Authors: Anna Boch

Edited by: –

Last updated: January 4, 2026

Executive summary

Multinational companies (MNCs) play a pivotal role in shaping global sustainability. They combine vast economic power with significant environmental and social impacts, making them both contributors to global challenges and potential catalysts for change. Climate change, biodiversity loss, and social inequality are systemic risks that transcend borders, requiring coordinated responses. MNCs influence these dynamics through their global reach, technological capabilities, and financial resources.

Corporate sustainability (CS) in MNCs involves integrating environmental, social, and economic objectives into core strategies and operations. Unlike corporate social responsibility (CSR), which often focuses on ethical obligations and localized initiatives, CS emphasizes strategic alignment and long-term value creation across global networks. This distinction is critical for MNCs operating in diverse institutional contexts, where balancing global integration with local responsiveness remains a persistent challenge.

Research identifies internal and external drivers of CS. Internal drivers include organizational structure, strategic orientation, leadership, and corporate culture. Structures such as regional divisions, matrix configurations, and network-based models shape how sustainability goals are disseminated and adapted. Leadership styles—particularly transformational and servant leadership—along with governance mechanisms and cultural alignment, strongly influence sustainability outcomes. External drivers encompass institutional pressures, stakeholder expectations, and reputational risks. Regulatory frameworks, global standards like the UN Sustainable Development Goals (SDGs), and industry norms compel MNCs to adopt sustainability practices, while stakeholder engagement and reputational considerations further reinforce these commitments.

The outcomes of CS in MNCs span economic, environmental, and social dimensions. Evidence suggests that sustainability-oriented firms achieve superior financial performance, enhanced innovation, and improved risk management. Environmental outcomes include reductions in emissions and resource use, while social outcomes involve contributions to poverty alleviation, education, and health initiatives. However, gaps persist, particularly in addressing issues such as gender equality and sustainable consumption.

Despite progress, challenges remain. Research on CS in MNCs is fragmented, often focusing on narrow issues or specific contexts. Implementation gaps between high-level commitments and operational practices persist, underscoring the need for robust governance and integrative frameworks. Future research should explore cross-sectoral comparisons, longitudinal analyses, and the role of digital technologies in advancing sustainability.

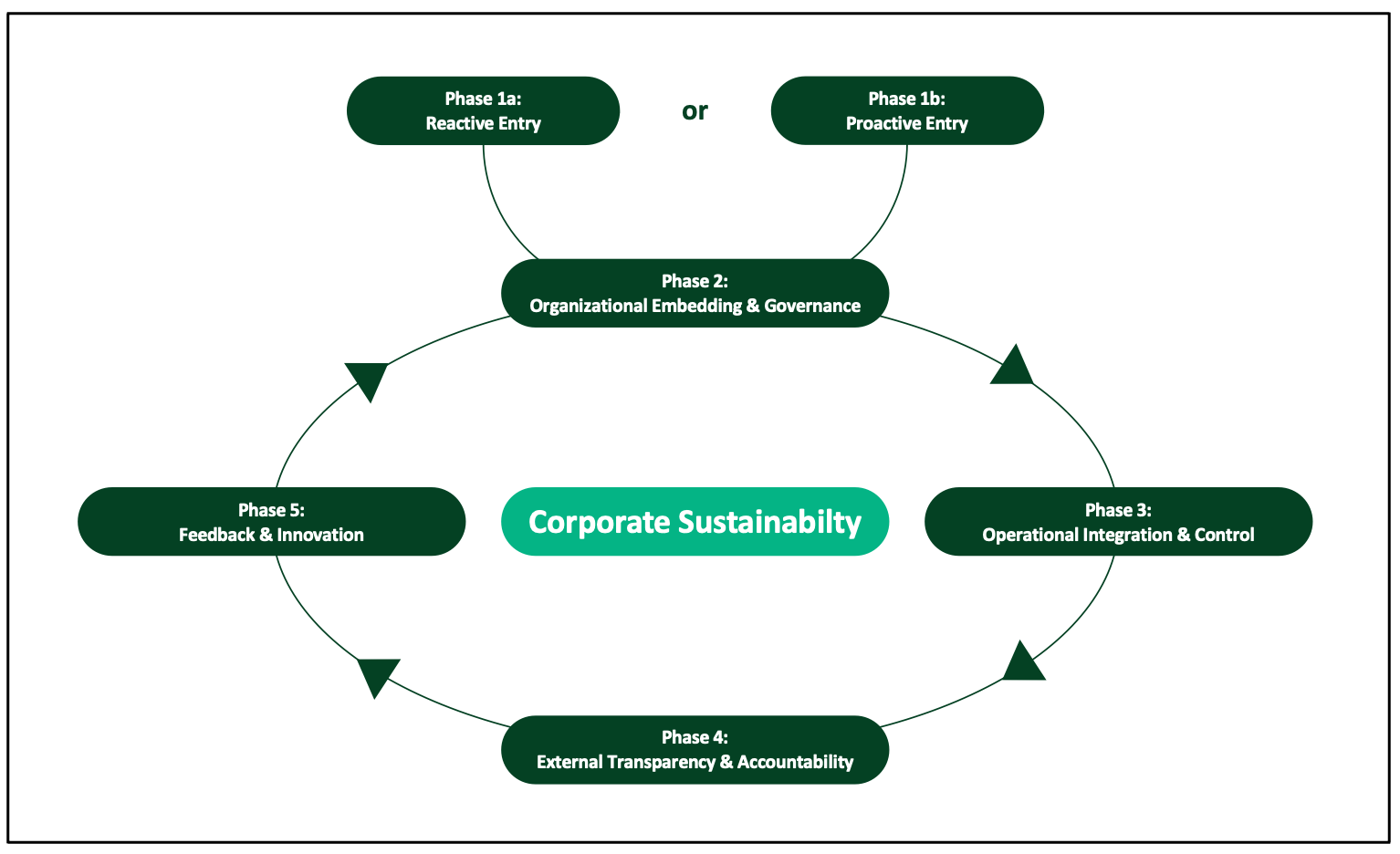

Practically, embedding sustainability in MNCs requires a process-oriented approach. This includes phases of entry and stabilization, organizational embedding and governance, operational integration, external transparency, and feedback-driven innovation. Tools such as management systems, performance metrics, and stakeholder engagement mechanisms support this integration. Ultimately, effective CS implementation in MNCs is iterative, requiring continuous adaptation to evolving institutional, technological, and societal conditions.

1 Introduction

Multinational companies stand at the crossroads of globalization and sustainability, embodying both the forces that drive global environmental and social crises and the capabilities needed to address them.1Christmann, P. Multinational Companies and the Natural Environment: Determinants of Global Environmental Policy Standardization. The Academy of Management Journal 47, 747-760 (2004). https://doi.org/10.5465/20159616,2Rasche, A., Morsing, M., Moon, J. & Kourula, A. Corporate Sustainability: Managing Responsible Business in a Globalised World. 2. edn, (Cambridge University Press, 2023). This position becomes particularly evident in the twenty-first century: climate change, loss of biodiversity, resource scarcity and increasing social inequality constitute systemic risks that transcend national borders, confront the global community on a daily basis and require coordinated responses at the global level.3Burritt, R. L., Christ, K. L., Rammal, H. G. & Schaltegger, S. Multinational Enterprise Strategies for Addressing Sustainability: the Need for Consolidation. Journal of Business Ethics 164, 389-410 (2020). https://doi.org/10.1007/s10551-018-4066-0,4Ocelík, V., Kolk, A. & Ciulli, F. Multinational enterprises, Industry 4.0 and sustainability: A multidisciplinary review and research agenda. Journal of Cleaner Production 413 (2023). https://doi.org/10.1016/j.jclepro.2023.137434,5Ghauri, P., Strange, R. & Cooke, F. L. Research on international business: The new realities. International Business Review 30 (2021). https://doi.org/10.1016/j.ibusrev.2021.101794,6Beltrami, M., Orzes, G., Sarkis, J. & Sartor, M. Industry 4.0 and sustainability: Towards conceptualization and theory. Journal of Cleaner Production 312 (2021). https://doi.org/10.1016/j.jclepro.2021.127733

Companies are no longer perceived merely as economic actors but as institutions whose decisions and practices affect environmental resilience.7Zhang, Z. et al. Embodied carbon emissions in the supply chains of multinational enterprises. Nature Climate Change 10, 1096-1101 (2020). https://doi.org/10.1038/s41558-020-0895-9 Among corporate actors, multinational companies (hereafter abbreviated as MNC) occupy a particularly prominent position.8Korten, D. C. When Corporations Rule the World. 2. edn, (Berrett-Koehler, 2001).,9Adib, M., Zhang, X., A.A.Zaid, M. & Sahyouni, A. Management control system for corporate social responsibility implementation – a stakeholder perspective. Corporate Governance 21, 410-432 (2020). https://doi.org/10.1108/cg-06-2020-0247 By virtue of their power, size, resource and geographic reach, MNCs represent both powerful drivers of economic expansion and environmental degradation.10Andersson, L., Shivarajan, S. & Blau, G. Enacting Ecological Sustainability in the MNC: A Test of an Adapted Value-Belief-Norm Framework. Journal of Business Ethics 59, 295-305 (2005). https://doi.org/10.1007/s10551-005-3440-x,11Zaheer, S. The sustainability of MNE sustainability initiatives. Journal of International Business Studies 56, 491-500 (2025). https://doi.org/10.1057/s41267-024-00760-0,12Allen, F., Barbalau, A., Chavez, E. & Zeni, F. Leveraging the capabilities of multinational firms to address climate change: a finance perspective. Journal of International Business Studies 56, 461-480 (2025). https://doi.org/10.1057/s41267-024-00748-w They account for a disproportionate share of international trade, investment strategies and technological advancements, thereby shaping the material and institutional foundations of globalization.13Fourati, A., Zenaidi, A. & Jeriji, M. Like Parent, Like Subsidiary? On the Diffusion of Sustainability Reporting in Multinational Companies. Corporate Social Responsibility and Environmental Management 32, 3210-3226 (2025). https://doi.org/10.1002/csr.3100 In 2021, the combined earnings of the top 100 MNCs exceeded 11 trillion US dollars, a figure greater than the total GDP of Germany, France, Italy and Spain combined.14Pilgrim, G. & Wahlgren, A. Unlocking New Insights into Multinational Enterprise with the Power of Open-Source-Data, <https://oecdstatistics.blog/2023/05/10/unlocking-new-insights-into-multinational-enterprises-with-the-power-of-open-source-data/> (2023). At the same time, their environmental footprint is equally significant, as even their foreign affiliates alone have been estimated to account for almost one-fifth of global CO2 emissions in the period between 2005 and 2016.7Zhang, Z. et al. Embodied carbon emissions in the supply chains of multinational enterprises. Nature Climate Change 10, 1096-1101 (2020). https://doi.org/10.1038/s41558-020-0895-9 This combination of economic weight and environmental impact underlines the role of MNCs in shaping the trajectory of globalization and sustainability.

