Authors: Philip Klose

Edited by:

Last updated: July 3, 2026

Executive summary

ESG ratings have become a central tool in sustainable finance because they translate complex environmental, social, and governance information into structured signals for investors, customers, lenders, regulators, and corporate decision-makers. Their rise reflects growing recognition that sustainability-related risks and opportunities affect long-term value creation, capital access, supply chain relationships, and organizational resilience. For companies, ESG ratings are no longer only an investor relations issue; they increasingly shape customer requirements, regulatory preparedness, internal performance assessment, and strategic sustainability management.

The article shows that ESG ratings are useful but limited information products. Rating providers differ significantly in what they measure, how they collect data, how they define materiality, and how they weight and aggregate indicators. Some focus on financial materiality and enterprise risk, while others incorporate broader environmental and social impacts or assess management systems. As a result, ratings from different providers often diverge substantially, meaning that the same company can be assessed as a leader by one provider and a laggard by another.

Key barriers include inconsistent ESG data, limited methodological transparency, proprietary weighting systems, firm-size and regional biases, and an overreliance on policies, targets, and disclosures rather than verified sustainability outcomes. These weaknesses create greenwashing risks: companies may improve ratings by communicating more or aligning with specific rating methodologies without materially improving environmental or social performance. Evidence also suggests that ESG ratings often correlate more strongly with disclosure capacity and apparent performance than with real-world sustainability impacts.

For practitioners, the central implication is that ESG ratings should be managed strategically but not treated as definitive measures of sustainability performance. Organizations should identify which stakeholders use which ratings, select providers based on methodological fit and business relevance, maintain consistent and transparent data processes, and engage continuously with rating agencies to correct factual errors and understand methodology changes. At the same time, ratings should remain diagnostic tools, not steering targets. Internal governance should separate rating management from sustainability performance management and prioritize measurable improvements in emissions, labor practices, human rights, supply chain standards, governance quality, and other material impacts.

A robust implementation approach therefore combines strategic anchoring, provider selection, relationship management, reliable ESG data architecture, and careful score interpretation. The most mature organizations use multiple ratings in parallel, explain their differences, and avoid collapsing them into a single composite score. This preserves the information contained in rating divergence and helps prevent cosmetic optimization. Ultimately, ESG ratings can support better decision-making only when organizations understand their methodological limits and use them alongside credible sustainability data, stakeholder dialogue, and real performance indicators.

1 Introduction

Human activity has pushed the Earth system into a critical state. According to the Potsdam Institute for Climate Impact Research and Rockström et al. (2024), seven out of nine planetary boundaries that define “the safe operating space for humanity” (S.774) have been crossed.1Elisha, O. & Jebbin, F. The Loss of Biodiversity and Ecosystems: A Threat to the Functioning of our Planet, Economy and Human Society. Int. J. Econ. Environ. Dev. Soc. 1, 30–44 (2020).,2Rockström, J. et al. Planetary Boundaries guide humanity’s future on Earth. Nat. Rev. Earth Environ. 5, 773–788 (2024). Environmental degradation increases pressure on essential resources and erodes the social trust required for collective responses, which further weakens societies’ ability to address sustainability challenges in an equitable manner.3Edelman Trust Institute. 2025 Edelman Trust Barometer. https://www.edelman.de/sites/g/files/aatuss401/files/2025-01/2025%20Edelman%20Trust%20Barometer_Germany%20Report.pdf (2025).

The so-called funnel metaphor illustrates how the capacity of Earth’s ecological and social systems to support human civilization is systematically degrading due to unsustainable practices. As the “walls” of the funnel narrow over time, they represent the shrinking capacity of nature and society to support civilization. This metaphor was developed to clarify the above-mentioned safe operating space for humanity in combination with the self-benefit of proactivity by highlighting how these systemic changes will inevitably impact all companies. By understanding these dynamics, leaders and companies can better manage risks and innovate in ways that support the transition to sustainability.4Broman, G. I. & Robèrt, K.-H. A framework for strategic sustainable development. J. Clean. Prod. 140, 17–31 (2017).,5Esteban-Amaro, R., Estelles-Miguel, S. & Lengua, I. Towards sustainable business: Leading change from the bottom-up. WPOM-Work. Pap. Oper. Manag. 15, 95–111 (2024).

Figure 1: The Funnel metaphor

The Funnel metaphor, own visualisation after Broman & Robèrt (2017).4Broman, G. I. & Robèrt, K.-H. A framework for strategic sustainable development. J. Clean. Prod. 140, 17–31 (2017).

Building on these systemic sustainability challenges, it becomes quite clear that addressing them cannot be limited to political action or individual behavioural change alone. Given the central role of capital allocation in shaping economic activity, the financial system appears as a critical lever in the transition toward sustainability. As of 2024, approximately 27% of global regulated fund assets (~USD 16.7 trillion) report the application of responsible and sustainable investment approaches, up from around 3% in 2018.6GSIA. Global Sustainable Investment Review 2024. https://www.gsi-alliance.org/members-resources/gsir2024/. In this context, the International Energy Agency (IEA) estimates that global investments in i.e. clean energy would need to rise to around USD 4–4.5 trillion per year by 2030 in order to align with a pathway consistent with the 1.5 °C target of Paris.7IEA. World Energy Investment 2025 – Analysis. https://www.iea.org/reports/world-energy-investment-2025 (2025). This highlights that the achievement of climate goals depends fundamentally on large-scale shifts in investment flows and has given rise to the field of sustainable finance, as an approach to align financial decision-making with environmental and social objectives. Rather than treating sustainability as an externality, sustainable finance integrates environmental, social and governance (ESG) considerations into how risks, returns and long-term value are assessed. In doing so, it aims to redirect financial flows toward activities that contribute to long-term societal value creation while mitigating systemic risks arising from unsustainable business practices.8Schoenmaker, D. & Schramade, W. Principles of Sustainable Finance. (Oxford University Press, 2019).

The growing relevance of sustainable finance is closely linked to the recognition that sustainability-related risks are financially material. Biodiversity loss can disrupt supply chains and increase cash flow uncertainty. Energy price volatility increases input cost risk. And tighter environmental regulation can lead to higher compliance costs and stranded assets for carbon-intensive firms.8Schoenmaker, D. & Schramade, W. Principles of Sustainable Finance. (Oxford University Press, 2019). The list goes on. As a result, investors and regulators have intensified their demand for decision-useful information that allows them to assess a firm’s exposure to sustainability-related risks and opportunities in a structured and comparable way. However, sustainability performance is difficult to assess and quantify in practice, as it is inherently multidimensional and forward-looking. This creates a fundamental information problem: while sustainability considerations are recognized as financially relevant, they are not directly observable in standard financial statements.9Friede, G., Busch, T. & Bassen, A. ESG and financial performance: aggregated evidence from more than 2000 empirical studies. J. Sustain. Finance Invest. 5, 210–233 (2015).,10Pagano, M. S., Sinclair, G. & Yang, T. Understanding ESG ratings and ESG indexes. in Research Handbook of Finance and Sustainability 339–371 (Edward Elgar Publishing, Cheltenham, UK; Northampton, MA, USA, 2018).

It is precisely at this intersection of sustainability challenges and financial decision-making that ESG ratings have become increasingly important. How central ESG ratings have become is visible in current practice: the FNG 2026 industry survey shows that 72% of sustainable investors use aggregated ESG ratings to assess their portfolio companies on ESG criteria, more than any other instrument.11FNG. FNG Marktbericht 2026. (2026). Yet despite this central role, what ESG ratings actually measure and whether they fulfil their informational function remains contested, which makes their theoretical foundation and practical use a matter of active debate. ESG ratings aim to translate complex, heterogeneous and largely nonfinancial information on ESG issues into standardized metrics that can be integrated within financial markets.10Pagano, M. S., Sinclair, G. & Yang, T. Understanding ESG ratings and ESG indexes. in Research Handbook of Finance and Sustainability 339–371 (Edward Elgar Publishing, Cheltenham, UK; Northampton, MA, USA, 2018).,12Zumente, I. & Lāce, N. ESG Rating—Necessity for the Investor or the Company? Sustainability 13, 8940 (2021).,13Larcker, D. F., Pomorski, L., Tayan, B. & Watts, E. M. ESG Ratings: A Compass without Direction. SSRN Scholarly Paper at https://papers.ssrn.com/abstract=4179647 (2022).,14Stewart, R. Towards a better understanding of ESG ratings. J. Sustain. Finance Invest. 15, 624–643 (2025). By aggregating firm-level data on topics such as carbon emissions, biodiversity, labor practices or corporate governance structures, ESG ratings serve as information bridges between companies and capital providers. In practice, they are used by investors to screen portfolios regarding sustainability-related risks and from this construct ESG-based investment strategies or comply with regulatory disclosure requirements.10Pagano, M. S., Sinclair, G. & Yang, T. Understanding ESG ratings and ESG indexes. in Research Handbook of Finance and Sustainability 339–371 (Edward Elgar Publishing, Cheltenham, UK; Northampton, MA, USA, 2018).,12Zumente, I. & Lāce, N. ESG Rating—Necessity for the Investor or the Company? Sustainability 13, 8940 (2021). Consequently, ESG ratings have become a central infrastructure element of sustainable finance.8Schoenmaker, D. & Schramade, W. Principles of Sustainable Finance. (Oxford University Press, 2019). To stay in the picture of the Funnel, ESG ratings can be understood as an attempt to assess how firms are positioned within a progressively narrowing operating space shaped by ecological and social constraints. By translating sustainability-related exposures and strategic resilience into standardized metrics, ESG ratings aim to reflect a firms’ vulnerability to, and preparedness for, the systemic pressures described by the Funnel Metaphor. Derived from this logic, the following shows the research question:

RQ: “What theoretical insights does the existing literature on ESG Ratings provide and which practical implications can be derived for an implementation by practitioners?”

