unaffected by short-term oriented behavior, creating a moral hazard.41Bertrand, M. & Mullainathan, S. Enjoying the Quiet Life? Corporate Governance and Managerial Preferences. The Journal of Political Economy 111, 1043–1075 (2003). As discussed in the preceding section, managers have incentives to focus on the short term for opportunistic reasons, disregarding the consequences for the company. This aligns with the agency theory, according to which the objectives of managers and companies do not always coincide, which can lead to undesirable outcomes.42Wang, X. Too much incentive to innovate? CEO stock option exercise and myopic R&D management. The Journal of Product Innovation Management 41, 1141–1164 (2024).,43Flammer, C. & Bansal, P. Does a Long-Term Orientation Create Value? Evidence from a Regression Discontinuity. Strategic Management Journal 38, 1827–1847 (2017). To resolve this discrepancy and align the interests, many companies have established performance-based compensation for managers by tying it to the stock price.10Wiersema, M. & Koo, H. & Chen, W. & Zhang, Y. Corporate Short-Termism: A Review and Research Agenda. Journal of Management 51, 2389–2418 (2025).,42Wang, X. Too much incentive to innovate? CEO stock option exercise and myopic R&D management. The Journal of Product Innovation Management 41, 1141–1164 (2024).

However, research suggests that this approach may itself be a source of shorttermism.42Wang, X. Too much incentive to innovate? CEO stock option exercise and myopic R&D management. The Journal of Product Innovation Management 41, 1141–1164 (2024). Managers who want to increase their compensation might resort to manipulative behavior.13Mizik, N. The Theory and Practice of Myopic Management. Journal of Marketing Research 47, 594–611 (2010).,42Wang, X. Too much incentive to innovate? CEO stock option exercise and myopic R&D management. The Journal of Product Innovation Management 41, 1141–1164 (2024).,44Fusso, N. A. Systems thinking review for solving short-termism. Management Research Review 36, 805–822 (2013). Specifically, they may engage in myopic R&D management to increase the stock price.42Wang, X. Too much incentive to innovate? CEO stock option exercise and myopic R&D management. The Journal of Product Innovation Management 41, 1141–1164 (2024). They could then profit by selling their shares at a high price.45Ladika, T. & Sautner, Z. Managerial Short-Termism and Investment: Evidence from Accelerated Option Vesting. Review of Finance 24, 305–344 (2020).

Mizik (2010) argues that stock-based compensation only leads to increased efficiency under perfect information conditions. But this changes once information asymmetriesare taken into account. Owners have no insight into whether managers engage in value-enhancing or manipulative behavior, which enables managers to employ short-term-oriented practices.13Mizik, N. The Theory and Practice of Myopic Management. Journal of Marketing Research 47, 594–611 (2010). Wang (2024) shows a positive correlation between stock-option exercise and myopic R&D management.42Wang, X. Too much incentive to innovate? CEO stock option exercise and myopic R&D management. The Journal of Product Innovation Management 41, 1141–1164 (2024). Similarly, Souder and Shaver (2010) show a negative correlation between stock-option exercise and longterm oriented investments.46Souder, D. & Shaver, J. M. Constraints and incentives for making long horizon corporate investments. Strategic Management Journal 31, 1316–1336 (2010). Moreover, Martin et al. (2019) provide findings that reveal a positive relationship between managerial stock option ownership and earnings management.47Martin, G. P. & Wiseman, R. M. & Gomez-Mejia, L. R. The Interactive Effect of Monitoring and Incentive Alignment on Agency Costs. Journal of Management 45, 701–727 (2019). The evidence, therefore, suggests that share-based compensation drives short-termism.

3.2.4 Individual factors

So far, the analysis has been limited to external factors that influence managerial decision-making. The following chapter will now examine whether the internal predispositions of decision-makers can facilitate short-termism.