Building on this significance, MNCs have become a central topic to debates on global sustainability. While they contribute significantly to global environmental degradation and social externalities, they simultaneously possess the technological capabilities and financial capital to mitigate these challenges.10Andersson, L., Shivarajan, S. & Blau, G. Enacting Ecological Sustainability in the MNC: A Test of an Adapted Value-Belief-Norm Framework. Journal of Business Ethics 59, 295-305 (2005). https://doi.org/10.1007/s10551-005-3440-x Their transnational reach enables them to diffuse innovative practices across markets and their role as standards-setters in global supply chains grants them the capacity to influence suppliers, competitors and policymakers alike.15Soundararajan, V., Sahasranamam, S., Khan, Z. & Jain, T. Multinational enterprises and the governance of sustainability practices in emerging market supply chains: An agile governance perspective. Journal of World Business 56 (2021). https://doi.org/10.1016/j.jwb.2020.101149,16Tong, X. et al. Multinational enterprise buyers’ choices for extending corporate social responsibility practices to suppliers in emerging countries: A multi-method study. Journal of Operations Management 63, 25-43 (2018). https://doi.org/10.1016/j.jom.2018.05.003,17D’Souza, C. et al. An empirical examination of sustainability for multinational firms in China: Implications for cleaner production. Journal of Cleaner Production 242 (2020). https://doi.org/10.1016/j.jclepro.2019.118446,18Franco, S. The influence of the external and internal environments of multinational enterprises on the sustainability commitment of their subsidiaries: A cluster analysis. Journal of Cleaner Production 297 (2021). https://doi.org/10.1016/j.jclepro.2021.126654 As such, MNCs are increasingly recognized not only as contributors to problems, but also as potential catalysts of large-scale transformation towards sustainability.19Vigneau, L., Humphreys, M. & Moon, J. How Do Firms Comply with International Sustainability Standards? Processes and Consequences of Adopting the Global Reporting Initiative. Journal of Business Ethics 131, 469-486 (2015). https://doi.org/10.1007/s10551-014-2278-5

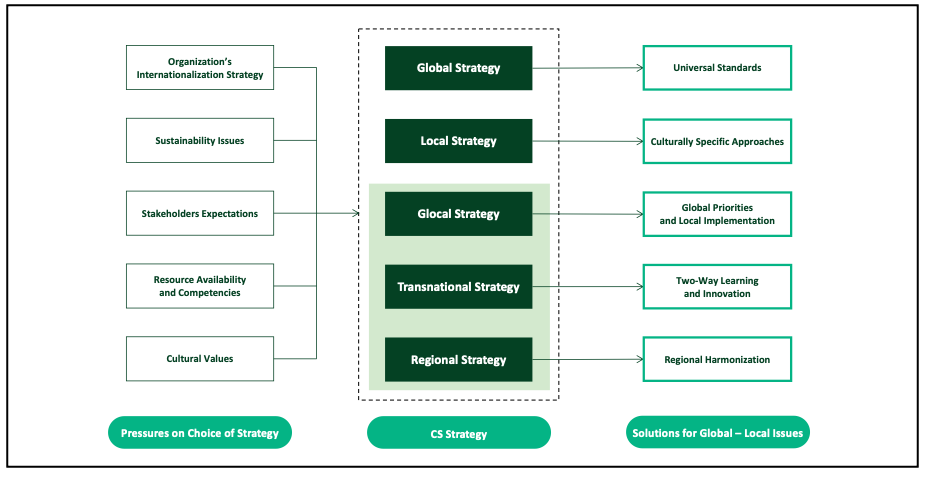

However, the potential of MNCs to act as drivers of sustainability is offset by inherent contradictions. Operating across diverse institutional, cultural and regulatory contexts, MNCs face heterogeneous expectations regarding corporate sustainability (hereafter abbreviated as CS).20Bondy, K. & Starkey, K. The Dilemmas of Internationalization: Corporate Social Responsibility in the Multinational Corporation. British Journal of Management 25, 4-22 (2014). https://doi.org/10.1111/j.1467-8551.2012.00840.x These challenges are further amplified by the structural tensions between global integration and local responsiveness.21Doz, Y. L., Bartlett, C. A. & Prahalad, C. K. Global Competitive Pressures and Host Country Demands Managing Tensions in MNCs. California Management Review 23, 63-74 (1981). https://doi.org/10.2307/41172603 On the one hand, MNCs are expected to define sustainability as a coherent global strategy that aligns with international norms and reflects their corporate identity. On the other hand, subsidiaries are embedded in host-country contexts that require context-specific responses to local regulations, stakeholder priorities and cultural values.3Burritt, R. L., Christ, K. L., Rammal, H. G. & Schaltegger, S. Multinational Enterprise Strategies for Addressing Sustainability: the Need for Consolidation. Journal of Business Ethics 164, 389-410 (2020). https://doi.org/10.1007/s10551-018-4066-0 Balancing these competing imperatives often proves difficult: global strategies risk overlooking local particularities, while locally tailored initiatives can undermine overall coherence.3Burritt, R. L., Christ, K. L., Rammal, H. G. & Schaltegger, S. Multinational Enterprise Strategies for Addressing Sustainability: the Need for Consolidation. Journal of Business Ethics 164, 389-410 (2020). https://doi.org/10.1007/s10551-018-4066-0 This tension raises questions about the strategic effectiveness and legitimacy of CS in multinational settings.

Building on this motivation, the academic and practical relevance of examining CS in MNCs becomes evident. Research on CS in MNCs has developed into a dynamic and multifaceted field over the past decades. Scholars across international business22George, G. & Schillebeeckx, S. J. D. Digital transformation, sustainability, and purpose in the multinational enterprise. Journal of World Business 57 (2022). https://doi.org/10.1016/j.jwb.2022.101326, strategic management3Burritt, R. L., Christ, K. L., Rammal, H. G. & Schaltegger, S. Multinational Enterprise Strategies for Addressing Sustainability: the Need for Consolidation. Journal of Business Ethics 164, 389-410 (2020). https://doi.org/10.1007/s10551-018-4066-0, political science23van der Ven, H. Gatekeeper power: understanding the influence of lead firms over transnational sustainability standards. Review of International Political Economy 25, 624-646 (2018). https://doi.org/10.1080/09692290.2018.1490329 and organizational studies24Akhtar, P., Ullah, S., Amin, S. H., Kabra, G. & Shaw, S. Dynamic capabilities and environmental sustainability for emerging economies’ multinational enterprises. International Studies of Management & Organization 50, 27-42 (2020). https://doi.org/10.1080/00208825.2019.1703376 have provided valuable insights into how sustainability becomes embedded in globally operating firms. This research has advanced the understanding in several important ways. For instance, studies have clarified how MNCs are exposed to heterogeneous institutional environments and how they respond to different regulatory frameworks.3Burritt, R. L., Christ, K. L., Rammal, H. G. & Schaltegger, S. Multinational Enterprise Strategies for Addressing Sustainability: the Need for Consolidation. Journal of Business Ethics 164, 389-410 (2020). https://doi.org/10.1007/s10551-018-4066-0 Other contributions have explored the role of MNCs in promoting sustainability in emerging and developing markets, while further research has illustrated the outcomes of CS initiatives in relation to global frameworks.25Elg, U. & Hånell, S. M. Driving sustainability in emerging markets: The leading role of multinationals. Industrial Marketing Management 114, 211-225 (2023). https://doi.org/10.1016/j.indmarman.2023.08.010,26Ameer, R. & Othman, R. Sustainability Practices and Corporate Financial Performance: A Study Based on the Top Global Corporations. Journal of Business Ethics 108, 61-79 (2012). https://doi.org/10.1007/s10551-011-1063-y,27Ordonez-Ponce, E. & Talbot, D. Multinational enterprises’ sustainability practices and focus on developing countries: Contributions and unexpected results of SDG implementation. Journal of International Development35, 201-232 (2023). https://doi.org/10.1002/jid.3682 This growing amount of literature demonstrates that research has already established a rich understanding of the multiple dimensions of CS in MNCs.

Despite these advantages, the academic debate on CS in MNCs continues to face several challenges. Many studies adopt narrow focus on well-defined problems, which provide valuable depth but leave broader questions underexplored.3Burritt, R. L., Christ, K. L., Rammal, H. G. & Schaltegger, S. Multinational Enterprise Strategies for Addressing Sustainability: the Need for Consolidation. Journal of Business Ethics 164, 389-410 (2020). https://doi.org/10.1007/s10551-018-4066-0 In particular, there is still limited knowledge about how MNCs develop comprehensive sustainability strategies and how responsibilities are negotiated between headquarters and subsidiaries.28Elg, U. & Ghauri, P. N. in Creating a Sustainable Competitive Position: Ethical Challenges for International Firms Vol. 37 (eds Pervez N. Ghauri, Ulf Elg, & Sara Melén Hånell) (Emerald Publishing Limited, 2023). While a considerable number of studies have examined the drivers of CS, much of this research does not focus explicitly on MNCs. Instead, insights are frequently derived from samples that include a mix of corporate actors.29Lozano, R. A Holistic Perspective on Corporate Sustainability Drivers. Corporate Social Responsibility and Environmental Management 22, 32-44 (2015). https://doi.org/10.1002/csr.1325 Although these contributions provide valuable understanding of general sustainability drivers in companies, they do not fully capture the specific complexities faced by MNCs. In addition, much of the existing empirical work is concentrated on specific industries or country contexts, often producing deep but contextualized insights.30Edoho, F. M. Oil transnational corporations: corporate social responsibility and environmental sustainability. Corporate Social Responsibility and Environmental Management 15, 210-222 (2008). https://doi.org/10.1002/csr.143,31Amoah, P. & Eweje, G. Impact mitigation or ecological restoration? Examining the environmental sustainability practices of multinational mining companies. Business Strategy and the Environment 30, 551-565 (2021). https://doi.org/10.1002/bse.2637,32Xiao, S., Roh, T. & Park, Byung I. Entrepreneurial Orientation, Environmental Dynamism, and Disruptive Sustainability in Emerging Markets: Evidence From MNE Subsidiaries in China. Business Strategy and the Environment (2025). https://doi.org/10.1002/bse.70105

Against this background, the thesis makes a dual contribution. On the academic side, it consolidates insights, maps the relationship between internal and external drivers and sustainability outcomes and critically reflects on limitations in the existing body of literature. In doing so, it seeks to overcome disciplinary fragmentation by integrating dispersed findings into a coherent framework and by highlighting both the drivers that shape CS in MNCs and the outcomes that result from such engagement. On the practical side, it provides a structured lens to understand how sustainability can be embedded into global corporate strategies and operations. By focusing explicitly on MNCs, the thesis highlights the unique challenges and opportunities that distinguish them from other corporate actors. Therefore, the following research question can be derived for this thesis:

What is the current state of research on corporate sustainability for multinational companies and how is corporate sustainability implemented in a multinational context?