This research question will be explored within the following structure: The literature review is divided into five chapters. The first chapter is 2.1, definitions and concepts of ESG ratings, where central terminology used throughout the wiki entry will be clarified and situated within the broader sustainable finance discourse. In 2.2, historical background and evolution of ESG and ESG ratings, the development of the field will be traced from its SRI and CSR roots to the current ESG backlash, with particular attention to the commercial infrastructure of ESG ratings. In 2.3, the structure and concentration of the provider landscape will be characterized. In 2.4, the methodological architecture of the two largest providers will be examined as a concrete entry point into the question of rating divergence. Chapter 2.5 synthesizes the literature along a drivers, barriers and outcomes framework and identifies limitations and directions for future research. This chapter provides an answer to the first part of the research question on what theoretical insights the existing literature on ESG ratings provides.

The practical implementation is divided into two sub-chapters. In 3.1, the rating process will be reconstructed step by step from the perspective of the provider. In 3.2, this logic is mirrored from the perspective of the rated company along four steps: Strategic Anchoring, Provider Selection, Relationship Building and Continuous Engagement and Score Interpretation and Internal Anchoring. This chapter provides an answer to the second part of the research question on the practical implications that can be derived for an implementation by practitioners.

2 Literature review

Several systematic literature reviews on ESG ratings already exist, notably those by Clement et al. (2023), Halid et al. (2023) and La Torre et al. (2023), complemented by a wide range of individual contributions. Building on this body of work, the following definition and historical background consolidate the current state of the literature and provide the foundation for the analysis that follows.

A central challenge in the academic literature on ESG ratings lies in the lack of a unified definition of what ESG ratings represent and how they should be interpreted. Despite their widespread use in empirical research and investment practice, ESG ratings remain conceptually ambiguous, as they pursue different objectives and rely on diverse measurement logics.15Clement, A., Robinot, E. & Trespeuch, L. (PDF) The use of ESG scores in academic literature: a systematic literature review. ResearchGate https://doi.org/10.1108/JEC-10-2022-0147 (2023) doi:10.1108/JEC-10-2022-0147. Given the role assigned to ESG ratings within the Funnel Metaphor, the question of what these ratings actually capture is anything but secondary. This chapter therefore clarifies the core definitions and conceptual distinctions, traces the historical background of ESG and ESG ratings, examines the methodologies of leading rating providers and synthesizes the academic debate along the drivers, barriers and outcomes of ESG ratings.

2.1 Definition ESG ratings

To ensure conceptual clarity of this article, it is important to begin by clarifying terminology. In the existing academic literature, the terms “ESG Scores” and “ESG Ratings” are commonly used interchangeably and generally refer to the same concept. Both describe standardized assessments of a organizations environmental, social and governance characteristics. Literature still suggests a conceptual distinction for academic writing: “ESG Score” often denotes a quantitative output, typically a numerical value produced by Rating Providers.16Ferro, A., Marazzina, D. & Stocco, D. Uncovering ESG Ratings: The (Im)Balance of Aspirational and Performance Features. Corp. Soc. Responsib. Environ. Manag. 32, 5895–5917 (2025). “ESG Rating” can be used as the broader umbrella term, covering both quantitative scores and categorical assessments and can apply across different object types.10Pagano, M. S., Sinclair, G. & Yang, T. Understanding ESG ratings and ESG indexes. in Research Handbook of Finance and Sustainability 339–371 (Edward Elgar Publishing, Cheltenham, UK; Northampton, MA, USA, 2018). Ultimately, these are two sides of the same coin. For simplicity, this article uses the term “ESG ratings” to refer to both ESG ratings and ESG scores. Within this broader category, a further distinction is sometimes drawn between absolute ratings, which assess companies against a fixed scale, and “ESG Rankings”, which position companies relative to peers on a best-to-worst basis.17ERM Sustainability Institute. Rate the Raters 2025: ESG Ratings in Evolution – Corporate Survey Results. (2025).

In broad terms, ESG ratings are standardized, aggregated assessments produced by specialized rating agencies that evaluate firms against environmental, social and governance criteria. They condense a wide range of sustainability-related information into a structured indicator that allows comparison across firms, industries and markets.15Clement, A., Robinot, E. & Trespeuch, L. (PDF) The use of ESG scores in academic literature: a systematic literature review. ResearchGate https://doi.org/10.1108/JEC-10-2022-0147 (2023) doi:10.1108/JEC-10-2022-0147.,18Berg, F., Fabisik, K. & Sautner, Z. Is history repeating itself? The (un) predictable past of ESG ratings. SSRN Electron. J. 3722087, (2021).

Three structural features distinguish ESG ratings from comparable financial information products. First, they are not designed to capture a single, clearly defined outcome. While credit ratings assess one well-defined construct, the probability of default, ESG ratings aggregate heterogeneous dimensions that include risk exposure, management quality, broader environmental and social impacts and in some cases ethical considerations.19Berg, F., Kölbel, J. F. & Rigobon, R. Aggregate confusion: The divergence of ESG ratings. Rev. Finance 26, 1315–1344 (2022).,20Eccles, R. G. & Stroehle, J. C. Exploring social origins in the construction of ESG measures. SSRN Electron. J. https://ora.ox.ac.uk/objects/uuid:8b655ba6-a5d6-4774-a24f-8a235176a595 (2018). Stewart (2025) argues that rating providers therefore do not measure the same construct with varying degrees of accuracy, but conceptually different things, an observation that will be developed in detail in Chapter 2.5.2.4.14Stewart, R. Towards a better understanding of ESG ratings. J. Sustain. Finance Invest. 15, 624–643 (2025). Second, ESG ratings rely on data that is heterogeneous, only partly standardized and frequently disclosed on a voluntary basis. Third, methodologies are largely proprietary, which limits transparency regarding the choices that shape the final score.19Berg, F., Kölbel, J. F. & Rigobon, R. Aggregate confusion: The divergence of ESG ratings. Rev. Finance 26, 1315–1344 (2022).,20Eccles, R. G. & Stroehle, J. C. Exploring social origins in the construction of ESG measures. SSRN Electron. J. https://ora.ox.ac.uk/objects/uuid:8b655ba6-a5d6-4774-a24f-8a235176a595 (2018).

These structural features matter because ESG ratings are not passive descriptions of corporate behavior. As Ridgway observed in his early critique of performance measurement, what gets measured, gets managed.21Ridgway, V. F. Dysfunctional Consequences of Performance Measurements. Adm. Sci. Q. 1, 240–247 (1956). The composition of an ESG rating therefore shapes the behavior it intends to assess. Whether the current measurement infrastructure captures sustainability in a meaningful way, or whether it incentivises corporate responses that diverge from genuine sustainability outcomes, is a recurring question across the literature reviewed in this chapter.

2.1.1 Major research streams on ESG ratings

The academic literature on ESG ratings has developed across three disciplinary traditions that share a subject but approach it with fundamentally different questions.

The largest stream comes from financial economics. It treats ESG ratings as information products and asks whether they carry signal value for investor-relevant outcomes, stock returns, portfolio risk, cost of capital. The method is predominantly quantitative and financial materiality is the central concern. Friede et al. (2015), synthesising evidence from over 2,000 empirical studies, remain the most cited reference point within this tradition.9Friede, G., Busch, T. & Bassen, A. ESG and financial performance: aggregated evidence from more than 2000 empirical studies. J. Sustain. Finance Invest. 5, 210–233 (2015).

Management and organizational research forms a second stream. Rather than asking what ratings predict, it asks what they actually measure and how firms respond to them. Work on rating divergence, the social construction of rating methodologies and corporate responses to rating pressure all belong here.

A third stream, less cohesive than the other two, draws on sustainability science and political economy. Its concern is whether ESG ratings can meaningfully capture ecological and social performance at all. A question Ferro et al. (2025) approach empirically through their finding that roughly 60% of ESG scores reflect aspirational commitments rather than demonstrated performance.16Ferro, A., Marazzina, D. & Stocco, D. Uncovering ESG Ratings: The (Im)Balance of Aspirational and Performance Features. Corp. Soc. Responsib. Environ. Manag. 32, 5895–5917 (2025).