Managerial decision-making, deriving from cognitive processes, is subject to cognitive biases. While managers may intend to behave rationally, biases limit their ability to accurately assess rational courses of action.1Laverty, K. J. Economic “Short-Termism”: The Debate, The Unresolved Issues, and The Implications for Management Practice and Research. The Academy of Management Review, 21, 825–860 (1996).,14Milano, G. Corporate Short‐Termism and How It Happens. Journal of Applied Corporate Finance 30, 27–35 (2018). In addition, individuals cannot obtain nor process all information needed to decide rationally.10Wiersema, M. & Koo, H. & Chen, W. & Zhang, Y. Corporate Short-Termism: A Review and Research Agenda. Journal of Management 51, 2389–2418 (2025). The principle at play, referred to as Bounded Rationality, explains the occurrence of irrational individual judgment.1Laverty, K. J. Economic “Short-Termism”: The Debate, The Unresolved Issues, and The Implications for Management Practice and Research. The Academy of Management Review, 21, 825–860 (1996).,10Wiersema, M. & Koo, H. & Chen, W. & Zhang, Y. Corporate Short-Termism: A Review and Research Agenda. Journal of Management 51, 2389–2418 (2025). It is therefore a useful addition to the discussion of short-termism.

One bias that can lead to short-sighted decision-making is optimism.48Campbell, T. C. & Gallmeyer, M. & Johnson, S. A. & Rutherford, J. & Stanley, B.W. CEO optimism and forced turnover. Journal of Financial Economics 101, 695–712 (2011).,49Wang, X. Does CEO temporal myopia always lead to firm short-termism? The critical role of CEO optimism and perceived opportunity costs. Journal of Business Research 180, 114739 (2024). CEO optimism refers to an inclination to expect positive results.50Langabeer, J. R. & DelliFraine, J. Does CEO optimism affect strategic process? Management Research Review 34, 857–868 (2011). In his study, Wang (2024) analyzes the effects of this bias regarding short-termism. He argues that “Overall, optimistic CEOs tend to overestimate their abilities to overcome the adverse effects of short-termism and overweigh the favorable outcome that can be realized”49Wang, X. Does CEO temporal myopia always lead to firm short-termism? The critical role of CEO optimism and perceived opportunity costs. Journal of Business Research 180, 114739 (2024).(p.4). Optimistic CEOs are therefore more likely to underestimate the consequences of shorttermism.49Wang, X. Does CEO temporal myopia always lead to firm short-termism? The critical role of CEO optimism and perceived opportunity costs. Journal of Business Research 180, 114739 (2024). He also argues that CEO optimism leads to fewer long-term initiatives being pursued, which is supported by his empirical findings. The findings show that optimistic CEOs prioritize value appropriation over value creation, i.e., they give priority to achieving immediate results over investments aimed at long-term development.49Wang, X. Does CEO temporal myopia always lead to firm short-termism? The critical role of CEO optimism and perceived opportunity costs. Journal of Business Research 180, 114739 (2024). This is consistent with the findings of Langabeer and DelliFraine (2011), who find a negative correlation between CEO optimism and rational decisionmaking.50Langabeer, J. R. & DelliFraine, J. Does CEO optimism affect strategic process? Management Research Review 34, 857–868 (2011). CEO optimism can therefore drive short-termism by restricting managers’ rational assessment of consequences.

Another cognitive bias that is believed to promote short-term behavior is the bias toward herding.2Dallas, L. L. Short-Termism, the Financial Crisis, and Corporate Governance. The Journal of Corporation Law 37, 265 (2012).,14Milano, G. Corporate Short‐Termism and How It Happens. Journal of Applied Corporate Finance 30, 27–35 (2018). Herding manifests itself in managers’ desire to conform to their peers, due to the fear of falling behind.14Milano, G. Corporate Short‐Termism and How It Happens. Journal of Applied Corporate Finance 30, 27–35 (2018). However, this can lead them to engage in illadvised management practices. Herding can lead managers to subordinate their own insights to those of the majority. Managers will believe that other companies are more knowledgeable and therefore lose confidence in their own original approach.2Dallas, L. L. Short-Termism, the Financial Crisis, and Corporate Governance. The Journal of Corporation Law 37, 265 (2012). The more companies adopt a certain behavior, the stronger managers believe it to be the correct approach. This bias becomes relevant in the context of short-termism once a short-term orientation prevails among companies, as managers will encourage each other to continue the behavior in question.2Dallas, L. L. Short-Termism, the Financial Crisis, and Corporate Governance. The Journal of Corporation Law 37, 265 (2012).