By addressing this question, the thesis seeks to consolidate existing scholarship, identify key drivers and outcomes and evaluate the limitations of current approaches. In doing so, it contributes to a more comprehensive understanding of how CS is conceptualized and operationalized in the specific setting of MNCs and develops a process-oriented framework for the systematic implementation of CS in MNCs.

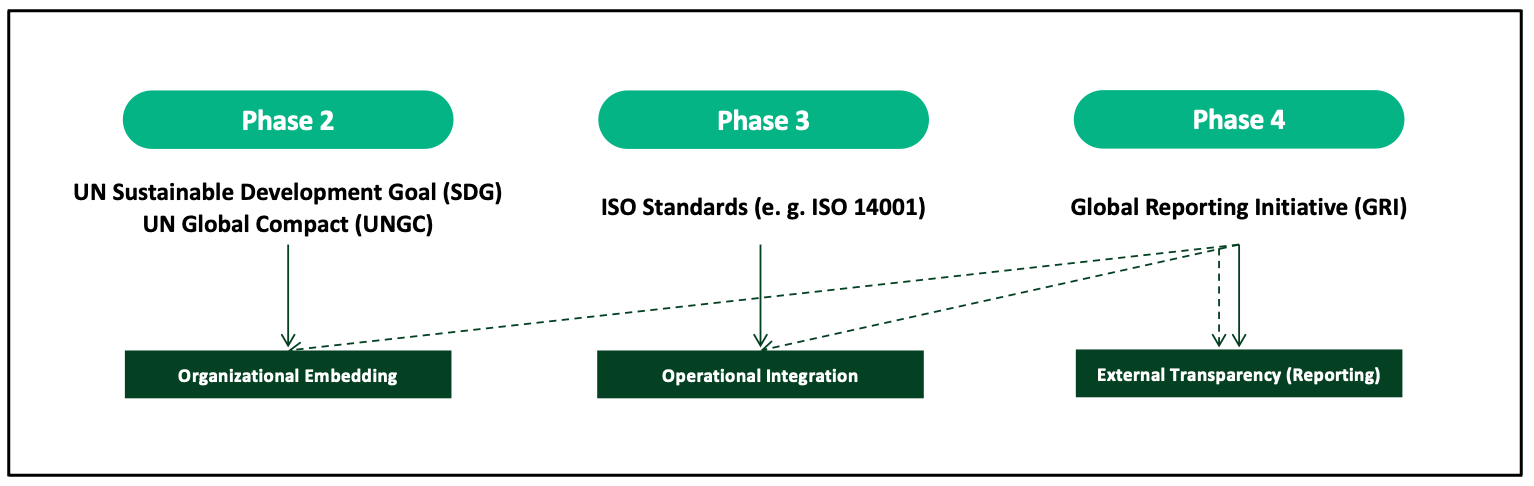

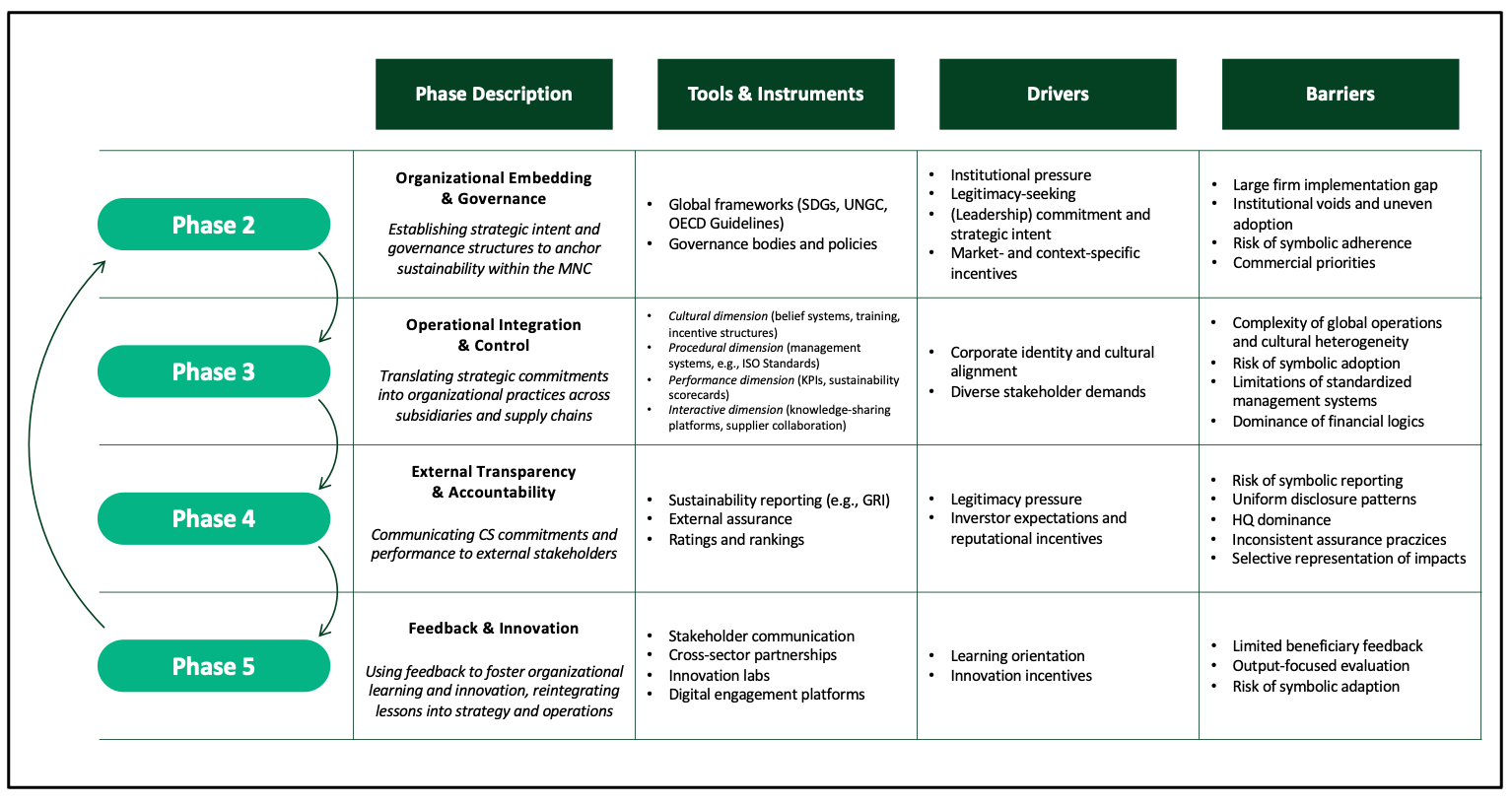

Following the introduction, the second chapter outlines the methodological approach of this thesis, describing the unsystematic integrative review and the qualitative thematic analysis applied to identify and synthesize relevant contributions. The third chapter presents the literature review. It begins by clarifying the key concepts of MNC and CS before tracing the historical background of corporate internationalization and the emergence of sustainability in international business debates. Building on this background, the chapter reviews the main academic contributions on CS in a multinational context. It discusses both internal and external drivers that shape corporate engagement with sustainability, highlights the economic, environmental and social outcomes documented in the literature and reflects on the limitations that continue to characterize this field of research. The fourth chapter turns from literature review to implementation. Drawing on identified recurring patterns, it develops a process-oriented framework for the implementation of CS in MNCs. The framework distinguishes five interrelated phases, from initial entry and stabilization through governance, operational integration and external transparency to feedback and innovation, and illustrates how these phases are connected in an iterative cycle. The chapter also discusses the tools and mechanisms that support implementation in practice, such as international frameworks, management systems, reporting standards and stakeholder engagement instruments. In doing so, the thesis not only consolidates and systematizes existing insights but also develops a framework that advances both academic understanding and managerial practice of CS in MNCs.

2 Literature review

2.1 Key terminology

2.1.1 Multinational companies

The concept of the multinational company (also referred to as multinational enterprise (MNE)) has been examined from a wide range of disciplinary perspectives, each offering distinct definitional and analytical emphases. Rather than converging around a single definition, scholars have conceptualized MNCs according to their disciplinary paradigms and research objectives.33Ghoshal, S. & Westney, D. E. in Organization Theory and the Multinational Corporation (eds Sumantra Ghoshal & D. Eleanor Westney) 1-23 (Palgrave Macmillan UK, 1993). From an organizational theory standpoint, MNCs are seen as structurally complex systems that operate across multiple institutional environments. Ghoshal and Westney (1993) define the MNC as an organizational form that comprises entities in two or more countries, regardless of legal form or field of activity, which operates under a system of decision-making permitting coherent policies and a common strategy through one or more decision-making centers. These entities are so linked, by ownership or otherwise, that one or more of them may be able to exercise a significant influence over the activities of the others and to share knowledge, resources and responsibilities.33Ghoshal, S. & Westney, D. E. in Organization Theory and the Multinational Corporation (eds Sumantra Ghoshal & D. Eleanor Westney) 1-23 (Palgrave Macmillan UK, 1993).

In contrast to the organizational perspective, the international economics literature offers a more operational definition centered on foreign direct investment (FDI). Dunning and Lundan (2008) define MNC as “an enterprise that engages in foreign direct investment and owns or, in some way, controls value-added activities in more than one country” (p. 3).34Dunning, J. H. & Lundan, S. M. Multinational Enterprises and the Global Economy. Second Edition edn, (Edward Elgar Publishing, 2008). This understanding is frequently used by institutions such as the Organization for Economic Co-Operation and Development (OECD) and the United Nations Conference on Trade and Development (UNCTAD) and forms the basis for empirical assessments of multinationalism. Within this perspective, the degree of multinationalism is typically assessed using quantitative indicators, such as the number of foreign affiliates, the geographic scope of operations or the share of revenues, assets or employment generated abroad.34Dunning, J. H. & Lundan, S. M. Multinational Enterprises and the Global Economy. Second Edition edn, (Edward Elgar Publishing, 2008).