Financial economics assumes rating quality and studies outputs. Management research unpacks the construction process. Sustainability science questions the normative premises of the whole enterprise. The present review draws on all three, which is one reason a semi-systematic approach was chosen over a narrower systematic one.

2.2 Historical background and evolution of ESG and ESG ratings

An initial deep dive into the historical background and evolution of ESG and ESG ratings will serve as a foundation for the analysis that follows afterwards. This chapter therefore outlines the evolution of ESG ratings chronologically, starting from early forms of responsible investing and continuing to current market practices. By outlining how ESG concepts and actors have developed over time, this chapter forms the foundation to later clarify why ESG ratings are inherently complex and why they remain contested today.

2.2.1 Early roots and normative origins

Although today’s ESG market is often portrayed as a recent innovation, much of its underlying logic builds on older traditions of value-based investing. The literature commonly locates early roots in the concept of socially responsible investing (SRI) in the 1960s, which played only a limited role in mainstream capital markets for most of the twentieth century, despite being practiced for decades.22Billio, M., Costola, M., Hristova, I., Latino, C. & Pelizzon, L. Inside the ESG ratings: (Dis)agreement and performance. Corp. Soc. Responsib. Environ. Manag. 28, 1426–1445 (2021).,23Dorfleitner, G., Halbritter, G. & Nguyen, M. Measuring the level and risk of corporate responsibility – An empirical comparison of different ESG rating approaches. J. Asset Manag. 16, 450–466 (2015).,24Ballestero, E., Bravo, M., Pérez-Gladish, B., Arenas-Parra, M. & Plà-Santamaria, D. Socially Responsible Investment: A multicriteria approach to portfolio selection combining ethical and financial objectives. Eur. J. Oper. Res. 216, 487–494 (2012). Terminology in this field has not always been entirely consistent. While some authors use the term ethical investment to describe specialized retail funds, others treat SRI as a broader umbrella term that includes a range of related investment approaches incorporating ethical or social considerations.25Sparkes, R. & Cowton, C. J. The Maturing of Socially Responsible Investment: A Review of the Developing Link with Corporate Social Responsibility. J. Bus. Ethics 52, 45–57 (2004). Within this broader understanding, many of these approaches correspond in some way to Cowton’s (1994) definition of ethical investment as “the exercise of ethical and social criteria in the selection and management of investment portfolios”(p. 213)26Cowton, C. J. The development of ethical investment products. Ethical Confl. Finance 213–232 (1994)..

A defining feature of these early approaches of SRI was that “responsibility” was primarily operationalized through exclusionary screening. Investment decisions were shaped by normative judgments that varied across investors and contexts. As a result, portfolios were often built by avoiding activities seen as ethically problematic.20Eccles, R. G. & Stroehle, J. C. Exploring social origins in the construction of ESG measures. SSRN Electron. J. https://ora.ox.ac.uk/objects/uuid:8b655ba6-a5d6-4774-a24f-8a235176a595 (2018).,27Drempetic, S., Klein, C. & Zwergel, B. The influence of firm size on the ESG score: Corporate sustainability ratings under review. J. Bus. Ethics 333–360 (2020). In this context, “sin” screens (e.g., adult entertainment, alcohol, gambling, nuclear power, tobacco and weapons) illustrate differing moral views translated into varied investment rather than to standardized measurement systems.27Drempetic, S., Klein, C. & Zwergel, B. The influence of firm size on the ESG score: Corporate sustainability ratings under review. J. Bus. Ethics 333–360 (2020).

Closely related to this development, ideas from Corporate Social Responsibility (CSR) gained increasing attention from the 1970s onward. The academic literature contains a wide range of interpretations that reflect different views on the role of corporations in society.28Schneider, A. & Schmidpeter, R. Corporate Social Responsibility: Verantwortungsvolle Unternehmensführung in Theorie Und Praxis. (2012). doi:10.1007/978-3-642-25399-7. To bring more clarity to this debate, the European Commission offered a widely cited definition of CSR in 2011 as “process to integrate social, environmental, ethical and human rights concerns into their business operations and core strategy in close interaction with their stakeholders, with the aim [of] maximising the creation of shared value for their owners/shareholders and for their other stakeholders and society at large [as well as] identifying, preventing and mitigating their possible adverse impacts.” (p. 6)28Schneider, A. & Schmidpeter, R. Corporate Social Responsibility: Verantwortungsvolle Unternehmensführung in Theorie Und Praxis. (2012). doi:10.1007/978-3-642-25399-7.,29European Comission. MITTEILUNG DER KOMMISSION AN DAS EUROPÄISCHE PARLAMENT, DEN RAT, DEN EUROPÄISCHEN WIRTSCHAFTS- UND SOZIALAUSSCHUSS UND DEN AUSSCHUSS DER REGIONEN Eine Neue EU-Strategie (2011-14) Für Die Soziale Verantwortung Der Unternehmen (CSR). (2011)..

In parallel, the rise of CSR debates in the late twentieth century created a growing demand for structured information on a firm’s social and environmental conduct. Eccles and Stroehle (2018) link the data-collection infrastructure behind today’s ESG measurement back to the late 1970s, when sustainability issues began entering capital market considerations, often driven by NGOs.20Eccles, R. G. & Stroehle, J. C. Exploring social origins in the construction of ESG measures. SSRN Electron. J. https://ora.ox.ac.uk/objects/uuid:8b655ba6-a5d6-4774-a24f-8a235176a595 (2018). These organizations aimed to inform concerned investors about corporate involvement in disputed issues such as nuclear weapons development or Apartheid South Africa, anticipating the later role of “controversy” monitoring in ESG ratings.20Eccles, R. G. & Stroehle, J. C. Exploring social origins in the construction of ESG measures. SSRN Electron. J. https://ora.ox.ac.uk/objects/uuid:8b655ba6-a5d6-4774-a24f-8a235176a595 (2018).,30Escrig-Olmedo, E., Fernández-Izquierdo, M. Á., Ferrero-Ferrero, I., Rivera-Lirio, J. M. & Muñoz-Torres, M. J. Rating the Raters: Evaluating how ESG Rating Agencies Integrate Sustainability Principles. Sustainability 11, 915 (2019). Taken together, CSR and SRI provided the intellectual and practical context from which the later ESG concept emerged.20Eccles, R. G. & Stroehle, J. C. Exploring social origins in the construction of ESG measures. SSRN Electron. J. https://ora.ox.ac.uk/objects/uuid:8b655ba6-a5d6-4774-a24f-8a235176a595 (2018).,30Escrig-Olmedo, E., Fernández-Izquierdo, M. Á., Ferrero-Ferrero, I., Rivera-Lirio, J. M. & Muñoz-Torres, M. J. Rating the Raters: Evaluating how ESG Rating Agencies Integrate Sustainability Principles. Sustainability 11, 915 (2019). At this stage, however, sustainability-related investment approaches remained largely normative, fragmented in their application, and only marginally integrated into mainstream financial analysis.

2.2.2 Early non-financial research and data infrastructure

Before ESG became a clearly defined concept, important parts of its later informational infrastructure had already begun to develop. By the late 1980s and early 1990s, extra-financial research had moved beyond ad hoc data collection and become more systematic, even though the term “ESG” was not yet widely used. Organizations providing information to SRI-focused investors expanded their coverage and developed more structured research practices. During this period, several organizations were founded that later became central actors in the ESG ratings landscape, including KLD Research & Analytics in the United States (1988), EIRIS in the United Kingdom (1983), and Jantzi Research in Canada (1992). These organizations developed structured databases to assess corporate environmental and social performance, often shaped by explicit normative or mission-driven goals rather than purely financial objectives.20Eccles, R. G. & Stroehle, J. C. Exploring social origins in the construction of ESG measures. SSRN Electron. J. https://ora.ox.ac.uk/objects/uuid:8b655ba6-a5d6-4774-a24f-8a235176a595 (2018).

At the same time, the underlying informational infrastructure remained relatively simple, relying mainly on qualitative assessments, company disclosure and media reports rather than standardized metrics, which contributed to substantial heterogeneity in coverage and evaluation criteria. Governance-related assessments initially played a less prominent role, as early rating providers on nonfinancial information focused primarily on environmental and social dimensions.20Eccles, R. G. & Stroehle, J. C. Exploring social origins in the construction of ESG measures. SSRN Electron. J. https://ora.ox.ac.uk/objects/uuid:8b655ba6-a5d6-4774-a24f-8a235176a595 (2018).

Nevertheless, this period established the core idea that corporate behavior beyond financial performance could and should be systematically evaluated. At the same time, it created important path dependencies. Because these early research practices emerged from different institutional settings and served different purposes, they contributed to the methodological heterogeneity that continues to shape ESG ratings today, which will be further detailed in chapter 2.3 and 2.4.