Present bias can also foster a tendency toward short-termism in managers. Present bias refers to the tendency to prefer smaller, near-term rewards over larger rewards received in the future.51Chakraborty, A. Present Bias. Econometrica 89, 1921–1961 (2021). Managers often have to choose between two mutually exclusive investment opportunities. One such option may be more profitable in the short term, while the other may generate overall higher returns over the long run.1Laverty, K. J. Economic “Short-Termism”: The Debate, The Unresolved Issues, and The Implications for Management Practice and Research. The Academy of Management Review, 21, 825–860 (1996). To address this choice, managers normatively use the discounted cash flow analysis.1Laverty, K. J. Economic “Short-Termism”: The Debate, The Unresolved Issues, and The Implications for Management Practice and Research. The Academy of Management Review, 21, 825–860 (1996). This capital budgeting technique entails the discounting of all future cash flows each alternative is expected to generate.1Laverty, K. J. Economic “Short-Termism”: The Debate, The Unresolved Issues, and The Implications for Management Practice and Research. The Academy of Management Review, 21, 825–860 (1996). By calculating the net present value, managers are able to evaluate and compare investment options with different time horizons.1Laverty, K. J. Economic “Short-Termism”: The Debate, The Unresolved Issues, and The Implications for Management Practice and Research. The Academy of Management Review, 21, 825–860 (1996). The investment with the highest net present value is generally considered to be the most reasonable choice.13Mizik, N. The Theory and Practice of Myopic Management. Journal of Marketing Research 47, 594–611 (2010). The discount rate describes how much compensation an individual demands to forgo immediate satisfaction and defer it to the future instead.52Shoham, A. & Malul, M. Cultural attributes, national saving and economic outcomes. The Journal of Socio-Economics 47, 180–184 (2013). To obtain accurate results, it is essential to use an appropriate discount rate.1Laverty, K. J. Economic “Short-Termism”: The Debate, The Unresolved Issues, and The Implications for Management Practice and Research. The Academy of Management Review, 21, 825–860 (1996).,13Mizik, N. The Theory and Practice of Myopic Management. Journal of Marketing Research 47, 594–611 (2010).

However, researchers suspect a tendency among managers to use hyperbolic discount rates.1Laverty, K. J. Economic “Short-Termism”: The Debate, The Unresolved Issues, and The Implications for Management Practice and Research. The Academy of Management Review, 21, 825–860 (1996).,13Mizik, N. The Theory and Practice of Myopic Management. Journal of Marketing Research 47, 594–611 (2010).,43Flammer, C. & Bansal, P. Does a Long-Term Orientation Create Value? Evidence from a Regression Discontinuity. Strategic Management Journal 38, 1827–1847 (2017). Attempts to explain such hyperbolic discounting commonly focus on the present bias, as managers’ preference for short-term returns is believed to cause an undervaluation of long-term-oriented projects.13Mizik, N. The Theory and Practice of Myopic Management. Journal of Marketing Research 47, 594–611 (2010). The use of hyperbolic discount rates leads to the distortion of net present value in favor of short-term investments. If a manager bases decisions on a distorted net present value, this can contribute to shorttermism, as investments in R&D and product development become less likely.28Ortiz‐de‐Mandojana, N. & Bansal, P. & Aragón‐Correa, J.A. Older and Wiser: How CEOs’ Time Perspective Influences Long‐Term Investments in Environmentally Responsible Technologies. British Journal of Management 30, 134–150 (2019).

Present bias is closely related to a person’s general temporal focus, which can also influence their tendency toward short-term thinking. Temporal focus is defined as “the extent to which people characteristically devote their attention to the perceptions of past, present, and future”53Shipp, A. J. & Edwards, J. R. & Lambert, L. S. Conceptualization and measurement of temporal focus: The subjective experience of the past, present, and future. Organizational Behavior and Human Decision Processes110, 1–22 (2009).(p.1). Researchers generally agree that individuals differ in the time dimension they prioritize.53Shipp, A. J. & Edwards, J. R. & Lambert, L. S. Conceptualization and measurement of temporal focus: The subjective experience of the past, present, and future. Organizational Behavior and Human Decision Processes110, 1–22 (2009).,54Das, T. K. Strategic planning and individual temporal orientation. Strategic Management Journal 8, 203–209 (1987). Moreover, temporal focus is associated with individual characteristics such as behavior, attitude, and decision-making.53Shipp, A. J. & Edwards, J. R. & Lambert, L. S. Conceptualization and measurement of temporal focus: The subjective experience of the past, present, and future. Organizational Behavior and Human Decision Processes110, 1–22 (2009). A key contribution to this topic comes from Das (1987), who conducted an empirical study on the relationship between temporal orientation and planning horizons.54Das, T. K. Strategic planning and individual temporal orientation. Strategic Management Journal 8, 203–209 (1987). His findings indicate that long-term-oriented decision-makers tend to prefer longer planning horizons. A short-term orientation, on the other hand, is associated with a preference for short planning horizons.54Das, T. K. Strategic planning and individual temporal orientation. Strategic Management Journal 8, 203–209 (1987). This is relevant to the debate on short-termism, as it demonstrates that managers’ temporal focus influences the strategic orientation of the company.54Das, T. K. Strategic planning and individual temporal orientation. Strategic Management Journal 8, 203–209 (1987). Therefore, only a certain kind of executives, namely the future-oriented kind, is inclined to undertake long-term innovation.54Das, T. K. Strategic planning and individual temporal orientation. Strategic Management Journal 8, 203–209 (1987). Thus, short-termism can be traced to managers who are cognitively inclined towards the present or the past.