In political science, the MNC is often conceptualized as a powerful non-state actor with transnational influence. Vernon (1971) describes MNCs as global actors whose economic and strategic activities increasingly escape the regulatory grasp of national governments.35Vernon, R. Sovereignty at bay: The multinational spread of U. S. enterprises. The International Executive 13, 1-3 (1971). https://doi.org/10.1002/tie.5060130401 He observes, that “the network of any multinational enterprise cannot escape serving as a conduit through which sovereign states exert an influence on the economies of other sovereign states” (pp.517 f.).36Vernon, R. Sovereignty at Bay Ten Years after. International Organization 35, 517-529 (1981). This results in a fundamental asymmetry: while national governments are territorially bound, MNCs can shift operations across borders, thereby altering power dynamics and limiting the policy autonomy of host countries.36Vernon, R. Sovereignty at Bay Ten Years after. International Organization 35, 517-529 (1981).

From a strategic management perspective, MNCs are defined as firms that configure and coordinate its globally dispersed units in accordance with strategic objectives, particularly the need to balance global integration and local responsiveness. Stopford and Wells (1972) developed an early typology that linked structural design to two key variables: the degree of internationalization and product diversification. Based on these, they identified international, multidomestic and globalstructures as archetypal organizational forms.37Stopford, J. M. & Wells, L. T. Managing the Multinational Enterprise; Organization of the Firm and Ownership of the Subsidiaries. (Basic Books, 1972). Building on this foundation, Bartlett and Ghoshal (1989) extended the analysis by introducing a behavioral and strategic dimension. In their typology, comprising international, multidomestic, global and transnational models, MNCs are understood as organizational systems that seek to reconcile the competing demands of global integration and local responsiveness.38Bartlett, C. A. & Ghoshal, S. Managing across borders : the transnational solution. (Harvard Business School Press, 1989).

Despite the conceptual diversity outlined above, a unified definition of MNC remains elusive in the academic literature. Recent literature increasingly emphasizes the functional characteristics and organizational complexity of MNCs rather than attempting to establish a universally accepted definition. MNCs are described as firms operating across multiple institutional contexts, managing globally dispersed structures and responding to heterogeneous stakeholder expectations. This reflects a shift towards viewing the multinational form as an adaptive organizational response to global pressures such as digitization, climate change or geopolitical uncertainty.22George, G. & Schillebeeckx, S. J. D. Digital transformation, sustainability, and purpose in the multinational enterprise. Journal of World Business 57 (2022). https://doi.org/10.1016/j.jwb.2022.101326,39Buckley, P. J. & Casson, M. The Internalization Theory of the Multinational Enterprise: Past, Present and Future. British Journal of Management 31, 239-252 (2020). https://doi.org/10.1111/1467-8551.12344,40Petricevic, O. & Teece, D. J. The structural reshaping of globalization: Implications for strategic sectors, profiting from innovation, and the multinational enterprise. Journal of International Business Studies 50, 1487-1512 (2019). https://doi.org/10.1057/s41267-019-00269-x

In addition to the varying disciplinary perspectives, it is essential to distinguish analytically between the MNC as a corporate whole and its individual foreign subsidiaries. The term multinational company refers to the overarching organizational entity that coordinates value-creating activities across multiple national environments through integrated strategic and structural systems. In contrast, a MNC subsidiary denotes a legally and operationally distinct unit situated outside the firm’s home country, under the formal control or significant influence of the parent organization.41Meyer, K. E., Li, C. & Schotter, A. P. J. Managing the MNE subsidiary: Advancing a multi-level and dynamic research agenda. Journal of International Business Studies 51, 538-576 (2020). https://doi.org/10.1057/s41267-020-00318-w According to Birkinshaw, Hood and Jonsson (1998) a MNC subsidiary is defined as “any operational unit controlled by the MNE and situated outside the home country. In some cases, there will be a single subsidiary in the host country; in other cases, there will be several” (p. 224).42Birkinshaw, J., Hood, N. & Jonsson, S. Building Firm-Specific Advantages in Multinational Corporations: The Role of Subsidiary Initiative. Strategic Management Journal 19, 221-241 (1998). MNC subsidiaries vary significantly in terms of strategic relevance, autonomy and functional responsibilities. While some operate under centralized control, others possess considerable decision-making authority and contribute actively to the firm’s global value creation.41Meyer, K. E., Li, C. & Schotter, A. P. J. Managing the MNE subsidiary: Advancing a multi-level and dynamic research agenda. Journal of International Business Studies 51, 538-576 (2020). https://doi.org/10.1057/s41267-020-00318-w The heterogeneity of subsidiary roles and mandates underscores the need for conceptual precision, as much of the literature addresses either the MNC as an integrated actor or its subsidiaries as semi-autonomous units embedded in distinct institutional environments.

While the concept of the multinational company remains analytically contested and multifaceted, this thesis adopts a functional understanding of MNCs as organizational systems operating across multiple national contexts and coordinating globally dispersed activities. Depending on the analytical focus of the respective literature, both the overarching corporate entity and its foreign subsidiaries are considered.

2.1.2 Corporate sustainability

While the notion of corporate sustainability is widely discussed in the academic literature, there is no universally accepted definition. The academic debate is characterized by a rich variety of conceptualizations that reflect disciplinary backgrounds and empirical contexts. This diversity, although sometimes perceived as a lack of conceptual clarity, also demonstrates the multidimensionality and adaptability of the CS concept.43Bansal, P. Evolving Sustainably: A Longitudinal Study of Corporate Sustainable Development. Strategic Management Journal 26, 197-218 (2005).,44Dyllick, T. & Hockerts, K. Beyond the business case for corporate sustainability. Business Strategy and the Environment 11, 130-141 (2002). https://doi.org/10.1002/bse.323

CS can broadly be understood as the integration of environmental, social and economic objectives into corporate strategy and operations in a way that enables the firm to meet the needs of its current stakeholders without compromising its capacity to serve future ones. This transfer of the sustainable development (SD) idea to the corporate level implies that firms must not only ensure long-term profitability but also preserve and enhance their environmental and social capital bases.44Dyllick, T. & Hockerts, K. Beyond the business case for corporate sustainability. Business Strategy and the Environment 11, 130-141 (2002). https://doi.org/10.1002/bse.323 This understanding of CS is derived from the definition of SD introduced in the Brundtland Report, which emphasizes the need to balance present and future needs within a broader socio-environmental framework.45Brundtland, G. H. Our Common Future: Report of the World Commission on Environment and Development. (1987).,46Sharma, S. & Henriques, I. Stakeholder influences on sustainability practices in the Canadian forest products industry. Strategic Management Journal 26, 159-180 (2005). https://doi.org/10.1002/smj.439 However, the variety of existing definitions also reflects that CS remains an evolving and relatively young concept within academic and managerial discourse.47Ashrafi, M., Magnan, G. M., Adams, M. & Walker, T. R. Understanding the Conceptual Evolutionary Path and Theoretical Underpinnings of Corporate Social Responsibility and Corporate Sustainability. Sustainability 12(2020). https://doi.org/10.3390/su12030760,48Montiel, I. & Delgado-Ceballos, J. Defining and Measuring Corporate Sustainability:Are We There Yet? Organization & Environment 27, 113-139 (2014). https://doi.org/10.1177/1086026614526413

Given the conceptual proximity between CS and corporate social responsibility (CSR) and the frequent overlap of their usage, especially within research on MNCs, it becomes necessary to clarify how these concepts differ and how they relate to each other in the academic discourse.49Derqui, B. Towards sustainable development: Evolution of corporate sustainability in multinational firms. Corporate Social Responsibility and Environmental Management 27, 2712-2723 (2020). https://doi.org/10.1002/csr.1995 Although CS and CSR are frequently used interchangeably in academic and managerial contexts, a growing body of literature emphasizes that the two concepts are not conceptually identical.3Burritt, R. L., Christ, K. L., Rammal, H. G. & Schaltegger, S. Multinational Enterprise Strategies for Addressing Sustainability: the Need for Consolidation. Journal of Business Ethics 164, 389-410 (2020). https://doi.org/10.1007/s10551-018-4066-0,50Bergman, M. M., Bergman, Z. & Berger, L. An Empirical Exploration, Typology, and Definition of Corporate Sustainability. Sustainability 9 (2017). https://doi.org/10.3390/su9050753,51van Marrewijk, M. Concepts and Definitions of CSR and Corporate Sustainability: Between Agency and Communion. Journal of Business Ethics 44, 95-105 (2003). https://doi.org/10.1023/A:1023331212247,52Bansal, P. & Song, H.-C. Similar But Not the Same: Differentiating Corporate Sustainability from Corporate Responsibility. Academy of Management Annals 11, 105-149 (2017). https://doi.org/10.5465/annals.2015.0095 CSR traditionally stems from the field of business ethics and is primarily normative in nature, focusing on the moral obligations of firms toward society, such as human rights, philanthropy or labor conditions.50Bergman, M. M., Bergman, Z. & Berger, L. An Empirical Exploration, Typology, and Definition of Corporate Sustainability. Sustainability 9 (2017). https://doi.org/10.3390/su9050753,53Barauskaite, G. & Streimikiene, D. Corporate social responsibility and financial performance of companies: The puzzle of concepts, definitions and assessment methods. Corporate Social Responsibility and Environmental Management 28, 278-287 (2021). https://doi.org/10.1002/csr.2048 In contrast, CS emerges from the SD discourse and emphasizes the strategic integration of environmental, social and economic considerations into core business operations, with the goal of ensuring long-term value creation and systemic resilience.50Bergman, M. M., Bergman, Z. & Berger, L. An Empirical Exploration, Typology, and Definition of Corporate Sustainability. Sustainability 9 (2017). https://doi.org/10.3390/su9050753,54Meuer, J., Koelbel, J. & Hoffmann, V. H. On the Nature of Corporate Sustainability. Organization & Environment33, 319-341 (2020). https://doi.org/10.1177/1086026619850180 Whereas CSR is often interpreted as a peripheral or externally driven activity aimed at meeting stakeholder expectations, CS tends to be framed as an intrinsic and organization-wide management paradigm that aligns sustainability objectives with core business functions and long-term competitiveness.48Montiel, I. & Delgado-Ceballos, J. Defining and Measuring Corporate Sustainability:Are We There Yet? Organization & Environment 27, 113-139 (2014). https://doi.org/10.1177/1086026614526413,54Meuer, J., Koelbel, J. & Hoffmann, V. H. On the Nature of Corporate Sustainability. Organization & Environment33, 319-341 (2020). https://doi.org/10.1177/1086026619850180 As such, CSR is typically grounded in ethical reasoning, while CS is characterized by its orientation toward strategic integration and operational implementation.50Bergman, M. M., Bergman, Z. & Berger, L. An Empirical Exploration, Typology, and Definition of Corporate Sustainability. Sustainability 9 (2017). https://doi.org/10.3390/su9050753,51van Marrewijk, M. Concepts and Definitions of CSR and Corporate Sustainability: Between Agency and Communion. Journal of Business Ethics 44, 95-105 (2003). https://doi.org/10.1023/A:1023331212247 Within this discourse, CSR is often conceptualized as a component or precursor of CS, representing an initial stage of corporate engagement with sustainability concerns that may, over time, evolve into more integrated and strategic sustainability approaches.50Bergman, M. M., Bergman, Z. & Berger, L. An Empirical Exploration, Typology, and Definition of Corporate Sustainability. Sustainability 9 (2017). https://doi.org/10.3390/su9050753,51van Marrewijk, M. Concepts and Definitions of CSR and Corporate Sustainability: Between Agency and Communion. Journal of Business Ethics 44, 95-105 (2003). https://doi.org/10.1023/A:1023331212247