2.2.3 Emergence of the concept of ESG

A consistent finding across the literature is that the concept of ESG emerged relatively late compared to earlier forms of SRI and CSR. While sustainability-related investment practices and related data had existed for decades, the explicit framing of environmental, social and governance issues under the unified label “ESG” only emerged as a widely used concept in the early 2000s.

The institutionalisation of ESG is commonly linked to two key UN-related initiatives. First, the 2004 United Nations Global Compact report Who Cares Wins: Connecting Financial Markets to a Changing World explicitly promoted the integration of ESG factors into financial analysis.14Stewart, R. Towards a better understanding of ESG ratings. J. Sustain. Finance Invest. 15, 624–643 (2025).,20Eccles, R. G. & Stroehle, J. C. Exploring social origins in the construction of ESG measures. SSRN Electron. J. https://ora.ox.ac.uk/objects/uuid:8b655ba6-a5d6-4774-a24f-8a235176a595 (2018).,31Chen, S., Song, Y. & Gao, P. Environmental, social, and governance (ESG) performance and financial outcomes: Analyzing the impact of ESG on financial performance. J. Environ. Manage. 345, 118829 (2023). Second, the 2005 Freshfields Report, produced under the UNEP Finance Initiative, addressed the legal implications of considering ESG issues in investment decision-making. Together, these initiatives played a central role in translating sustainability concerns into a language compatible with financial markets.14Stewart, R. Towards a better understanding of ESG ratings. J. Sustain. Finance Invest. 15, 624–643 (2025).,16Ferro, A., Marazzina, D. & Stocco, D. Uncovering ESG Ratings: The (Im)Balance of Aspirational and Performance Features. Corp. Soc. Responsib. Environ. Manag. 32, 5895–5917 (2025).,20Eccles, R. G. & Stroehle, J. C. Exploring social origins in the construction of ESG measures. SSRN Electron. J. https://ora.ox.ac.uk/objects/uuid:8b655ba6-a5d6-4774-a24f-8a235176a595 (2018).,32Shi, Y. & Yao, T. ESG Rating Divergence: Existence, Driving Factors, and Impact Effects. Sustainability 17, 4717 (2025).,33Shen, Y. ESG and firm performance: A literature review. BCP Bus. Manag. 46, 283–288 (2023).

They helped reframe ESG considerations by linking them explicitly to financial materiality and the launch of the UN Principles for Responsible Investment in 2005 provided an institutional frame for translating this thought into investor practice.34Abhayawansa, S. Swimming against the tide: back to single materiality for sustainability reporting. Sustain. Account. Manag. Policy J. 13, 1361–1385 (2022). For the rating industry, the practical significance of this shift was that demand for structured, comparable sustainability information now came from mainstream investors rather than only from value-based niches. The stage was set for the later expansion of ESG ratings and their integration into mainstream investment analysis.10Pagano, M. S., Sinclair, G. & Yang, T. Understanding ESG ratings and ESG indexes. in Research Handbook of Finance and Sustainability 339–371 (Edward Elgar Publishing, Cheltenham, UK; Northampton, MA, USA, 2018).,35Christensen, D. M., Serafeim, G. & Sikochi, A. (Siko). Why is Corporate Virtue in the Eye of the Beholder? The Case of ESG Ratings. SSRN Scholarly Paper at https://papers.ssrn.com/abstract=3793804 (2021).

2.2.4 Mainstream ESG investing

Following its institutionalisation in the early 2000s, ESG investing entered a period of rapid expansion and moved into the financial mainstream. The niche form of SRI gained broader acceptance and increasingly became part of general investment thinking rather than a specialized ethical approach.22Billio, M., Costola, M., Hristova, I., Latino, C. & Pelizzon, L. Inside the ESG ratings: (Dis)agreement and performance. Corp. Soc. Responsib. Environ. Manag. 28, 1426–1445 (2021).

One way this mainstreaming becomes visible is through the changing definition of sustainable investing itself. While earlier approaches to responsible investment mainly relied on ethical screening and exclusion strategies, as described before, Abhayawansa and Tyagi (2021) characterise sustainable investing as an approach that explicitly considers ESG factors in investment decision-making, marking a move beyond purely financial signals.34Abhayawansa, S. Swimming against the tide: back to single materiality for sustainability reporting. Sustain. Account. Manag. Policy J. 13, 1361–1385 (2022).

The mainstreaming of ESG investing was also reflected in rapid market growth. Assets under management (AUM) applying ESG-related investment strategies increased from around US$4 trillion in 2006 to approximately US$60 trillion by 2016 at an annualized rate of 35%.10Pagano, M. S., Sinclair, G. & Yang, T. Understanding ESG ratings and ESG indexes. in Research Handbook of Finance and Sustainability 339–371 (Edward Elgar Publishing, Cheltenham, UK; Northampton, MA, USA, 2018). Similarly, the expansion of investor initiatives further signals the increasing institutional adoption of ESG. The AUM represented by members of the PRI, for instance, grew from only a few hundred billion dollars in the early years after their introduction in 2005 to more than US$100 trillion by 2020.36Serafeim, G. & Yoon, A. Stock price reactions to ESG news: the role of ESG ratings and disagreement. Rev. Account. Stud. 28, 1500–1530 (2023).

In parallel, ESG considerations became more visible also at the firm level. The number of companies reporting ESG-related information increased substantially, rising from fewer than 20 firms in the early 1990s to nearly 6000 firms by 2014, reflecting the growing relevance of sustainability-related information for investors and other stakeholders.36Serafeim, G. & Yoon, A. Stock price reactions to ESG news: the role of ESG ratings and disagreement. Rev. Account. Stud. 28, 1500–1530 (2023). At the firm level, ESG considerations also became more embedded in corporate evaluation. Chen et al. (2023) for example show that ESG performance increasingly came to be treated as an indicator of a firm’s commitments to environmental protection and social responsibility, suggesting that ESG was no longer understood merely as reputational rhetoric, but as a structured lens through which corporate behavior was assessed on nonfinancial criteria by investors and other stakeholders.31Chen, S., Song, Y. & Gao, P. Environmental, social, and governance (ESG) performance and financial outcomes: Analyzing the impact of ESG on financial performance. J. Environ. Manage. 345, 118829 (2023). Chen et al. (2023) also link this mainstreaming of ESG to a broader ecosystem of market institutions and note that ESG investment entered a phase of rapid development alongside initiatives such as the Sustainable Stock Exchanges Initiative (SSEi), which supported the integration of ESG consideration at the level of stock exchanges.31Chen, S., Song, Y. & Gao, P. Environmental, social, and governance (ESG) performance and financial outcomes: Analyzing the impact of ESG on financial performance. J. Environ. Manage. 345, 118829 (2023).

As ESG investing expanded, so did the demand for comparable and systematic information on corporate sustainability performance. This created favorable conditions for the emergence of ESG ratings as scalable market tools.

2.2.5 ESG ratings as a commercial information product

Building on this growing demand, early research practices evolved into a distinct market for ESG ratings designed to assess and represent firms’ ESG performance in a scalable way. Rather than remaining specialized outputs for niche responsible investors, ESG assessments increasingly became standardized tools that translated diverse sustainability-related information into metrics usable at scale.22Billio, M., Costola, M., Hristova, I., Latino, C. & Pelizzon, L. Inside the ESG ratings: (Dis)agreement and performance. Corp. Soc. Responsib. Environ. Manag. 28, 1426–1445 (2021). They functioned as intermediaries that reduced informational complexity and made ESG considerations actionable for financial market participants. This shift also changed how sustainability information was perceived more broadly. Major credit rating agencies such as Moody’s, S&P and Fitch began incorporating ESG-related assessments into their analytical frameworks, reflecting a move from treating sustainability as an ethical concern toward treating it as financially relevant information for risk assessment and investment analysis.10Pagano, M. S., Sinclair, G. & Yang, T. Understanding ESG ratings and ESG indexes. in Research Handbook of Finance and Sustainability 339–371 (Edward Elgar Publishing, Cheltenham, UK; Northampton, MA, USA, 2018).

The period following the global financial crisis marked an important turning point. Growing investor demand, combined with advances in data processing and financial analytics, transformed ESG ratings into a commercially attractive market segment.10Pagano, M. S., Sinclair, G. & Yang, T. Understanding ESG ratings and ESG indexes. in Research Handbook of Finance and Sustainability 339–371 (Edward Elgar Publishing, Cheltenham, UK; Northampton, MA, USA, 2018).,30Escrig-Olmedo, E., Fernández-Izquierdo, M. Á., Ferrero-Ferrero, I., Rivera-Lirio, J. M. & Muñoz-Torres, M. J. Rating the Raters: Evaluating how ESG Rating Agencies Integrate Sustainability Principles. Sustainability 11, 915 (2019).