4 Cultural and industrial influences on short-termism

Driven by various structural, market-related, and intrapersonal factors, short-termism can become integrated into corporate decision-making. Nevertheless, an argument can be made that it is not a ubiquitous issue but instead varies greatly depending on the culture and industry in which a company operates.

4.1 Cultural environment

Research suggests that the objectives of business leaders across countries may be a reflection of their cultural values.55Irving, K. Overcoming Short-Termism: Mental Time Travel, Delayed Gratification and How Not to Discount the Future. Australian Accounting Review 19, 278–294 (2009). Althoug mental programming is partly inherited and individual, it is also shaped by the environment in which an individual grows up.56Hofstede, G. Culture‘s consequences : comparing values, behaviors, institutions, and organizations across nations. Thousand Oaks: Sage Publications, (2001). Cultures, therefore, determine the value systems that are shared by the majority of a society.56Hofstede, G. Culture‘s consequences : comparing values, behaviors, institutions, and organizations across nations. Thousand Oaks: Sage Publications, (2001). Hofstede (2001) developed a framework that categorizes cultures based on five dimensions. These dimensions are power distance, masculinity vs femininity, uncertainty avoidance, individualism vs collectivism, and long-term vs short-term orientation.56Hofstede, G. Culture‘s consequences : comparing values, behaviors, institutions, and organizations across nations. Thousand Oaks: Sage Publications, (2001). This model can be used to explain whether certain cultures are more prone to short-termism due to their inherent characteristics. Resarchers have already analyzed the two dimensions of individualism and temporal orientation in this context. These two dimensions will therefore be discussed in this chapter.

A good starting point is the dimension of temporal orientation, which has already been established as an influence on short-termism. According to the framework, some cultures are generally short-term oriented, while others have a long-term orientation.56Hofstede, G. Culture‘s consequences : comparing values, behaviors, institutions, and organizations across nations. Thousand Oaks: Sage Publications, (2001). A long-term orientation is particularly evident among Asian countries. By contrast, the Anglo-American regions can be categorized as short-term oriented countries.57Antonczyk, R. C. & Breuer, W. & Salzmann, A. J. Long-Term Orientation and Relationship Lending: A Cross-Cultural Study on the Effect of Time Preferences on the Choice of Corporate Debt. Management International Review 54, 381–415 (2014). This model allows the manager’s individual disposition to be embedded in a broader cultural context. To this end, Hofstede et al. (2002) conducted a cross-national analysis examining how managers’ business goals differ depending on the time orientation prevalent in their culture. They concluded that managers in long-term-oriented countries pursue profit targets over a period of 10 years. In short-term-oriented countries, on the other hand, the focus lies on profits within the same year.58Hofstede, G. & Van Deusen, C. A. & Müller, C. B. & Charles, T. A. What Goals Do Business Leaders Pursue? A Study in Fifteen Countries. Journal of International Business Studies 33, 785–803 (2002). This is consistent with the focus on quarterly results, which is particularly prevalent in AngloAmerican countries.57Antonczyk, R. C. & Breuer, W. & Salzmann, A. J. Long-Term Orientation and Relationship Lending: A Cross-Cultural Study on the Effect of Time Preferences on the Choice of Corporate Debt. Management International Review 54, 381–415 (2014). In contrast, companies in long-term oriented countries work toward a strong market position and subordinate immediate results.57Antonczyk, R. C. & Breuer, W. & Salzmann, A. J. Long-Term Orientation and Relationship Lending: A Cross-Cultural Study on the Effect of Time Preferences on the Choice of Corporate Debt. Management International Review 54, 381–415 (2014). It also coincides with the general academic discourse, which often cites Japan in particular as a counterexample to short-term orientation.1Laverty, K. J. Economic “Short-Termism”: The Debate, The Unresolved Issues, and The Implications for Management Practice and Research. The Academy of Management Review, 21, 825–860 (1996).,59Coates, J. & Davis, T. & Stacey, R. Performance measurement systems, incentive reward schemes and short-termism in multinational companies: a note. Management Accounting Research 6, 125–135 (1995). At the same time, the US and the UK are considered short-term oriented.55Irving, K. Overcoming Short-Termism: Mental Time Travel, Delayed Gratification and How Not to Discount the Future. Australian Accounting Review 19, 278–294 (2009).,59Coates, J. & Davis, T. & Stacey, R. Performance measurement systems, incentive reward schemes and short-termism in multinational companies: a note. Management Accounting Research 6, 125–135 (1995).