The conceptual relevance of distinguishing CS from CSR becomes particularly pronounced when applied to MNCs.49Derqui, B. Towards sustainable development: Evolution of corporate sustainability in multinational firms. Corporate Social Responsibility and Environmental Management 27, 2712-2723 (2020). https://doi.org/10.1002/csr.1995 Due to their operations across diverse regulatory, cultural and institutional settings, MNCs must simultaneously address heterogeneous stakeholder expectations while maintaining organizational coherence. In such contexts, CSR is often employed as a localized and adaptive mechanism to respond to external pressures and secure legitimacy in fragmented environments.55Zhou, X., Ying, S. X., You, J. & Wu, H. Like parent, like child: MNCs’ CSR and their foreign subsidiaries’ environmental footprint. Journal of Business Research 172 (2024). https://doi.org/10.1016/j.jbusres.2023.114413,56Bondy, K., Moon, J. & Matten, D. An Institution of Corporate Social Responsibility (CSR) in Multi-National Corporations (MNCs): Form and Implications. Journal of Business Ethics 111, 281-299 (2012). https://doi.org/10.1007/s10551-012-1208-7,57Aguilera-Caracuel, J., Guerrero-Villegas, J. & García-Sánchez, E. Reputation of multinational companies. European Journal of Management and Business Economics 26, 329-346 (2017). https://doi.org/10.1108/EJMBE-10-2017-019 In contrast, CS represents a more unified and strategically integrated framework that aspires to embed sustainability principles across global operations and decision-making structures.51van Marrewijk, M. Concepts and Definitions of CSR and Corporate Sustainability: Between Agency and Communion. Journal of Business Ethics 44, 95-105 (2003). https://doi.org/10.1023/A:1023331212247 Despite the frequent semantic convergence of CSR and CS in managerial practice, scholars emphasize that the two concepts differ in their theoretical orientation and level of organizational embeddedness, particularly in multinational settings.49Derqui, B. Towards sustainable development: Evolution of corporate sustainability in multinational firms. Corporate Social Responsibility and Environmental Management 27, 2712-2723 (2020). https://doi.org/10.1002/csr.1995,58Feng, P. & Ngai, C. S.-b. Doing More on the Corporate Sustainability Front: A Longitudinal Analysis of CSR Reporting of Global Fashion Companies. Sustainability 12 (2020). https://doi.org/10.3390/su12062477 While CSR continues to dominate many MNC’s sustainability discourses and reporting practices, there is growing recognition of more strategically oriented sustainability conceptions in multinational context.59Yin, J. & Jamali, D. Strategic Corporate Social Responsibility of Multinational Companies Subsidiaries in Emerging Markets: Evidence from China. Long Range Planning 49, 541-558 (2016). https://doi.org/10.1016/j.lrp.2015.12.024

For this thesis, the term corporate sustainability will be used as the overarching concept that captures the strategic, long-term integration of environmental, social and economic dimensions into corporate decision-making. Where academic sources refer to corporate social responsibility in a manner consistent with this understanding, particularly in the context of MNCs, the respective insights will be considered part of the broader framework of CS, unless otherwise specified.

2.2 Historical background

2.2.1 Evolution of corporate internationalization

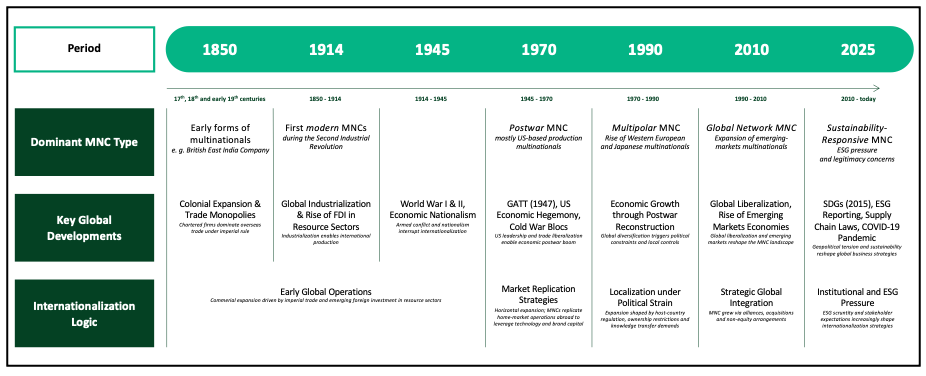

The history of multinational companies is characterized by continuous adaption to technological, institutional and geopolitical shifts. Although international commercial activity predates industrial capitalism, the multinational organizational form began to emerge as early as the late 17th and 18th centuries, with the rise of trading corporations such as the British East India Company. These early entities, however, were primarily focused on commerce rather than on the production of goods and services outside the home economy. The decisive shift toward what would become the modern multinational occurred when firms began to engage in FDI and to manage their operations abroad through structured organizational forms such as subsidiaries and affiliates.60Wilkins, M. in Oxford Handbook of International Business (eds Alan M. Rugman & Thomas L. Brewer) (Oxford University Press, 2001).,61Morgan, G. in The Oxford Handbook of Work and Organization (eds Stephen Ackroyd, Rosemary Batt, Paul Thompson, & Pamela S. Tolbert) (Oxford University Press, 2006).

This transition gained momentum during the 19th century, as global economic integration deepened and FDI increasingly complemented traditional forms of portfolio investment. Particularly in resource-based sectors such as oil, rubber, coffee and minerals, firms from Europe and the United States began establishing foreign operations.61Morgan, G. in The Oxford Handbook of Work and Organization (eds Stephen Ackroyd, Rosemary Batt, Paul Thompson, & Pamela S. Tolbert) (Oxford University Press, 2006). The modern MNC, however, took its institutional and strategic shape during the Second Industrial Revolution.62Guillen, M. & García-Canal, E. The American Model of the Multinational Firm and the “New” Multinationals From Emerging Economies. Academy of Management Perspectives 23, 23-35 (2009). https://doi.org/10.5465/AMP.2009.39985538 From the late 19th to the early 20th century, firms from Britain, North America and continental Europe began expanding internationally not only through trade but also by intangible assets such as managerial expertise, technology and brands.63Wilkins, M. in Transnational Corporations and the Global Economy (eds Richard Kozul-Wright & Robert Rowthorn) 95-133 (Palgrave Macmillan UK, 1998).,64Krugman, P. Multinational enterprise: The old and the new in history and theory. North American Review of Economics and Finance 1, 267-280 (1990). https://doi.org/10.1016/1042-752X(90)90020-G

The Second World War constituted a historical rupture: the dismantling of cartels and the emergence of U.S. economic hegemony allowed American MNCs to dominate global markets during the early Cold War era.65Jones, G. Nationality and multinationals in historical perspective. (Division of Research, Harvard Business School Boston, 2006).,66Dymsza, W. A. Trends in Multinational Business and Global Environments: A Perspective. Journal of International Business Studies 15, 25-46 (1984). https://doi.org/10.1057/palgrave.jibs.8490493 Enabled by institutional frameworks such as the General Agreement on Tariffs and Trade (GATT, 1947), which laid the groundwork for liberalized global trade, U.S. firms engaged in FDI on an unprecedented scale. The relevance of GATT for MNC growth has been empirically confirmed by studies showing positive capital market reactions to its implementation.67Ghani, W. I. & Haverty, J. L. Market reaction of multinational corporations to the passage of the General Agreement on Tariffs and Trade (GATT). Journal of International Accounting, Auditing and Taxation 7, 95-112 (1998). https://doi.org/10.1016/S1061-9518(98)90008-8 Between 1950 and 1970, the volume of American FDI abroad grew from $3.8 to over $32 billion, marking the rise of what Fayerweather termed the postwar multinational.68Fayerweather, J. The Internationalization of Business. The Annals of the American Academy of Political and Social Science 403, 1-11 (1972). During this period, the United States likely accounted for as much as 85 percent of all new FDI flows globally, underscoring the country’s dominant position in shaping the organizational and strategic foundations of modern MNCs.65Jones, G. Nationality and multinationals in historical perspective. (Division of Research, Harvard Business School Boston, 2006). These postwar MNCs were characterized by centralized organizational structures, full ownership of foreign subsidiaries and the transfer of proprietary knowledge across borders.62Guillen, M. & García-Canal, E. The American Model of the Multinational Firm and the “New” Multinationals From Emerging Economies. Academy of Management Perspectives 23, 23-35 (2009). https://doi.org/10.5465/AMP.2009.39985538,68Fayerweather, J. The Internationalization of Business. The Annals of the American Academy of Political and Social Science 403, 1-11 (1972). Their expansion was predominantly horizontal, replicating home-market activities abroad and driven by the need to exploit firm-specific advantages (FSA) such as technology and managerial know-how.64Krugman, P. Multinational enterprise: The old and the new in history and theory. North American Review of Economics and Finance 1, 267-280 (1990). https://doi.org/10.1016/1042-752X(90)90020-G,69Behrman, J. N. & Fischer, W. A. Overseas R&D activities of transnational companies. The International Executive22, 15-17 (1980). https://doi.org/10.1002/tie.5060220309,70Ronstadt, R. C. International R&D: The Establishment and Evolution of Research and Development Abroad by Seven U.S. Multinationals. Journal of International Business Studies 9, 7-24 (1978). https://doi.org/10.1057/palgrave.jibs.8490647