This phase was characterized by extensive mergers and acquisitions, which led to the integration of ESG data into large financial information platforms.10Pagano, M. S., Sinclair, G. & Yang, T. Understanding ESG ratings and ESG indexes. in Research Handbook of Finance and Sustainability 339–371 (Edward Elgar Publishing, Cheltenham, UK; Northampton, MA, USA, 2018).,13Larcker, D. F., Pomorski, L., Tayan, B. & Watts, E. M. ESG Ratings: A Compass without Direction. SSRN Scholarly Paper at https://papers.ssrn.com/abstract=4179647 (2022). The acquisition of RiskMetrics Group by MSCI in 2010 served as an early and consequential example, consolidating ESG pioneers such as KLD and Innovest under a single umbrella.10Pagano, M. S., Sinclair, G. & Yang, T. Understanding ESG ratings and ESG indexes. in Research Handbook of Finance and Sustainability 339–371 (Edward Elgar Publishing, Cheltenham, UK; Northampton, MA, USA, 2018).,20Eccles, R. G. & Stroehle, J. C. Exploring social origins in the construction of ESG measures. SSRN Electron. J. https://ora.ox.ac.uk/objects/uuid:8b655ba6-a5d6-4774-a24f-8a235176a595 (2018).,32Shi, Y. & Yao, T. ESG Rating Divergence: Existence, Driving Factors, and Impact Effects. Sustainability 17, 4717 (2025). Similar consolidation followed in Europe with the merger of Vigeo and EIRIS in 2015.1026. Further transactions included Morningstar’s acquisition of 40% of Sustainalytics in 2017 and both Moody’s purchase of Vigeo-Eiris and S&P Global’s acquisition of RobecoSAM in 2019.10Pagano, M. S., Sinclair, G. & Yang, T. Understanding ESG ratings and ESG indexes. in Research Handbook of Finance and Sustainability 339–371 (Edward Elgar Publishing, Cheltenham, UK; Northampton, MA, USA, 2018).

Consolidation expanded the global reach of ESG data and made it easier to embed ESG metrics in financial products such as indices and ETFs. At the same time, it strengthened the proprietary character of ESG methodologies and reduced transparency around weighting and aggregation.13Larcker, D. F., Pomorski, L., Tayan, B. & Watts, E. M. ESG Ratings: A Compass without Direction. SSRN Scholarly Paper at https://papers.ssrn.com/abstract=4179647 (2022).

The various social origins help to explain why ESG ratings never converged around a single, universally accepted definition.14Stewart, R. Towards a better understanding of ESG ratings. J. Sustain. Finance Invest. 15, 624–643 (2025).,19Berg, F., Kölbel, J. F. & Rigobon, R. Aggregate confusion: The divergence of ESG ratings. Rev. Finance 26, 1315–1344 (2022).,20Eccles, R. G. & Stroehle, J. C. Exploring social origins in the construction of ESG measures. SSRN Electron. J. https://ora.ox.ac.uk/objects/uuid:8b655ba6-a5d6-4774-a24f-8a235176a595 (2018).,22Billio, M., Costola, M., Hristova, I., Latino, C. & Pelizzon, L. Inside the ESG ratings: (Dis)agreement and performance. Corp. Soc. Responsib. Environ. Manag. 28, 1426–1445 (2021).,37Liu, M. Quantitative ESG disclosure and divergence of ESG ratings. Front. Psychol. 13, (2022).

2.2.6 Current ESG backlash

In recent years, the mainstream view on ESG has begun to shift again. Blum (2025) describes this backlash as a reaction to the rapid expansion of ESG ratings during an ongoing “ESG rush”.38Blum, V. From the ESG Rush to the ESG Backlash: A Western Story. SSRN Scholarly Paper at https://doi.org/10.2139/ssrn.5238272 (2025). As ESG ratings became integrated in investment processes and regulatory discussions, expectations regarding their ability to capture sustainability outcomes increased substantially. When ESG-labeled investments appeared to underperform or when highly rated firms later became involved in major controversies, dissatisfaction with ESG ratings intensified.38Blum, V. From the ESG Rush to the ESG Backlash: A Western Story. SSRN Scholarly Paper at https://doi.org/10.2139/ssrn.5238272 (2025). One widely cited example of these concerns is the case of Tesla. In 2018, the car manufacturer received an exemplary “AA” environmental rating from MSCI, while FTSE assessed Tesla very poorly and Sustainalytics placed it around the middle of its peer group.39Dimson, E., Marsh, P. & Staunton, M. Divergent ESG ratings. https://doi.org/10.17863/CAM.55949 (2020) doi:10.17863/CAM.55949.,40Gibson Brandon, R., Krueger, P. & Schmidt, P. S. ESG Rating Disagreement and Stock Returns. Financ. Anal. J. 77, 104–127 (2021). These differences reflect the contrasting methodological choices of rating agencies and reinforce the doubts about what ESG ratings actually measure and how reliably they reflect the sustainability performance. According to Blum (2025) the gap between expectations and what ESG ratings can realistically measure is a central driver of the backlash, which she interprets as partly rooted in an attribute substitution confusion: The tendency to mistake proxy indicators for real-world sustainability outcomes.38Blum, V. From the ESG Rush to the ESG Backlash: A Western Story. SSRN Scholarly Paper at https://doi.org/10.2139/ssrn.5238272 (2025). This discussion represents only a small part of the broader academic debate on the divergence of ESG ratings, which will be examined in detail in chapter 2.5.2.4.

Along with methodological and informational concerns, the ESG backlash also has a clear political root. Sætra (2025) situates the backlash within broader ideological conflicts, particularly in the United States, where ESG has increasingly been framed as a form of political or activist intervention in markets.41Sætra, H. S. The ESG Backlash: Politics, Ideology, and the Future of Sustainable Business. SSRN Scholarly Paper at https://doi.org/10.2139/ssrn.4782018 (2024). From this perspective, criticism of ESG reflects ongoing debates about shareholder versus stakeholder capitalism and concerns about what critics perceive as excessive regulation or progressive social agendas embedded in corporate decision-making. As ESG became associated with issues such as climate policy, diversity and social justice, it moved beyond the technical domain of investment analysis and entered a polarized political arena, thereby intensifying backlash dynamics.41Sætra, H. S. The ESG Backlash: Politics, Ideology, and the Future of Sustainable Business. SSRN Scholarly Paper at https://doi.org/10.2139/ssrn.4782018 (2024).

The ESG backlash marks the most recent stage in the historical evolution of ESG and ESG ratings. It highlights that ESG ratings have reached a level of influence at which their limitations are no longer only academic concerns but have tangible market and political consequences. The underlying market infrastructure and practical implications for ESG rating agencies of these developments will be examined in more detail in the following section. In context of this wiki entry, understanding the origins of the backlash provides an important bridge to the following look at ESG rating methodologies and the divergence of ESG ratings.

2.3 The ESG rating market

ESG ratings have become a central component of modern financial markets. Understanding their role therefore requires examining the structure and characteristics of the ESG rating market.

The OECD notes that the market for ESG data products and related services exceeded USD 1.5 billion in 2023 and continued to grow rapidly with an expected growth rate of 23% through 2025.42OECD. Behind ESG ratings: Unpacking sustainability metrics. OECD https://www.oecd.org/en/publications/behind-esg-ratings_3f055f0c-en.html (2025) doi:10.1787/3f055f0c-en. ESG metrics and ratings have become a central input into investment and corporate decision-making. US-based institutional investors spent on average around USD 487,000 per year on external ESG rating and data services in 2022, with total expenditures estimated to be about 2.5 times higher than for traditional credit rating services.43ERM. Costs and Benefits of Climate-Related Disclosure Activities by Corporate Issuers and Institutional Investors. ERM https://www.erm.com/insights/costs-and-benefits-of-climate-related-disclosure-activities-by-corporate-issuers-and-institutional-investors/. Despite these costs, the demand for ESG data continues to rise, underlining the growing reliance of market participants on external ESG information.42OECD. Behind ESG ratings: Unpacking sustainability metrics. OECD https://www.oecd.org/en/publications/behind-esg-ratings_3f055f0c-en.html (2025) doi:10.1787/3f055f0c-en.

The market environment in which ESG rating agencies operate is continuously evolving. The dynamics around the EU Corporate Sustainability Reporting Directive (CSRD) and the growing adoption of the International Sustainability Standards Board (ISSB) framework are reshaping the availability and standardization of ESG data.17ERM Sustainability Institute. Rate the Raters 2025: ESG Ratings in Evolution – Corporate Survey Results. (2025). At the same time, the aforementioned increasing political and societal backlash against ESG has led to a closer review of rating methodologies and their underlying assumptions. This is also supported by evolving regulatory requirements for ESG and impact investment products, particularly those aimed at addressing greenwashing risks.17ERM Sustainability Institute. Rate the Raters 2025: ESG Ratings in Evolution – Corporate Survey Results. (2025).,42OECD. Behind ESG ratings: Unpacking sustainability metrics. OECD https://www.oecd.org/en/publications/behind-esg-ratings_3f055f0c-en.html (2025) doi:10.1787/3f055f0c-en. More on that in chapter 2.5.1.