Furthermore, Shoham and Malul (2013) provide empirical evidence on the relationship between a nation’s temporal orientation and its willingness to save. According to their results, a long-term orientation is associated with an increased tendency to save. Shortterm oriented nations, on the other hand, exhibit a significantly lower willingness to save.52Shoham, A. & Malul, M. Cultural attributes, national saving and economic outcomes. The Journal of Socio-Economics 47, 180–184 (2013). These findings can be applied to short-termism, as they indicate that long-termoriented nations are willing to forego immediate consumption in favor of future benefits.52Shoham, A. & Malul, M. Cultural attributes, national saving and economic outcomes. The Journal of Socio-Economics 47, 180–184 (2013). In contrast, short-term-oriented nations insist on immediate consumption, which they are less willing to sacrifice for future benefits.52Shoham, A. & Malul, M. Cultural attributes, national saving and economic outcomes. The Journal of Socio-Economics 47, 180–184 (2013). In summary, it can be said that cultures differ in terms of their temporal orientation and their susceptibility to short-termism.55Irving, K. Overcoming Short-Termism: Mental Time Travel, Delayed Gratification and How Not to Discount the Future. Australian Accounting Review 19, 278–294 (2009).

Another cultural dimension associated with short-termism is individualism. According to Hofstede (2001), Asian cultures tend to be collectivist while Western cultures tend to be individualistic.56Hofstede, G. Culture‘s consequences : comparing values, behaviors, institutions, and organizations across nations. Thousand Oaks: Sage Publications, (2001). Collectivist cultures are characterized by the fact that they prioritize the common good. People in individualistic cultures, on the other hand, tend to prioritize their own well-being.56Hofstede, G. Culture‘s consequences : comparing values, behaviors, institutions, and organizations across nations. Thousand Oaks: Sage Publications, (2001). But what influence does this have on shorttermism? To answer this question, it is essential to note that research suggests a connection between economic opportunism and individualism.60Sakalaki, M. & Kazi, S. & Karamanoli, V. Do individualists have a higher opportunistic propensity than collectivists? Individualism and economic cooperation. Revue internationale de psychologie sociale 20, 59–75 (2007). As has been established, short-termism often stems from opportunistic behavior. Managers might act opportunistically to secure higher compensation or advance their career opportunities, disregarding the consequences for the company. Thus, individualistic cultures tend to be more affected by short-termism due to the increased prevalence of opportunistic behavior.

4.2 Industry affiliation

In addition to culture, a company’s industry affiliation may also influence its susceptibility to short-termism. Currently, this area is under-researched, as there is a lack of empirical inquiry examining short-termism in relation to industry structure.61Thanassoulis, J. Industry Structure, Executive Pay, and Short-Termism. Management Science 59, 402–419 (2013). Short-termism seems to be prevalent among companies across many industries.61Thanassoulis, J. Industry Structure, Executive Pay, and Short-Termism. Management Science 59, 402–419 (2013). However, there are initial approaches that address this research gap, most notably the research conducted by Brochet et al. (2015). To measure the degree of short-termism exhibited in different industries, they analyzed the time horizon that firms communicated to investors. To this end, they examined the call transcripts of earnings conferences with regard to certain keywords referring to long and short time horizons.62Brochet, F. & Loumioti, M. & Serafeim, G. Speaking of the short-term: disclosure horizon and managerial myopia. Review of Accounting Studies 20, 1122–1163 (2015).