Throughout the 1960s and 1970s, U.S. MNCs such as General Motors and IBM expanded globally, establishing vertically integrated industrial systems that linked R&D, production and distribution.65Jones, G. Nationality and multinationals in historical perspective. (Division of Research, Harvard Business School Boston, 2006).,68Fayerweather, J. The Internationalization of Business. The Annals of the American Academy of Political and Social Science 403, 1-11 (1972). However, the growing influence of U.S.-based MNCs provoked political resistance, particularly in developing countries. In many cases, they were perceived as vehicles of economic domination or as enclave actors with limited local spillovers.65Jones, G. Nationality and multinationals in historical perspective. (Division of Research, Harvard Business School Boston, 2006).,71Narula, R. Multinational firms and the extractive sectors in the 21st century: Can they drive development? Journal of World Business 53, 85-91 (2018). https://doi.org/10.1016/j.jwb.2017.09.004 Governments responded by introducing restrictions on ownership, enforcing localization requirements and demanding knowledge and technology transfer to promote domestic capacity-building.64Krugman, P. Multinational enterprise: The old and the new in history and theory. North American Review of Economics and Finance 1, 267-280 (1990). https://doi.org/10.1016/1042-752X(90)90020-G,71Narula, R. Multinational firms and the extractive sectors in the 21st century: Can they drive development? Journal of World Business 53, 85-91 (2018). https://doi.org/10.1016/j.jwb.2017.09.004 From the 1970s onward, the dominance of U.S.-based MNCs gradually gave way to a more multipolar landscape. Firms from Western Europe and Japan, benefiting from postwar reconstruction and export-oriented growth models, began to internationalize aggressively and establish a strong global presence.65Jones, G. Nationality and multinationals in historical perspective. (Division of Research, Harvard Business School Boston, 2006).,66Dymsza, W. A. Trends in Multinational Business and Global Environments: A Perspective. Journal of International Business Studies 15, 25-46 (1984). https://doi.org/10.1057/palgrave.jibs.8490493,68Fayerweather, J. The Internationalization of Business. The Annals of the American Academy of Political and Social Science 403, 1-11 (1972).

By the 1990s, the strategic logic of MNCs began to shift.71Narula, R. Multinational firms and the extractive sectors in the 21st century: Can they drive development? Journal of World Business 53, 85-91 (2018). https://doi.org/10.1016/j.jwb.2017.09.004 New firms from emerging markets entered the global arena, not to exploit existing FSAs, but to acquire them. The new multinationals often pursued rapid internationalization through acquisitions, alliances and non-equity arrangements, circumventing the gradual, experience-based models of earlier decades.62Guillen, M. & García-Canal, E. The American Model of the Multinational Firm and the “New” Multinationals From Emerging Economies. Academy of Management Perspectives 23, 23-35 (2009). https://doi.org/10.5465/AMP.2009.39985538,66Dymsza, W. A. Trends in Multinational Business and Global Environments: A Perspective. Journal of International Business Studies 15, 25-46 (1984). https://doi.org/10.1057/palgrave.jibs.8490493 Organizationally, MNCs moved away from strict hierarchical control toward networked governance structures, managing complex webs of subsidiaries, suppliers and partners.71Narula, R. Multinational firms and the extractive sectors in the 21st century: Can they drive development? Journal of World Business 53, 85-91 (2018). https://doi.org/10.1016/j.jwb.2017.09.004,72Narula, R. & Verbeke, A. Making internalization theory good for practice: The essence of Alan Rugman’s contributions to international business. Journal of World Business 50, 612-622 (2015). https://doi.org/10.1016/j.jwb.2015.08.007 The 21st century has further intensified this transformation. MNCs are now deeply embedded in global production, finance and innovation systems. For example, MNCs accounted for over 80 percent of industrial R&D in the United States inn.201777 However, their growing complexity and reach have made MNCs targets of increasing scrutiny, not only in terms of economic power but also with regard to their social and environmental impact. Concerns about corporate accountability, inequality and global externalities have reshaped public expectations of MNC conduct and fueled calls for more responsible global business practices.71Narula, R. Multinational firms and the extractive sectors in the 21st century: Can they drive development? Journal of World Business 53, 85-91 (2018). https://doi.org/10.1016/j.jwb.2017.09.004,73Foley, C. F., Hines, J. R. & Wessel, D. Global Goliaths: Multinational Corporations in the 21st Century Economy. (Brookings Institution Press, 2021).

Since the 2010s, MNCs have operated in an increasingly complex strategic environment, shaped by new pressures for environmental and social accountability. Even before the COVID-19 pandemic, many firms began reevaluating the efficiency-driven logic of global supply chains in light of growing expectations regarding corporate sustainability.71Narula, R. Multinational firms and the extractive sectors in the 21st century: Can they drive development? Journal of World Business 53, 85-91 (2018). https://doi.org/10.1016/j.jwb.2017.09.004 The pandemic further exposed systemic vulnerabilities in global production systems and accelerated a shift toward regionalization, resilience-based design and dual sourcing strategies.73Foley, C. F., Hines, J. R. & Wessel, D. Global Goliaths: Multinational Corporations in the 21st Century Economy. (Brookings Institution Press, 2021). Simultaneously, corporate sustainability has evolved from a peripheral or reputational issue to a core strategic capability. In resource-intensive sectors such as mining and energy, the ability to demonstrate environmental and social responsibility now constitutes a higher-order ownership advantage, shaping access to markets, licenses and capital.71Narula, R. Multinational firms and the extractive sectors in the 21st century: Can they drive development? Journal of World Business 53, 85-91 (2018). https://doi.org/10.1016/j.jwb.2017.09.004 In parallel, the institutional environment has undergone a significant transformation. MNCs are increasingly expected to assume quasi-regulatory roles, particularly in regions where state governance is weak or fragmented, by enforcing labor standards, ensuring environmental compliance and promoting transparency throughout global value chains.74Verbeke, A., Oh, C. H. & Jain, R. What is the future of regional multinational enterprises? International Business Review 34 (2025). https://doi.org/10.1016/j.ibusrev.2025.102442

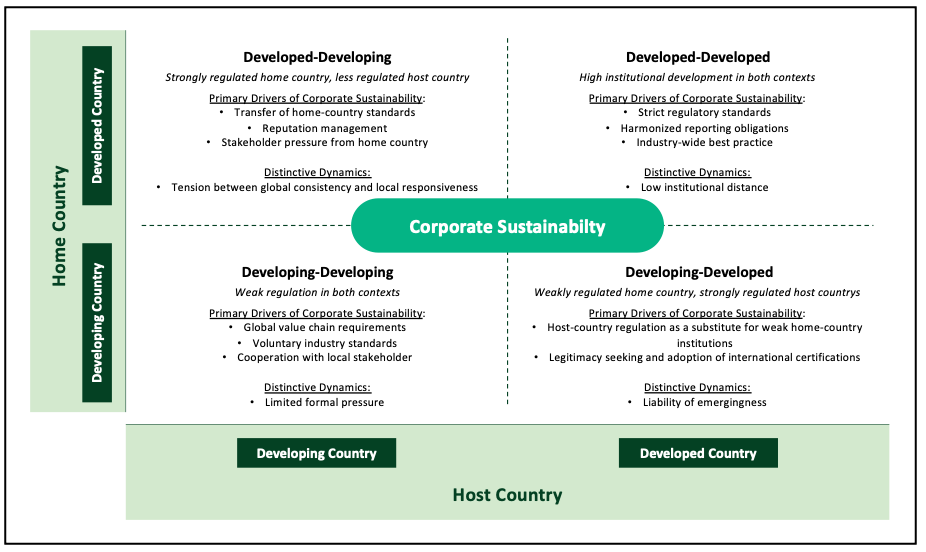

By the mid-2010s, a deeper shift in how MNCs are perceived and assessed had become increasingly evident. Beyond their economic footprint, MNCs are now also evaluated on their ability to address global challenges through environmental, social and governance (ESG) integration.75Kolk, A., Kourula, A. & Pisani, N. Multinational enterprises and the sustainable development goals: What do we know and how to proceed? Transnational Corporations 24, 9-32 (2017).,76Munro, V. & Arli, D. Corporate sustainable actions through United Nations sustainable development goals: The internal customer’s response. International Journal of Nonprofit and Voluntary Sector Marketing 25 (2020). https://doi.org/10.1002/nvsm.1660 Normative frameworks such as the United Nations Sustainable Development Goals (SDGs) have emerged as central benchmarks, shaping not only how firms disclose sustainability efforts but also how they define legitimacy and long-term strategic value.77Ivanaj, S., Ivanaj, V., McIntyre, J. & Guimaraes da Costa, N. What can multinational enterprises do to implement sustainable development goals? Journal of Cleaner Production 296 (2021). https://doi.org/10.1016/j.jclepro.2021.126586 In this evolving context, MNCs’ internationalization strategies are increasingly driven not only by economic opportunity, but also by the need to respond to institutional complexity, reputational risk and increasing public scrutiny.78Nasta, L. & Cundari, V. Aligning multinational corporate strategies with Sustainable Development Goals: A case study of an Italian energy firm’s initiatives in developing markets. Corporate Social Responsibility and Environmental Management 31, 3902-3915 (2024). https://doi.org/10.1002/csr.2779 While normative frameworks such as the SDGs have begun to influence the way companies shape their global expansion, the actual integration of social legitimacy, environmental responsibility and political accountability into cross-border operations remains uneven and subject to significant variation across sectors and institutional contexts.74Verbeke, A., Oh, C. H. & Jain, R. What is the future of regional multinational enterprises? International Business Review 34 (2025). https://doi.org/10.1016/j.ibusrev.2025.102442,77Ivanaj, S., Ivanaj, V., McIntyre, J. & Guimaraes da Costa, N. What can multinational enterprises do to implement sustainable development goals? Journal of Cleaner Production 296 (2021). https://doi.org/10.1016/j.jclepro.2021.126586 China illustrates this duality well. As the world’s largest developing country, it has not only become one of the central host markets for foreign MNCs but also has emerged, alongside the Unites States, as a leading home country of MNCs. This paradox underscores the rise of a developing country to the forefront of global corporate power while continuing to face severe sustainability challenges.17D’Souza, C. et al. An empirical examination of sustainability for multinational firms in China: Implications for cleaner production. Journal of Cleaner Production 242 (2020). https://doi.org/10.1016/j.jclepro.2019.118446

Between 2013 and 2019, longitudinal case evidence illustrates a transformation in the way MNCs operationalize sustainability within their global structures. Firms moved from maintaining isolated CSR departments to embedding sustainability responsibilities across core functions. This shift was accompanied by a gradual transition from predominantly top-down governance towards more participatory approaches, enabling employees to act as internal sustainability ambassadors. In addition to traditional climate and energy targets, new thematic areas such as plastic reduction, waste management and product reformulation gained relevance.49Derqui, B. Towards sustainable development: Evolution of corporate sustainability in multinational firms. Corporate Social Responsibility and Environmental Management 27, 2712-2723 (2020). https://doi.org/10.1002/csr.1995