In this more dynamic environment, ESG rating agencies need to demonstrate a considerable degree of adaptability. As shown before, organizational restructuring and mergers between several players have become common practice among rating agencies, as well as ongoing refinements of their methodology. This is reflected, for example, in the increasing integration of materiality-driven frameworks and more granular data structures.22Billio, M., Costola, M., Hristova, I., Latino, C. & Pelizzon, L. Inside the ESG ratings: (Dis)agreement and performance. Corp. Soc. Responsib. Environ. Manag. 28, 1426–1445 (2021). MSCI, for example, has continuously refined its methodology by strengthening its focus on financially material ESG issues and expanding its use of alternative data sources, including controversy monitoring and external datasets, to improve the risk assessment.44MSCI, E. MSCI ESG ratings methodology. (2022). At the same time, the weighting of key issues has been more closely aligned with industry-specific risk exposure. The result is a increasingly data-driven approach to materiality.

2.3.1 Major ESG rating providers and their methodologies

Most leading providers are oriented toward the investment community, assessing how firms manage sustainability risks and perform on ESG-related issues. At the same time, ESG ratings are also relevant for a broader set of stakeholders, including employees, business partners and customers.10Pagano, M. S., Sinclair, G. & Yang, T. Understanding ESG ratings and ESG indexes. in Research Handbook of Finance and Sustainability 339–371 (Edward Elgar Publishing, Cheltenham, UK; Northampton, MA, USA, 2018).,14Stewart, R. Towards a better understanding of ESG ratings. J. Sustain. Finance Invest. 15, 624–643 (2025).

ESG rating agencies differ in their methodological approaches. Some follow an active model, collecting data directly from companies through questionnaires and engagement, while others rely primarily on publicly available information complemented by company feedback. To provide an overview of the ESG rating market today, Table 1 shows the eight leading ESG data vendors providing ESG ratings, selected based on market share and company coverage.

The market is shaped by a relatively small group of globally recognized providers. According to Opimas data, these eight providers together account for about 86% of the estimated ESG data providers market share in 2023.45Opimas. Market Share of ESG Data Vendors. Opimas: We begin with an understanding https://www.opimas.com/research/976/detail/ (2024). This indicates a relatively high level of market concentration, despite the presence of numerous smaller or specialized providers. The ESG rating market can be described as relatively dynamic as mergers and acquisitions occur regularly, as described in the historical background.

Table 1: Overview of the most relevant rating agencies

| MSCI46MSCI. ESG Ratings Methodology. (2024). | S&P Global ESG47S&P Global. S&P Global ESG Score: Methodology. (2025). | ISS ESG48ISS ESG. ESG Corporate Rating: Methodology and Process. (2025). | Moody’s49Moody’s. General Principles for Assessing Environmental, Social and Governance Risks Methodology. (2021). | |

|---|---|---|---|---|

| Rating Score | CCC – AAA | 0 – 100 | D-/1.00 – A+/4.00 with industry-specific prime labels | 5 – 1 |

| Ownership Type17ERM Sustainability Institute. Rate the Raters 2025: ESG Ratings in Evolution – Corporate Survey Results. (2025). | Financial data firm (public company) | Credit rater (public company) | Stock exchange-owned (Deutsche Börse subsidiary) | Credit rater (public company) |

| Primary Rating Objective | Opinion of companies’ management of financially relevant ESG risks and opportunities | Performance on and management of material ESG risks, opportunities and impacts | ESG performance: manage material risks, mitigate negative / generate positive impacts, capture opportunities | Measurement of the integration of material ESG impact into credit analysis / credit risk |

| Data Sources | 100+ specialized datasets, company disclosures, 3,400+ media sources | 62 industry-specific company questionnaires + supporting evidence; public data for non-responders, media & stakeholder analysis | Company disclosure + third-party sources; in-house analyst research; company dialogue, media sources | Company disclosures; relevant third-party sources; non-public issuer information; internal credit and sector research |

| N Criteria | 33 | Up to 30 | Ca. 100 | No fixed number of criteria |

| Main Risk Factors | Climate, natural capital, pollution, product liability, stakeholder opposition, governance, opportunities | E/S/G core and industry-specific factors; risk exposure and management quality, stakeholder and environmental impacts, controversies | Not only risk exposures, but also staff & suppliers; society & product responsibility; governance & business ethics; environmental management; products & services | ESG risks that can materially impact cash flows, costs or risk profile |

| Materiality | Only industry-material issues | Double materiality; industry / sub-industry specific | Double materiality; industry- and sub-industry-specific key issues | Financial materiality: only credit-relevant ESG factors; issuer- and sector-specific |

| Weighting | Depending on the industry: E & S issues typically 5–30% each / G issues min. 33% | Industry-specific weighting, 40–50% core cross-industry criteria / 50–60% industry-specific criteria | Industry-specific weighting scenarios; key issues usually 50–80% of total score; product/service impact can get 10–50% | No fixed additive weighting like classic ESG ratings; qualitative integration into issuer profile and credit impact scores |

| Ecovadis50Ecovadis. EcoVadis Ratings: Methodology Overview and Principles. (2025). | Sustainalytics51Sustainalytics. The ESG Risk Ratings: Methodology Abstract Version 3.1. (2024). | LSEG/Refinitiv52LSEG. Environmental, Social and Governance scores from LSEG. (2024). | Bloomberg53Bloomberg. Bloomberg ESG Scores: Methodology. (2025). | |

|---|---|---|---|---|

| Rating Score | 0 – 100 | 50 – 0 | D- to A+ & 0 – 100 | D- to A+ & 0 – 100 |

| Ownership Type17ERM Sustainability Institute. Rate the Raters 2025: ESG Ratings in Evolution – Corporate Survey Results. (2025). | Independent (private company) | Financial data firm (Morningstar subsidiary) | Stock exchange-owned (LSE subsidiary) | Financial data firm (private company) |

| Primary Rating Objective | Measurement of quality of sustainability management systems | Measurement of ESG-driven risk to enterprise value (unmanaged ESG risk level) | Measurement of relative ESG performance, commitment, and effectiveness | Measurement of exposure to and management of financially material ESG factors |

| Data Sources | Evidence-based company documents, questionnaires, third-party sources | Public company disclosures, company-provided data, Morningstar data, third-party sources (NGOs, media, regulators), automated web scraping | Public company disclosures, NGO data, media; processed by 600+ analysts | Public company disclosures, Bloomberg data, BI research; limited estimation where needed |

| N Criteria | 21 | 22 | 186 | Over 30 |

| Main Risk Factors | ESG risks and impacts across environment, labor & human rights, ethics & sustainable procurement; stakeholder controversies | Material ESG risks via exposure + management lens; includes systemic and idiosyncratic risks, controversies | ESG performance and exposure across 10 themes (e.g., emissions, human rights, governance); includes controversies overlay | Financially material ESG risks and opportunities (E/S) + governance practices; based on industry-specific key issues |

| Materiality | Industry-, size-, and geography-specific materiality | Financial materiality | Financial materiality | Financial materiality |

| Weighting | Based on policies, actions and results with the final score being the weighted average of theme scores | Issue weights implicit via exposure, betas and manageable risk factors (30–100%) with the final score being the sum of issue-level unmanaged risks | Category weights derived from industry-specific materiality matrix | Industry-specific weighting derived from materiality and statistical modeling |

Today’s leading ESG raters can be grouped into four primary ownership categories: financial data companies, stock exchange-owned entities, credit rating agencies and independent firms.17ERM Sustainability Institute. Rate the Raters 2025: ESG Ratings in Evolution – Corporate Survey Results. (2025).,38Blum, V. From the ESG Rush to the ESG Backlash: A Western Story. SSRN Scholarly Paper at https://doi.org/10.2139/ssrn.5238272 (2025). As Blum (2025) notes, in just twenty years of existence, the ESG rating market has undergone a dramatic consolidation toward an oligopolistic structure, with major financial institutions absorbing formerly independent ESG pioneers.38Blum, V. From the ESG Rush to the ESG Backlash: A Western Story. SSRN Scholarly Paper at https://doi.org/10.2139/ssrn.5238272 (2025). These distinct ownership models are not just structural characteristics, they shape the commercial incentives, methodological priorities and target audiences of each provider.38Blum, V. From the ESG Rush to the ESG Backlash: A Western Story. SSRN Scholarly Paper at https://doi.org/10.2139/ssrn.5238272 (2025).

These providers differ not only in size and coverage, but also in their positioning and target audience. MSCI, Sustainalytics, S&P Global and ISS ESG are primarily oriented toward the investment community, acting as intermediaries that assess how firms manage sustainability risks and perform on ESG-related issues.46MSCI. ESG Ratings Methodology. (2024).,47S&P Global. S&P Global ESG Score: Methodology. (2025).,48ISS ESG. ESG Corporate Rating: Methodology and Process. (2025).,54Sustainalytics. The ESG Risk Ratings – Methodology Abstract: Version 3.1. (2024). Bloomberg and LSEG focus more strongly on processing and standardising large volumes of publicly available ESG data for financial market participants.52LSEG. Environmental, Social and GOvernance scores from LSEG. (2024).,53Bloomberg. Bloomberg ESG Scores: Methodology. (2025). EcoVadis specialises in supply chain assessments, particularly for business-to-business relationships.50Ecovadis. EcoVadis Ratings: Methodology Overview and Principles. (2025). Moody’s integrates ESG considerations into credit risk analysis rather than producing a standalone ESG performance score.49Moody`s. General Principles for Assessing Environmental, Social and Governance Risks Methodology. (2021).

Another central distinction between ESG rating providers lies in their underlying conceptual approach, particularly whether ratings are designed to capture financially material ESG risks or broader environmental and social impacts. MSCI and Sustainalytics center their approaches on financially material ESG risks.46MSCI. ESG Ratings Methodology. (2024).,54Sustainalytics. The ESG Risk Ratings – Methodology Abstract: Version 3.1. (2024). S&P Global and ISS ESG go beyond this and explicitly incorporate opportunities and broader impacts.47S&P Global. S&P Global ESG Score: Methodology. (2025).,48ISS ESG. ESG Corporate Rating: Methodology and Process. (2025). EcoVadis focuses on the quality of sustainability management systems, based on policies, actions and results of sustainability efforts of the above-mentioned B2B relationships.50Ecovadis. EcoVadis Ratings: Methodology Overview and Principles. (2025). These differences highlight that ESG ratings do not capture a single, clearly defined concept, but reflect distinct analytical perspectives.

Differences also exist in how providers collect and process information. S&P Global and EcoVadis rely on active data collection through company questionnaires and direct engagement.47S&P Global. S&P Global ESG Score: Methodology. (2025).,50Ecovadis. EcoVadis Ratings: Methodology Overview and Principles. (2025). In contrast, MSCI, LSEG and Bloomberg primarily use publicly available information, complemented by company feedback.46MSCI. ESG Ratings Methodology. (2024).,52LSEG. Environmental, Social and GOvernance scores from LSEG. (2024).,53Bloomberg. Bloomberg ESG Scores: Methodology. (2025). Sustainalytics and ISS ESG combine reported data with third-party sources, media screening and controversy analysis.48ISS ESG. ESG Corporate Rating: Methodology and Process. (2025).,54Sustainalytics. The ESG Risk Ratings – Methodology Abstract: Version 3.1. (2024). As a result, the underlying data basis varies significantly across providers.

The structure of the assessment frameworks also differs. MSCI works with 35 key issues, while EcoVadis uses 21 criteria organized around management practices.46MSCI. ESG Ratings Methodology. (2024).,50Ecovadis. EcoVadis Ratings: Methodology Overview and Principles. (2025). Sustainalytics assesses 22 material ESG issues.54Sustainalytics. The ESG Risk Ratings – Methodology Abstract: Version 3.1. (2024). In contrast, LSEG relies on a highly granular system with hundreds of indicators, and ISS ESG evaluates around 100 indicators per industry.48ISS ESG. ESG Corporate Rating: Methodology and Process. (2025).,52LSEG. Environmental, Social and GOvernance scores from LSEG. (2024). Moody’s does not follow a fixed ESG criteria catalogue.49Moody`s. General Principles for Assessing Environmental, Social and Governance Risks Methodology. (2021).

Another dimension of differentiation is the treatment of materiality. Whereas MSCI, Sustainalytics and Bloomberg predominantly follow a financial materiality perspective, S&P Global and ISS ESG incorporate elements of double materiality by considering both financial risks and broader environmental and social impacts.46MSCI. ESG Ratings Methodology. (2024).,47S&P Global. S&P Global ESG Score: Methodology. (2025).,48ISS ESG. ESG Corporate Rating: Methodology and Process. (2025).,53Bloomberg. Bloomberg ESG Scores: Methodology. (2025).,54Sustainalytics. The ESG Risk Ratings – Methodology Abstract: Version 3.1. (2024). EcoVadis, in turn, applies a context-specific approach in which materiality depends on industry, size and geographic exposure.50Ecovadis. EcoVadis Ratings: Methodology Overview and Principles. (2025). These differing interpretations of materiality further contribute to inconsistencies across ESG ratings.

Finally, there is no common approach to the weighting and aggregation of ESG factors. MSCI assigns weights at the level of industry-specific key issues, with governance receiving a minimum share.46MSCI. ESG Ratings Methodology. (2024). S&P Global determines weights through its industry-specific assessment framework within the Corporate Sustainability Assessment.47S&P Global. S&P Global ESG Score: Methodology. (2025). ISS ESG uses industry-specific weighting scenarios in which key issues dominate the score.48ISS ESG. ESG Corporate Rating: Methodology and Process. (2025). Sustainalytics derives weights implicitly from exposure and management assessments rather than fixed pillar weights.54Sustainalytics. The ESG Risk Ratings – Methodology Abstract: Version 3.1. (2024). LSEG and Bloomberg base their weighting on materiality matrices and statistical models.52LSEG. Environmental, Social and GOvernance scores from LSEG. (2024).,53Bloomberg. Bloomberg ESG Scores: Methodology. (2025). Moody’s, again, does not aggregate ESG factors into a single ESG score but integrates them qualitatively into credit ratings.53Bloomberg. Bloomberg ESG Scores: Methodology. (2025).

Moody’s takes a somewhat different role in the ESG rating market. Following its 2024 partnership with MSCI, the focus has shifted further toward integrating ESG and climate data into credit risk analysis rather than providing a standalone ESG rating. Therefore, while Moody’s remains relevant in the ESG data landscape, it is better understood as linking ESG factors to financial risk instead of acting as a traditional ESG rating provider.49Moody`s. General Principles for Assessing Environmental, Social and Governance Risks Methodology. (2021).

At the same time, ESG rating methodologies are largely proprietary, which limits transparency regarding data selection, weighting and aggregation. As a result, users of ESG ratings often face challenges in fully understanding how scores are constructed and how different dimensions are reflected in the final assessment. This limited transparency reflects the commercial nature of ESG ratings as data-driven products and represents a defining characteristic of the current ESG rating market.19Berg, F., Kölbel, J. F. & Rigobon, R. Aggregate confusion: The divergence of ESG ratings. Rev. Finance 26, 1315–1344 (2022).

2.3.2 Correlation of ESG ratings among each other

Given the methodological differences across ESG rating providers, an important aspect examined in literature is the degree of agreement between ESG ratings and the respective dimension. Berg et al. (2022) provide empirical evidence on the correlation of ratings across major providers and show that this agreement is only moderate.

The authors report an average correlation of approximately 0.54 across Sustainalytics, S&P Global ESG, Moody`s ESG, Refinitiv LSEG, KLD and MSCI, with values ranging from 0.38 to 0.71.19Berg, F., Kölbel, J. F. & Rigobon, R. Aggregate confusion: The divergence of ESG ratings. Rev. Finance 26, 1315–1344 (2022). They explicitly include KLD as a separate data source, although it has been acquired by MSCI via RiskMetrics, as it continues to exist as a distinct dataset and is widely used in academic research.

In this wiki entry, KLD is excluded from the analysis to avoid double counting conceptually and historically related data sources, as KLD forms part of MSCI’s ESG data infrastructure. In addition, the analysis focuses on the current ESG rating market landscape, in which KLD no longer operates as an independent provider. Focusing on the remaining providers results in a slightly higher average correlation of approximately 0.57 at the aggregate ESG level. Similarly, Billio et al. (2021) find an average correlation of around 0.58 between Sustainalytics, RobecoSAM, Refinitiv and MSCI.22Billio, M., Costola, M., Hristova, I., Latino, C. & Pelizzon, L. Inside the ESG ratings: (Dis)agreement and performance. Corp. Soc. Responsib. Environ. Manag. 28, 1426–1445 (2021).

The pairwise comparison in Table

2 show that the highest level of agreement is observed between Sustainalytics and Moody’s ESG, with a correlation of 0.71. When breaking down ESG ratings into their individual dimensions, the level of agreement varies further. Environmental scores show the highest consistency, with an average correlation of about 0.53, followed by social scores at around 0.42. Governance scores exhibit the lowest level of agreement, with correlations averaging only 0.30.19Berg, F., Kölbel, J. F. & Rigobon, R. Aggregate confusion: The divergence of ESG ratings. Rev. Finance 26, 1315–1344 (2022).

These differences can be traced back to three main sources identified by Berg et al. (2022): divergences in the scope of what is measured (which indicators are included), in the measurement of those indicators (how they are quantified), and in the weighting schemes used to aggregate them into overall scores.19Berg, F., Kölbel, J. F. & Rigobon, R. Aggregate confusion: The divergence of ESG ratings. Rev. Finance 26, 1315–1344 (2022). This can be seen as a barrier of ESG ratings and will be discussed more in detail in 3.5.2.