At the same time, these shifts unfold within a broader debate about the future of globalization.79Temouri, Y., Pereira, V., Delis, A. & Wood, G. How Does Protectionism Impact Multinational Firm Reshoring? Evidence from the UK. Management International Review 63, 791-822 (2023). https://doi.org/10.1007/s11575-023-00521-5 Although narratives of deglobalization have gained visibility in political discourse, recent empirical research suggests that MNCs remain resilient and adaptive global actors. Rather than reversing internationalization, MNCs are responding to geopolitical, environmental and institutional pressures through strategic reconfiguration. Cross-border trade and investment flows remain robust and firms increasingly rely on multisourcing and regional diversification models to maintain operational resilience without abandoning their multinational reach.80Altman, S. A., Bastian, C. R. & Fattedad, D. Challenging the deglobalization narrative: Global flows have remained resilient through successive shocks. Journal of International Business Policy 7, 416-439 (2024). https://doi.org/10.1057/s42214-024-00197-0,81Yücesan, E. Does deglobalization imply the end of global supply chains? International Business Review (2025). https://doi.org/10.1016/j.ibusrev.2025.102398 While isolated reshoring activities have occurred, they remain selective and tied to specific operational contexts. Overall, MNCs continue to pursue internationalization through adjusted, but sustained, forms of global engagement.79Temouri, Y., Pereira, V., Delis, A. & Wood, G. How Does Protectionism Impact Multinational Firm Reshoring? Evidence from the UK. Management International Review 63, 791-822 (2023). https://doi.org/10.1007/s11575-023-00521-5,81Yücesan, E. Does deglobalization imply the end of global supply chains? International Business Review (2025). https://doi.org/10.1016/j.ibusrev.2025.102398

2.2.2 Evolution of research on multinationals and corporate sustainability

Multinational companies began to attract serious academic attention as a distinct organizational form in the early 1960s. Prior to this, their activities were mostly subsumed under the study of international capital flows. The work of Hymermarked a conceptual shift by positioning the MNC as a subject that required its own theoretical framework.82Hymer, S. H. The international operations of national firms, a study of direct foreign investment, Massachusetts Institute of Technology, (1960).,83Dunning, J. H. & Pitelis, C. N. Stephen Hymer’s Contribution to International Business Scholarship: An Assessment and Extension. Journal of International Business Studies 39, 167-176 (2008).,84Aharoni, Y. & Ramamurti, R. in Standing on the Shoulders of International Business Giants 153-177 (2011). In the late 1960s, the first major empirical study on U.S. MNCs, conducted at Harvard Business School, defined multinationalism primarily through offshore manufacturing. This narrow understanding became standard in the international management literature. However, as firms began to internationalize through a wider range of activities beyond production, scholars increasingly questioned this production-centric definition, which ultimately triggered a rethinking of how MNCs were to be conceptualized in academic research.33Ghoshal, S. & Westney, D. E. in Organization Theory and the Multinational Corporation (eds Sumantra Ghoshal & D. Eleanor Westney) 1-23 (Palgrave Macmillan UK, 1993).

Throughout the 1970s and 1980s, economic and strategic models dominated the study of MNCs. Central among them was Dunning’s eclectic paradigm, which sought to explain international expansion through a combination of ownership, location and internationalization advantages (OLI; also known as OLI model or OLI framework).85Dunning, J. H. Toward an Eclectic Theory of International Production: Some Empirical Tests. Journal of International Business Studies 11, 9-31 (1980). https://doi.org/10.1057/palgrave.jibs.8490593,86Dunning, J. H. The Eclectic Paradigm of International Production: A Restatement and Some Possible Extensions. Journal of International Business Studies 19, 1-31 (1988). This perspective treated internationalization as a means to exploit home-based firm-specific advantages, such as superior technology or firm-specific assets, particularly in order to overcome the liability of foreignness.82Hymer, S. H. The international operations of national firms, a study of direct foreign investment, Massachusetts Institute of Technology, (1960).,87Rugman, A. M. Inside the multinationals : the economics of internal markets / Alan M. Rugman. (Croom Helm, 1981).,88Dunning, J. H. in The International Allocation of Economic Activity: Proceedings of a Nobel Symposium held at Stockholm (eds Bertil Ohlin, Per-Ove Hesselborn, & Per Magnus Wijkman) 395-418 (Palgrave Macmillan UK, 1977). While these foundational contributions acknowledged the institutional challenges of foreign operations, analytical attention remained focused on efficiency and competitive positioning, with comparatively little regard for the internal complexity and functional heterogeneity of foreign subsidiaries.89Papanastassiou, M., Pearce, R. & Zanfei, A. Changing perspectives on the internationalization of R&D and innovation by multinational enterprises: A review of the literature. Journal of International Business Studies 51, 623-664 (2020). https://doi.org/10.1057/s41267-019-00258-0

From the 1990s onwards, academic research on MNCs began to critically reassess the limitations of earlier efficiency-focused models and introduced new analytical dimensions to account for the complexity of globally operating firms.89Papanastassiou, M., Pearce, R. & Zanfei, A. Changing perspectives on the internationalization of R&D and innovation by multinational enterprises: A review of the literature. Journal of International Business Studies 51, 623-664 (2020). https://doi.org/10.1057/s41267-019-00258-0,90Roth, K. & Kostova, T. The Use of the Multinational Corporation as a Research Context. Journal of Management29, 883-902 (2003). https://doi.org/10.1016/s0149-2063_03_00083-7,91Holm, D. et al. Vol. 4 3-20 (2009). Scholars increasingly began to reconceptualize MNCs as networks embedded in complex international environments, where coordination, learning and institutional negotiation became central analytical.84Aharoni, Y. & Ramamurti, R. in Standing on the Shoulders of International Business Giants 153-177 (2011). This shift in perspective led to a growing interest in how MNCs integrate dispersed knowledge, manage cross-border uncertainty and evolve under the influence of technological change, political fragmentation and global competition. As a result, MNC research expanded its disciplinary heterogeneity, strategic agility and the institutional embeddedness of international operations.84Aharoni, Y. & Ramamurti, R. in Standing on the Shoulders of International Business Giants 153-177 (2011).,90Roth, K. & Kostova, T. The Use of the Multinational Corporation as a Research Context. Journal of Management29, 883-902 (2003). https://doi.org/10.1016/s0149-2063_03_00083-7

Beginning the early 2000s, corporate sustainability increasingly entered the international business literature, as scholars started to examine how MNCs address environmental and social challenges in an increasingly complex global context.92Christmann, P. Multinational Companies and the Natural Environment: Determinants of Global Environmental Policy. Academy of Management Journal 47, 747-760 (2004). https://doi.org/10.5465/20159616 This development was partly driven by the recognition that while industrial capitalism, globalization and MNCs have been major contributors to global environmental challenges, MNCs also hold significant potential to help address and mitigate these sustainability issues.4Ocelík, V., Kolk, A. & Ciulli, F. Multinational enterprises, Industry 4.0 and sustainability: A multidisciplinary review and research agenda. Journal of Cleaner Production 413 (2023). https://doi.org/10.1016/j.jclepro.2023.137434,93Wright, C. & Nyberg, D. Climate Change, Capitalism, and Corporations: Processes of Creative Self-Destruction. (Cambridge University Press, 2015).,94McNeill, J. R. Something New under the Sun: An Environmental History of the Twentieth-Century World. (W. W. Norton, 2000). The role of MNCs as agents of change became an increasingly central debate around SD, particularly as stakeholders and policymakers began demanding greater accountability and transparency from globally operating firms.4Ocelík, V., Kolk, A. & Ciulli, F. Multinational enterprises, Industry 4.0 and sustainability: A multidisciplinary review and research agenda. Journal of Cleaner Production 413 (2023). https://doi.org/10.1016/j.jclepro.2023.137434,95Sun, P., Doh, J. P., Rajwani, T. & Siegel, D. Navigating cross-border institutional complexity: A review and assessment of multinational nonmarket strategy research. J Int Bus Stud 52, 1818-1853 (2021). https://doi.org/10.1057/s41267-021-00438-x,96Torres de Oliveira, R., Ghobakhloo, M. & Figueira, S. Industry 4.0 towards social and environmental sustainability in multinationals: Enabling circular economy, organizational social practices, and corporate purpose. Journal of Cleaner Production 430 (2023). https://doi.org/10.1016/j.jclepro.2023.139712

From the 2010s onwards, CS research focused more and more on how MNCs integrate sustainability into core business functions and strategic planning, moving beyond peripheral CSR departments towards organization-wide transformation.49Derqui, B. Towards sustainable development: Evolution of corporate sustainability in multinational firms. Corporate Social Responsibility and Environmental Management 27, 2712-2723 (2020). https://doi.org/10.1002/csr.1995,97Asmussen, C. G. & Fosfuri, A. Orchestrating corporate social responsibility in the multinational enterprise. Strategic Management Journal 40, 894-916 (2019). https://doi.org/10.1002/smj.3007 Studies began to document that sustainability was no longer considered a matter of ethical responsibility alone but became a central component of competitive advantage and brand strategy.98Schaltegger, S. Sustainability as a driver for corporate economic success. Society and Economy 33, 15-28 (2011). https://doi.org/10.1556/SocEc.33.2011.1.4,99Kiron, D. et al. Corporate sustainability at a crossroads: Progress toward our common future in uncertain times. MIT Sloan Management Review (2017). The global institutionalization of sustainability, marked by frameworks such as the UN Global Compact and the Sustainable Development Goals, has led researcher to increasingly examine how MNCs operationalize sustainability in line with global norms while addressing local variations in regulatory and stakeholder expectations.78Nasta, L. & Cundari, V. Aligning multinational corporate strategies with Sustainable Development Goals: A case study of an Italian energy firm’s initiatives in developing markets. Corporate Social Responsibility and Environmental Management 31, 3902-3915 (2024). https://doi.org/10.1002/csr.2779,100Park, J., Cuervo-Cazurra, A. & Montiel, I. in Research Handbook on International Corporate Social Responsibility (ed Anthony Goerzen) Ch. 2, (Edward Elgar Publishing Limited, 2023). Taken together, these developments reflect an ongoing scholarly interest in understanding how MNCs balance the pursuit of global sustainability objectives with the realities of operational complexity, institutional diversity and stakeholder fragmentation.

2.3 Foundations of multinationals’ corporate sustainability

This thesis applies a conceptual framework of Drivers and Outcomes to systematically review the academic literature on CS in MNCs. This framework provides a structured lens to investigate both the underlying forces that shape MNC engagement with sustainability and the tangible results that arise from such strategic orientation. Drivers refer to the internal and external factors that initiate or institutionalize sustainability-related behavior within MNCs. Outcomes denote the observable consequences of sustainability-oriented corporate strategies and practices.

2.3.1 Internal drivers of multinationals’ corporate sustainability

2.3.1.1 Organizational structure and strategies

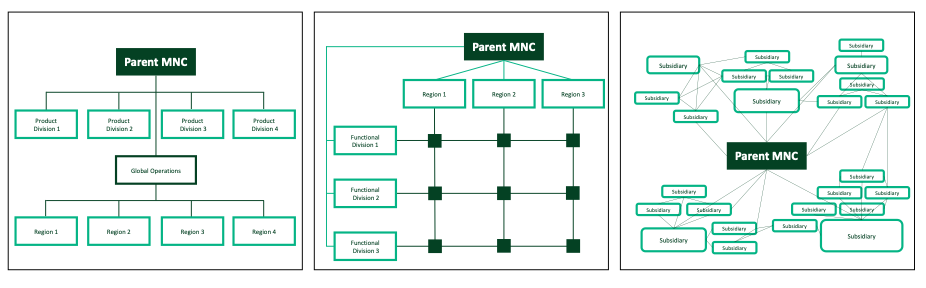

MNCs operate across multiple institutional, cultural and economic environments, requiring organizational structures that can effectively coordinate dispersed units while balancing global efficiency and local responsiveness.41Meyer, K. E., Li, C. & Schotter, A. P. J. Managing the MNE subsidiary: Advancing a multi-level and dynamic research agenda. Journal of International Business Studies 51, 538-576 (2020). https://doi.org/10.1057/s41267-020-00318-w,101Raziq, M. M., Benito, G. R. G. & Kang, Y. Multinational Enterprise Organizational Structures and Subsidiary Role and Capability Development: The Moderating Role of Establishment Mode. Group & Organization Management 48, 908-952 (2023). https://doi.org/10.1177/10596011211060952 These structural arrangements are particularly relevant in the context of CS, as they shape the ways in which sustainability goals are formulated at the headquarters level and subsequently translated or adapted across diverse subsidiary contexts.3Burritt, R. L., Christ, K. L., Rammal, H. G. & Schaltegger, S. Multinational Enterprise Strategies for Addressing Sustainability: the Need for Consolidation. Journal of Business Ethics 164, 389-410 (2020). https://doi.org/10.1007/s10551-018-4066-0 In order to understand how internal factors such as strategic orientations and headquarters-subsidiary relations may act as drivers of CS in MNCs, it is necessary to first examine the structural configurations through which MNCs typically organize their international operations. The structure of a MNC determines not only how decision-making authority is distributed across units but also how knowledge, resources and responsibilities are coordinated across geographical and functional boundaries.101Raziq, M. M., Benito, G. R. G. & Kang, Y. Multinational Enterprise Organizational Structures and Subsidiary Role and Capability Development: The Moderating Role of Establishment Mode. Group & Organization Management 48, 908-952 (2023). https://doi.org/10.1177/10596011211060952,102Dasí, À., Pedersen, T. & Pla-Barber, J. MNCs’ Intermediate Units and Their Choice of Control Mechanisms. Management International Review 64, 59-88 (2024). https://doi.org/10.1007/s11575-023-00527-z

Among the formal structural types identified in the literature, the regional division structure is one of the most prevalent in MNCs. In this configuration, subsidiaries are grouped into broad geographical regions, each managed by a regional headquarters with responsibility for the operations within its designated area.103Celo, S., Nebus, J. & Kim Wang, I. MNC structure, complexity, and performance: Insights from NK methodology. Journal of International Management 21, 182-199 (2015). https://doi.org/10.1016/j.intman.2015.06.002 The regional headquarters (RHQ) serves as an intermediary between the global corporate center and the local subsidiaries, facilitating context-sensitive decision-making while maintaining strategic alignment. This structure is particularly effective when market and institutional conditions vary significantly across regions, as it enables MNCs to benefit from localized adaptation while retaining control over overarching corporate objectives.103Celo, S., Nebus, J. & Kim Wang, I. MNC structure, complexity, and performance: Insights from NK methodology. Journal of International Management 21, 182-199 (2015). https://doi.org/10.1016/j.intman.2015.06.002,104Egelhoff, W. G. Strategy and Structure in Multinational Corporations: An Information- Processing Approach. Administrative Science Quarterly 27, 435-458 (1982). https://doi.org/10.2307/2392321,105Egelhoff, W. G. Organizing the multinational enterprise : an information-processing perspective. (Ballinger Pub. Co., 1988).

A second widely adopted model is the matrix structure, which combines two or more organizational dimensions, typically geography, product or function, into a dual-reporting framework.103Celo, S., Nebus, J. & Kim Wang, I. MNC structure, complexity, and performance: Insights from NK methodology. Journal of International Management 21, 182-199 (2015). https://doi.org/10.1016/j.intman.2015.06.002 Subsidiaries in matrix-configured MNCs often report simultaneously to regional managers and product or functional leaders, reflecting the dual imperative of global integration and local responsiveness. Although matrix structures aim to enhance flexibility and cross-functional coordination, they are frequently associated with high internal complexity, increased coordination costs and managerial ambiguity.103Celo, S., Nebus, J. & Kim Wang, I. MNC structure, complexity, and performance: Insights from NK methodology. Journal of International Management 21, 182-199 (2015). https://doi.org/10.1016/j.intman.2015.06.002,106Egelhoff, W. G. How a Flexible Matrix Structure Could Create Ambidexterity at the Macro Level of Large, Complex Organizations Like MNCs. MIR: Management International Review 60, 459-484 (2020). https://doi.org/10.1007/s11575-020-00418-7 Despite these challenges, matrix designs continue to be used in MNCs that operate in complex, interdependent environments where multiple strategic logistics must be balanced simultaneously.107Egelhoff, W. G. & Wolf, J. in Understanding Matrix Structures and their Alternatives: The Key to Designing and Managing Large, Complex Organizations (eds William G. Egelhoff & Joachim Wolf) 75-108 (Palgrave Macmillan UK, 2017).,108Wolf, J. & Egelhoff, W. G. in Collaborative Communities of Firms: Purpose, Process, and Design (eds Anne Bøllingtoft et al.) 35-57 (Springer New York, 2012).

Beyond these formal hierarchies, network-based structures have gained prominence as flexible alternatives in global operations.103Celo, S., Nebus, J. & Kim Wang, I. MNC structure, complexity, and performance: Insights from NK methodology. Journal of International Management 21, 182-199 (2015). https://doi.org/10.1016/j.intman.2015.06.002 These configurations are characterized by decentralized decision-making, non-hierarchical coordination and the use of informal mechanisms such as trust, shared norms and lateral knowledge exchange.108Wolf, J. & Egelhoff, W. G. in Collaborative Communities of Firms: Purpose, Process, and Design (eds Anne Bøllingtoft et al.) 35-57 (Springer New York, 2012). In such settings, subsidiaries may act as autonomous nodes within a larger network, enabling responsiveness and innovation while reducing reliance on central control. However, the effectiveness of network structures depends heavily on the willingness and ability of individual units to share information and align with broader strategic goals.109Malnight, T. W. The Transition from Decentralized to Network-Based MNC Structures: An Evolutionary Perspective. Journal of International Business Studies 27, 43-65 (1996). https://doi.org/10.1057/palgrave.jibs.8490125,110Wolf, J. & Egelhoff, W. G. in Reshaping the Boundaries of the Firm in an Era of Global Interdependence Vol. 5 (eds José Pla-Barber & Joaquín Alegre) 0 (Emerald Group Publishing Limited, 2010).

While organizational structures provide the formal scaffolding for managing complexity in MNCs, the HQ-subsidiary relationship also influences the internal capacity to initiate, coordinate and embed CS across geographies.112Kostova, T., Marano, V. & Tallman, S. Headquarters–subsidiary relationships in MNCs: Fifty years of evolving research. Journal of World Business 51, 176-184 (2016). https://doi.org/10.1016/j.jwb.2015.09.003,113Mahnke, V., Ambos, B., Nell, P. C. & Hobdari, B. How do regional headquarters influence corporate decisions in networked MNCs? Journal of International Management 18, 293-301 (2012). https://doi.org/10.1016/j.intman.2012.04.001 Structural configurations shape not only how sustainability strategies are disseminated from the parent MNC to regional and local units, but also how subsidiaries can contribute to sustainability through localized knowledge and context-sensitive implementation.114Jamali, D., Makarem, Y. & Willi, A. From diffusion to translation: implementation of CSR practices in MNC subsidiaries. Social Responsibility Journal 16, 309-327 (2019). https://doi.org/10.1108/srj-05-2018-0108 In regional division structures, the existence of intermediary RHQs can enable MNCs to balance CS objectives with regional contextual demands. Where RHQs are endowed with strategic autonomy and operate within an advanced, entrepreneurial governance framework, they may actively contribute to the development and implementation of sustainability initiatives.115Nachbagauer, A. Stimulating Sustainability in Multinational Companies: the Significance of Regional Headquarters. Management Dynamics in the Knowledge Economy 4, 215-214 (2016).,116Conroy, K., Gammelgaard, J. & Jooss, S. Operating in the middle-power position: Conceptualising the role of regional headquarters through loaned and owned power. International Business Review 32 (2023). https://doi.org/10.1016/j.ibusrev.2023.102161 These settings allow sustainability to be tailored to local institutional environments while remaining aligned with global goals. However, the effectiveness of RHQs as sustainability drivers depends on their structural authority, integration with corporate-level sustainability agendas and access to relevant resources.115Nachbagauer, A. Stimulating Sustainability in Multinational Companies: the Significance of Regional Headquarters. Management Dynamics in the Knowledge Economy 4, 215-214 (2016).,117Ambos, B. & Schlegelmilch, B. B. The New Role of Regional Management. 1 edn, (Palgrave Macmillan, 2009).

Matrix structures can support CS when coordination across product, regional and functional dimensions is well-managed and strategically aligned. Their potential lies in enabling both global standardization and local adaptation.108Wolf, J. & Egelhoff, W. G. in Collaborative Communities of Firms: Purpose, Process, and Design (eds Anne Bøllingtoft et al.) 35-57 (Springer New York, 2012). However, high internal complexity, role ambiguity and inter-unit conflict often impede sustainability integration.115Nachbagauer, A. Stimulating Sustainability in Multinational Companies: the Significance of Regional Headquarters. Management Dynamics in the Knowledge Economy 4, 215-214 (2016).,117Ambos, B. & Schlegelmilch, B. B. The New Role of Regional Management. 1 edn, (Palgrave Macmillan, 2009). Thus, matrix structures act as drivers of CS only if supported by clear accountability, strong sustainability governance and shared organizational priorities.