Earlier evidence by Chatterji et al. (2016) points in the same direction. Comparing KLD, DJSI, Calvert, FTSE4Good, Asset4 and Innovest corporate social responsibility ratings, the authors find correlations of roughly 0.3 to 0.6 across providers.55Chatterji, A. K., Durand, R., Levine, D. I. & Touboul, S. Do ratings of firms converge? Implications for managers, investors and strategy researchers. Strateg. Manag. J. 37, 1597–1614 (2016).

Table 2: Correlation between ESG ratings after Berg et al. (2022), excluding KLD

2.3.3 ESG ratings vs. credit ratings

The purely financial counterpart of ESG ratings are the classic credit ratings. Although the two are often compared, they differ fundamentally in their objectives and underlying concepts. Credit ratings are designed to assess a clearly defined outcome, namely the probability of default and therefore focus strictly on financial risk. ESG ratings, by contrast, do not measure a single, universally agreed-upon construct.14Stewart, R. Towards a better understanding of ESG ratings. J. Sustain. Finance Invest. 15, 624–643 (2025).,19Berg, F., Kölbel, J. F. & Rigobon, R. Aggregate confusion: The divergence of ESG ratings. Rev. Finance 26, 1315–1344 (2022).,35Christensen, D. M., Serafeim, G. & Sikochi, A. (Siko). Why is Corporate Virtue in the Eye of the Beholder? The Case of ESG Ratings. SSRN Scholarly Paper at https://papers.ssrn.com/abstract=3793804 (2021). Instead, and as shown above, ESG ratings capture a broader and considerably more heterogeneous set of dimensions.

A further key difference lies in the level of standardization. Credit rating methodologies are relatively harmonised and lead to highly comparable outcomes across agencies.14Stewart, R. Towards a better understanding of ESG ratings. J. Sustain. Finance Invest. 15, 624–643 (2025). ESG ratings, in contrast, are based on diverse methodological choices regarding data sources, scope, materiality and aggregation. As a result, ESG ratings should not be interpreted as directly comparable measures in the same way as credit ratings.

Finally, ESG ratings are more strongly shaped by subjective and normative elements. Decisions about which ESG issues to include, how materiality is defined, and how individual indicators are weighted all involve value-laden choices that vary considerably across providers.35Christensen, D. M., Serafeim, G. & Sikochi, A. (Siko). Why is Corporate Virtue in the Eye of the Beholder? The Case of ESG Ratings. SSRN Scholarly Paper at https://papers.ssrn.com/abstract=3793804 (2021). Credit ratings, while not entirely free from judgment, operate within a more narrowly defined and widely accepted analytical framework.14Stewart, R. Towards a better understanding of ESG ratings. J. Sustain. Finance Invest. 15, 624–643 (2025).

The literature quantifies the correlation among selected ESG ratings. While Billio et al. (2021) and Berg et al. (2022) report correlations of approximately 0.54 and 0.58, respectively, credit ratings show a near-perfect correlation of around 0.99.15Clement, A., Robinot, E. & Trespeuch, L. (PDF) The use of ESG scores in academic literature: a systematic literature review. ResearchGate https://doi.org/10.1108/JEC-10-2022-0147 (2023) doi:10.1108/JEC-10-2022-0147.,19Berg, F., Kölbel, J. F. & Rigobon, R. Aggregate confusion: The divergence of ESG ratings. Rev. Finance 26, 1315–1344 (2022).,22Billio, M., Costola, M., Hristova, I., Latino, C. & Pelizzon, L. Inside the ESG ratings: (Dis)agreement and performance. Corp. Soc. Responsib. Environ. Manag. 28, 1426–1445 (2021).. These figures speak for themselves. The implications for investors, firms and capital markets will be examined in detail in Chapter 2.5.3, Outcomes of ESG ratings.

Before turning to consequences, however, it is worth asking where this divergence originates, not at the aggregate market level, but within the methodological choices of individual providers. The following section examines this question by comparing MSCI and Sustainalytics in depth, two of the most widely studied ESG rating providers.

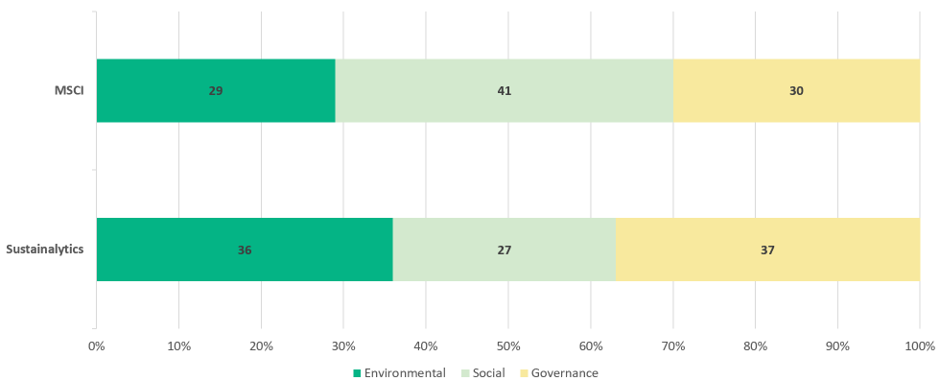

2.4 A methodological comparison between MSCI and sustainalytics

Both rating agencies appear as a central point of comparison in Bissoondoyal-Bheenick et al. (2024), Berg et al. (2022), Billio et al. (2021) and Dimson et al. (2020). Both are explicitly oriented toward institutional investors and apply a financial materiality lens, although MSCI evaluates both risks and opportunities while Sustainalytics focuses exclusively on unmanaged risk. The shared underlying paradigm makes a comparison particularly meaningful.39Dimson, E., Marsh, P. & Staunton, M. Divergent ESG ratings. https://doi.org/10.17863/CAM.55949 (2020) doi:10.17863/CAM.55949.,46MSCI. ESG Ratings Methodology. (2024).,51Sustainalytics. The ESG Risk Ratings: Methodology Abstract Version 3.1. (2024). With 25% market share for MSCI and 6% market share for Sustainalytics.1Elisha, O. & Jebbin, F. The Loss of Biodiversity and Ecosystems: A Threat to the Functioning of our Planet, Economy and Human Society. Int. J. Econ. Environ. Dev. Soc. 1, 30–44 (2020). the two providers have among the largest company coverage in the ESG rating industry, making their methodological choices consequential at scale also beyond academic coverage.45Opimas. Market Share of ESG Data Vendors. Opimas: We begin with an understanding https://www.opimas.com/research/976/detail/ (2024).

Figure 2: Pillar weights for MSCI and sustainalytics across ESG dimensions (in %)

If two providers with the same purpose arrive at materially different conclusions, the source of divergence does not originate in fundamentally different goals, but in how each provider operationalises that goal in practice. The goal of this section is therefore not to replicate what Table 1 covers at a summary level, but to uncover the divergence at the level of individual methodological choices. This understanding provides the analytical foundation for the chapter on barriers of ESG ratings that follows, where the consequences of these architectural differences are examined.

2.4.1 Conceptual foundation: What is being measured?

The most fundamental difference lies not in the stated purpose, but in what each provider actually measures and how the result needs to be interpreted. MSCI ESG ratings are designed to provide an opinion on a company’s management of financially relevant ESG risks and opportunities. Companies are rated on an AAA-to-CCC scale relative to the standards and performance of their industry peers, with the result explicitly intended to reflect a company’s standing within a defined peer group rather than its absolute level of ESG risk.46MSCI. ESG Ratings Methodology. (2024). As a structural consequence, an AAA-rated tobacco producer and a BBB-rated solar company are positioned against different benchmarks rather than against a common standard. The implications of this design choice for comparability are examined in the Outcomes chapter 2.5.3.

Sustainalytics starts from a different angle. Rather than measuring how well a company manages ESG risks relative to peers, it measures how much ESG risk remains unmanaged in absolute terms. In their methodological abstract, Sustainalytics describes the ESG Risk Rating as assessing “the magnitude of a company’s unmanaged ESG risks (p.2)”, expressed on an open-ended numerical scale on which a score close to zero indicates negligible unmanaged risk.51Sustainalytics. The ESG Risk Ratings: Methodology Abstract Version 3.1. (2024). For 95% of companies, the score remains below 50. Sustainalytics refers to this as a “single-currency-of-risk” approach, designed to allow direct comparability of companies across industries on the same scale, something MSCI’s peer-relative framework does not permit by design.46MSCI. ESG Ratings Methodology. (2024).,51Sustainalytics. The ESG Risk Ratings: Methodology Abstract Version 3.1. (2024).

2.4.2 The exposure-management framework: Shared architecture, different logic

Despite their different objectives, both providers share a structural approach: they breakdown the ESG assessment into an exposure dimension and a management dimension. However, the logic of this decomposition and the role each dimension plays in the final score differ substantially.46MSCI. ESG Ratings Methodology. (2024).,51Sustainalytics. The ESG Risk Ratings: Methodology Abstract Version 3.1. (2024).